|

市場調查報告書

商品編碼

2072614

企業級VSAT系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Enterprise VSAT System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

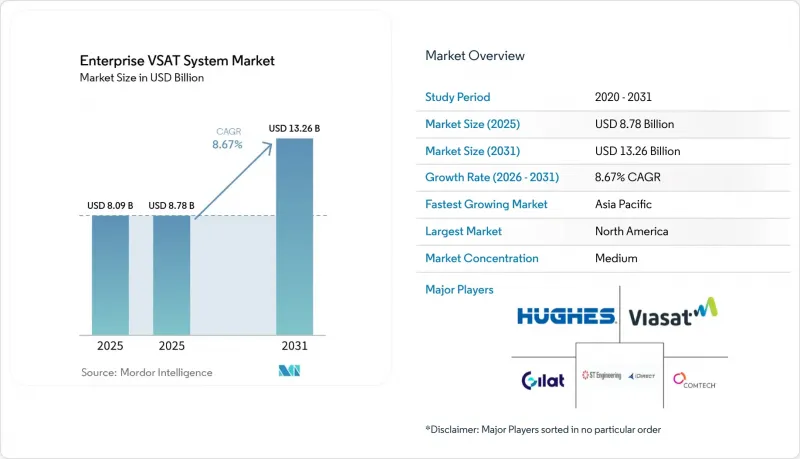

根據 Mordor Intelligence 預測,企業級 VSAT 系統市場預計將從 2025 年的 80.9 億美元成長到 2026 年的 87.8 億美元,到 2031 年達到 132.6 億美元,2026 年至 2031 年的複合年成長率為 8.67%。

本報告按組件(硬體和服務)、平台規模(小型地球站、中型地球站、大型地球站)、頻段(Ku波段、C波段、 Ka波段等)、終端用戶產業(石油天然氣、航運、政府和國防、銀行和金融服務、電信和IT、採礦等)以及地區進行細分。市場預測以美元計價。

全球企業級VSAT系統市場趨勢與洞察

偏遠地區和離岸地區對寬頻連線的需求激增。

目前,海上鑽井、遠端採礦和遠洋航行等作業需要對稱、低延遲的通訊線路,而光纖或行動電話網路通常無法滿足這些需求。巴西石油公司(Petrobras)的子公司Transpetro於2025年初完成了26艘船舶的混合VSAT和Starlink升級,透過最佳化航線實現了3-5%的燃油節省。 Movistar Argentina報告稱,截至2026年2月,瓦卡穆埃爾塔頁岩區承包商的衛星通訊合約年增了40%。 Interioran指出,該行業傾向於過度配置設備以避免代價高昂的停機時間,例如在馬來西亞國家石油公司(Petronas)的浮體式液化天然氣(LNG)設施上部署三重冗餘終端。國際電信聯盟(ITU)的無線電法律規範簡化了許可程序,使得新的企業級VSAT系統無需冗長的核准流程即可擴展。

數位化油田和智慧航運計劃正在加速VSAT技術的應用。

隨著鑽井專案和數據驅動型船隊營運中感測器應用的日益廣泛,連接性正逐漸成為提升生產效率的關鍵因素。新加坡科技工程公司(ST Engineering)旗下的iDirect公司與stc Solutions合作,正在沙烏地阿拉伯900億美元的數位經濟舉措下,對油井和煉油廠進行監控。 SES和Viasat Energy已在亞太地區的近海平台部署了低於150毫秒的延遲服務,實現了對機器人的即時控制。太平洋盆地航運公司(Pacific Basin)和商船三井(Mitsui OSK Lines)等航運公司已於2025年完成與NexusWave的合作系統維修,以符合國際海事組織(IMO)的網路安全準則,並將非計畫進塢維修減少高達30%。企業級VSAT系統市場正從中受益,因為相關人員現在不再僅僅將頻寬視為營運成本,而是將其視為提升效能的手段。

與地面通訊方式相比,資本投資(Capex)和營運成本(Opex)較高。

在光纖和5G網路覆蓋的地區,VSAT硬體、安裝成本和衛星通訊營運成本仍然優於地面通訊方式。 2024年,由於零件短缺,砷化鎵(GaAs)低雜訊放大器(LNA)的價格從28.50美元飆升至175美元。根據公開數據,Comtec和KVH分別報告了1.3624億美元和3096萬美元的季度營運支出,凸顯了全天候網路營運帶來的固定成本負擔。雖然遠端用戶可以接受更高的價格,但都市區企業正在仔細權衡經濟效益,這阻礙了企業級VSAT系統的廣泛應用。

細分市場分析

到2025年,託管服務將超越硬體,複合年成長率(CAGR)將達到9.98%,而硬體仍將佔據大部分收入,這主要歸因於初始終端採購。隨著企業將頻寬、網路安全和合規性納入營運支出(OPEX),透過服務合約實現的企業級VSAT系統市場規模正在擴大。 L3Harris和Comtech的5650C2/MP調變解調器簡化了多軌道漫遊,並降低了內部技術需求。供應商現在將編配、安裝和工單管理入口網站捆綁在一起,競爭的重點也從標價轉向了總擁有成本(TCO)。整合商正在利用大容量合約來保護客戶頻寬波動的影響,並增強經常性收入來源。硬體創新仍在繼續,例如Hughes的HM400機載調變解調器瞄準了ISR(資訊、監視和偵察)飛機,但產品發布擴大成為簽訂長期服務合約的切入點。

因此,企業級VSAT系統市場反映了更廣泛的IT外包趨勢。企業傾向於整合供應商,並透過單一聯繫點集中負責運作SLA。為此,供應商正在收購區域安裝商並投資建造網路營運中心,以縮短部署時間並實現跨區域的標準化支援。隨著服務組合的日趨成熟,差異化的關鍵在於網路安全增強功能和將衛星鏈路整合到DevOps工具鏈中的API存取。

中型地面站(1.2-2.4公尺)在增益和成本之間取得了良好的平衡,預計到2025年將佔據45.67%的市場佔有率。小型終端(小於1.2米)正以9.63%的複合年成長率快速成長,這得益於無需機械萬向節且可嵌入式安裝在甲板或車輛上的電子控制天線陣列。隨著海事和國防客戶優先考慮降低風阻、加快安裝速度和降低維護成本,企業級VSAT系統緊湊型天線市場正在成長。 Orbit公司的「OrBeam MIL」和Egatel公司的改裝面板就是能夠無縫整合到現有數據機生態系統中的典型產品,最大限度地減少了更換的負擔。

雖然大型隱形拋物面天線對於閘道器和頻寬樞紐仍然至關重要,但企業的需求正轉向支援移動性的外形規格。休斯和QEST的相位陣列將於2024年展示多衛星追蹤功能,預示未來單一面板即可覆蓋地球同步軌道(GEO)、中地球軌道(MEO)和低地球軌道(LEO)網路。這種架構增強了鏈路容錯能力,同時節省了在空間有限的船舶桅杆上的安裝空間。

區域分析

受國防採購和頁岩氣開發的推動,北美地區預計在2025年將佔總收入的34.56%,但都市區光纖和5G網路的飽和限制了其進一步成長。 Viasat的Ka波段一體化服務透過解決加拿大、美國和墨西哥之間的跨境合約摩擦,加速了區域部署。美國國防部在2025年至2026年間授予Gillatt和L3 Harris的多份合約凸顯了衛星冗餘的戰略價值。

亞太地區是成長最快的地區,預計複合年成長率將達到8.78%。印度、印尼和馬來西亞的國有石油公司正在將位於陸地通訊無法涵蓋地區的資產數位化。 SES公司的O3b mPOWER低延遲鏈路支援水下機器人的運作和即時資料共用,而太平洋盆地和商船三井已為其所有船隊配備了符合國際海事組織(IMO)網路安全法規的設備。印尼的BRIsat公司正在展示其銀行網路如何利用國內衛星覆蓋偏遠島嶼。

儘管歐洲的光纖網路限制了衛星通訊的廣泛應用,但北海石油鑽井平台、波羅的海航道和國防機動等特定應用場景正在推動其成長。電訊(ITU)公開譴責跨界破壞活動,凸顯了衛星資產在歐洲大陸的地緣政治敏感性。在中東,沙烏地阿拉伯的數位經濟願景正透過本地通訊業者與全球數據機供應商的合作,推動全國範圍內的衛星部署。阿曼衛星公司(OmanSat)的軟體定義衛星、EshailSat在北非的擴張以及歐洲通訊衛星公司(Eutelsat)在象牙海岸共和國的「KONNECT」計畫都表明,新興經濟體將衛星視為實現「全民寬頻」的最快途徑。

在南美洲,巴西的鹽鹽層下資源和阿根廷的頁岩氣革命正在推動市場發展。巴西國家電信管理局(Anatel)於2026年3月批准的許可證將使Viasat能夠覆蓋巴西全境,而Transpetro混合終端的初步成功也證明了燃料成本的實際降低。非洲仍然是一個尚未開發的市場,滲透率較低。儘管與MTN象牙海岸共和國和Eutelsat等公司簽訂的容量合約前景可觀,但監管分散和購買力有限正在減緩企業級VSAT系統市場的短期成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 偏遠和離岸地區對寬頻連線的需求激增。

- 數位化油田和智慧航運計劃正在加速VSAT技術的應用。

- 透過擴展高通量衛星星系來降低頻寬成本

- 需要始終保持線上連線的雲端企業應用程式的成長。

- 平板電子控制天線的出現,減少了安裝空間。

- 5G 非地面電波網路標準的廣泛採用將使企業級服務類別成為可能。

- 市場限制因素

- 與地面電波廣播相比,資本支出和營運支出更高。

- 主要頻段的頻率擁擠和許可壁壘

- 針對衛星地面段的網路攻擊加劇

- 地緣政治摩擦下射頻元件供應鏈所面臨的風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 服務

- 按平台大小

- 小型地面站(小於1.2公尺)

- 中型地面站(1.2-2.4公尺)

- 大型地面站(超過 2.4 公尺)

- 按頻段

- Ku波段

- C波段

- Ka波段

- 其他頻段

- 按最終用戶行業分類

- 石油和天然氣

- 海上

- 政府/國防

- 銀行和金融服務

- 通訊/IT

- 礦業

- 能源公用事業

- 零售

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Hughes Network Systems LLC

- ViaSat Inc.

- Gilat Satellite Networks Ltd.

- Comtech Telecommunications Corp.

- ST Engineering iDirect

- Newtec

- ND SatCom GmbH

- KVH Industries Inc.

- Signalhorn Trusted Networks GmbH

- CPI International Inc.

- Advantech Wireless Technologies Inc.

- Paradise Datacom LLC

- Satpro M&C Tech Co. Ltd.

- Intellian Technologies Inc.

- Isotropic Systems Ltd.

- Elbit Systems Ltd.

- L3Harris Technologies Inc.

- Ultra Electronics Antennas Group

- Satcom Direct Inc.

- Cobham Satcom

第7章 市場機會與未來展望

According to Mordor Intelligence, the enterprise VSAT system market size is expected to increase from USD 8.09 billion in 2025 to USD 8.78 billion in 2026 and reach USD 13.26 billion by 2031, growing at a CAGR of 8.67% over 2026-2031.

This report is Segmented by Component (Hardware and Services), Platform Size (Small Earth Station, Medium Earth Station, and Large Earth Station), Frequency Band (Ku-Band, C-Band, Ka-Band and More), End-User Industry (Oil and Gas, Maritime, Government and Defense, Banking and Financial Services, Telecom and IT, Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise VSAT System Market Trends and Insights

Surging Demand for Broadband Connectivity in Remote and Offshore Sites

Operations in offshore drilling, remote mining, and blue-water shipping now demand symmetric, low-latency links that fiber and cellular often cannot deliver. Petrobras subsidiary Transpetro completed hybrid VSAT and Starlink upgrades across 26 vessels in early 2025, achieving 3-5% fuel savings through optimized routing. Movistar Argentina noted 40% year-over-year growth in satellite subscriptions among contractors in the Vaca Muerta shale as of February 2026. Intellian equipped a Petronas floating LNG unit with triple-redundant terminals, underscoring the sector's willingness to over-provision to avoid costly downtime. ITU radio-regulation frameworks have streamlined licensing, so new enterprise VSAT system market deployments can scale without protracted approvals.

Digital-Oilfield and Smart-Shipping Initiatives Accelerating VSAT Uptake

Sensor-rich drilling programs and data-driven fleet operations convert connectivity into a production enabler. ST Engineering iDirect works with Solutions by stc to monitor wells and refineries under Saudi Arabia's USD 90 billion digital economy initiative. SES and Viasat Energy introduced sub-150 ms services to offshore platforms in Asia-Pacific, enabling real-time robot control. Shipping lines such as Pacific Basin and Mitsui O.S.K. Lines finalized NexusWave retrofits in 2025 to comply with IMO cyber guidelines and cut unplanned dry-dock visits by up to 30%. The enterprise VSAT system market is benefiting as stakeholders treat bandwidth as a performance lever rather than a utility overhead.

High Capex and Opex Relative to Terrestrial Alternatives

VSAT hardware, installation labor, and teleport overhead still exceed terrestrial equivalents where fiber or 5G are present. Component shortages in 2024 pushed gallium arsenide LNA prices from USD 28.50 to USD 175. Public filings show Comtech and KVH carried quarterly operating expenses of USD 136.24 million and USD 30.96 million, respectively, highlighting the fixed-cost burden of 24/7 network operations. While remote users accept the premium, urban enterprises weigh the economics carefully, curbing wider uptake within the enterprise VSAT system market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of HTS Constellations Lowering Bandwidth Cost

- Growth of Cloud-Based Enterprise Applications Requiring Always-On Links

- Spectrum Congestion and Licensing Hurdles in Key Bands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware-dominated revenue in 2025 thanks to up-front terminal purchases, yet managed offerings are outpacing boxes at 9.98% CAGR. The enterprise VSAT system market size for service contracts is rising as organizations fold bandwidth, cybersecurity, and regulatory compliance into OPEX. L3Harris and Comtech's 5650C2/MP modem simplifies multi-orbit roaming, lowering in-house skill demands. Vendors now bundle orchestration, installation, and ticketing portals, shifting competition toward total cost of ownership rather than sticker price. Integrators leverage bulk capacity deals to shield customers from bandwidth volatility, deepening recurring revenue streams. Hardware innovation continues, Hughes' HM400 airborne modem targets ISR aircraft, but product releases increasingly act as on-ramps to long-term service agreements.

The enterprise VSAT system market, therefore, reflects broader IT outsourcing trends. Enterprises consolidate suppliers, preferring a single throat to choke for uptime SLAs. Vendors respond by acquiring regional installers and investing in network operations centers, shrinking time-to-deploy and standardizing support across geographies. As service portfolios mature, differentiation leans on cybersecurity overlays and API access that integrate satellite links into DevOps toolchains.

Medium earth stations (1.2-2.4 m) balanced gain and cost to win 45.67% share in 2025. Small terminals under 1.2 m, advancing at 9.63% CAGR, benefit from electronically steered arrays that mount flush on decks and vehicles without mechanical gimbals. The enterprise VSAT system market size for compact antennas grows as maritime and defense customers prioritize reduced wind drag, faster installation, and lower maintenance. Orbit's OrBeam MIL and Egatel's retrofit panels exemplify offerings that slide into existing modem ecosystems, minimizing swap-out friction.

Large teleport dishes remain essential for gateways and bandwidth hubs, but enterprise appetite skews toward mobility-ready form factors. Hughes and QEST's phased array proved multi-satellite tracking in 2024, signaling a future where a single panel can roam across GEO, MEO, and LEO networks. This architecture enhances link resiliency while containing topside real estate on cramped vessel masts.

Complete Report Scope:

- By Component

- Hardware

- Services

- By Platform Size

- Small Earth Station (Less Than 1.2 m)

- Medium Earth Station (1.2-2.4 m)

- Large Earth Station (Greater Than 2.4 m)

- By Frequency Band

- Ku-Band

- C-Band

- Ka-Band

- Other Frequency Band

- By End-User Industry

- Oil and Gas

- Maritime

- Government and Defense

- Banking and Financial Services

- Telecom and IT

- Mining

- Energy and Utilities

- Retail

- Other End-User Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America contributed 34.56% of 2025 revenue, underpinned by defense procurement and shale activity, yet urban saturation of fiber and 5G caps incremental growth. Viasat's unified Ka-band service eliminates cross-border contract friction across Canada, the United States, and Mexico, accelerating regional deployments. Multiple U.S. Department of Defense contracts awarded to Gilat and L3Harris during 2025-2026 reinforce the strategic value of satellite redundancy.

Asia-Pacific is the fastest-growing territory with an 8.78% CAGR outlook. National oil companies in India, Indonesia, and Malaysia are digitizing assets that sit beyond terrestrial reach. SES's O3b mPOWER low-latency links empower subsea robot operations and live data collaboration, while Pacific Basin and Mitsui O.S.K. Lines have already outfitted full fleets to meet IMO cyber-resilience rules. Indonesia's BRIsat illustrates how banking networks exploit domestic satellites to blanket rural archipelagos.

Europe's fiber richness restrains broad adoption, yet specialty use cases, North Sea rigs, Baltic shipping, defense mobility, sustain niche growth. The ITU's public censure of cross-border jamming spotlights the geopolitical sensitivity of continental satellite assets. In the Middle East, Saudi Arabia's digital economy vision drives nationwide deployments through partnerships between local telcos and global modem vendors. OmanSat's software-defined satellite, Es'hailSat's North Africa extension, and Eutelsat's KONNECT deal in Cote d'Ivoire confirm that emerging economies view satellite as the quickest route to universal broadband.

South America benefits from Brazil's pre-salt assets and Argentina's shale revolution. Anatel's March 2026 license approvals permit Viasat to blanket Brazil, while Transpetro's early success with hybrid terminals illustrates tangible fuel savings. Africa remains an under-penetrated frontier; capacity deals such as MTN Cote d'Ivoire's with Eutelsat show promise, but fragmented regulation and limited purchasing power moderate the near-term curve of the enterprise VSAT system market.

- Hughes Network Systems LLC

- ViaSat Inc.

- Gilat Satellite Networks Ltd.

- Comtech Telecommunications Corp.

- ST Engineering iDirect

- Newtec

- ND SatCom GmbH

- KVH Industries Inc.

- Signalhorn Trusted Networks GmbH

- CPI International Inc.

- Advantech Wireless Technologies Inc.

- Paradise Datacom LLC

- Satpro M&C Tech Co. Ltd.

- Intellian Technologies Inc.

- Isotropic Systems Ltd.

- Elbit Systems Ltd.

- L3Harris Technologies Inc.

- Ultra Electronics Antennas Group

- Satcom Direct Inc.

- Cobham Satcom

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Broadband Connectivity in Remote and Offshore Sites

- 4.2.2 Digital-Oilfield and Smart-Shipping Initiatives Accelerating VSAT Uptake

- 4.2.3 Expansion of HTS Constellations Lowering Bandwidth Cost

- 4.2.4 Growth of Cloud-Based Enterprise Applications Requiring Always-On Links

- 4.2.5 Emergence of Flat-Panel Electronically Steered Antennas Reducing Installation Footprint

- 4.2.6 Proliferation of 5G Non-Terrestrial Network Standards Unlocking Enterprise-Grade Service Classes

- 4.3 Market Restraints

- 4.3.1 High Capex and Opex Relative to Terrestrial Alternatives

- 4.3.2 Spectrum Congestion and Licensing Hurdles in Key Bands

- 4.3.3 Escalating Cyber-Attacks on Satellite Ground Segment

- 4.3.4 RF Component Supply-Chain Risk Amid Geopolitical Frictions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Services

- 5.2 By Platform Size

- 5.2.1 Small Earth Station (Less Than 1.2 m)

- 5.2.2 Medium Earth Station (1.2-2.4 m)

- 5.2.3 Large Earth Station (Greater Than 2.4 m)

- 5.3 By Frequency Band

- 5.3.1 Ku-Band

- 5.3.2 C-Band

- 5.3.3 Ka-Band

- 5.3.4 Other Frequency Band

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Maritime

- 5.4.3 Government and Defense

- 5.4.4 Banking and Financial Services

- 5.4.5 Telecom and IT

- 5.4.6 Mining

- 5.4.7 Energy and Utilities

- 5.4.8 Retail

- 5.4.9 Other End-User Industry

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Hughes Network Systems LLC

- 6.4.2 ViaSat Inc.

- 6.4.3 Gilat Satellite Networks Ltd.

- 6.4.4 Comtech Telecommunications Corp.

- 6.4.5 ST Engineering iDirect

- 6.4.6 Newtec

- 6.4.7 ND SatCom GmbH

- 6.4.8 KVH Industries Inc.

- 6.4.9 Signalhorn Trusted Networks GmbH

- 6.4.10 CPI International Inc.

- 6.4.11 Advantech Wireless Technologies Inc.

- 6.4.12 Paradise Datacom LLC

- 6.4.13 Satpro M&C Tech Co. Ltd.

- 6.4.14 Intellian Technologies Inc.

- 6.4.15 Isotropic Systems Ltd.

- 6.4.16 Elbit Systems Ltd.

- 6.4.17 L3Harris Technologies Inc.

- 6.4.18 Ultra Electronics Antennas Group

- 6.4.19 Satcom Direct Inc.

- 6.4.20 Cobham Satcom

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

VSAT(甚小孔徑終端)市場預測至2034年-按組件、網路類型、頻段、企業規模、最終用戶和地區分類的全球分析

VSAT(甚小孔徑終端)市場預測至2034年-按組件、網路類型、頻段、企業規模、最終用戶和地區分類的全球分析 微型VSAT市場-全球產業規模、佔有率、趨勢、機會、預測:按頻率、應用、技術、地區和競爭格局分類,2021-2031年

微型VSAT市場-全球產業規模、佔有率、趨勢、機會、預測:按頻率、應用、技術、地區和競爭格局分類,2021-2031年 VSAT(甚小孔徑終端)市場報告:按解決方案、平台、頻率、最終用途、行業垂直領域和地區分類(2026-2034 年)

VSAT(甚小孔徑終端)市場報告:按解決方案、平台、頻率、最終用途、行業垂直領域和地區分類(2026-2034 年) 超小型孔徑終端市場:按類型、組件、頻段、天線尺寸、設計趨勢、應用和最終用戶分類-2026-2032年全球市場預測

超小型孔徑終端市場:按類型、組件、頻段、天線尺寸、設計趨勢、應用和最終用戶分類-2026-2032年全球市場預測 2026年全球VSAT(甚小型天線終端)市場報告

2026年全球VSAT(甚小型天線終端)市場報告 2026-2034年全球微型開放式孔徑終端(VSAT)市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球微型開放式孔徑終端(VSAT)市場規模、佔有率、趨勢和成長分析報告 基於衛星的消費者與企業寬頻:全球趨勢與預測(2024-2034)船用VSAT市場:依船舶類型、頻段、服務模式、網路拓樸、應用、最終用戶分類,全球預測(2026-2032年)

基於衛星的消費者與企業寬頻:全球趨勢與預測(2024-2034)船用VSAT市場:依船舶類型、頻段、服務模式、網路拓樸、應用、最終用戶分類,全球預測(2026-2032年) 甚小孔徑終端 (VSAT) 市場:依頻段、平台、網路架構、解決方案和最終用途劃分 - 全球預測至 2036 年

甚小孔徑終端 (VSAT) 市場:依頻段、平台、網路架構、解決方案和最終用途劃分 - 全球預測至 2036 年 企業級VSAT系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型及最終用戶分類

企業級VSAT系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型及最終用戶分類