|

市場調查報告書

商品編碼

2072592

自主身分(SSI):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Self-Sovereign Identity (SSI) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

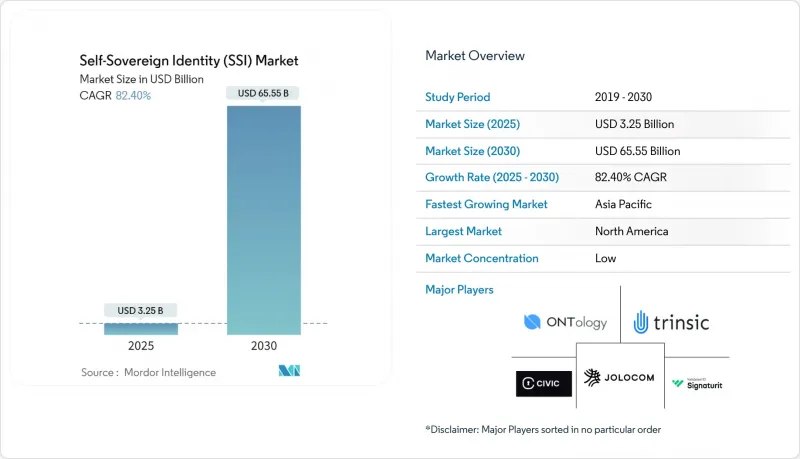

根據 Mordor Intelligence 預測,自主身分 (SSI) 市場規模預計將在 2025 年達到 32.5 億美元,並在 2030 年擴大到 655.5 億美元,複合年成長率高達 82.40%。

本報告按產品/服務(平台/軟體、服務)、身分類型(個人身分、組織身分等)、應用領域(身分驗證/存取管理、支付和金融服務等)、最終使用者產業(政府和公共部門、醫療保健和生命科學等)以及地區進行細分。市場預測以美元計價。

全球主權身分(SSI)市場趨勢與洞察

政府機構對去中心化數位身分的需求日益成長

在隱私法規日益嚴格和服務成本壓力不斷增加的背景下,國家和州政府機構正在將SSI試點計畫擴展為全面運作。美國聯邦政府的現代化計畫是基於NIST 800-63-4架構,使各機構能夠在不依賴集中式資料孤島的情況下頒發高度安全的憑證。同時,歐盟eIDAS 2.0要求所有歐盟成員國在2026年前分發可互通的數位錢包,為公民提供一套用於跨境服務的憑證。日本的「我的號碼卡」(My Number Card)現在可以直接註冊到Apple Wallet,這表明傳統的身份識別方案可以在滿足監管標準的同時,過渡到公民控制的儲存方式。政府的採用正在為私營部門的採用創造關鍵規模,並促進網路效應,從而吸引金融科技公司、航空公司和醫療保健提供者。隨著越來越多的司法管轄區設定錢包部署的最後期限,SSI正從一項實驗性技術發展成為標準化的識別基礎設施。

將SSI與國家電子識別和旅行授權計劃整合。

國際航空運輸協會 (IATA) 的「數位旅行認證舉措」透過將護照儲存在用戶的電子錢包中,實現了幾秒鐘內完成文件驗證,從而緩解了機場擁塞。歐洲數位身分錢包專為整個申根區設計,允許公民使用相同的身份驗證資訊在德國開設銀行帳戶、在法國接受醫療服務以及在整個申根區內登機。美國運輸安全管理局(TSA) 的行動駕駛執照試點計畫表明,國內身分文件可以滿足國際航空要求,為更順暢的登機手續辦理體驗鋪平了道路。國際民航組織 (ICAO) 等國際標準化機構的互通性要求正在影響電子錢包的規範,加速了邊境管制機構之間標準的協調統一。

一種超越 W3C 的 VC/DID 的未定義全球互通性標準。

儘管 W3C 已於 2024 年最終確定了“可驗證憑證資料模型 2.0”,但撤銷、跨鏈驗證和信任框架發現方面的規範仍不完善。供應商正透過各自的擴展來填補這些空白,導致各自為政,損害了 SSI 的「通用可移植性」願景。擔心被供應商鎖定的企業正在推遲多供應商部署,直到更多標準穩定下來。碎片化也導致實施成本增加,因為整合提供者必須在不相容的技術棧之間建立橋樑。去中心化身分基金會正在起草補充指南,但共識的延遲可能會導致企業的採購週期超出預期。

細分市場分析

2024年,平台和軟體產品佔據了自主身分(SSI)市場61.43%的佔有率,這印證了早期採用者對核心基礎設施的偏好。然而,服務層預計將以83.14%的複合年成長率成長。這是因為企業需要整合、客製化和管治的專業知識,才能在複雜的跨司法管轄區網路中運作錢包。服務層包括憑證頒發編配、零知識證明配置和持續合規性審計,這些都能產生除一次性許可費之外的經常性收入。像Dock Labs和cheqd之間的合作這樣的聯盟,透過將產品堆疊與諮詢深度相結合,正在加速大規模部署。隨著SSI在高度監管行業的應用日益廣泛,專業服務的範圍也不斷擴大,涵蓋了系統整合商、網路安全公司和專業顧問公司。

向服務型模式的轉變正在改變採購週期中的預算分配。決策者越來越要求簽訂基於結果的契約,將供應商的報酬與降低上線成本和避免欺詐損失掛鉤。隨著雲端原生交付模式實現無縫升級,託管服務供應商必須持續追蹤合規情況,以符合不斷變化的法規。因此,儘管平台層面的價格競爭日益激烈,但服務利潤率仍保持穩健。這一趨勢使得以諮詢主導的供應商即使在軟體商品化的情況下也能保持永續的盈利。

到了2024年,個人身分的應用案例已奠定商業性基礎,因為大多數電子錢包程式的目標客戶群是一般大眾和零售銀行客戶。個人憑證領域自主身分的市場規模正在為後續向企業和設備領域的擴展奠定基礎。受聯網汽車安全、智慧電網管理和工業感測器認證等需求的推動,物聯網和設備身分應用預計到2030年將實現82.87%的複合年成長率。汽車製造商目前正在採用檢驗的設備憑證來授權空中下載(OTA)更新,同時保護車主隱私。智慧電錶、路由器和無人機製造商也同樣採用去中心化註冊方式,以消除憑證授權單位(CA)的單點故障,這表明設備身分將推動收入多元化。

個人身分驗證憑證與裝置身分驗證憑證之間的交互作用催生了全新的體驗。例如,駕駛員可以使用與檢驗憑證關聯的臉部認證對共享汽車進行身份驗證,而家庭則可以為送貨機器人設定限時進入許可權。這些跨領域的工作流程迫使供應商建立早期消費級錢包無需的授權協議和多重簽章方案。因此,身分平台藍圖日益將分層金鑰管理和安全元件整合納入汽車、工業和家用電子電器供應鏈的各個環節。

區域分析

2024年,北美繼續佔據自主身分(SSI)市場44.87%的佔有率。這主要得益於聯邦和州政府機構採納了基於NIST 800-63-4標準的錢包試點計畫。例如,運輸安全局(TSA)的行動駕駛執照檢驗項目,在實現機場查核點現代化的同時,也重振了國內錢包生態系統。紐約和舊金山的金融科技中心正在將檢驗憑證整合到新銀行的註冊流程中,從而形成良性循環,促進個人投資者、零工經濟平台和醫療保健入口網站等平台的普及。加拿大的公私合作機構——數位身分和認證委員會,正在建立一個符合美國規範的跨州認證框架;墨西哥的金融科技法也推動了新興銀行對錢包的採用。智慧型手機的高普及率和研發人才的集中也進一步鞏固了該地區的領先地位。

歐洲以「eIDAS 2.0」市場規模位居全球第二。該法案以法律形式強制所有成員國在2026年前至少發行一款數位錢包。德國正投資基於區塊鏈的行政服務身分註冊系統,法國正在將醫療保險卡整合到公民錢包中,而英國則在脫歐後的信任框架中推廣身分驗證。歐洲區塊鏈服務基礎設施支援跨境身分驗證,使居民無需重新出示紙本身分證明即可在國外開設銀行帳戶、簽署房產契約和領取社會安全福利。歐盟的資料主權規範,例如《一般資料保護規範》(GDPR),鼓勵以使用者為中心的錢包,最大限度地減少儲存在伺服器上的個人數據,從而強化自主身分(SSI)的設計原則。

亞太地區是該地區成長最快的區域,複合年成長率高達82.47%。日本在該領域處於領先地位,已將「我的號碼」卡整合到主流智慧型手機錢包中,在隱私保護的環境下,為消費者提供即時的年齡、地址和納稅人識別號碼驗證。印度正在探索將社會安全資訊系統(SSI)疊加到Aadhaar基礎設施上,旨在透過在信用評分和零工保險中選擇性揭露資訊來實現身分驗證。在韓國,一項數位駕照試點計畫正在與主要銀行應用程式整合,而澳洲的可信賴數位身分框架正在擴大電子錢包在醫療保健和教育領域的應用。中國專注於國家控制的數位身份,而香港的試點區正在金融科技沙盒中測試去中心化驗證,以實現跨境電子KYC(e-KYC)。區域聯盟正在製定互通性規範,以支持東協的跨境貿易,從而進一步加速其應用。

中東、非洲和南美洲正在崛起為關鍵區域。巴西承諾在2032年前實施基於區塊鏈的公民身分證,旨在簡化公共服務取得流程並減少證件偽造。南非正在將智慧ID卡擴展到行動身分驗證領域,並試驗推行自主身分識別(SSI)用於福利金支付。波灣合作理事會(GCC)成員國正在試驗區塊鏈護照,以簡化外籍勞工的招募流程。智慧型手機普及率低和網路連線不穩定是短期障礙,但隨著4G和5G網路投資的不斷增加,一旦設備價格下降,預計普及率將出現快速「突破」。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 各國政府對去中心化數位身分的需求日益成長

- 將SSI與國家電子識別和旅行授權計劃整合

- Web3錢包作為通用身份管理器的迅速崛起

- 促進符合歐盟 eIDAS 2.0 和美國 NIST 800-63-4 標準

- 人工智慧驅動的身份驗證降低了用戶註冊門檻。

- 利用 SSI 的可重複使用 KYC 網路可以降低銀行取得新客戶的成本。

- 市場限制因素

- 除 W3C VC/DID 之外,其他未定義的全球互通性標準

- 對智慧型手機普及率在儲存身分驗證資訊方面的依賴性

- 基於獎勵的SSI帳本中代幣經濟永續性的風險

- 發行人在到期糾紛中面臨較高的法律責任風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 平台/軟體

- 服務

- ID 類型

- 個人識別資訊

- 組織/企業 ID

- 物聯網/設備 ID

- 透過使用

- 身份驗證/存取管理

- 支付和金融服務

- 檢驗憑證和電子身份驗證

- 供應鍊和資源

- 其他用途

- 按最終用戶行業分類

- 銀行、金融服務和保險(BFSI)

- 政府/公共部門

- 醫療保健和生命科學

- 資訊科技/通訊

- 零售與電子商務

- 出遊與交通

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Evernym, Inc.

- Civic Technologies, Inc.

- Validated ID, SL

- Trinsic, Inc.

- Jolocom GmbH

- Ontology Foundation Ltd.

- Dock Labs AG

- SelfKey Foundation

- cheqd Ltd.

- Spruce Systems, Inc.

- GATACA Digital Identity Solutions SL

- Keyp GmbH

- Veres One Foundation

- Affinidi Pte Ltd.

- Serto Labs, Inc.

- R3 LLC

- uPort by ConsenSys AG

- ID2020 Alliance, Inc.

- Obsidian Systems LLC

- Tykn BV

第7章 市場機會與未來展望

According to Mordor Intelligence, the self-sovereign identity (SSI) market size reached USD 3.25 billion in 2025 and is projected to climb to USD 65.55 billion by 2030, delivering an exceptional 82.40% CAGR.

This report is Segmented by Offering (Platform/Software, and Services), Identity Type (Individual Identity, Organizational Identity, and More), Application (Authentication/Access Management, Payments and Financial Services, and More), End-User Industry (Government and Public Sector, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Self-Sovereign Identity (SSI) Market Trends and Insights

Growing demand for decentralized digital IDs among governments

National and state agencies are scaling SSI pilots into full production as privacy regulation tightens and cost-to-serve pressures mount. The U.S. federal modernization program anchors its architecture on NIST 800-63-4, letting agencies issue high-assurance credentials without central data silos. In parallel, eIDAS 2.0 compels every EU member state to distribute interoperable digital wallets by 2026, providing citizens with one credential for cross-border services. Japan's My Number card now loads directly into Apple Wallet, illustrating how legacy ID schemes can migrate to citizen-controlled storage while meeting regulatory criteria. Government adoption establishes critical mass for private-sector uptake, spurring network effects that attract fintechs, airlines, and healthcare providers. As more jurisdictions declare wallet deadlines, SSI transitions from exploratory technology to default identity infrastructure.

Integration of SSI with national eID and travel credential programs

The International Air Transport Association's Digital Travel Credentials initiative stores passports inside user wallets, permitting document verification in seconds and lowering airport congestion. European Digital Identity wallets are built for Schengen-wide acceptance, enabling citizens to open bank accounts in Germany, receive healthcare in France, and board aircraft across the region using the same credential. Transportation Security Administration pilots of mobile driver's licenses show domestic IDs can fit global aviation requirements, paving the way for frictionless corridor-to-gate experiences. Interoperability mandates from international civil aviation standards bodies now shape wallet specifications, accelerating standard alignment among border agencies.

Undefined global interoperability standards beyond W3C VC/DID

W3C finalized Verifiable Credential Data Model 2.0 in 2024, yet specifications for revocation, cross-chain proofs, and trust-framework discovery remain unfinished. Vendors are filling gaps with proprietary extensions, creating silos that undermine the universal portability vision of SSI. Enterprises wary of lock-in postpone multi-vendor rollout until additional standards stabilize. Fragmentation also increases implementation costs because integrators must build bridges between incompatible stacks. The Decentralized Identity Foundation is drafting supplemental guidance, but slow consensus risks delaying enterprise procurement cycles beyond the forecast window.

Other drivers and restraints analyzed in the detailed report include:

- Rapid rise of Web3 wallets as universal identity managers

- Compliance push from EU eIDAS 2.0 and U.S. NIST 800-63-4

- Reliance on smartphone penetration for credential custody

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform and software products captured 61.43% of the self-sovereign identity market share in 2024, confirming that early adopters prioritized core infrastructure. Services, however, are projected to post an 83.14% CAGR because enterprises now need integration, customization, and governance expertise to operationalize wallets across complex, multi-jurisdiction networks. The services layer includes credential issuance orchestration, zero-knowledge proof configuration, and ongoing compliance audits, yielding recurring revenue streams that outstrip one-time license fees. Alliances such as Dock Labs partnering with cheqd fuse product stacks with consulting depth to accelerate large-scale rollouts. As more regulated sectors adopt SSI, the professional-services pool widens across system integrators, cybersecurity firms, and specialty advisory boutiques.

The shift to services alters budget allocations in procurement cycles. Decision-makers increasingly seek outcome-based contracts that tie vendor remuneration to onboarding-cost reductions or fraud-loss avoidance. Cloud-native delivery models make upgrades seamless, meaning managed services vendors must demonstrate continuous compliance tracking as regulations evolve. Consequently, price competition in the platform tier intensifies while service margins remain resilient. This dynamic supports sustained profitability for consulting-led providers even as software commoditizes.

Individual identity use cases established the commercial baseline in 2024 because most wallet programs target citizens and retail banking clients. The self-sovereign identity market size for individual credentials underpins subsequent extensions into enterprise and device realms. IoT and device identity applications are poised for an 82.87% CAGR to 2030, driven by connected-car security, smart-grid management, and industrial sensor authentication. Automotive manufacturers now embed verifiable device credentials that authorize over-the-air updates while protecting owner privacy. Manufacturers of smart meters, routers, and drones are likewise adopting decentralized onboarding to neutralize certificate-authority single points of failure, signaling that device identity will broaden revenue diversity.

Interplay between personal and device credentials unlocks novel experiences. Drivers can authenticate to shared vehicles with a face scan that resolves to a verifiable credential, while household members delegate limited-time access rights to delivery robots. These cross-domain workflows push vendors to build delegation protocols and multi-signature schemes that were unnecessary in early consumer wallets. In turn, identity-platform roadmaps increasingly include hierarchical key management and secure-element integration across automotive, industrial, and consumer electronics supply chains.

Complete Report Scope:

- By Offering

- Platform / Software

- Services

- By Identity Type

- Individual Identity

- Organizational / Enterprise Identity

- IoT / Device Identity

- By Application

- Authentication / Access Management

- Payments and Financial Services

- Verifiable Credentials and e-KYC

- Supply-Chain and Provenance

- Other Applications

- By End-User Industry

- Banking, Financial Services and Insurance (BFSI)

- Government and Public Sector

- Healthcare and Life Sciences

- IT and Telecom

- Retail and e-Commerce

- Mobility and Transportation

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America retained 44.87% of the self-sovereign identity market size in 2024 because federal and state agencies embraced wallet pilots under NIST 800-63-4. Programs such as the Transportation Security Administration's mobile driver's license verification modernize airport security checkpoints while feeding domestic wallet ecosystems. Fintech hubs in New York and San Francisco integrate verifiable credentials into neobank onboarding, creating a virtuous loop that drives platform utilization across retail investors, gig-economy platforms, and healthcare portals. Canada's public-private Digital Identity and Authentication Council cultivates cross-province credential frameworks that dovetail with U.S. specifications, and Mexico's fintech law spurs wallet deployment among challenger banks. High smartphone penetration and developer talent density further sustain the region's leadership.

Europe ranks second in value terms thanks to eIDAS 2.0, which establishes a binding obligation for every member state to issue at least one digital wallet by 2026. Germany invests in blockchain-backed identity registries for public-administration services, France integrates health-insurance cards into citizen wallets, and the United Kingdom advances post-Brexit trust-framework certifications. The European Blockchain Services Infrastructure underpins cross-border verification, letting residents open bank accounts, sign property deeds, or claim social benefits abroad without re-presenting paper ID. EU data-sovereignty norms such as GDPR favor user-centric wallets that store minimal personal data on servers, reinforcing SSI design principles.

Asia-Pacific posts the fastest regional trajectory with an 82.47% CAGR. Japan leads with My Number card integration into major smartphone wallets, providing consumers instant proof of age, address, and tax identification within a privacy-preserving container. India explores SSI overlays on its Aadhaar infrastructure to enable selective-disclosure proofs in credit scoring and gig-worker insurance. South Korea's digital-driver-license pilot couples with major bank apps, while Australia's Trusted Digital Identity Framework expands wallet-acceptance in healthcare and education. China focuses on state-controlled digital ID, but pilot zones in Hong Kong test decentralized proofs for cross-border e-KYC within fintech sandboxes. Regional consortiums craft interoperability profiles to support cross-border trade in the Association of Southeast Asian Nations, further intensifying adoption.

The Middle East and Africa, and South America form emerging hot spots. Brazil committed to blockchain-based citizen ID by 2032, aiming to simplify public-service access and reduce document forgery. South Africa expands smart-ID cards into mobile credentials and pilots SSI for welfare disbursement. Gulf Cooperation Council countries experiment with blockchain passports to streamline expatriate labor onboarding. Limited smartphone reach and patchy internet coverage act as near-term brakes, yet rising investment in 4G and 5G networks points toward rapid leapfrog adoption once device costs decline.

- Evernym, Inc.

- Civic Technologies, Inc.

- Validated ID, S.L.

- Trinsic, Inc.

- Jolocom GmbH

- Ontology Foundation Ltd.

- Dock Labs AG

- SelfKey Foundation

- cheqd Ltd.

- Spruce Systems, Inc.

- GATACA Digital Identity Solutions S.L.

- Keyp GmbH

- Veres One Foundation

- Affinidi Pte Ltd.

- Serto Labs, Inc.

- R3 LLC

- uPort by ConsenSys AG

- ID2020 Alliance, Inc.

- Obsidian Systems LLC

- Tykn B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for decentralized digital IDs among governments

- 4.2.2 Integration of SSI with national eID and travel credential programs

- 4.2.3 Rapid rise of Web-3 wallets as universal identity managers

- 4.2.4 Compliance push from EU eIDAS 2.0 and U.S. NIST 800-63-4

- 4.2.5 Gen-AI-driven identity proofing reducing onboarding friction

- 4.2.6 SSI-enabled reusable KYC networks lowering bank onboarding cost

- 4.3 Market Restraints

- 4.3.1 Undefined global interoperability standards beyond W3C VC/DID

- 4.3.2 Reliance on smart-phone penetration for credential custody

- 4.3.3 Token-economics sustainability risks for incentive-based SSI ledgers

- 4.3.4 High liability exposure for issuers under revocation disputes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Platform / Software

- 5.1.2 Services

- 5.2 By Identity Type

- 5.2.1 Individual Identity

- 5.2.2 Organizational / Enterprise Identity

- 5.2.3 IoT / Device Identity

- 5.3 By Application

- 5.3.1 Authentication / Access Management

- 5.3.2 Payments and Financial Services

- 5.3.3 Verifiable Credentials and e-KYC

- 5.3.4 Supply-Chain and Provenance

- 5.3.5 Other Applications

- 5.4 By End-User Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Government and Public Sector

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 IT and Telecom

- 5.4.5 Retail and e-Commerce

- 5.4.6 Mobility and Transportation

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Evernym, Inc.

- 6.4.2 Civic Technologies, Inc.

- 6.4.3 Validated ID, S.L.

- 6.4.4 Trinsic, Inc.

- 6.4.5 Jolocom GmbH

- 6.4.6 Ontology Foundation Ltd.

- 6.4.7 Dock Labs AG

- 6.4.8 SelfKey Foundation

- 6.4.9 cheqd Ltd.

- 6.4.10 Spruce Systems, Inc.

- 6.4.11 GATACA Digital Identity Solutions S.L.

- 6.4.12 Keyp GmbH

- 6.4.13 Veres One Foundation

- 6.4.14 Affinidi Pte Ltd.

- 6.4.15 Serto Labs, Inc.

- 6.4.16 R3 LLC

- 6.4.17 uPort by ConsenSys AG

- 6.4.18 ID2020 Alliance, Inc.

- 6.4.19 Obsidian Systems LLC

- 6.4.20 Tykn B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

自主身分市場:按類型、身分類別、技術、部署模式、組織規模和最終用戶產業分類-2026-2032年全球市場預測

自主身分市場:按類型、身分類別、技術、部署模式、組織規模和最終用戶產業分類-2026-2032年全球市場預測 2026年全球自主身分市場報告自主身分服務市場:依服務、組織規模、部署模式、應用程式和最終用戶產業分類,全球預測,2026-2032年自主身分解決方案市場:按解決方案、部署模式、企業規模、最終用戶產業和應用程式分類,全球預測(2026-2032 年)

2026年全球自主身分市場報告自主身分服務市場:依服務、組織規模、部署模式、應用程式和最終用戶產業分類,全球預測,2026-2032年自主身分解決方案市場:按解決方案、部署模式、企業規模、最終用戶產業和應用程式分類,全球預測(2026-2032 年) 2032 年自主主權身分市場預測:按產品、網路類型、部署類型、組織規模、技術、應用、最終用戶和地區進行的全球分析

2032 年自主主權身分市場預測:按產品、網路類型、部署類型、組織規模、技術、應用、最終用戶和地區進行的全球分析 自主身分市場-全球產業規模、佔有率、趨勢、機會和預測(按產品、類型、垂直產業、地區和競爭細分,2020-2030 年預測)

自主身分市場-全球產業規模、佔有率、趨勢、機會和預測(按產品、類型、垂直產業、地區和競爭細分,2020-2030 年預測) 全球自主主權身分(SSI)市場

全球自主主權身分(SSI)市場 自主身分市場規模、佔有率和趨勢分析報告:按產品、身分類型、網路、垂直產業、地區和細分市場預測,2025 年至 2030 年

自主身分市場規模、佔有率和趨勢分析報告:按產品、身分類型、網路、垂直產業、地區和細分市場預測,2025 年至 2030 年 全球自主主權身分市場規模研究,依產品、身分類型、網路、組織規模、垂直和區域預測 2022-2032

全球自主主權身分市場規模研究,依產品、身分類型、網路、組織規模、垂直和區域預測 2022-2032