|

市場調查報告書

商品編碼

2072587

資料居住和主權合規工具:市場佔有率分析、行業趨勢和統計數據以及成長預測(2025-2030 年)Data Residency and Sovereignty Compliance Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

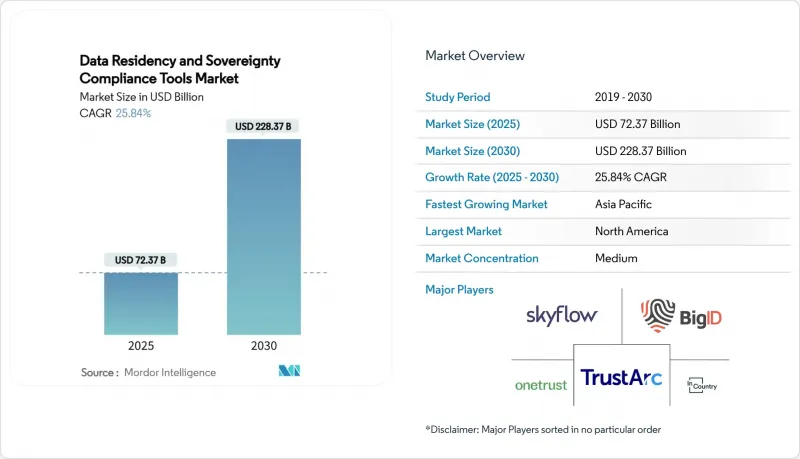

根據 Mordor Intelligence 預測,資料居住和主權合規工具市場規模預計將在 2025 年達到 723.7 億美元,到 2030 年將擴大到 2,283.7 億美元,複合年成長率為 25.84%。

本報告按部署模式(本地部署、公共雲端、混合部署)、工具類型(DRaaS(數據駐留即服務)平台、其他)、組織規模(大型企業、中小企業)、最終用戶行業(銀行、金融服務和保險、醫療保健和生命科學、其他)以及地區(北美、南美、歐洲、亞太、中東和非洲)進行分類。

全球數據居住和主權合規工具市場趨勢與洞察

更嚴格的數據在地化法律和更嚴厲的處罰

GDPR的執行力道在2024年達到高峰,罰款總額高達12億歐元,平均每天發生363起資料外洩事件。中國的《網路資料安全管理條例》於2025年1月生效,對處理大量個人資料的公司分階段施加義務。印度的《數位個人資料保護法》引入了域外適用原則,並規定最高罰款可達25億印度盧比(約3000萬美元)。印尼和馬來西亞的類似舉措顯示亞太地區正在推動監管協調。這些法規共同推高了合規成本,並將資料駐留解決方案市場定位為跨境業務營運的基本需求。

利用超大規模資料中心業者部署主權雲

AWS已撥款78億歐元(約88億美元)用於建設歐洲主權雲端基礎設施,目標是在2025年底前全面運作,其中包括在歐盟境內居住人員。微軟的「主權雲端」支援加密和策略控制的工作負載,並持續增加區域金鑰管理選項。包括Oracle在內的超大規模資料中心業者正在亞太地區部署類似的藍圖,鼓勵企業將雲端服務與司法管轄區的監管控制結合。這些投資透過創建獨立且經過認證的工具和諮詢服務連接點,正在擴大資料駐留解決方案市場。

高昂的實施和編配成本

實施過程通常涉及基礎設施變更、法律諮詢和持續的審計管理,導致總擁有成本超出初始預算。儘管雲端原生的「駐留即服務」(RaaS)模式有助於平衡資本支出,但中小企業(SME)感受到的壓力最大。雖然提供諮詢支援和自動化監控的供應商越來越受歡迎,但宏觀經濟的謹慎態度意味著一些組織仍處於試點階段,而非全面部署。

細分市場分析

混合環境兼具柔軟性,既能將高度敏感的資料保留在私有雲域內,又能利用公共雲端的成本優勢處理敏感度較低的工作負載。該細分市場30.2%的複合年成長率凸顯了其作為跨國公司敏捷性驅動力的重要地位。儘管由於超大規模資料中心業者雲端服務商對私有雲域的投資,公共雲端仍保持著市場主導地位,但對於國防等高度監管的工作負載而言,本地部署系統仍然至關重要。資訊長們正計劃將部分工作負載遷回國內,預計將進一步提升對可配置部署引擎的需求。能夠統一管理物件儲存、私有雲端和託管設施的資料規則的供應商正在建立競爭優勢。

隨著AWS、微軟和Oracle持續認證新的主權區域,源自公共雲端採用的資料駐留解決方案市場規模預計將持續擴大。同時,混合解決方案正日益融入“碳感知部署能力”,將低風險數據遷移到可再生能源運作的設施,從而滿足合規性和永續性要求。在地緣政治緊張局勢加劇的背景下,許多董事會將混合策略引擎視為戰略保障,而不僅僅是技術工具,以應對被迫脫鉤的情況。

資料隱私管理套件將偵測、分類和執行功能整合到一個統一的主機中,預計將在 2024 年推動收入成長。目前,市場需求正轉向「居住即服務」(RaaS)模式,該模式以訂閱收費系統提供預先定義的控制措施、國內資料保險庫和自動化的傳輸影響評估。 Skyflow 的隱私保險庫支援超過 150 個司法管轄區,這表明市場對承包解決方案的需求強勁。隨著零信任框架在人工智慧工作負載中逐漸成為標準,令牌化和託管工具正迅速獲得廣泛應用。

在嚴格的監管要求下,企業需要實現單一螢幕整合,但對包含資料居住模組的管治、風險和合規 (GRC) 平台的投入仍然強勁。同時,基於主權雲端的工具包正在最佳化 Kubernetes叢集,使其能夠在超大規模資料中心業者資料中心的主權區域內運行,從而降低整合門檻。對 BigID 及類似供應商的融資表明,投資者將人工智慧驅動的數據衛生管理視為數據居住解決方案市場的下一個成長點。

區域分析

預計到2024年,北美將佔據38.2%的市場佔有率,這主要得益於美國《雲端法案》、加拿大《個人資訊保護和超大規模資料中心業者法》(PIPEDA)以及超大規模雲端服務供應商的廣泛企業發展。該地區已成為合規性試驗場,跨國公司在向全球部署之前,會在此完善架構,以協調聯邦、州和行業特定法規。美國近期發布的關於人工智慧出口管制的政策文件,為平台供應商增加了另一層法律和監管責任。加拿大允許採用「受保護B級」公共雲端的決定表明,政策的明確性可以在維持主權控制的同時,加速公有雲的普及。

亞太地區預計將實現28.1%的複合年成長率,成為所有地區中成長最快的地區。印度的《數位個人資料保護法》、中國的《網路資料安全管理條例》和印尼的《個人資料保護法》正在共同建構一個和諧的基礎,簡化解決方案提供者的區域規模部署。人工智慧工作負載驅動的大規模資料中心的擴張,為資料居住儲存庫和主權雲提供了實體基礎。跨國公司現在將亞太地區的在地化預算視為核心項目,而非緊急資金,這鞏固了該地區在資料駐留解決方案市場中的重要地位。

歐洲正充分利用其GDPR的成熟度以及超大規模資料中心業者雲端服務商對自主雲端基礎設施的投資。 AWS斥資78億歐元(88億美元)的計畫包括在歐盟境內設立專門人員並空氣間隙管治。隨著執法力度的加大,合規預算依然充足,2024年的罰款總額便印證了這一點。歐盟人工智慧法擴大了治理範圍,將演算法輸出納入其中,這增加了對精細審計追蹤的需求,而駐留工具恰好可以提供這種追蹤。在中東和非洲,各國政府正在製定全面的隱私框架,並為雲端園區津貼以吸引外國投資,從而為駐留專業人員開拓了新的市場。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 更嚴格的數據在地化法律和更嚴厲的處罰

- 利用超大規模資料中心業者部署主權雲

- 因違規和網路侵權訴訟而導致的成本增加

- 「居留即服務」平台已擴展到 70 多個國家。

- 本地化人工智慧模型需要符合規範的資料管道。

- 數位貿易協定包含主權條款。

- 市場限制因素

- 實施和調整的相關成本相對較高。

- 法規差異/不同司法管轄區之間的波動

- 由於永續性問題,將資料中心遷往日本存在風險

- 貿易壁壘為跨境SaaS帶來了不利影響。

- 宏觀經濟因素的影響

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 現場

- 公共雲端

- 混合

- 新產品

- DRaaS(資料駐留即服務)平台

- 資料隱私管理套件

- GRC平台及駐留模組

- 主權雲端實施工具

- 令牌化和資料保險庫解決方案

- 按組織規模

- 大公司

- 中小企業

- 按最終用途行業分類

- BFSI

- 醫療保健和生命科學

- 政府/公共部門

- 資訊科技/通訊

- 零售與電子商務

- 製造業和工業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- OneTrust, LLC

- TrustArc Inc.

- BigID, Inc.

- InCountry, Inc.

- Skyflow, Inc.

- Riscosity, Inc.

- Odaseva SAS

- Protegrity USA, Inc.

- Privacera, Inc.

- SecuPi Ltd.

- Immuta, Inc.

- Securiti, Inc.

- DataGrail, Inc.

- DataGuard GmbH

- Ketch, Inc.

- Delphix Corporation

- Anonos Inc.

- Data Sentinel Inc.

- Egnyte, Inc.

- Atakama Inc.

- Virtru, Inc.

- Enveil, Inc.

- Evervault Ltd.

- CryptoMove, Inc.

- StrongSalt, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, data residency and Sovereignty Compliance Tools market size reached USD 72.37 billion in 2025 and is forecast to rise to USD 228.37 billion by 2030, implying a compounding CAGR of 25.84%.

This report is Segmented by Deployment Model (On-Premises, Public Cloud, and Hybrid), Tool Type (Data Residency-As-A-Service Platforms, and More), Organisation Size (Large Enterprises, and Small and Medium Enterprises), End-Use Industry (BFSI, Healthcare and Life Sciences, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Global Data Residency and Sovereignty Compliance Tools Market Trends and Insights

Proliferation of Strict Data-Localization Laws and Penalties

GDPR enforcement peaked during 2024 with EUR 1.2 billion in fines, while daily breach notifications averaged 363 incidents. China's Network Data Security Management regulations, which took effect in January 2025, layer tiered obligations on firms processing large personal data volumes. India's Digital Personal Data Protection Act introduces extraterritorial reach and penalties up to INR 250 crore (USD 30 million). Similar moves in Indonesia and Malaysia signal Asia-Pacific harmonisation. Collectively, these statutes boost the compliance premium and position the data residency solutions market as a foundational requirement for cross-border operations.

Hyperscaler Sovereign-Cloud Roll-outs

AWS earmarked EUR 7.8 billion (USD 8.8 billion) for European sovereign-cloud infrastructure to be fully operational by end-2025, including EU-resident personnel. Microsoft's Cloud for Sovereignty enables encrypted policy-controlled workloads and continues to add regional key-management options. Oracle and other hyperscalers mirror the blueprint across Asia-Pacific, encouraging enterprises to mix cloud services with jurisdictional controls. These investments enlarge the data residency solutions market by creating plug-in points for independence-certified tooling and advisory overlays.

High Implementation and Orchestration Costs

Deployment often combines infrastructure change, legal consultancy, and ongoing audit management, sending total ownership beyond initial budgets. SMEs feel the pinch most acutely, even though cloud-native residency-as-a-service models help to flatten capital outlays. Vendors that bundle advisory support with automated monitoring find traction, yet macro-economic caution keeps some organisations in pilot phases rather than full roll-outs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Cost of Non-Compliance and Cyber-Breach Litigation

- AI-Model Localization Demands Compliant Data Pipes

- Regulatory Patchwork and Volatility Across Jurisdictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid environments deliver the flexibility to hold sensitive data within sovereign space while leveraging public-cloud cost benefits for non-sensitive workloads. The segment's 30.2% CAGR underscores its role as the agility lever for multinational firms. Public cloud maintains a commanding share due to hyperscaler investment in sovereign zones, whereas on-premises systems remain essential for ultra-regulated workloads such as defense. CIO plans to repatriate selected workloads to further energise demand for configurable placement engines. Vendors able to orchestrate data rules across object stores, private clouds, and colocation footprints are carving a competitive advantage.

The data residency solutions market size attributed to public-cloud deployments is expected to keep expanding as AWS, Microsoft, and Oracle certify additional sovereign regions. At the same time, hybrid solutions increasingly include carbon-aware placement features that shift low-risk data toward facilities powered by renewable energy, fulfilling both compliance and sustainability mandates. As geopolitical tensions rise, many boards consider hybrid policy engines not merely technical tooling but strategic insurance against forced decoupling scenarios.

Data-privacy management suites integrate discovery, classification, and policy enforcement in one console and therefore lead to 2024 revenue. Demand now tilts toward residency-as-a-service offerings that wrap predefined controls, in-country vaults, and automated transfer impact assessments behind subscription pricing. Skyflow's privacy vault supports 150+ jurisdictions, illustrating market appetite for turnkey coverage. Tokenisation and vaulting tools gain particular velocity as zero-trust frameworks become standard for AI workloads.

Spending on governance, risk, and compliance platforms that incorporate residency modules remains steady among highly regulated enterprises that want single-pane consolidation. Meanwhile, sovereign-cloud enablement toolkits optimise Kubernetes clusters to run inside hyperscaler sovereign regions, lowering integration friction. Funding into BigID and similar vendors signals that investors view AI-aligned data hygiene as the next catalyst for the data residency solutions market.

Complete Report Scope:

- By Deployment Model

- On-Premises

- Public Cloud

- Hybrid

- By Tool Type

- Data Residency-as-a-Service Platforms

- Data-Privacy Management Suites

- GRC Platforms with Residency Modules

- Sovereign-Cloud Enablement Tools

- Tokenisation and Data-Vault Solutions

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-Use Industry

- BFSI

- Healthcare and Life Sciences

- Government and Public Sector

- IT and Telecom

- Retail and eCommerce

- Manufacturing and Industrial

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held a 38.2% share in 2024, anchored by the US CLOUD Act, Canada's PIPEDA, and expansive hyperscaler footprints. The region serves as a compliance testbed; multinationals refine architectures that reconcile federal, state, and sectoral statutes before rolling them out globally. Recent US policy papers on AI export controls add another jurisdictional layer that platform vendors must encode. Canada's adoption of public cloud up to Protected B classification shows how policy clarity can accelerate rollout while maintaining sovereignty controls.

Asia-Pacific is forecast to register a 28.1% CAGR, the fastest among all regions. India's Digital Personal Data Protection Act, China's Network Data Security Management regulations, and Indonesia's Personal Data Protection Law together form a harmonising backbone that simplifies regional scaling for solution providers. Massive data-centre expansion, driven by AI workloads, provides the physical substrate for residency vaults and sovereign clouds. Multinationals now treat Asia-Pacific localisation budgets as core project lines rather than contingency items, cementing the region's importance within the data residency solutions market.

Europe capitalises on GDPR maturity and hyperscaler sovereign-cloud capital expenditure. AWS's EUR 7.8 billion (USD 8.8 billion) programme includes dedicated EU-resident staff and air-gapped networks. Rising enforcement, evidenced by 2024's fine tally, keeps compliance budgets resilient. The EU AI Act extends governance to algorithmic outputs, intensifying the need for fine-grained audit trails that residency tooling can supply. In the Middle East and Africa, governments are drafting comprehensive privacy frameworks and subsidising cloud campuses to attract foreign investment, opening a greenfield for residency specialists.

- OneTrust, LLC

- TrustArc Inc.

- BigID, Inc.

- InCountry, Inc.

- Skyflow, Inc.

- Riscosity, Inc.

- Odaseva SAS

- Protegrity USA, Inc.

- Privacera, Inc.

- SecuPi Ltd.

- Immuta, Inc.

- Securiti, Inc.

- DataGrail, Inc.

- DataGuard GmbH

- Ketch, Inc.

- Delphix Corporation

- Anonos Inc.

- Data Sentinel Inc.

- Egnyte, Inc.

- Atakama Inc.

- Virtru, Inc.

- Enveil, Inc.

- Evervault Ltd.

- CryptoMove, Inc.

- StrongSalt, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of strict data-localization laws and penalties

- 4.2.2 Hyperscalers' sovereign-cloud roll-outs

- 4.2.3 Rising cost of non-compliance and cyber-breach litigation

- 4.2.4 Residency-as-a-Service platforms reach 70+ nations

- 4.2.5 AI-model localisation demands compliant data pipes

- 4.2.6 Digital-trade pacts embed sovereignty clauses

- 4.3 Market Restraints

- 4.3.1 High implementation and orchestration costs

- 4.3.2 Regulatory patchwork/ volatility across jurisdictions

- 4.3.3 Sustainability-driven data-centre repatriation risk

- 4.3.4 Trade-barrier headwinds for cross-border SaaS

- 4.4 Impact of Macroeconomic Factors

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premises

- 5.1.2 Public Cloud

- 5.1.3 Hybrid

- 5.2 By Tool Type

- 5.2.1 Data Residency-as-a-Service Platforms

- 5.2.2 Data-Privacy Management Suites

- 5.2.3 GRC Platforms with Residency Modules

- 5.2.4 Sovereign-Cloud Enablement Tools

- 5.2.5 Tokenisation and Data-Vault Solutions

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-Use Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Government and Public Sector

- 5.4.4 IT and Telecom

- 5.4.5 Retail and eCommerce

- 5.4.6 Manufacturing and Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 OneTrust, LLC

- 6.4.2 TrustArc Inc.

- 6.4.3 BigID, Inc.

- 6.4.4 InCountry, Inc.

- 6.4.5 Skyflow, Inc.

- 6.4.6 Riscosity, Inc.

- 6.4.7 Odaseva SAS

- 6.4.8 Protegrity USA, Inc.

- 6.4.9 Privacera, Inc.

- 6.4.10 SecuPi Ltd.

- 6.4.11 Immuta, Inc.

- 6.4.12 Securiti, Inc.

- 6.4.13 DataGrail, Inc.

- 6.4.14 DataGuard GmbH

- 6.4.15 Ketch, Inc.

- 6.4.16 Delphix Corporation

- 6.4.17 Anonos Inc.

- 6.4.18 Data Sentinel Inc.

- 6.4.19 Egnyte, Inc.

- 6.4.20 Atakama Inc.

- 6.4.21 Virtru, Inc.

- 6.4.22 Enveil, Inc.

- 6.4.23 Evervault Ltd.

- 6.4.24 CryptoMove, Inc.

- 6.4.25 StrongSalt, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

隱私技術(PET)市場預測至2034年-按部署類型、組織規模、技術、應用、最終用戶和地區分類的全球分析

隱私技術(PET)市場預測至2034年-按部署類型、組織規模、技術、應用、最終用戶和地區分類的全球分析 2026年全球筆記型電腦隱私螢幕市場報告2026年HIPAA(健康保險流通與責任法案)合規服務全球市場報告2026年全球監管數據市場報告資料隱私基礎設施和運算市場預測至 2034 年—按解決方案、部署類型、組織規模、最終用戶和地區分類的全球分析人工智慧資料隱私市場預測至2034年-按隱私解決方案類型、組件、部署模式、技術、最終用戶和地區分類的全球分析

2026年全球筆記型電腦隱私螢幕市場報告2026年HIPAA(健康保險流通與責任法案)合規服務全球市場報告2026年全球監管數據市場報告資料隱私基礎設施和運算市場預測至 2034 年—按解決方案、部署類型、組織規模、最終用戶和地區分類的全球分析人工智慧資料隱私市場預測至2034年-按隱私解決方案類型、組件、部署模式、技術、最終用戶和地區分類的全球分析 主權資料中心主權資料中心:市場資料概覽(2026 年第二季)

主權資料中心主權資料中心:市場資料概覽(2026 年第二季) 隱私螢幕保護貼市場:按材料、應用和地區分類2026年全球數據主權合規市場報告

隱私螢幕保護貼市場:按材料、應用和地區分類2026年全球數據主權合規市場報告