|

市場調查報告書

商品編碼

2072586

冷藏式冷卻器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Refrigeration Coolers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

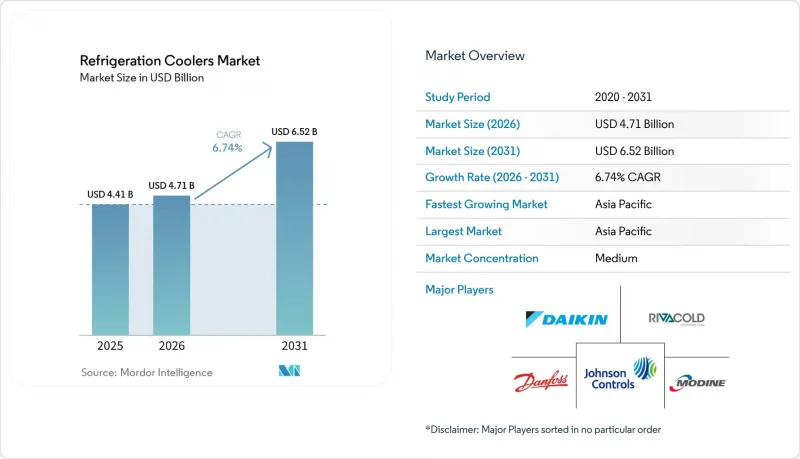

根據 Mordor Intelligence 預測,冷藏冷藏櫃市場規模將從 2025 年的 44.1 億美元和 2026 年的 47.1 億美元成長到 2031 年的 65.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.74%。

本報告按產品類型(蒸發器和空氣冷卻器、冷凝器、其他)、冷媒類型(氨、二氧化碳、其他)、終端用戶產業(食品加工、冷凍和物流、其他)、系統類型(獨立式、遠端冷凝機組、集中式機架系統、其他)和地區進行細分。市場預測以美元(USD)計價。

全球冷凍冷卻市場趨勢及洞察

低溫運輸倉庫和最後一公里冷藏物流的擴張

在經歷了亞洲、非洲和南美洲部分地區多年的投資不足之後,冷凍和冷藏設備市場正受益於溫控基礎設施領域的清晰資本投資週期。截至2025年12月31日, 開發平臺,總投資額估計達10.95億美元,涵蓋待開發區和自動化項目。隨後,在2026年5月,Americold和EQT宣布成立一家價值13億美元的合資企業,在北美建造一座冷藏倉庫。這表明,機構投資者的資金仍在推動未來多年的產能擴張。此外,由於自動化設施對溫度控制的要求比傳統倉庫更高,因此不僅對更多設備的需求不斷成長,而且對更高效能的蒸發器、控制系統和監控系統的需求也在不斷成長。因此,預計未來十年低溫運輸的擴張將成為冷凍和冷藏設備市場持續成長的需求來源。

更嚴格地逐步淘汰氫氟碳化合物,並過渡到低全球暖化潛勢冷媒

關鍵地區對低全球暖化潛勢(GWP)法規的合規期限日益縮短,也加速了冷凍和冷藏設備市場的需求。修訂後的歐盟氟化氣體法規結構加快了分階段減排的步伐,要求到2032年,功率超過40千瓦的新型集中式製冷系統的平均GWP必須低於150。這一轉變將影響整個系統的配置,因為運營商在從氫氟碳化合物(HFC)集中式製冷機組過渡到二氧化碳跨臨界或氨製冷系統時,通常需要更換壓縮機、熱交換器、控制設備和管道。在德國食品零售業,2026年初,60%的能源效率投資都用於冷凍技術,這顯示監管合規壓力正在影響資本投資的優先順序。在美國,環保署於 2026 年 5 月修訂了《AIM 法案》的某些時間表,將一些雜貨店設備的最後期限延長至 2032 年。然而,大型零售商已經決定採用二氧化碳減排的新建設,這表明冷藏展示櫃市場的市場需求已經超過了該政策設定的最低要求。

監理合規系統的維修成本和初始費用都很高。

在冷藏展示櫃市場,企業從以氫氟碳化合物(HFC)為中心的系統過渡到二氧化碳跨臨界或氨製冷系統時,仍面臨巨大的前期成本障礙。丹佛斯公司指出,跨臨界二氧化碳增壓系統的初始成本通常比同等的HFC機架系統高出15%至25%,而且在氣候溫暖的地區,由於需要額外的硬體來提高效率,這一差距還會進一步擴大。對於小規模食品零售商而言,這筆負擔尤其沉重。德國EHI零售實驗室的數據顯示,到2025年,每平方公尺的投資額將達到961歐元(約1040美元),而提交的草案根據2025年的外匯將其換算為每平方公尺1057美元。日本環境省提供最高5億日圓(約346萬美元)的津貼,根據美國國稅局2024年的平均匯率1美元兌151.98日圓(約1.06美元),提交的草案將其折算成330萬美元。然而,補貼範圍仍無法涵蓋所有企業。因此,冷藏櫃市場呈現兩極化,大型連鎖企業和物流公司率先採取行動,而小規模企業則繼續推遲更換冷藏櫃的決定。

細分市場分析

到2025年,蒸發式冷卻器和氣冷式冷卻器將佔冷凍冷卻器市場36.24%的佔有率,成為最大的產品類型。這一領先地位反映了它們在各種系統結構中的廣泛應用,從自主型展示櫃到集中控制的工業冷庫,無所不包。在冷凍冷卻器產業,隨著倉庫、超級市場或製藥冷庫等場所冷卻設備的不斷增加或升級,它們的地位也進一步鞏固。即使整個系統的升級計劃被推遲,壓縮機、冷凝器和配件仍然佔據剩餘需求的大部分,因為冷媒的更換通常需要組件層級的升級。

預計到2031年,磁控冷卻模組的複合年成長率將達到6.81%,成為冷藏展示櫃市場成長最快的產品類型。 MAGNOTHERM Solutions公司於2026年開始在REWE超市試行部署其無冷媒冷藏櫃「ECLIPSE」。 REWE計畫部署10至20台,初步的店內測試證實,與同類R290冷藏櫃相比,該冷藏櫃能夠在將產品溫度維持在目標範圍內的同時,降低15%的能耗。儘管固態冷卻技術目前市場佔有率仍然小規模,但作為一種可靠的長期解決方案,尤其是在高效商業應用場景中,固態冷卻技術正逐漸受到冷藏展示櫃市場的關注。

預計到2025年,氨製冷設備在冷凍機市場仍將佔最大佔有率,達到29.11%。這反映了氨製冷在工業冷庫、食品加工和區域冷卻領域的穩固地位。由於許多氨製冷系統設計壽命長達20至40年,即使在嚴苛的工況下也能穩定運作,因此其裝置容量保持穩定。 LU-VE推出了一款循環比低至1.8的新型氨製冷機組,顯示供應商正在拓展氨製冷系統的運作範圍,而非強制用戶完全更換現有系統。雖然HFC和HFO混合冷媒在預算有限的用戶中仍佔有一席之地,但由於逐步淘汰的趨勢,它們在製冷機市場的佔有率正在持續下降。

二氧化碳 (CO2) 是成長最快的冷媒,預計到 2031 年的複合年成長率將達到 6.95%。在歐洲,跨臨界 CO2 系統數量將在 2025 年達到 111,650 套,其中歐洲食品零售業的門市採用率將達到 34%。在北美,食品零售和工業設施的安裝量將在 2025 年達到 6,360 套,較去年同期成長 28%。 ALDI USA、Costco、Kroger、Rob Lowes 和 Target 等大型連鎖企業已決定在新建設中採用 CO2 冷媒。 Copeland 將於 2025 年 12 月推出一款具有動態蒸汽噴射功能的超臨界 CO2渦捲式壓縮機,這表明製冷市場的這一轉型不再僅僅是法規遵從問題,而是一場涵蓋組件和服務模式的廣泛平台變革。

區域分析

預計到2025年,亞太地區將佔全球冷凍冷卻市場的43.33%,到2031年將以6.88%的複合年成長率成長。該地區在製冷和冷卻市場的地位得益於冷藏倉庫建設的擴張、零售業的系統性發展以及政策支持的冷媒轉型等因素的同步推進。在日本,截至2025年,將有14,350家食品零售商使用跨臨界二氧化碳冷凍系統,便利商店和超級市場的滲透率將從2024年的16%上升至18%。 2025 年 7 月,永旺宣布其目標是在 2040 年前將其所有國內門市的冷凍設備更換為天然冷媒。日本低溫運輸從含氟冷媒過渡到天然冷媒的補貼,以及樂天全球物流計畫於 2026 年 5 月在越南同奈完成低溫運輸中心建設,都顯示公共支持和私人物流投資都在繼續擴大該地區的需求。

歐洲冷凍和冷藏市場仍成熟且活躍,已有10.6萬家食品零售店採用二氧化碳冷凍機組或冷凝機組系統,歐盟採用率達34%。此外,冷凍機組的安裝數量從2024年的7.62萬套增加到2025年的8.8萬套。麥德龍在全球對天然冷媒的採用率已達59%,歐盟已有73%的門市在使用,並計劃在2026年新增40個專案。德國的食品零售業尤其突出,該產業將60%的能源效率投資用於冷凍設備,使冷凍設備成為門市現代化改造的核心。雖然預計每平方公尺的用電量將從 2018 年的 317 千瓦時下降到 2025 年的 289 千瓦時,但製冷仍然佔食品零售業總用電量的 52%,這凸顯了為什麼現代化在冷藏市場仍然活躍。

在北美,各地區的進展不盡相同,冷藏展示櫃市場的發展更受到零售商策略的影響,而非聯邦政府對某些類別設備的最後期限延長。儘管美國環保署 (EPA) 於 2026 年 5 月對《AIM 法案》進行了修訂,將某些雜貨店設備的最後期限延長至 2032 年,但大型零售商的自願努力仍然傾向於將二氧化碳跨臨界系統作為新店的首選平台。 Americold 的 Port St. John 專案以及 Americold 與 EQT 的合資企業表明,全部區域對冷凍基礎設施的投資持續強勁。南美市場雖然規模仍然較小,但正在穩步發展,Senkosud 在五個國家的擴張表明天然冷媒模式的採用率正在不斷提高。在中東和非洲,儘管電網可靠性在一些低度開發市場仍然是一個重大限制因素,但由糧食安全驅動的潛在成長機會仍然存在。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大低溫運輸倉儲和最後一公里冷鏈物流。

- 更嚴格地逐步淘汰氫氟碳化合物,並過渡到低全球暖化潛勢冷媒

- 零售食品銷售和便利商店業態的成長

- 引入人工智慧驅動的監控和預測性維護

- R290 的最大填充容量增加,使得插入式櫃體可以更大。

- 公共資金投入和零售商店的廣泛採用將加速二氧化碳冷凍技術的普及。

- 市場限制因素

- 合規系統維修高,初始成本負擔重。

- 二氧化碳、氨氣和碳氫化合物認證技術人員短缺。

- 大規模油氣設施的建築規範應用因地區而異。

- 新興低溫運輸中電網的不穩定性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 蒸發器和空氣冷卻器

- 冷凝器

- 壓縮機

- 磁冷卻模組

- 控制設備及配件

- 其他

- 依冷媒類型

- 氨(NH3)

- 二氧化碳(CO2)

- HFC/HFO混合物

- 碳氫化合物(R-290、R-600a)

- 其他冷媒類型

- 按最終用戶行業分類

- 食品和飲料加工

- 冷凍與物流

- 超級市場和大賣場

- 製藥和生命科學

- 資料中心和電子設備的冷卻

- 其他

- 依系統類型

- 獨立式(插件)

- 遠端冷凝器單元

- 集中式貨架系統

- 混合/跨臨界二氧化碳系統

- 其他系統類型

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Daikin Industries, Ltd.

- Rivacold Srl

- Danfoss A/S

- Johnson Controls International plc

- Modine Manufacturing Company

- GEA Group Aktiengesellschaft

- Hillphoenix, Inc.

- BITZER Kuhlmaschinenbau GmbH

- Guntner GmbH & Co. KG

- EVAPCO, Inc.

- Baltimore Aircoil Company, Inc.

- LU-VE SpA

- Mayekawa Mfg. Co., Ltd.

- Hussmann Corporation

- Panasonic Holdings Corporation

- Frascold SpA

- Advansor A/S

- Arctic Industries, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the refrigeration coolers market size is projected to expand from USD 4.41 billion in 2025 and USD 4.71 billion in 2026 to USD 6.52 billion by 2031, registering a CAGR of 6.74% between 2026 and 2031.

This report is Segmented by Product Type (Evaporators and Air Coolers, Condensers, and More), Refrigerant Type (Ammonia, Carbon Dioxide, and More), End-User Industry (Food and Beverage Processing, Cold-Storage and Logistics, and More), System Type (Self-Contained, Remote Condensing Units, Centralized Rack Systems, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Refrigeration Coolers Market Trends and Insights

Expansion Of Cold-Chain Warehousing And Last-Mile Cold Logistics

The refrigeration coolers market is benefiting from a clear capital-spending cycle in temperature-controlled infrastructure, following years of underinvestment across parts of Asia, Africa, and South America. Lineage reported 83 automated warehouses and a development pipeline with an estimated total cost of USD 1.095 billion on December 31, 2025, covering both greenfield and automated projects in the United States and Europe. Americold and EQT then announced a USD 1.3 billion North American cold-storage joint venture in May 2026, which showed that institutional capital was still backing multi-year capacity growth. Automated sites also require tighter temperature consistency than conventional warehouses, which lifts demand for higher-specification evaporators, controls, and monitoring layers rather than just more equipment. This makes cold-chain build-out a durable demand source for the refrigeration coolers market through the rest of the decade.

Tightening HFC Phase-Down And Low-GWP Refrigerant Migration

Tighter low-GWP compliance deadlines in major regions are also pulling forward the refrigeration coolers market. The revised EU F-Gas framework has accelerated phase-down timelines and is pushing new centralized refrigeration systems above 40 kW toward an average GWP below 150 by 2032. That shift affects full system architecture because compressors, heat exchangers, controls, and piping often need replacement when operators move from HFC centralized racks to CO2 transcritical or ammonia-based systems. Germany's food retail sector directed 60% of its energy efficiency investment to refrigeration technology in early 2026, demonstrating how compliance pressure is shaping capex priorities. In the United States, the EPA revised certain AIM Act timelines in May 2026 and extended some grocery equipment deadlines to 2032, but large retailers were already moving ahead with CO2-based new-build decisions, indicating that market demand in the refrigeration cooler market is now running ahead of minimum policy requirements.

High Retrofit And First-Cost Burden For Compliant Systems

The refrigeration coolers market still faces a clear first-cost barrier when operators move from HFC centralized systems to CO2 transcritical or ammonia-based architectures. Danfoss noted that a transcritical CO2 booster system typically costs 15-25% more upfront than a comparable HFC rack, and the gap widens further in warm climates that require extra efficiency-support hardware. That burden is especially hard on smaller food retail operators, where Germany's EHI Retail Institute recorded investment rates of EUR 961 (USD 1,040) per square meter in 2025, which the supplied draft converted to USD 1,057 per square meter using 2025 exchange rates. Japan's Ministry of Environment offers grants of up to JPY 500 million (USD 3.46 million), which the supplied draft converted to USD 3.3 million using the IRS 2024 yearly average rate of JPY 151.98 (USD 1.06) per USD, but subsidy coverage is still not universal. This leaves the refrigeration cooler market on a two-speed path, with large chains and logistics owners moving earlier, while smaller operators continue to delay replacement decisions.

Other drivers and restraints analyzed in the detailed report include:

- Growth In Retail Food Merchandising And Convenience Formats

- AI-Enabled Monitoring And Predictive Maintenance Adoption

- Shortage Of Technicians Certified For CO2, Ammonia, And Hydrocarbons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Evaporators and air coolers accounted for 36.24% of the refrigeration cooler market in 2025, the largest share among product types. Their lead reflects their widespread use across every system architecture, from self-contained display cases to centralized industrial cold rooms. In the refrigeration coolers industry, that position is reinforced every time a warehouse, supermarket, or pharmaceutical cold room adds or replaces cooling equipment. Compressors, condensers, and accessories still account for much of the remaining demand because refrigerant transitions often require component-level upgrades, even when full-system replacement is delayed.

Magnetic cooling modules are projected to grow at a 6.81% CAGR through 2031, making them the fastest-growing product type in the refrigeration coolers market. MAGNOTHERM Solutions launched a pilot deployment of its ECLIPSE refrigerant-free cabinet in REWE stores in 2026. REWE planned 10-20 installations, and earlier in-store testing showed that the unit used 15% less energy than a comparable R290 cabinet while maintaining product temperature within the target range. The segment remains small in absolute terms, but the refrigeration coolers market is beginning to treat solid-state cooling as a credible long-range option for high-efficiency commercial use cases.

Ammonia retained the largest share at 29.11% of the refrigeration coolers market in 2025, reflecting its entrenched role in industrial cold storage, food processing, and district cooling. That installed base remains stable because many NH3 systems are designed to operate for 20-40 years under heavy-duty conditions. LU-VE reported new low-charge ammonia unit coolers with recirculation ratios as low as 1.8, demonstrating that suppliers are extending the operating range of ammonia systems rather than forcing full replacement. HFC and HFO blends still hold a place among budget-constrained operators, but the phase-down path continues to erode that position in the refrigeration coolers market.

Carbon Dioxide (CO2) is the fastest-growing refrigerant type with a 6.95% CAGR through 2031. European transcritical CO2 installations reached 111,650 sites in 2025, and penetration in European food retail rose to 34% of stores. North America reached 6,360 food retail and industrial sites in 2025 with 28% year-over-year growth, and major chains, including ALDI US, Costco, Kroger, Loblaws, and Target, had already committed to CO2 for new builds. Copeland's December 2025 launch of a transcritical CO2 scroll compressor with dynamic vapor injection showed that the refrigeration coolers market is no longer treating this shift as a narrow compliance response, but as a broader platform change across components and service models.

Complete Report Scope:

- By Product Type

- Evaporators and Air Coolers

- Condensers

- Compressors

- Magnetic Cooling Modules

- Controls and Accessories

- Other Product Types

- By Refrigerant Type

- Ammonia (NH3)

- Carbon Dioxide (CO2)

- HFC/HFO Blends

- Hydrocarbons (R-290, R-600a)

- Other Refrigerant Types

- By End-user Industry

- Food and Beverage Processing

- Cold-Storage and Logistics

- Supermarkets and Hypermarkets

- Pharmaceuticals and Life-Sciences

- Data Centres and Electronics Cooling

- Other End-user Industries

- By System Type

- Self-Contained (Plug-in)

- Remote Condensing Units

- Centralised Rack Systems

- Hybrid / Transcritical CO2 Systems

- Other System Types

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

Asia-Pacific accounted for 43.33% of the refrigeration coolers market in 2025 and is projected to grow at a 6.88% CAGR through 2031. The region's position in the refrigeration coolers market is being shaped by cold-storage build-out, organized retail expansion, and policy-backed refrigerant transitions, all occurring simultaneously. Japan had 14,350 food retail stores using transcritical CO2 systems in 2025, and penetration in convenience stores and supermarkets rose to 18% from 16% in 2024. In July 2025, AEON said it aims to shift all domestic store refrigeration equipment to natural refrigerants by 2040. Japan's cold-chain de-fluorination subsidy and Lotte Global Logistics' May 2026 completion of its Dong Nai Cold Chain Center in Vietnam show that both public support and private logistics investment are still expanding regional demand.

Europe is a mature but still very active part of the refrigeration coolers market, with 106,000 food retail outlets already using CO2 rack or condensing-unit systems and EU-wide penetration at 34%, while rack installations rose from 76,200 sites in 2024 to 88,000 in 2025. METRO's global natural refrigerant penetration reached 59%, and 73% of its EU stores were already on natural refrigerants, with 40 more projects planned in 2026. Germany stands out because food retail directed 60% of energy-efficiency investment to refrigeration, keeping this equipment category at the center of store modernization. Electricity use per square meter fell from 317 kWh in 2018 to 289 kWh in 2025, yet refrigeration still accounted for 52% of total food retail electricity use, underscoring why modernization remains active in the refrigeration market.

North America is moving at a differentiated pace, and the refrigeration coolers market there is being shaped more by retailer strategy than by the extended federal timelines in some categories. The EPA's May 2026 AIM Act revision extended certain grocery equipment deadlines to 2032, but voluntary commitments from large retailers continued to support CO2 transcritical as the preferred platform for new stores. Americold's Port Saint John project and the Americold-EQT joint venture point to continued strength in cold-storage infrastructure spending across the region. South America remains smaller but is still advancing, while Cencosud's rollout across 5 countries shows the natural-refrigerant model is spreading, and the Middle East and Africa continue to offer food security-led potential even as grid reliability remains a real constraint in several underdeveloped markets.

- Daikin Industries, Ltd.

- Rivacold S.r.l.

- Danfoss A/S

- Johnson Controls International plc

- Modine Manufacturing Company

- GEA Group Aktiengesellschaft

- Hillphoenix, Inc.

- BITZER Kuhlmaschinenbau GmbH

- Guntner GmbH & Co. KG

- EVAPCO, Inc.

- Baltimore Aircoil Company, Inc.

- LU-VE S.p.A.

- Mayekawa Mfg. Co., Ltd.

- Hussmann Corporation

- Panasonic Holdings Corporation

- Frascold S.p.A.

- Advansor A/S

- Arctic Industries, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Cold-Chain Warehousing and Last-Mile Cold Logistics

- 4.2.2 Tightening HFC Phase-Down and Low-GWP Refrigerant Migration

- 4.2.3 Growth in Retail Food Merchandising and Convenience Formats

- 4.2.4 AI-Enabled Monitoring and Predictive Maintenance Adoption

- 4.2.5 Higher R290 Charge Limits Enabling Larger Plug-In Cabinets

- 4.2.6 Public Funding and Retail Rollouts Accelerating CO2 Refrigeration Adoption

- 4.3 Market Restraints

- 4.3.1 High Retrofit and First-Cost Burden for Compliant Systems

- 4.3.2 Shortage of Technicians Certified for CO2, Ammonia, and Hydrocarbons

- 4.3.3 Patchy Building Code Adoption for Larger Hydrocarbon Charges

- 4.3.4 Grid Instability in Emerging Cold Chains

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Evaporators and Air Coolers

- 5.1.2 Condensers

- 5.1.3 Compressors

- 5.1.4 Magnetic Cooling Modules

- 5.1.5 Controls and Accessories

- 5.1.6 Other Product Types

- 5.2 By Refrigerant Type

- 5.2.1 Ammonia (NH3)

- 5.2.2 Carbon Dioxide (CO2)

- 5.2.3 HFC/HFO Blends

- 5.2.4 Hydrocarbons (R-290, R-600a)

- 5.2.5 Other Refrigerant Types

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage Processing

- 5.3.2 Cold-Storage and Logistics

- 5.3.3 Supermarkets and Hypermarkets

- 5.3.4 Pharmaceuticals and Life-Sciences

- 5.3.5 Data Centres and Electronics Cooling

- 5.3.6 Other End-user Industries

- 5.4 By System Type

- 5.4.1 Self-Contained (Plug-in)

- 5.4.2 Remote Condensing Units

- 5.4.3 Centralised Rack Systems

- 5.4.4 Hybrid / Transcritical CO2 Systems

- 5.4.5 Other System Types

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Turkey

- 5.5.4.4 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries, Ltd.

- 6.4.2 Rivacold S.r.l.

- 6.4.3 Danfoss A/S

- 6.4.4 Johnson Controls International plc

- 6.4.5 Modine Manufacturing Company

- 6.4.6 GEA Group Aktiengesellschaft

- 6.4.7 Hillphoenix, Inc.

- 6.4.8 BITZER Kuhlmaschinenbau GmbH

- 6.4.9 Guntner GmbH & Co. KG

- 6.4.10 EVAPCO, Inc.

- 6.4.11 Baltimore Aircoil Company, Inc.

- 6.4.12 LU-VE S.p.A.

- 6.4.13 Mayekawa Mfg. Co., Ltd.

- 6.4.14 Hussmann Corporation

- 6.4.15 Panasonic Holdings Corporation

- 6.4.16 Frascold S.p.A.

- 6.4.17 Advansor A/S

- 6.4.18 Arctic Industries, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

冷凍冷卻器市場分析及預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝配置、解決方案、模式

冷凍冷卻器市場分析及預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝配置、解決方案、模式 冷藏冷卻器市場:2026-2032年全球市場預測(依產品類型、溫度範圍、應用、最終用戶及銷售管道)製冰機過濾器市場:依產品類型、材料、安裝方式、應用領域、最終用戶、通路分類,全球預測(2026-2032)吧台後部貫通式冷藏庫市場:按類型、容量、冷卻方式、安裝方式、最終用戶、分銷管道分類,全球預測(2026-2032年)行動式冷凍機組市場:依溫度範圍、燃料類型、安裝方式、應用和最終用戶分類,全球預測,2026-2032年吧台冷藏櫃市場:依產品類型、最終用戶和通路分類,全球預測(2026-2032年)快速玻璃冷卻器市場:依產品類型、最終用戶、技術、價格範圍和分銷管道分類,全球預測,2026-2032年玻璃冷卻器市場:按冷卻器類型、技術、容量、最終用戶和分銷管道分類,全球預測(2026-2032年)製冰機市場:依冰型、最終用戶、安裝類型、通路、技術和產能分類,全球預測,2026-2032年

冷藏冷卻器市場:2026-2032年全球市場預測(依產品類型、溫度範圍、應用、最終用戶及銷售管道)製冰機過濾器市場:依產品類型、材料、安裝方式、應用領域、最終用戶、通路分類,全球預測(2026-2032)吧台後部貫通式冷藏庫市場:按類型、容量、冷卻方式、安裝方式、最終用戶、分銷管道分類,全球預測(2026-2032年)行動式冷凍機組市場:依溫度範圍、燃料類型、安裝方式、應用和最終用戶分類,全球預測,2026-2032年吧台冷藏櫃市場:依產品類型、最終用戶和通路分類,全球預測(2026-2032年)快速玻璃冷卻器市場:依產品類型、最終用戶、技術、價格範圍和分銷管道分類,全球預測,2026-2032年玻璃冷卻器市場:按冷卻器類型、技術、容量、最終用戶和分銷管道分類,全球預測(2026-2032年)製冰機市場:依冰型、最終用戶、安裝類型、通路、技術和產能分類,全球預測,2026-2032年 冷凍與冷卻市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、冷媒類型、最終用戶產業、地區和競爭對手分類,2021-2031年

冷凍與冷卻市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、冷媒類型、最終用戶產業、地區和競爭對手分類,2021-2031年