|

市場調查報告書

商品編碼

2072535

歐洲生質乙醇:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Europe Bioethanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

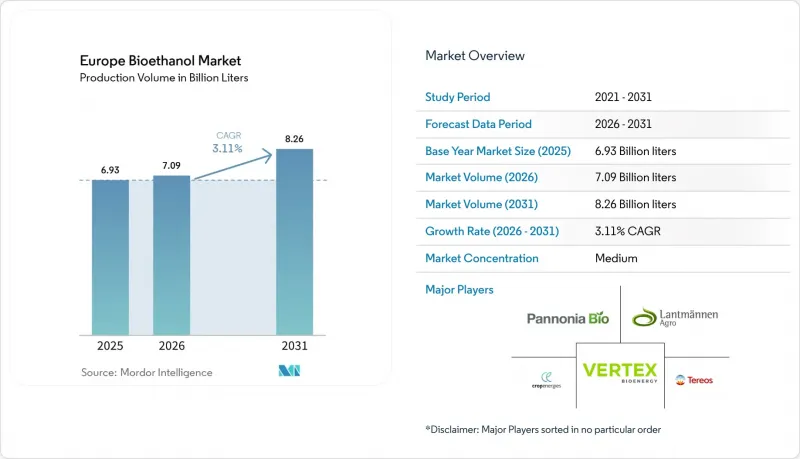

根據 Mordor Intelligence 預測,歐洲生質乙醇市場(以產量計算)預計將從 2025 年的 69.3 億公升成長到 2026 年的 70.9 億公升,然後從 2026 年到 2031 年以 3.11% 的複合年成長,到 2031 年達到 82.

本報告按原料(小麥、玉米、糖、木質纖維素殘渣等)、應用領域(燃料混合物、食品飲料、藥品、化妝品和個人護理用品等)以及地區(德國、英國、法國、西班牙、義大利、北歐國家、荷蘭、波蘭等)進行細分。市場規模和預測以產量(公升)為單位。

歐洲生質乙醇市場的趨勢與洞察

強制實施 RED III 將增加可再生燃料的分配。

修訂後的RED III指令將使可再生能源在運輸領域的比例在2030年達到29%。如果目前的混合比例不變,這將新增12億公升乙醇需求。法國和德國已發布國家實施藍圖,優先考慮遵守乙醇法規;西班牙和義大利計畫在2026年前完成藍圖。先進生質燃料的子目標允許對秸稈基生物乙醇生產進行雙重計算,這使得資金轉移到能夠與合規機構簽訂溢價收購合約的第二代生物乙醇工廠。因此,獲得低間接土地利用變化(ILUC)殘留物認證的生產商享有結構性利潤優勢,並能有效抵禦糧食價格波動的影響。這種監管確定性正在推動歐洲生質乙醇市場的穩定擴張。

在其他歐盟成員國引入E10/E85

波蘭在2024年底前完成了全國的E10加油站轉換,新增8000個加油站,預計2025年波蘭國內生質乙醇消費量將比上一年成長15%。西班牙緊隨其後,於2025年初完成轉換,雷普索爾(Repsol)和塞普薩(Cepsa)兩大能源公司對其60%的銷售網點維修。預計到2027年,這項轉變將額外滿足2億公升的需求。德國啟動了津貼計劃,用於維修2000個加油站,使其符合E85標準,從而將其靈活燃料網路擴展到法國和瑞典以外的地區。隨著碳權額度轉移和消費稅的降低,E85的經濟吸引力日益增強,預計到2025年,其與E10的價格差將擴大至每公升0.20歐元。基礎設施的擴建將打破混合比例的限制,並支撐歐洲生質乙醇市場預計3.11%的複合年成長率。

原物料價格波動與「糧食與燃料」之爭

2025年,歐洲小麥的交易價格在每噸210歐元至280歐元之間波動,30%的價格波動給那些沒有避險能力的工廠帶來了利潤壓力。南歐的乾旱再次引發了「糧食與燃料」之爭,非政府組織批評將糧食轉用於乙醇生產。 RED III將農作物衍生生質燃料的產量限制在2020年的水平,但在西班牙和義大利,政治審查仍然嚴格,這兩個國家的麵包小麥價格在2025年中期飆升。大型公司已簽署多年期糧食合約並在其廠區內建立了倉儲設施,但財務基礎較弱的小規模釀酒廠正面臨利潤壓力,這加速了行業的整合。因此,原物料價格的波動限制了歐洲生質乙醇市場的成長潛力。

細分市場分析

到2025年,隨著匈牙利、羅馬尼亞和中歐地區大規模乾磨設施的建成,玉米將佔歐洲生質乙醇產量的50.2%。這一壓倒性佔有率凸顯了玉米在歐洲生質乙醇產業中的關鍵作用。同時,預計到2031年,木質纖維素殘渣的年複合成長率將達到6.2%。這一成長主要得益於生產商為應對日益嚴格的脫碳法規,擴大了利用農業廢棄物和林產品生產先進乙醇的規模。小麥是法國、德國和英國的主要原料,受益於與製粉基礎設施的整合以及靈活的原料經濟。糖的生產則得益於當地農業相關企業營運的甜菜加工和共發酵設施的優勢。此外,其他原料還包括在試驗和商業規模設施中加工的混合生質能和特殊農業殘渣。

第二代生質乙醇生產受益於碳權額的雙重計算,其溢價足以抵消高昂的資本投資成本,從而降低了在碳定價法規嚴格的地區小麥的獲利能力。 Verbio 的模組化方案將秸稈收集與現有蒸餾生產線整合,與待開發區專案相比,降低了投資門檻,每個 5 萬噸模組的成本為 1.5 億至 2 億歐元(約 1.74 億至 2.32 億美元)。 CropEnergies 計劃在其 Zeitz 工廠複製這一模式,到 2027 年新增 3 萬噸先進產能。雖然預計玉米在 2031 年之前仍將佔據歐洲生質乙醇市場的最大佔有率,但隨著木質纖維素殘渣市場佔有率的成長,其主導地位將會減弱,而這主要得益於碳減排目標和原料多元化策略的推動。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- RED III 的強制實施增加了可再生燃料的分配。

- 其他歐盟成員國引入E10和E85

- 碳定價和溫室氣體排放額度溢價提高了乙醇的經濟可行性。

- 將酒精燃料轉化為噴射燃料的途徑整合到「歐盟航空燃料再利用計畫」中

- 將發酵過程中所獲得的「綠色」二氧化碳貨幣化

- 富含蛋白質的產品正在提高綜合生物煉製廠的利潤率。

- 市場限制因素

- 原物料價格波動與「糧食與燃料」之爭

- 遵守ILUC係數會增加認證成本。

- 能源價格的劇烈波動給蒸餾行業的獲利能力帶來了壓力。

- 預計有關電動車和電子燃料的政策將抑制汽油的長期供應。

- 供應鏈分析

- 監理情勢

- 技術趨勢(1G 與 2G,ATJ)

- 波特五力模型

第5章 市場規模與成長預測

- 按原料

- 小麥

- 玉米

- 木質纖維素殘渣

- 糖

- 其他

- 透過使用

- 燃料混合物(用於運輸)

- 食品和飲料(烈酒、萃取物)

- 製藥

- 化妝品和個人護理

- 其他

- 按地區

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 北歐國家

- 荷蘭

- 波蘭

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- CropEnergies AG

- Vertex Bioenergy

- Tereos SCA

- Pannonia Bio Zrt.

- Lantmannen Agroetanol

- Abengoa

- ADM

- AGRANA Beteiligungs-AG

- Cargill

- ALCOGROUP SA

- Anora Group Plc

- BIOAGRA SA

- Verbio SE

- Clariant AG

- British Sugar plc

- Vivergo Fuels

- BioWanze SA

- Euro Ethyl Ltd.

- Essentica Ltd.

- Tereos Syral(France)

- Ryssen Alcool(France)

- Sekab E-Technology AB

- Green Biologics Ltd.

- Ryazan(Valio Biofuels)

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe bioethanol market size in terms of production volume is expected to grow from 6.93 Billion liters in 2025 to 7.09 Billion liters in 2026 and is forecast to reach 8.26 Billion liters by 2031 at 3.11% CAGR over 2026-2031.

This report is Segmented by Feedstock (Wheat, Corn, Sugars, Lignocellulosic Residues, and Other), Application (Fuel Blending, Food and Beverages, Pharmaceuticals, Cosmetics and Personal Care, and Others), and Geography (Germany, United Kingdom, France, Spain, Italy, NORDIC Countries, Netherlands, Poland, and More). The Market Sizes and Forecasts are Provided in Terms of Production Volume (Liters).

Europe Bioethanol Market Trends and Insights

RED III Mandates Raise Renewable-Fuel Quotas

Revised RED III lifts the renewable share in transport to 29% by 2030, triggering incremental demand for 1.2 billion liters of ethanol if current blend levels persist. France and Germany have already published national transposition roadmaps that emphasize ethanol compliance, while Spain and Italy intend to finalize theirs in 2026. Advanced-biofuel sub-targets grant double counting for straw-based volumes, shifting capital toward second-generation plants that can lock in premium off-take contracts with obligated parties. Producers that certify low-ILUC residues therefore enjoy structural margin advantages, cushioning them against grain-price swings. This regulatory certainty underpins the steady expansion of the European bioethanol market.

Roll-Out of E10 / E85 Across Additional EU States

Poland completed nationwide E10 pump conversions in late 2024, adding 8,000 dispensers and lifting domestic bioethanol use by 15% year on year in 2025. Spain followed in early 2025 as Repsol and Cepsa upgraded 60% of their outlets, a change that is expected to absorb an extra 200 million liters by 2027. Germany launched a grant program to retrofit 2,000 stations for E85, broadening the flex-fuel network beyond France and Sweden. Carbon-credit transfers and lower excise taxes make E85 economically attractive, widening the price gap with E10 to €0.20 per liter in 2025. Expanded infrastructure removes blend-wall constraints, supporting the projected 3.11% CAGR of the European bioethanol market.

Feedstock-Price Volatility and Food-Versus-Fuel Debate

European wheat traded between €210 and €280 per ton in 2025, a 30% swing that compressed margins for plants lacking hedging capacity. Drought in Southern Europe rekindled the food-fuel debate as NGOs criticized the diversion of cereals to ethanol. RED III caps crop-based biofuels at 2020 levels, yet political scrutiny remains high in Spain and Italy, where bread-wheat prices spiked during mid-2025. Larger players lock multiyear grain contracts and build on-site storage, but small distillers without balance-sheet strength face margin squeezes that accelerate consolidation. Volatile feedstock, therefore, restricts upside for the European bioethanol market.

Other drivers and restraints analyzed in the detailed report include:

- Carbon-Pricing and GHG-Credit Premiums Enhance Economics

- Alcohol-to-Jet Pathway Inclusion in ReFuelEU Aviation

- ILUC-Factor Compliance Increases Certification Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, corn accounted for 50.2% of bioethanol production in Europe, bolstered by extensive dry-mill facilities in Hungary, Romania, and Central Europe. This dominance underscores corn's pivotal role in Europe's bioethanol landscape. Meanwhile, lignocellulosic residues are projected to grow at a 6.2% CAGR through 2031. This surge is driven by producers ramping up advanced ethanol production from agricultural waste and forestry by-products, all in a bid to align with tightening decarbonization mandates. Wheat, a key feedstock in France, Germany, and the UK, enjoys advantages from its integration with milling infrastructure and adaptable feedstock economics. Sugars benefit from sugar beet processing and co-fermentation perks at facilities run by local agribusinesses. Additionally, other feedstocks encompass mixed biomass and specialized agricultural residues, processed at both pilot and commercial-scale facilities.

Second-generation output enjoys double-counting credits and commands price premiums that offset higher capex, eroding wheat's margin advantage where carbon pricing is stringent. Verbio's modular approach, integrating straw collection with existing distillation trains at EUR 150-200 million (~ USD 174-232 million) per 50,000-ton module, lowers investment hurdles compared with greenfield builds. CropEnergies will replicate the model at its Zeitz site, adding 30,000 tons of advanced capacity by 2027. While corn is set to command the largest share of Europe's bioethanol market until 2031, its dominance will wane as lignocellulosic residues capture an increasing share, propelled by carbon reduction goals and strategies for feedstock diversification.

Complete Report Scope:

- By Feedstock

- Wheat

- Corn

- Lignocellulosic Residues

- Sugars

- Other

- By Application

- Fuel Blending (Transportation)

- Food and Beverages (Spirits, Extracts)

- Pharmaceuticals

- Cosmetics and Personal Care

- Others

- By Geography

- Germany

- United Kingdom

- France

- Spain

- Italy

- NORDIC Countries

- Netherlands

- Poland

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- CropEnergies AG

- Vertex Bioenergy

- Tereos SCA

- Pannonia Bio Zrt.

- Lantmannen Agroetanol

- Abengoa

- ADM

- AGRANA Beteiligungs-AG

- Cargill

- ALCOGROUP SA

- Anora Group Plc

- BIOAGRA S.A.

- Verbio SE

- Clariant AG

- British Sugar plc

- Vivergo Fuels

- BioWanze SA

- Euro Ethyl Ltd.

- Essentica Ltd.

- Tereos Syral (France)

- Ryssen Alcool (France)

- Sekab E-Technology AB

- Green Biologics Ltd.

- Ryazan (Valio Biofuels)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 RED III mandates raise renewable-fuel quotas

- 4.2.2 Roll-out of E10/E85 across additional EU states

- 4.2.3 Carbon-pricing & GHG-credit premiums enhance ethanol economics

- 4.2.4 Alcohol-to-Jet pathway inclusion in ReFuelEU Aviation

- 4.2.5 Monetisation of "green" CO2 from fermentation streams

- 4.2.6 Protein-rich co-products boost integrated biorefinery margins

- 4.3 Market Restraints

- 4.3.1 Feedstock-price volatility & food-versus-fuel debate

- 4.3.2 ILUC-factor compliance increases certification costs

- 4.3.3 High energy-price swings hit distillation economics

- 4.3.4 EV & e-fuel policy signals cap long-term gasoline pool

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (1G vs 2G, ATJ)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Feedstock

- 5.1.1 Wheat

- 5.1.2 Corn

- 5.1.3 Lignocellulosic Residues

- 5.1.4 Sugars

- 5.1.5 Other

- 5.2 By Application

- 5.2.1 Fuel Blending (Transportation)

- 5.2.2 Food and Beverages (Spirits, Extracts)

- 5.2.3 Pharmaceuticals

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 NORDIC Countries

- 5.3.7 Netherlands

- 5.3.8 Poland

- 5.3.9 Russia

- 5.3.10 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 CropEnergies AG

- 6.4.2 Vertex Bioenergy

- 6.4.3 Tereos SCA

- 6.4.4 Pannonia Bio Zrt.

- 6.4.5 Lantmannen Agroetanol

- 6.4.6 Abengoa

- 6.4.7 ADM

- 6.4.8 AGRANA Beteiligungs-AG

- 6.4.9 Cargill

- 6.4.10 ALCOGROUP SA

- 6.4.11 Anora Group Plc

- 6.4.12 BIOAGRA S.A.

- 6.4.13 Verbio SE

- 6.4.14 Clariant AG

- 6.4.15 British Sugar plc

- 6.4.16 Vivergo Fuels

- 6.4.17 BioWanze SA

- 6.4.18 Euro Ethyl Ltd.

- 6.4.19 Essentica Ltd.

- 6.4.20 Tereos Syral (France)

- 6.4.21 Ryssen Alcool (France)

- 6.4.22 Sekab E-Technology AB

- 6.4.23 Green Biologics Ltd.

- 6.4.24 Ryazan (Valio Biofuels)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

生質乙醇酵母市場規模、佔有率和成長分析:按產品類型、原料類型、應用、終端用戶產業、形態、發酵製程和地區分類-2026-2033年產業預測

生質乙醇酵母市場規模、佔有率和成長分析:按產品類型、原料類型、應用、終端用戶產業、形態、發酵製程和地區分類-2026-2033年產業預測 生物液體熱電發電市場:依技術、容量範圍、原料、應用和最終用途分類-2026-2032年全球市場預測生質乙醇市場:依原料、製造技術、混合類型、等級、通路和最終用途分類-2026-2032年全球市場預測生物丁醇市場:2026-2032年全球市場預測(依產品類型、原料、生產流程、應用、終端用戶產業及通路分類)

生物液體熱電發電市場:依技術、容量範圍、原料、應用和最終用途分類-2026-2032年全球市場預測生質乙醇市場:依原料、製造技術、混合類型、等級、通路和最終用途分類-2026-2032年全球市場預測生物丁醇市場:2026-2032年全球市場預測(依產品類型、原料、生產流程、應用、終端用戶產業及通路分類) 生物丁醇市場報告:按原料、應用、終端用戶產業和地區分類(2026-2034 年)生質乙醇市場規模、佔有率、趨勢和預測:按類型、燃料混合物、生產方法、最終用途行業和地區分類,2026-2034年生質乙醇酵母市場:2026-2032年全球市場預測(按產品類型、配方類型、技術、應用和最終用戶產業分類)

生物丁醇市場報告:按原料、應用、終端用戶產業和地區分類(2026-2034 年)生質乙醇市場規模、佔有率、趨勢和預測:按類型、燃料混合物、生產方法、最終用途行業和地區分類,2026-2034年生質乙醇酵母市場:2026-2032年全球市場預測(按產品類型、配方類型、技術、應用和最終用戶產業分類) 2026年全球生質乙醇酵母市場報告2026年全球生質乙醇市場報告生質乙醇交通運輸市場:依原料、純度、製造技術、應用及通路分類-2026-2032年全球市場預測

2026年全球生質乙醇酵母市場報告2026年全球生質乙醇市場報告生質乙醇交通運輸市場:依原料、純度、製造技術、應用及通路分類-2026-2032年全球市場預測