|

市場調查報告書

商品編碼

2072502

耐腐蝕樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Corrosion-resistant Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

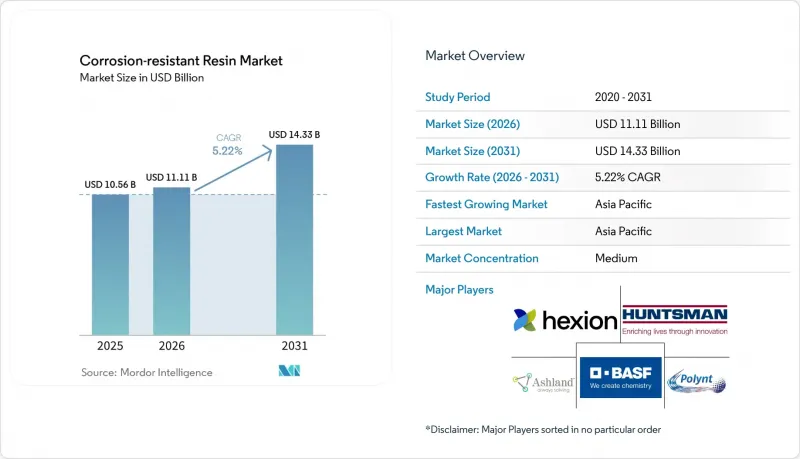

據 Mordor Intelligence 稱,耐腐蝕樹脂市場預計到 2026 年價值 111.1 億美元,高於 2025 年的 105.6 億美元,預計到 2031 年將達到 143.3 億美元。

預計 2026 年至 2031 年的複合年成長率為 5.22%。

本報告按樹脂類型(環氧樹脂、乙烯基酯樹脂、聚酯樹脂、聚氨酯樹脂及其他)、應用領域(複合材料、塗料及其他)、終端用戶行業(汽車及交通運輸、基礎設施、船舶、石油天然氣及其他)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球耐腐蝕樹脂市場趨勢及洞察

環氧樹脂需求不斷成長

隨著奈米二氧化矽填充基體提供更優異的阻隔性能和更長的維護週期,環氧樹脂不斷革新腐蝕管理領域。螢光塗層能夠直覺地偵測微裂紋,為海上平台等檢查機會有限的場所提供預防性維護支援。監管機構對永續性的重視推動了植物油基環氧樹脂的商業化應用,在維持現有機械性能的同時,也能減少碳排放。能夠響應溫度快速升高而觸發抑制劑釋放的自修復技術,進一步鞏固了環氧樹脂作為下一代防護系統基石的地位。這些技術的進步共同提高了重工業終端使用者的設備運作,並降低了整體擁有成本 (TCO)。

石油和天然氣管道腐蝕導致資本支出 (CAPEX) 和營運支出 (OPEX) 增加。

管線營運商每年面臨約13.72億美元的腐蝕成本,促使他們採用非金屬管線網路和先進的富樹脂襯裡。沙烏地阿美公司已在沙漠和海洋環境中安裝了超過1萬公里的增強型熱塑性管道,以減輕脫臭氣腐蝕。新型樹脂系統能夠承受198.33兆帕和352.25度C的地下環境,從而能夠完成深層儲存的開採,並減少因油管故障造成的停機時間。利用響應曲面法進行腐蝕建模,工程師可以根據局部氯化物和二氧化碳濃度選擇合適的樹脂,從而降低生命週期成本並提高安全性。這些經濟效益正推動各大能源公司持續採購高性能耐腐蝕樹脂解決方案。

REACH 和 TSCA 中雙酚 A 的重新分類

歐洲大幅降低雙酚A (BPA) 的可接受攝取量,以及美國對亞洲環氧樹脂進口徵收反傾銷稅,迫使配方開發商轉向使用不含BPA的化學成分。剪切機司和PPG工業公司目前銷售不含BPA的容器內襯,而Rocket公司的異山梨醇基固化劑在保持耐化學性的同時,也避免了內分泌干擾問題。過渡期內的供應不確定性可能會增加生產成本,並延長航太和食品接觸應用領域新產品的認證週期。

細分市場分析

預計到2025年,環氧樹脂將佔據耐腐蝕樹脂市場42.38%的佔有率。這主要得益於其優異的黏合強度、化學惰性以及在海洋、石油天然氣和基礎設施項目中的廣泛應用。添加雙矽烷改質劑的環氧樹脂配方在鹽霧試驗後可達到超過90%的自癒率,從而延長海上設備的維護週期。聚氨酯的複合年成長率(CAGR)為5.74%,這反映了其快速固化的特性,可縮短葉片生產週期並減少模具投入,因此促進了其在百米級風力渦輪機葉片中的應用。乙烯基酯在化學品儲罐製造領域保持著強勁的地位,因為其酯鍵能夠抵抗腐蝕傳統聚酯的酸和溶劑。

新興的智慧樹脂平台整合了螢光示踪劑,能夠可視化早期裂紋,並具備溫度響應型抑制劑釋放功能,從而支援預測性維護計劃,可將煉油廠運營商的意外停機時間減少高達 25%。這些進步進一步鞏固了環氧樹脂的高階地位,即便其他化學品正在迅速縮小性能差距。

區域分析

亞太地區正鞏固其主導地位,預計2025年將佔全球耐腐蝕樹脂市場銷售額的38.21%,並預計在2031年前以6.35%的複合年成長率持續成長。在中國,每年新增超過30吉瓦的風力發電設備,推動了葉片和機艙用玻璃纖維環氧樹脂的大量消耗。在印度,Kineko Excel對維斯塔斯(Vestas)碳纖維板的契約製造特別引人注目,這表明印度先進複合材料的本地附加價值不斷提升。台灣的Swanko公司為該地區的離岸風力發電專案供應超過50%的材料,反映了該地區供應鏈的成熟度。

北美正透過技術創新和貿易政策來滿足市場需求。美國對部分亞洲環氧樹脂進口徵收反傾銷稅,既保護了美國本土企業,也鼓勵了產能提升,從而確保了國防和基礎設施應用領域的穩定供應。埃克森美孚與麥克拉倫複合材料公司在聚烯熱固性樹脂領域的合作,凸顯了該地區在推廣低碳替代材料的同時,努力維持材料拉伸性能的努力。BASF已營運多家運作再生能源的塗料工廠,在降低範圍2排放的同時,維持了加工能力。

歐洲優先考慮永續性和監管領導地位,並在嚴格的化學品註冊、評估、授權和限制(REACH)框架下,快速實現不含雙酚A(BPA)的環氧樹脂和生物基中間體的商業化。在中東和非洲,透過在地化專案(例如Sadara的「PlasChem Park」防腐蝕產品專案)推動成長,而阿拉伯聯合大公國正憑藉Strata Solvay的預浸料生產設施,將自身打造成為航太材料供應商中心。在南美洲,工業化和港口現代化使樹脂需求保持適度成長,但該地區在複合材料專業技術方面較為落後,並且仍然依賴進口關鍵中間體。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 環氧樹脂需求增加

- 石油和天然氣管道腐蝕導致資本支出 (CAPEX) 和營運支出 (OPEX) 增加。

- 風力渦輪機葉片複合材料減重趨勢

- 水性乙烯基酯塗料在船舶領域的主流化

- 在中東的儲槽區附近,本地樹脂混合企業正在湧現。

- 市場限制因素

- 基於REACH和TSCA對雙酚A進行重新分類

- MDI價格波動

- 中東和非洲地區缺乏熟練的複合材料加工技術人員

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 環氧樹脂

- 乙烯基酯

- 聚酯纖維

- 聚氨酯

- 其他

- 透過使用

- 複合材料

- 塗層

- 其他(黏合劑和襯裡材料)

- 按最終用戶行業分類

- 汽車和運輸業

- 食品/飲料

- 產業

- 基礎設施

- 海上

- 石油和天然氣

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Aditya Birla Chemicals

- AOC Resins

- Ashland Inc.

- BASF SE

- DIC Corporation

- Guangdong Yinyang Environment-Friendly New Materials Co., Ltd.

- Hexion Inc.

- Huntsman Corporation

- Olin Corporation

- Polynt-Reichhold Group

- Resonac

- Scott Bader Co. Ltd.

- Sino Polymer Co. Ltd.

- Sir Industriale

第7章 市場機會與未來展望

According to Mordor Intelligence, the corrosion-resistant resin market size in 2026 is estimated at USD 11.11 Billion, growing from 2025 value of USD 10.56 Billion with 2031 projections showing USD 14.33 Billion, growing at 5.22% CAGR over 2026-2031.

This report is Segmented by Resin Type (Epoxy, Vinyl Ester, Polyester, Polyurethane, and Others), Application (Composites, Coatings, and Others), End-User Industry (Automotive and Transportation, Infrastructure, Marine, Oil and Gas, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Corrosion-resistant Resin Market Trends and Insights

Increasing Demand for Epoxy Resins

Epoxy resins continue to redefine corrosion management because nano-silica-filled matrices are delivering higher barrier performance and longer service intervals. Fluorescence-enabled coatings allow visual detection of microcracks, supporting proactive maintenance on offshore platforms where inspection windows are limited . Regulators' focus on sustainability is catalyzing commercial roll-out of vegetable-oil-derived epoxies that match incumbent mechanical properties while lowering carbon footprints. Self-healing chemistries that trigger inhibitor release in response to temperature spikes are further positioning epoxies as the workhorse for next-generation protective systems. Collectively, these advances boost asset uptime and compress total cost of ownership for heavy-industry end-users.

Rising Corrosion-related CAPEX (Capital Expenditures) and OPEX (Operational Expenditures) in Oil & Gas Pipelines

Pipeline operators confront corrosion costs of roughly USD 1.372 Billion annually, prompting adoption of nonmetallic pipe networks and advanced resin-rich liners. Aramco has already installed over 10,000 km of reinforced thermoplastic pipe to mitigate sweet-gas corrosion in desert and offshore environments. New resin systems qualified for 198.33 MPa and 352.25°C downhole conditions are unlocking deep-reservoir completions while reducing downtime linked to tubing failures. Response-surface corrosion modelling lets engineers tailor resin selection to local chloride and CO2 levels, lowering lifecycle spend and enhancing safety metrics. These economics underpin sustained purchasing of high-performance corrosion-resistant resin market solutions by energy majors.

REACH and TSCA Re-classification of Bisphenol-a

Europe's sharp reduction of Bisphenol-A (BPA) tolerable daily intake and the United States' antidumping levies on Asian epoxy imports are forcing formulators to pivot toward Bisphenol A (BPA)-free chemistries. Sherwin-Williams and PPG Industries, Inc. now market non-Bisphenol A (BPA) container linings, while Roquette's isosorbide-based hardeners preserve chemical resistance without endocrine-disruption concerns . Supply uncertainty during the transition period elevates production costs and may slow qualification cycles for new aerospace and food-contact applications.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Trend in Wind-blade Composites

- Mainstream Shift to Water-borne Vinyl-ester Systems in Marine

- Volatile MDI Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The epoxy segment commanded 42.38% of the Corrosion-resistant Resin market share in 2025, anchored by its bonding strength, chemical inertness, and adaptability across marine, oil and gas, and infrastructure projects. Epoxy-based formulations infused with bis-silane modifiers now achieve self-healing rates above 90% after salt-spray exposure, extending maintenance intervals for offshore installations. Polyurethane's 5.74% CAGR reflects its rapid curing, which cuts blade cycle times and lowers capital tied up in molds, propelling its use in 100-m class wind blades. Vinyl esters retain a foothold in chemical-tank fabrication because their ester linkage tolerates acids and solvents that attack conventional polyesters.

Emerging smart-resin platforms integrate fluorescent tracers for early-stage crack visibility and temperature-responsive inhibitor release, supporting predictive maintenance programs that slash unplanned downtime by up to 25% for refinery operators. These advances reinforce epoxy's premium positioning even as alternative chemistries race to close performance gaps.

Complete Report Scope:

- By Resin Type

- Epoxy

- Vinyl Ester

- Polyester

- Polyurethane

- Others

- By Application

- Composites

- Coatings

- Others (Adhesives & Linings)

- By End-User Industry

- Automotive and Transportation

- Food and Beverage

- Industrial

- Infrastructure

- Marine

- Oil and Gas

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Geography Analysis

Asia Pacific accounted for 38.21% of the Corrosion-resistant Resin market revenue in 2025 and is projected to expand at a 6.35% CAGR to 2031, cementing its leadership position. China's annual installation of over 30 GW of new wind capacity drives bulk consumption of glass-fiber-epoxy resins for blades and nacelles. India's contract manufacturing, highlighted by Kineco Exel's qualification for Vestas carbon-fiber planks, signals rising local value-addition in advanced composites. Taiwan's Swancor supplies more than 50% of material input for regional offshore wind projects, reflecting supply-chain maturation.

North America captures demand through technological innovation and trade policy. United States antidumping duties on certain Asian epoxy imports shield domestic players and encourage capacity expansions, ensuring a secure supply for defense and infrastructure applications. ExxonMobil's collaboration with McClarin Composites on polyolefin-based thermosets underscores the region's push for lower-carbon alternatives that maintain tensile performance. BASF already operates coating plants on 100% renewable electricity, reducing scope-2 emissions while holding throughput steady.

Europe prioritizes sustainability and regulatory leadership, prompting rapid commercialisation of BPA-free epoxies and bio-attributed intermediates under stringent Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) frameworks. Middle East and Africa accelerate through localization plans such as Sadara's PlasChem Park, geared toward anticorrosion products, while Strata-Solvay's prepreg facility positions the United Arab Emirates as an aerospace material supplier. South America's industrialization and port upgrades sustain moderate resin demand, yet the region trails in composite expertise and remains import-reliant for key intermediates.

- Aditya Birla Chemicals

- AOC Resins

- Ashland Inc.

- BASF SE

- DIC Corporation

- Guangdong Yinyang Environment-Friendly New Materials Co., Ltd.

- Hexion Inc.

- Huntsman Corporation

- Olin Corporation

- Polynt-Reichhold Group

- Resonac

- Scott Bader Co. Ltd.

- Sino Polymer Co. Ltd.

- Sir Industriale

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Epoxy Resins

- 4.2.2 Rising Corrosion-related CAPEX (Capital Expenditures) and OPEX (Operational Expenditures) in Oil & Gas Pipelines

- 4.2.3 Light-weighting Trend in Wind-blade Composites

- 4.2.4 Mainstream Shift to Water-borne Vinyl-ester Systems in Marine

- 4.2.5 Localized Resin Blenders Emerging Around Middle-east Tank-farm Clusters

- 4.3 Market Restraints

- 4.3.1 REACH and TSCA Re-classification of Bisphenol-a

- 4.3.2 Volatile MDI Prices

- 4.3.3 Lack of Skilled Composite Fabricators in the Middle East and Africa

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Vinyl Ester

- 5.1.3 Polyester

- 5.1.4 Polyurethane

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Composites

- 5.2.2 Coatings

- 5.2.3 Others (Adhesives & Linings)

- 5.3 By End-User Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Food and Beverage

- 5.3.3 Industrial

- 5.3.4 Infrastructure

- 5.3.5 Marine

- 5.3.6 Oil and Gas

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 AOC Resins

- 6.4.3 Ashland Inc.

- 6.4.4 BASF SE

- 6.4.5 DIC Corporation

- 6.4.6 Guangdong Yinyang Environment-Friendly New Materials Co., Ltd.

- 6.4.7 Hexion Inc.

- 6.4.8 Huntsman Corporation

- 6.4.9 Olin Corporation

- 6.4.10 Polynt-Reichhold Group

- 6.4.11 Resonac

- 6.4.12 Scott Bader Co. Ltd.

- 6.4.13 Sino Polymer Co. Ltd.

- 6.4.14 Sir Industriale

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Integration of Nanotechnology into Resin Formulations