|

市場調查報告書

商品編碼

2072496

數位學習:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)E-learning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

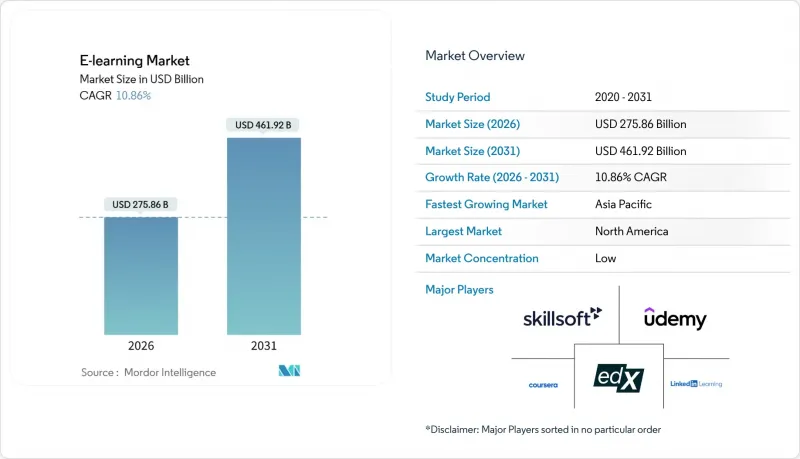

根據 Mordor Intelligence 預測,全球數位學習市場將從 2026 年的 2,758.6 億美元成長到 2031 年的 4,619.2 億美元,未來五年複合年成長率將達到 10.86%。

本報告按交付方式(自主學習和教師主導)、部署方式(雲端和本地部署)、技術(線上數位學習、學習管理系統 (LMS) 等)、最終用戶(教育機構、企業等)和地區(北美、南美等)進行細分。市場預測以美元計價。

全球數位學習市場趨勢與洞察

智慧型手機和高速網路的廣泛普及

行動網路存取和連接能力的提升正在改變人們參與線上學習和技能發展的方式。根據經合組織(OECD)2022年國際學生評估計畫(PISA)的數據,經合組織成員國98%的15歲青少年擁有智慧型手機,96%的青少年在家中可以使用桌上型電腦、筆記型電腦或平板電腦,這降低了他們參與課後影片課程、一對一輔導和完成作業的門檻。同時,聯合國教科文組織(UNESCO)的監測顯示,2024年底,全球79個教育系統(佔全球教育系統的40%)將限制或禁止在課堂上使用智慧型手機,以保障學生的注意力集中和學習效果。然而,課後作業和補充學習仍被允許使用智慧型手機。這種課堂限制與課後行動裝置使用活躍並存的局面,促使服務供應商加強對離線模式、低頻寬格式以及適合短時使用的內容等功能的投入。這種環境有助於數位學習市場擴大其覆蓋範圍,尤其是在農村和新興市場,行動優先策略在這些市場最為有效,目標群體是擁有智慧型手機但寬頻連線不穩定的學習者。

企業在數位轉型過程中對技能發展的需求日益成長

在2026年的勞動市場中,技能獲取的速度至關重要,而結構化、以結果為導向的專案是企業學習藍圖的核心。 edX在2025年的一項調查發現,大多數考慮接受培訓的適齡成年人計劃在幾個月內採取行動,這就要求學習管理者透過與工作要求相符的可擴展項目來滿足這些具體的時間節點。公共教育系統正朝著正式整合人工智慧素養和實踐的方向發展,利用強制性的專業活動日和資源來指導在課堂上安全有效地使用人工智慧。例如,安大略省教育廳將人工智慧列為2025-2026學年專業活動日的主題,要求教育工作者討論人工智慧在教育中的作用,探索已通過核准的寫作和批判性思維工具,並遵守安大略省的「可信賴人工智慧框架」和網路安全政策。旨在解決公共部門數位人才短缺問題的國家策略正在推動將人工智慧明確納入其中的持續培訓項目。例如,英國政府內閣辦公室的「2025年一項重大舉措」(One Big Thing 2025)舉措就是一個例子。舉措計劃將於2025年秋季啟動,旨在為所有公務員提供人工智慧基礎知識、提高工作效率的實際應用以及公共服務創新的培訓。此類措施正在擴大政府範圍內提供職位特定學習平台的潛在需求。

細分市場分析

到2025年,主導學習將佔市場佔有率的58.37%,這反映出人們對靈活、隨選存取且支援獨立練習的學習方式的強烈偏好。預計到2031年,講師主導學習模式將以12.76%的複合年成長率成長,這主要得益於企業將即時輔導與非同步內容相結合,以增強學員信心和提高完成率。管理者對角色相關的模擬練習的需求日益成長。例如,Udemy於2025年10月推出的「AI角色扮演」課程提供超過10,000個模擬練習,並與認證和回饋環節結合,從而降低績效風險。 Didask的基準測試表明,整合AI助理的平台效率提升了76%,不僅能補充講師的授課時間,還能為大規模學習群體提供多語言即時支援。

企業和公共部門的採購負責人正在將人工智慧技能發展和數位素養要求正式化,並利用即時課程確保團隊的行為符合負責任的實踐和組織框架。這種轉變正在強化混合式教學模式,該模式將講師主導的工具介紹、準備情況評估和工作流程標準化課程與非同步學習內容相結合,以彌補知識缺口。在整個預測期內,數位學習產業預計將維持這兩種模式,作為互補通路服務於不同的目的。即時課程對於新員工入職、領導力培養和軟性技能提升仍然至關重要,而自主學習模組將構成知識獲取和應用的基礎。

預計到2025年,基於雲端的部署將佔據54.37%的市場佔有率,並預計在2031年之前以11.77%的複合年成長率成長。企業正優先考慮快速更新、彈性容量和多租戶架構,以簡化管理。數位學習市場正透過專注於安全性、區域託管和合規性整合,為受監管行業提供支持,從而幫助這項轉型。雲端平台無需本地維護即可實現人工智慧輔導和分析等功能,確保全球用戶持續獲得改進和運作。訂閱模式展示了企業如何降低成本、整合供應商並跨越團隊和區域擴展。隨著教育機構將其使用的平台標準化為少數幾個,與本地部署解決方案相比,雲端優先策略能夠提供更高的速度和更低的整體擁有成本 (TCO)。

在國防領域和需要網路隔離的高度敏感環境中,本地部署仍將持續。然而,雲端功能數位學習市場的重要性日益凸顯。產品藍圖強調隱私控制、授權管理和可訪問性,以滿足教育機構和學生的保護需求,從而增強他們對託管解決方案的信心。雲端原生分析功能將課程活動與技能指標和證書關聯起來,以展示學習成果並支援職業發展。強調資料保護和人工智慧透明度的採購框架傾向於選擇具有區域覆蓋的認證雲端平台。這些因素表明,到2031年,雲端技術的應用將成為數位學習產業的基石。

區域分析

預計到2025年,北美將佔據34.74%的市場。這得益於其強大的平台、內容合作夥伴和企業買家生態系統,這些資源將在後疫情時代繼續支持數位學習。 2026年,教育和政府措施將加強學校和公共服務部門的數位素養和負責任的人工智慧實踐,從而加速其長期應用。美國和加拿大致力於培養人工智慧人才,這推動了對認證、結構化學習路徑和符合合規要求的供應商的需求。私部門買家正在擴展與企業系統整合的訂閱式和基於角色的學習項目,並進行多年期數位化培訓。本地網路連接的差異以及電信資金的潛在變化,為補貼寬頻服務帶來了不確定性,並對社區機構造成影響。在這個成熟市場中,成長將取決於人工智慧原生能力、微證書和相關證據。

在歐洲,歐盟數位教育行動計畫正持續推進至2026年,旨在提升中小學和高等教育機構的教師能力、系統韌性和數位轉型目標。旨在提升數位技能和支持教師的政策正在彌合能力差距,並確保成員國在基礎設施、內容和平台方面獲得多年預算。採購優先考慮隱私、安全和可近性,選擇符合歐盟框架和國家指南的平台。多語言內容和在地化正在影響不同語言群體的採用。隨著混合模式和學習分析的普及,穩定的採購週期和跨境夥伴關係正在使資格與勞動力市場需求相匹配。人工智慧素養和負責任的使用正在推動高等教育和企業環境中原生人工智慧平台的採用。

亞太地區預計到2031年將以8.87%的複合年成長率成長,這主要得益於網際網路連接的普及、移動優先學習模式的興起以及旨在提升學校和職場數字技能的政策舉措。政府和雇主正在投資人工智慧和數據素養項目,從而推動了對特定職業課程和專業認證的需求成長。在農村和郊區,行動網路存取和離線功能正在影響消費者的產品選擇。隱私和安全需求指南平台設計,而與大學和大型企業的合作則構成了市場策略的基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧型手機和高速網路的廣泛普及

- 企業在數位轉型過程中對技能發展的需求日益成長

- 政府在數位教育方面的舉措

- 與面授培訓相比,成本優勢顯著

- 大學與大型科技公司之間微證書合作關係的興起

- 教育科技企業的資金籌措正轉移到新興市場。

- 市場限制因素

- 低完成率和學習者參與度方面的挑戰

- 農村和低收入地區的數位鴻溝

- 多語言市場內容在地化的障礙

- 資料隱私法規的複雜性

- 價值供應鏈分析

- 監理情勢

- 數位學習市場消費行為分析

- 技術展望

- 波特五力模型

第5章 市場規模及成長預測(價值,10億美元)

- 透過串流媒體模式

- 自學型

- 講師主導

- 不同的發展

- 雲

- 現場

- 透過技術

- 線上數位學習

- 學習管理系統(LMS)

- 行動數位學習

- 快速數位學習

- 虛擬教室

- 最終用戶

- 學術機構

- 公司

- 政府/公共部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Coursera Inc.

- Udemy Inc.

- LinkedIn Learning

- edX(2U Inc.)

- Skillsoft

- Pluralsight

- Blackboard Inc.

- Instructure(Canvas)

- Cornerstone OnDemand

- Moodle

- Docebo SpA

- Pearson plc

- SAP Litmos

- G-Cube

- Chegg Inc.

- Udacity

- D2L Corp.(Brightspace)

- Google LLC(Classroom)

- Aptara

- FutureLearn Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the global e-learning market size is projected to grow from USD 275.86 billion in 2026 to USD 461.92 billion by 2031, reflecting a robust compound annual growth rate (CAGR) of 10.86% over the five years.

This report is Segmented by Delivery Mode (Self-Paced and Instructor-Led), Deployment (Cloud and On-Premise), Technology (Online E-Learning, Learning Management System (LMS), and More), End-User (Academic, Corporate, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global E-learning Market Trends and Insights

Growing Penetration of Smartphones and High-Speed Internet

Mobile access and better connectivity are reshaping how people engage with online learning and skills development. According to OECD PISA 2022 data, 98% of 15-year-olds across OECD countries own a smartphone, and 96% have access to a desktop, laptop, or tablet at home, lowering barriers to video lessons, tutoring, and coursework outside school hours. At the same time, 79 education systems worldwide, representing 40% of global systems, have implemented smartphone restrictions or bans in classrooms by the end of 2024 to protect attention and learning outcomes, per UNESCO monitoring, while permitting after-school use for homework and supplemental learning . The coexistence of classroom restrictions and strong out-of-school mobile use pushes providers to invest in features like offline modes, low-bandwidth formats, and content that fits short sessions. This environment helps the e-learning market extend reach among learners who have smartphones but inconsistent broadband, especially in rural districts and emerging markets where mobile-first strategies carry the most impact.

Corporate Up-Skilling Demand Amid Digital Transformation

Labor markets in 2026 prioritize speed-to-skill, making structured, outcomes-based programs central to enterprise learning roadmaps. A survey conducted by edX in 2025 found that most working-age adults considering training intended to act within months, pointing to concrete timelines that learning leaders must meet with scalable programs that align with job requirements. Public education systems are shifting to formalize AI literacy and practice through required professional learning days and resources that guide safe, effective classroom use. For instance, Ontario's Ministry of Education mandated AI as a topic for Professional Activity Days in 2025-26, requiring educators to discuss AI's role in teaching, explore approved tools for writing and critical thinking, and align with the Ontario Trustworthy AI Framework and cybersecurity policies. National strategies to address digital talent gaps in the public sector are driving evergreen training plans with explicit AI components, such as the UK Cabinet Office's One Big Thing 2025 initiative, which will train all civil servants on AI essentials, practical applications for streamlining work, and innovation in public services starting in autumn 2025. These efforts expand addressable demand for platforms that deliver role-aligned learning at government scale.

Other drivers and restraints analyzed in the detailed report include:

- Government Initiatives for Digital Education

- Cost Advantages Over Classroom Training

- Low Completion Rates and Learner-Engagement Challenges

- Digital Divide in Rural and Low-Income Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-paced learning accounts for 58.37% of the market in 2025, reflecting a strong preference for flexible, on-demand access that supports self-directed practice. Instructor-led formats are projected to grow at a 12.76% CAGR through 2031, driven by enterprises blending live coaching with asynchronous content to enhance confidence and completion rates. Managers increasingly request role-specific simulations, such as Udemy's October 2025 AI Role Play launch with over 10,000 simulations tied to certifications and feedback sessions, reducing performance risks. Platforms integrating AI assistance achieve 76% efficiency gains, as per Didask benchmarks, complementing instructor time and scaling live support across languages for large learner groups.

Corporate and public-sector buyers are formalizing AI up-skilling and digital literacy requirements, using live sessions to align teams with responsible practices and organizational frameworks. This shift strengthens hybrid designs, where instructor-led touchpoints introduce tools, assess readiness, and standardize workflows, while asynchronous content addresses knowledge gaps. Over the forecast period, the e-learning industry is expected to sustain both modes as complementary channels serving distinct objectives. Live formats will remain essential for onboarding, leadership, and soft skills, while self-paced modules will anchor knowledge acquisition and practice.

Cloud-based deployment, holding 54.37% of the base in 2025, is projected to grow at an 11.77% CAGR through 2031. Enterprises favor faster updates, elastic capacity, and multi-tenant architecture for simplified administration. The e-learning market supports this shift by focusing on security, regional hosting, and compliance integrations for regulated industries. Cloud platforms enable features like AI coaching and analytics without on-premises maintenance, ensuring continuous improvement and uptime for global users. Subscription models illustrate how enterprises scale across teams and geographies while reducing costs and consolidating vendors. As institutions standardize on fewer platforms, cloud-first strategies enhance speed and lower the total cost of ownership compared to on-premises solutions.

On-premises implementations will remain in defense and sensitive environments requiring network isolation. However, the e-learning market increasingly prioritizes cloud features. Product roadmaps emphasize privacy controls, consent management, and accessibility to meet institutional and student protection requirements, boosting confidence in hosted solutions. Cloud-native analytics link course activity to skill signals and credentials, proving outcomes and supporting career mobility. Procurement frameworks focusing on data protection and AI transparency favor cloud platforms with certifications and regional coverage. These factors position cloud deployment as the foundation of the e-learning industry through 2031.

Complete Report Scope:

- By Delivery Mode

- Self-Paced

- Instructor-Led

- By Deployment

- Cloud

- On-Premise

- By Technology

- Online e-learning

- Learning Management System (LMS)

- Mobile e-learning

- Rapid e-learning

- Virtual Classroom

- By End-User

- Academic

- Corporate

- Government & Public Sector

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

North America held a 34.74% market share in 2025, supported by a strong ecosystem of platforms, content partners, and enterprise buyers sustaining digital learning post-pandemic. Institutional and government actions in 2026 are reinforcing digital literacy and responsible AI practices in schools and public services, driving long-term adoption. United States and Canadian initiatives to build AI-ready workforces are increasing demand for certifications, structured learning pathways, and compliance-ready vendors. Private-sector buyers are expanding subscriptions and role-based learning programs integrated with enterprise systems, committing to multi-year digital training. Rural connectivity gaps and potential telecom funding shifts create uncertainties for subsidized broadband, affecting community institutions. Growth in this mature market is tied to AI-native features, micro-credentials, and evidence.

Europe continues implementing the EU Digital Education Action Plan in 2026, advancing educator readiness, system resilience, and digital transformation goals in schools and higher education. Policies addressing digital skills and teacher support bridge readiness gaps and secure multi-year budgets for infrastructure, content, and platforms across member states. Procurement prioritizes privacy, safety, and accessibility, favoring platforms compliant with EU frameworks and national guidelines. Multilingual content and localization influence adoption across diverse language communities. As hybrid models and learning analytics become embedded, steady procurement cycles and cross-border partnerships align credentials with labor market needs. AI literacy and responsible use strengthen the case for AI-native platforms in higher education and enterprise contexts.

Asia-Pacific is projected to grow at an 8.87% CAGR through 2031, driven by internet access gains, mobile-first learning behavior, and policy pushes for digital skills in schools and workplaces. Governments and employers are investing in AI and data capability programs, expanding demand for role-aligned courses and professional certificates. Mobile access and offline capabilities shape product choices in rural and peri-urban areas. Privacy and safety mandates guide platform design, while partnerships with universities and large employers anchor market strategies.

- Coursera Inc.

- Udemy Inc.

- LinkedIn Learning

- edX (2U Inc.)

- Skillsoft

- Pluralsight

- Blackboard Inc.

- Instructure (Canvas)

- Cornerstone OnDemand

- Moodle

- Docebo S.p.A.

- Pearson plc

- SAP Litmos

- G-Cube

- Chegg Inc.

- Udacity

- D2L Corp. (Brightspace)

- Google LLC (Classroom)

- Aptara

- FutureLearn Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing penetration of smartphones & high-speed internet

- 4.2.2 Corporate up-skilling demand amid digital transformation

- 4.2.3 Government initiatives for digital education

- 4.2.4 Cost advantages over classroom training

- 4.2.5 Rise of micro-credential partnerships between universities & Big Tech

- 4.2.6 EdTech venture funding shift toward emerging markets

- 4.3 Market Restraints

- 4.3.1 Low completion rates & learner-engagement challenges

- 4.3.2 Digital divide in rural & low-income areas

- 4.3.3 Content-localization barriers for multilingual markets

- 4.3.4 Data-privacy regulatory complexity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Consumer Behavior Insights in the E-Learning Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, US$ bn)

- 5.1 By Delivery Mode

- 5.1.1 Self-Paced

- 5.1.2 Instructor-Led

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Technology

- 5.3.1 Online e-learning

- 5.3.2 Learning Management System (LMS)

- 5.3.3 Mobile e-learning

- 5.3.4 Rapid e-learning

- 5.3.5 Virtual Classroom

- 5.4 By End-User

- 5.4.1 Academic

- 5.4.2 Corporate

- 5.4.3 Government & Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Coursera Inc.

- 6.4.2 Udemy Inc.

- 6.4.3 LinkedIn Learning

- 6.4.4 edX (2U Inc.)

- 6.4.5 Skillsoft

- 6.4.6 Pluralsight

- 6.4.7 Blackboard Inc.

- 6.4.8 Instructure (Canvas)

- 6.4.9 Cornerstone OnDemand

- 6.4.10 Moodle

- 6.4.11 Docebo S.p.A.

- 6.4.12 Pearson plc

- 6.4.13 SAP Litmos

- 6.4.14 G-Cube

- 6.4.15 Chegg Inc.

- 6.4.16 Udacity

- 6.4.17 D2L Corp. (Brightspace)

- 6.4.18 Google LLC (Classroom)

- 6.4.19 Aptara

- 6.4.20 FutureLearn Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

數位學習市場-2026-2032年全球市場預測數位學習IT基礎設施市場:按組件、部署模式、組織規模和最終用戶產業分類-2026-2032年全球市場預測數位學習法規遵從培訓市場:按組成部分、培訓類型、組織規模、部署模式和產業分類-2026-2032年全球市場預測

數位學習市場-2026-2032年全球市場預測數位學習IT基礎設施市場:按組件、部署模式、組織規模和最終用戶產業分類-2026-2032年全球市場預測數位學習法規遵從培訓市場:按組成部分、培訓類型、組織規模、部署模式和產業分類-2026-2032年全球市場預測 2034年幼兒數位化學習市場預測-全球分析(按組成部分、學習形式、部署方法、應用、最終用戶和地區分類)人工智慧驅動的知識評估市場預測至2034年:全球分析(按組成部分、評估類型、題型、部署模式、應用、最終用戶和地區分類)全球數位學習市場預測(至2034年):按學習形式、內容類型、技術、最終用戶和地區分類的分析數位學習體驗市場預測至2034年—按體驗類型、部署模式、技術、應用、最終用戶和地區分類的全球分析遠端教育市場預測至2034年-按學習形式、交付平台、課程類型、學科領域、最終用戶和地區分類的全球分析

2034年幼兒數位化學習市場預測-全球分析(按組成部分、學習形式、部署方法、應用、最終用戶和地區分類)人工智慧驅動的知識評估市場預測至2034年:全球分析(按組成部分、評估類型、題型、部署模式、應用、最終用戶和地區分類)全球數位學習市場預測(至2034年):按學習形式、內容類型、技術、最終用戶和地區分類的分析數位學習體驗市場預測至2034年—按體驗類型、部署模式、技術、應用、最終用戶和地區分類的全球分析遠端教育市場預測至2034年-按學習形式、交付平台、課程類型、學科領域、最終用戶和地區分類的全球分析 2026-2030年全球道德與合規培訓市場

2026-2030年全球道德與合規培訓市場 電子學習服務市場規模、佔有率和趨勢分析報告:按類型、課程、學習方法、技術、最終用途、地區和細分市場預測(2026-2033 年)

電子學習服務市場規模、佔有率和趨勢分析報告:按類型、課程、學習方法、技術、最終用途、地區和細分市場預測(2026-2033 年)