|

市場調查報告書

商品編碼

2072470

壓縮空氣儲能(CAES):市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Compressed Air Energy Storage (CAES) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

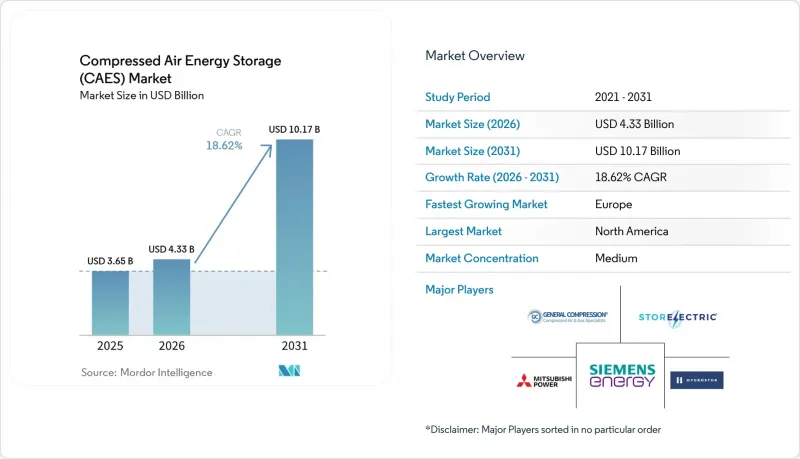

據 Mordor Intelligence 稱,壓縮空氣儲能市場預計到 2026 年價值 43.3 億美元,高於 2025 年的 36.5 億美元,預計到 2031 年將達到 101.7 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 18.6%。

本報告按類型(絕熱、非絕熱等)、儲存配置(鹽丘洞穴、硬岩/礦洞等)、發電容量(小規模和中型)、應用(透過可再生能源併網實現電力平滑、電轉氫混合等)、最終用戶(公用事業、資料中心和數位基礎設施等)和地區(北美、歐洲等)進行分類。

全球壓縮空氣儲能(CAES)市場趨勢與洞察

強制引入可再生能源將刺激對穩定電網的投資。

加州、歐盟和澳洲部分州的法規正迫使電力公司確保長期儲能能力,以彌補白天可再生能源的供不應求。僅加州就已撥款2.7億美元用於非鋰電池儲能,並設定了4吉瓦(GW)的6小時運行資產目標,為壓縮空氣儲能(CAES)市場項目提供了明確的政策路徑。英國的「上限和下限」機制將於2025年最終確定,該機制為放電時間超過6小時的裝置提供受監管的收入來源,使CAES成為投資者易於資金籌措。這些框架直接針對被稱為「鴨子曲線」的現象,即太陽能發電量隨著晚間需求的增加而急劇下降,導致4-6小時的供不應求,在這種情況下,CAES比電池更具優勢。澳洲新南威爾斯州也緊隨其後,簽署了一份1吉瓦/13吉瓦時的長期儲能契約,進一步擴大了壓縮空氣儲能市場。

絕熱壓縮空氣儲能技術的成本較低(美元/千瓦時)

溫度控管技術的進步和渦輪機械的標準化已將絕熱壓縮空氣儲能(CAES)的資本支出(CAPEX)降低至每千瓦1100至1400美元,並將往返效率提高至70%至75%。這在很大程度上縮小了其與抽水蓄能電站的差距。採用相變材料的填充床儲熱模組的能源效率現已達到61.5%,可在3.5年內實現投資回報,並可實現石化燃料運作和持續的排碳權收入。新興的低溫絕熱設計運作為度C,由於其啟動時間不到90秒,正在獲得頻率調節合約。憑藉這些成本和性能的提升,壓縮空氣儲能(CAES)市場正在成為包括套利、旋轉備用和組合慣性在內的多種服務組合中的主流選擇。

高昂的初始資本投入是進入市場的障礙。

對於典型的公用事業規模壓縮空氣儲能(CAES)裝置,採用絕緣設計每千瓦需要1600至2300美元,整個專案預算超過1億美元。經通膨調整後的麥金托什電廠建設成本清楚地顯示了開發商面臨的巨大資產負債表風險。即使是效率高達75%的絕緣系統,其投資回收期也需要4至6年,而電錶前電池組的回收期僅為2至3年,因此其優勢相對較弱。地質勘測、客製化渦輪機械以及儲氣庫襯砌的保固費用都會增加緊急資金,以應對不可預見的情況。這些因素,再加上缺乏針對性的政策支持,降低了壓縮空氣儲能(CAES)產業在資金匱乏地區的吸引力。

細分市場分析

隨著往返效率飆升至75%,且無燃料運作符合企業的淨零排放目標,投資人對絕熱式設計的興趣日益濃厚。儘管到2025年,非絕熱式裝置仍佔壓縮空氣儲能市場佔有率的49.75%,但預計到2031年,絕熱式裝置市場佔有率將以22.10%的複合年成長率成長。具有前瞻性的電力公司更傾向於選擇絕熱式裝置,因為它們擁有可靠的零排放記錄,但在天然氣管道密集且電力供應嚴重短缺的地區,非絕熱式裝置仍繼續部署。先進等溫原型壓縮空氣儲能裝置的市場規模仍然較小,但如果深海繫錨碇試驗能夠證明其理論效率可達90%,則該市場具有巨大的成長潛力。

自2022年以來,儲熱介質的成本已下降近30%,為絕熱系統的發展奠定了基礎。支持對流系統的主要廠商正以混合蒸氣循環來應對,這些循環雖然效率略有提高,但為了保持競爭力,它們依賴於較低的燃料熱耗率。等溫海底先導計畫旨在平衡離岸風力發電,但由於預計每千瓦的資本支出(CAPEX)將高達1500至3000美元,其短期應用受到限制。同時,由於相變複合材料的持續創新,壓縮空氣儲能產業正保持快速發展。

到2025年,鹽洞將佔壓縮空氣儲能市場52.40%的佔有率。這主要得益於北美和歐洲地質條件的改善、成熟的密封技術和成熟的浸出技術。開發商報告稱,年洩漏率低於0.02%,凸顯了該項目的資金籌措可行性。同時,利用硬岩洞穴和廢棄礦井的倉儲設施正以24.80%的複合年成長率成長,澳洲、德國和中國的營運商正在維修廢棄礦井,並透過利用現有隧道大幅降低挖掘成本。

雖然陸上壓力容器適用於偏遠微電網和10兆瓦以下的短期項目,但其成本效益並不高,尤其是在公用事業規模上。由於非均勻孔隙率帶來的複雜壓力管理問題,含水層儲能仍處於試驗階段。水下管線儲能方案在技術上可行,但在錨碇和維護方面仍面臨許多後勤挑戰。因此,鹽丘和硬岩洞穴很可能在未來十年主導壓縮空氣儲能市場。

區域分析

在聯邦政府資助和各州雄心勃勃的採購目標的推動下,北美預計到2025年將佔全球銷售額的34.40%。加州Hydrostore公司400兆瓦的柳岩中心專案是大型專案發展動能強勁的例證,而加拿大昆特電廠已獲得2億美元的成長資金,計畫擴建至500兆瓦。墨西哥目前仍在考慮階段,但其豐富的鹽礦資源使其有望成為未來潛在的建設地點,前提是相關政策獎勵能夠落實。

歐洲27.10%的複合年成長率得益於持續的脫碳政策。英國的「總量控制與下限」計畫保障了基本負載收入,並推動了一系列優先考慮放電持續時間超過六小時技術的競標。德國的電網平衡需求促使利用廢棄鹽礦建造壓縮空氣儲能(CAES)系統的提案激增,而荷蘭則在探索將天然氣田改造為結合氫能和CAES的混合能源樞紐。隨著可再生能源的日益普及,東歐的採礦歷史為低成本的洞穴改造提供了一種選擇。

亞太地區正逐漸成為千兆級儲能容量部署的示範區。中國江蘇省一座300兆瓦的電站已成功在40巴和600度C下運行,而一個500兆瓦的項目正在接受省級核准。在澳洲的長期儲能競標中,已鎖定超過1吉瓦的容量,其中包括儲能時間8至15小時的壓縮空氣儲能(CAES)競標。一個日本研究聯盟正在評估一種使用海底管道的等溫原型,而印度的「可再生能源儲能藍圖」則指出,儲能時間達到10小時或以上的設施可能獲得財政獎勵。整體而言,壓縮空氣儲能(CAES)市場正在快速擴張,尤其是在可再生能源滲透率高且擁有完善的配套資金籌措機制的地區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 全球已安裝和計劃建設的壓縮空氣儲能容量分析(兆瓦)

- 市場促進因素

- 可再生能源

- 絕緣壓縮空氣儲能裝置的每千瓦時價格正在下降。

- 政府主導的長期倉儲競標

- 將枯竭天然氣田改造為壓縮空氣儲能田

- 人工智慧最佳化的溫度控管提高了往返效率。

- 企業全天候清潔能源購電協議 (PPA) 正在推動儲能超過 8 小時。

- 市場限制因素

- 前期投資額高,投資回收期長。

- 地質約束

- 電池價格面臨下行壓力

- 當地居民對洞穴安全和地震活動表示反對

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 透過熱交換

- 絕緣

- 等溫

- 超/高水準等溫線型

- 按儲存配置

- 鹽丘儲存

- 硬岩/礦井空腔

- 含水層

- 廢棄的礦坑和隧道

- 地面安裝式壓力容器

- 水下和海底管道

- 按發電能力

- 小規模(小於10兆瓦)

- 中型(10-100兆瓦)

- 透過使用

- 可再生能源併網的電力穩定

- 抑低尖峰負載和負荷轉移

- 輸配電延期

- 備援與彈性/微電網

- 工業餘熱回收

- 動力氫氣混合動力

- 最終用戶

- 電力公司

- 獨立發電機

- 商業和工業用途

- 偏遠及無電網地區

- 資料中心和數位基礎設施

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 西班牙

- 法國

- 荷蘭

- 挪威

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Siemens Energy AG

- Hydrostor Inc.

- General Compression Ltd.

- Apex CAES LLC

- Ridge Energy Storage LP

- Storelectric Ltd.

- Mitsubishi Power Americas

- Dresser-Rand(Siemens)

- ALACAES SA

- RWE Power AG

- Corre Energy BV

- Bright Energy Storage

- Stiesdal Storage Tech.

- NRStor Inc.

- Shell Energy Storage

- Huaibei A-CAES Co.

- PG&E(Diablo CAES proj.)

- Cavergy Solutions Ltd.

- Enel Green Power(EGP)

- E.ON SE(Huntorf owner)

第7章 市場機會與未來展望

According to Mordor Intelligence, compressed air energy storage market size in 2026 is estimated at USD 4.33 billion, growing from 2025 value of USD 3.65 billion with 2031 projections showing USD 10.17 billion, growing at 18.6% CAGR over 2026-2031.

This report is Segmented by Type (Diabatic, Adiabatic, and More), Storage Configuration (Salt-Domed Cavern, Hard-rock/Mined Cavern, and More), Power Capacity (Small-Scale and Medium-Scale), Application (Renewable-Integration Firming, Power-To-X Hydrogen Hybrids, and More), End-User (Electric Utility, Data Centres and Digital Infra, and More), and Geography (North America, Europe, and More)

Global Compressed Air Energy Storage (CAES) Market Trends and Insights

Renewable-Energy Penetration Mandates Drive Grid Stability Investments

Mandates in California, the EU, and select Australian states are compelling utilities to secure long-duration capacity that can bridge daily renewable gaps. California alone has earmarked USD 270 million for non-lithium storage and set a 4 GW target for assets with a six-hour duration, providing compressed air energy storage market projects with a clear policy runway. The UK's cap-and-floor scheme, finalized in 2025, offers a regulated revenue stream for assets with discharge windows exceeding 6 hours, making CAES a bankable proposition for investors. These frameworks directly address the "duck curve," a scenario in which solar output falls steeply as evening demand rises, creating a four- to six-hour deficit that favors CAES over batteries. Australia's New South Wales followed suit, contracting 1 GW/13 GWh of long-duration storage capacity, further expanding the compressed air energy storage market.

Declining $/kWh Costs for Adiabatic CAES Technology

Thermal-management advances and standardized turbomachinery have driven adiabatic CAPEX down to USD 1,100-1,400 per kW, lifting round-trip efficiencies to 70-75%, and closing much of the gap versus pumped-hydro assets. Packed-bed heat-storage modules using phase-change materials now reach 61.5% energy efficiency and recoup costs within 3.5 years, enabling fossil-free operation and recurring carbon-credit revenue. Emerging low-temperature adiabatic designs operating at 90-200 °C are snaring frequency-regulation contracts thanks to sub-90-second start-up times. These cost and performance gains are positioning the compressed air energy storage market as a mainstream choice for multi-service portfolios that include arbitrage, spinning reserve, and synthetic inertia.

High Up-Front Capital Expenditure Constrains Market Entry

Typical utility-scale CAES installations require USD 1,600-2,300 per kW for diabatic designs, with overall project budgets exceeding USD 100 million. The McIntosh plant's inflation-adjusted build-out cost illustrates the sizable balance-sheet exposure developers face. Four- to six-year payback horizons-even for 75%-efficient adiabatic systems-compare unfavorably with two- to three-year returns on front-of-the-meter battery arrays. Geological surveys, bespoke turbomachinery, and cavern-lining warranties increase contingency allowances, which dampens the appeal of the compressed air energy storage industry in capital-scarce regions that lack targeted policy support.

Other drivers and restraints analyzed in the detailed report include:

- Government Long-Duration Storage Tenders Accelerate Deployment

- Repurposing Depleted Gas Fields Reduces Infrastructure Costs

- Battery Price Deflation Creates Competitive Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adiabatic designs captured rising investor attention as round-trip efficiencies surged toward 75% and fuel-free operation aligned with corporate net-zero targets. The adiabatic segment is forecast to grow at a 22.10% CAGR to 2031, despite diabatic plants still holding a 49.75% market share in the compressed air energy storage market as of 2025. Forward-looking utilities favor adiabatic assets for zero-emission credentials, while regions with abundant gas pipelines and urgent capacity shortages continue to commission diabatic units. The compressed air energy storage market size for advanced isothermal prototypes remains small, but could expand once deep-ocean tethering tests validate a 90% theoretical efficiency.

Thermal-storage media costs have fallen by almost 30% since 2022, underpinning the adiabatic runway. Diabatic stalwarts are responding with hybrid-steam cycles that marginally improve efficiency yet rely on lower fuel heat rates to stay relevant. Isothermal ocean-floor pilots target offshore wind balancing, but CAPEX estimates between USD 1,500 and USD 3,000 per kW constrain near-term uptake. Continual innovation in phase-change composites, meanwhile, keeps the compressed air energy storage industry on a rapid learning curve.

Salt caverns accounted for 52.40% of the compressed air energy storage market size in 2025, owing to their geological prevalence in North America and Europe, proven sealing integrity, and mature leaching techniques. Developers report leakage rates below 0.02% per year, reinforcing bankability. Hard-rock and mined caverns, however, are growing at a 24.80% CAGR as operators retrofit abandoned mines in Australia, Germany, and China, benefiting from pre-existing shafts that slash excavation costs.

Above-ground pressure vessels cater to remote microgrids and fast-track projects under 10 MW but become cost-prohibitive at utility scale. Aquifer storage remains limited to pilot deployments because heterogenous porosity complicates pressure management. Underwater pipe concepts, although technically viable, still wrestle with mooring and maintenance logistics. Consequently, salt-domed and hard-rock caverns are likely to dominate the compressed air energy storage market share throughout the decade.

Complete Report Scope:

- By Type

- Diabatic

- Adiabatic

- Isothermal

- Super-/Advanced Isothermal

- By Storage Configuration

- Salt-domed cavern

- Hard-rock/mined cavern

- Aquifer

- Abandoned mine/tunnel

- Above-ground pressure vessel

- Underwater/seabed pipe

- By Power Capacity

- Small-scale (Below 10 MW)

- Medium-scale (10 to 100 MW)

- By Application

- Renewable-integration firming

- Peak-shaving and load-shifting

- T&D deferral

- Backup and resilience/microgrids

- Industrial waste-heat recovery

- Power-to-X hydrogen hybrids

- By End-User

- Electric utilities

- Independent power producers

- Commercial and industrial

- Remote and off-grid communities

- Data centres and digital infra

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- Spain

- France

- Netherlands

- Norway

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Israel

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

North America captured 34.40% of revenues in 2025, driven by federal lending support and ambitious state procurement targets. Hydrostor's 400 MW Willow Rock center in California exemplifies large-scale momentum, while Canada's Quinte facility secured USD 200 million in growth capital to advance a 500 MW build-out. Mexico, though still exploratory, boasts ample salt formations that could host future sites once policy incentives materialize.

Europe's 27.10% CAGR trajectory rests on cohesive decarbonization mandates. The UK's cap-and-floor plan ensures baseload-style earnings, encouraging tender pipelines that favor technologies with discharge thresholds exceeding six hours. Germany's grid-balancing needs have catalyzed proposals for CAES systems utilizing disused salt mines, and the Netherlands is studying repurposed gas fields for hybrid hydrogen-CAES hubs. Eastern Europe's mining legacies offer an optionality for low-cost cavern conversion as renewable energy penetration grows.

Asia-Pacific region is evolving into a test bed for giga-scale installations. China's 300 MW Jiangsu plant validated 40-bar, 600 °C operation, and additional 500 MW projects are moving through provincial approvals. Australia's Long Duration Storage auctions secured over 1 GW of capacity, which includes CAES bids with 8-15-hour capabilities. Japan's research consortia are evaluating seabed-pipe isothermal prototypes, while India's Renewable Energy Storage Roadmap indicates potential fiscal incentives for assets with a storage duration of >= 10 hours. Overall, the compressed air energy storage market is expanding rapidly, particularly where high renewable energy penetration is combined with supportive financing mechanisms.

- Siemens Energy AG

- Hydrostor Inc.

- General Compression Ltd.

- Apex CAES LLC

- Ridge Energy Storage LP

- Storelectric Ltd.

- Mitsubishi Power Americas

- Dresser-Rand (Siemens)

- ALACAES SA

- RWE Power AG

- Corre Energy BV

- Bright Energy Storage

- Stiesdal Storage Tech.

- NRStor Inc.

- Shell Energy Storage

- Huaibei A-CAES Co.

- PG&E (Diablo CAES proj.)

- Cavergy Solutions Ltd.

- Enel Green Power (EGP)

- E.ON SE (Huntorf owner)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Global Installed & Planned CAES Capacity Analysis (MW)

- 4.3 Market Drivers

- 4.3.1 Renewable-energy penetration mandates

- 4.3.2 Declining $/kWh for adiabatic CAES

- 4.3.3 Government long-duration storage tenders

- 4.3.4 Repurposing depleted gas fields for CAES

- 4.3.5 AI-optimised thermal management boosts round-trip efficiency

- 4.3.6 Corporate 24/7 clean-power PPAs driving over 8-hour storage

- 4.4 Market Restraints

- 4.4.1 High up-front capex & long payback

- 4.4.2 Geological site limitations

- 4.4.3 Battery price deflation pressure

- 4.4.4 Community opposition over cavern integrity & seismicity

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Diabatic

- 5.1.2 Adiabatic

- 5.1.3 Isothermal

- 5.1.4 Super-/Advanced Isothermal

- 5.2 By Storage Configuration

- 5.2.1 Salt-domed cavern

- 5.2.2 Hard-rock/mined cavern

- 5.2.3 Aquifer

- 5.2.4 Abandoned mine/tunnel

- 5.2.5 Above-ground pressure vessel

- 5.2.6 Underwater/seabed pipe

- 5.3 By Power Capacity

- 5.3.1 Small-scale (Below 10 MW)

- 5.3.2 Medium-scale (10 to 100 MW)

- 5.4 By Application

- 5.4.1 Renewable-integration firming

- 5.4.2 Peak-shaving and load-shifting

- 5.4.3 T&D deferral

- 5.4.4 Backup and resilience/microgrids

- 5.4.5 Industrial waste-heat recovery

- 5.4.6 Power-to-X hydrogen hybrids

- 5.5 By End-User

- 5.5.1 Electric utilities

- 5.5.2 Independent power producers

- 5.5.3 Commercial and industrial

- 5.5.4 Remote and off-grid communities

- 5.5.5 Data centres and digital infra

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 Spain

- 5.6.2.5 France

- 5.6.2.6 Netherlands

- 5.6.2.7 Norway

- 5.6.2.8 Russia

- 5.6.2.9 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Australia

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Israel

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Siemens Energy AG

- 6.4.2 Hydrostor Inc.

- 6.4.3 General Compression Ltd.

- 6.4.4 Apex CAES LLC

- 6.4.5 Ridge Energy Storage LP

- 6.4.6 Storelectric Ltd.

- 6.4.7 Mitsubishi Power Americas

- 6.4.8 Dresser-Rand (Siemens)

- 6.4.9 ALACAES SA

- 6.4.10 RWE Power AG

- 6.4.11 Corre Energy BV

- 6.4.12 Bright Energy Storage

- 6.4.13 Stiesdal Storage Tech.

- 6.4.14 NRStor Inc.

- 6.4.15 Shell Energy Storage

- 6.4.16 Huaibei A-CAES Co.

- 6.4.17 PG&E (Diablo CAES proj.)

- 6.4.18 Cavergy Solutions Ltd.

- 6.4.19 Enel Green Power (EGP)

- 6.4.20 E.ON SE (Huntorf owner)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

液態空氣儲能(LAES)市場預測—按儲能容量、技術、應用、最終用戶和地區分類的全球分析—2034年

液態空氣儲能(LAES)市場預測—按儲能容量、技術、應用、最終用戶和地區分類的全球分析—2034年 壓縮空氣儲能市場-全球產業規模、佔有率、趨勢、機會、預測:依方法、儲存方法、應用、最終用戶產業、地區和競爭格局分類,2021-2031年

壓縮空氣儲能市場-全球產業規模、佔有率、趨勢、機會、預測:依方法、儲存方法、應用、最終用戶產業、地區和競爭格局分類,2021-2031年 壓縮空氣儲能(CAES)市場:按類型、儲能類型、應用和地區分類(2026-2034 年)

壓縮空氣儲能(CAES)市場:按類型、儲能類型、應用和地區分類(2026-2034 年) 壓縮空氣儲能市場:依技術類型、部署模式、應用程式和最終用戶分類-2026-2032年全球市場預測

壓縮空氣儲能市場:依技術類型、部署模式、應用程式和最終用戶分類-2026-2032年全球市場預測 2026年全球電網自動化系統市場報告2026年全球電網自動化系統市場報告

2026年全球電網自動化系統市場報告2026年全球電網自動化系統市場報告 壓縮空氣儲能(CAES)市場規模、佔有率及預測:依系統設計(絕熱、非絕熱、等溫)、儲能容量、往返效率及專案規模劃分-全球預測至2036年

壓縮空氣儲能(CAES)市場規模、佔有率及預測:依系統設計(絕熱、非絕熱、等溫)、儲能容量、往返效率及專案規模劃分-全球預測至2036年 全球壓縮空氣儲能市場規模、佔有率、趨勢及成長分析報告(2026-2034年)日本電網自動化市場規模、佔有率、趨勢及預測(按組件、應用、最終用戶和地區分類),2026-2034年液態空氣儲能市場-全球產業規模、佔有率、趨勢、機會、預測:按容量、應用、地區和競爭格局分類,2021-2031年

全球壓縮空氣儲能市場規模、佔有率、趨勢及成長分析報告(2026-2034年)日本電網自動化市場規模、佔有率、趨勢及預測(按組件、應用、最終用戶和地區分類),2026-2034年液態空氣儲能市場-全球產業規模、佔有率、趨勢、機會、預測:按容量、應用、地區和競爭格局分類,2021-2031年