|

市場調查報告書

商品編碼

2072448

青貯飼料添加劑:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Silage Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

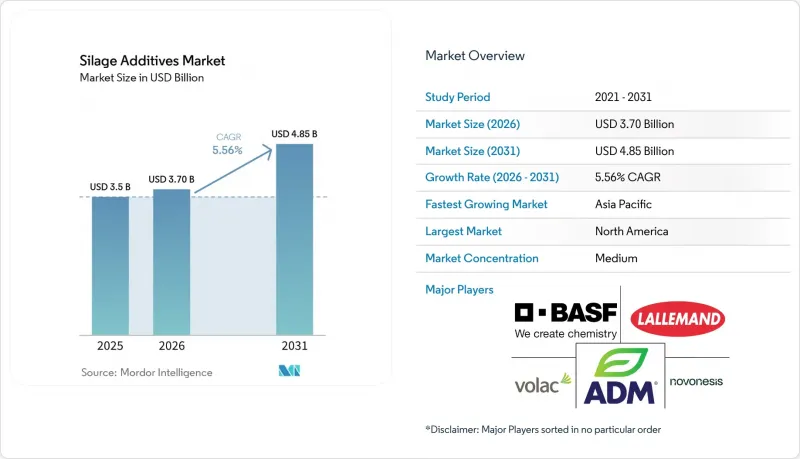

據 Mordor Intelligence 稱,2025 年青貯飼料添加劑市值為 35 億美元,預計到 2031 年將達到 48.5 億美元,而 2026 年為 37 億美元,預測期(2026-2031 年)的複合年成長率為 5.56%。

本報告按添加劑類型(接種劑、有機酸和鹽、酵素、吸附劑、防腐劑及其他)、青貯飼料類型(穀物、豆類及其他青貯飼料)和地區(北美、歐洲、亞太、南美以及中東和非洲)進行細分。市場預測以價值(美元)和數量(公噸)表示。

全球青貯添加劑市場趨勢與洞察

提高乳牛和肉牛的生產力目標

人們越來越關注如何最大限度地提高每頭牲畜的產奶量和產肉量,這推動了青貯添加劑市場的成長。這些產品對於提高飼料配方的效率和品質至關重要。美國農業部 (USDA) 預測,到 2026 年,平均每頭飼料的產奶量將達到 11.07 公噸,這凸顯了高品質青貯飼料對於支持此生產力的重要性。為了佐證這一預測,Lallemand 公司在 2025 年報告稱,其 Magniva Platinum 草青貯接種劑在 160 天內將中性清潔劑纖維 (NDF) 的消化率提高了 5.4 個百分點,並在試驗期間使每頭牲畜的日產奶量增加了 1.23 公斤。這些結果凸顯了青貯添加劑在提高畜牧生產力方面的重要作用,消費者的購買決策也從單純考慮加工成本轉向關注其對牛奶和肉類生產的貢獻。在飼料種植面積有限的地區,這種轉變更為關鍵,因為必須在相同的土地面積上實現更高的生產力。因此,對青貯飼料添加劑的需求不斷成長,反映出畜牧業管理越來越重視效率和生產力。

工業化畜牧養殖和飼料系統的擴張

此外,中國、印度和巴西等國工業化畜牧養殖體系的推廣,以及標準化飼料防腐劑使用量的增加,也推動了青貯飼料添加劑市場的擴張。在中國,農業農村部於2025年發布的「飼料計畫」旨在推廣青貯飼料的使用,以減少飼料配方中對穀物的依賴。新華社2026年2月通報稱,到2025年,內蒙古通遼市青貯玉米種植面積將達到8,039萬公頃,顯示商業性畜牧養殖體系的飼料基礎正在快速擴張。此外,聯合國糧農組織(FAO)和經濟合作暨發展組織(OECD)預測,到2034年,全球畜牧業產量將成長16.6%,其中中低收入國家的畜牧業成長預計將佔較大比例。這一趨勢正在擴大青貯飼料添加劑市場中入門級接種劑、緩衝酸混合物和區域性防腐劑產品的基本客群。

原料和有機酸的價格波動

在青貯飼料添加劑市場,原料價格波動劇烈,因為有機酸產品受化學原料和能源成本波動的影響。這種壓力在丙酸和甲酸產品線中尤其明顯,因為這些產品的利潤率較低,且顧客對價格較為敏感。大規模商業酪農可以透過長期供應合約更容易應對這些價格波動,但小規模企業往往會在價格上漲時減少用量或轉而使用規格較低的產品。此外,歐洲飼料添加劑法規限制了配方降級,因為即使成本高昂,也必須維持產品規格和純度標準。這些因素共同導致價格敏感地區的市場接受度降低,進一步加劇了青貯飼料添加劑市場中型生產商的壓力。

細分市場分析

2025年,接種劑仍維持其市場主導地位,佔青貯添加劑市場45.0%的佔有率。這一主導地位源於其在玉米、牧草和豆科植物青貯中的廣泛應用,以及其在集約化酪農和牛生產系統中顯著的投資回報。有機酸和鹽類是成長最快的添加劑類型,預計2026年至2031年將達到6.0%的複合年成長率。隨著生產商逐漸減少對純甲酸產品的使用,緩衝型和混合酸防腐劑正受到越來越多的關注。這種成長與對更安全、腐蝕性更低的配方的需求,以及在接種劑處理和低溫運輸可靠性不足的地區對靈活保藏方法的需求密切相關。

在青貯添加劑市場的其他領域,由於複合發酵劑兼具快速降低pH值和飼餵過程中高需氧穩定性的優點,市場對其需求日益成長。均質發酵發酵劑持續用於較簡單的青貯條件下,而異質發酵產品則擴大用於高乾物質玉米系統,因為這類系統有較高的熱原風險。隨著農場越來越重視纖維消化率、黴菌控制和黴菌毒素管理,酵素、發酵和腐敗抑制劑以及吸附劑的作用也不斷擴大。其他添加劑,包括糖基和營養基產品,雖然仍屬於小眾產品,但在濕飼料和豆科青貯計畫中發揮重要作用,尤其是在亞太和非洲地區。

區域分析

到2025年,北美將佔據青貯飼料添加劑市場34.5%的佔有率,成為最大的區域市場。美國之所以能保持領先地位,得益於其高度機械化的玉米青貯系統以及大規模酪農對飼料性能的精細監控。根據美國農業部預測,到2025年,美國牛奶產量將達到2,226億磅,乳牛存欄量將達到906萬頭,這將維持高水準的青貯飼料產量和添加劑需求。該地區的成長反映了市場滲透率的日趨成熟,同時多菌株產品的附加價值也在不斷提升。在加拿大和墨西哥,隨著集約化酪農和牛生產的擴張以及供應商獲得優質複合產品的管道日益豐富,市場需求也逐漸成長。

預計2026年至2031年間,亞太地區青貯飼料添加劑市場將以7.0%的複合年成長率(CAGR)實現最高成長,其中中國和印度將佔據新增需求的大部分。中國的「2025年飼料節約行動計畫」正在推廣使用青貯飼料以減少對穀物的依賴,這進一步凸顯了在商業性畜牧系統中引入防腐劑的必要性。南美洲預計也將成長,其中巴西將引領成長;中東和非洲的需求也在增加,因為在炎熱氣候下,商業性酪農的擴張增加了需氧腐敗的風險。

受德國、法國、英國和荷蘭等國的強勁推動,歐洲青貯飼料添加劑市場預計將在2026年至2031年間保持強勁的複合年成長率。儘管該地區市場已趨於成熟,但仍保持活躍,因為好氧穩定性及認證標準會影響消費者的購買決策。德國農業協會(DLG)的測試架構發揮品質篩選的作用,評估那些能夠在既定的青貯飼料生產規範下持續展現產品功效的供應商。 2024年六亞甲四胺的禁用迫使該地區部分產品線調整配方,到2024年11月,ADDCON已完成向六亞甲四胺的“KOFASIL LP”和“KOFASIL Ultra”產品的過渡。俄羅斯仍然是大規模的青貯飼料市場,但進口限制和本地生產的限制正在減緩高級產品的普及。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對乳牛和肉牛的生產力目標更加嚴格

- 工業化畜牧養殖和飼料系統的擴張

- 重點在於減少飼料損耗和乾物質損失。

- 向生物來源接種劑和微發酵過渡

- 高水分青貯飼料中黴菌毒素風險的管理

- 需要快速轉運船用燃料和儘早供應燃料。

- 市場限制因素

- 原料和有機酸的價格波動

- 監理核准和標籤標註的負擔

- 活微生物的保存與應用中的敏感性

- 飼料不均勻性導致生產力波動

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 添加劑的種類

- 接種劑

- 同型發酵

- 異型性發酵

- 組合接種劑

- 有機酸和鹽

- 甲酸及其鹽

- 丙酸及其鹽

- 乳酸和乳酸鹽

- 緩衝劑和混合酸性防腐劑

- 酵素

- 纖維消化酶

- 澱粉消化酶

- 複合酶混合物

- 吸附劑

- 黏土和礦物基吸附劑

- 纖維和穀物運輸車

- 防止發酵和腐敗的添加劑

- 黴菌抑制劑(非酸性)

- 有氧穩定性增強劑

- 其他類型

- 糖添加物

- 營養添加物

- 接種劑

- 青貯類型

- 乾草青貯

- 穀類

- 玉米

- 高粱

- 燕麥

- 大麥

- 其他穀物青貯

- 豆科植物

- 苜蓿

- 三葉草

- 其他豆科植物青貯飼料

- 混合飼料青貯

- 其他特殊青貯飼料

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 土耳其

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Archer-Daniels-Midland Company

- BASF SE

- Alltech, Inc.

- Lallemand Inc.

- Volac International Limited

- Novonesis A/S

- Corteva, Inc.

- Kemin Industries, Inc.

- ADDCON GmbH

- H. Wilhelm Schaumann GmbH

- Agri-King, Inc.

- EW Nutrition

- Josera GmbH & Co. KG

- Nutreco NV

- Cargill, Incorporated

- Market Opportunities and Future Outlook

According to Mordor Intelligence, the silage additives market size was valued at USD 3.5 billion in 2025 and estimated to grow from USD 3.7 billion in 2026 to reach USD 4.85 billion by 2031, at a CAGR of 5.56% during the forecast period (2026-2031).

This report is Segmented by Additive Type (Inoculants, Organic Acids and Salts, Enzymes, Adsorbents, Preservatives, and Other Types), by Silage Type (Cereals, Legumes, and Other Silage Types), and by Geography (North America, Europe, Asia-Pacific, South America, Middle-East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Silage Additives Market Trends and Insights

Intensifying Dairy and Beef Productivity Targets

The increasing focus on maximizing milk and beef production per animal is driving the silage additives market, as these products are essential for improving ration efficiency and forage quality. The United States Department of Agriculture (USDA) projects that average milk production per cow will reach 11.07 metric tons by 2026, highlighting the need for high-quality silage to support such productivity. Supporting this, Lallemand reported in 2025 that its MAGNIVA Platinum grass silage inoculant improved neutral detergent fiber digestibility by 5.4 percentage points over 160 days, resulting in an additional 1.23 kg of daily milk yield per cow during the trials. These results emphasize the role of silage additives in enhancing livestock output, shifting purchasing decisions to focus on their contribution to milk and meat production rather than just treatment costs. In regions with limited forage acreage, this shift is even more critical, as operations must achieve higher productivity from the same land base. Consequently, the growing demand for silage additives reflects the increasing priority placed on efficiency and output in livestock management.

Scaling Industrial Livestock and Forage Systems

The silage additives market is also expanding as industrial livestock systems spread across China, India, and Brazil, increasing the use of standardized forage preservation inputs. In China, the Ministry of Agriculture and Rural Affairs' feed-saving plan released in 2025 promotes silage use to reduce grain dependence in feed rations. Xinhua reported in February 2026 that Tongliao in Inner Mongolia had 80.39 million hectares of silage corn in 2025, showing how quickly the forage base is being scaled for commercial livestock systems. The FAO and the OECD also project global livestock output to grow by 16.6% through 2034, with lower-middle-income countries driving proportionately stronger herd expansion. That trend broadens the customer base for entry-level inoculants, buffered acid blends, and region-specific preservation products in the silage additives market.

Raw Material and Organic Acid Price Volatility

Raw material price remain volatile in the silage additives market because organic acid products are exposed to volatile chemical feedstocks and energy costs. This pressure is strongest in the propionic acid and formic acid lines, where margins are thinner and customers are often more price-sensitive. Large commercial dairies can absorb these moves more easily through longer supply contracts, but smaller operators often cut application rates or shift to lower-specification products when prices rise. European feed additive rules also limit downward reformulation because product specifications and purity standards must still be maintained during cost spikes. That combination slows adoption in price-sensitive regions and puts mid-scale manufacturers under more pressure in the silage additives market.

Other drivers and restraints analyzed in the detailed report include:

- Feed Shrink and Dry Matter Loss Reduction Focus

- Shift Toward Biological Inoculants and Precision Fermentation

- Regulatory Approval and Labeling Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inoculants held the largest share, accounting for 45.0% of the silage additives market share in 2025. Their lead came from broad use across corn, grass, and legume silage, along with a clear return on investment in intensive dairy and beef systems. Organic acids and salts are the fastest-growing additive type, registering 6.0% CAGR through 2026-2031, with buffered and blended acid preservatives gaining traction as producers shift away from neat formic acid products. This growth is tied to demand for safer, less corrosive formulations and to the need for flexible preservation tools in regions where inoculant handling and cold-chain reliability are less consistent.

Within the remaining segments of the silage additives market, combination inoculants are gaining premium demand because they pair rapid pH reduction with stronger aerobic stability at feedout. Homofermentative inoculants continue to serve simpler ensiling conditions, while heterofermentative products are seeing greater use in high-dry-matter corn systems where heating risks are high. Enzymes, fermentation and spoilage control additives, and adsorbents are also expanding their role as farms place more emphasis on fiber digestibility, mold control, and mycotoxin management. Other additive types, including sugar-based and nutrient-based products, remain niche but relevant in wet forage and legume silage programs, especially in the Asia-Pacific and Africa.

Complete Report Scope:

- Additive Type

- Inoculants

- Homofermentative

- Heterofermentative

- Combination Inoculants

- Organic Acids and Salts

- Formic Acid and Formates

- Propionic Acid and Propionates

- Lactic Acid and Lactates

- Buffered/Blended Acid Preservatives

- Enzymes

- Fiber-Digesting Enzymes

- Starch-Digesting Enzymes

- Multi-enzyme Blends

- Adsorbents

- Clay and Mineral Adsorbents

- Fiber and Grain Carriers

- Fermentation & Spoilage Control Additives

- Mold Inhibitors (Non-Acid Based)

- Aerobic Stability Enhancers

- Other Types

- Sugar-based Additives

- Nutrient-based Additives

- Inoculants

- Silage Type

- Grass Silage

- Cereals

- Corn

- Sorghum

- Oats

- Barley

- Other Cereal Silage

- Legumes

- Alfalfa

- Clover

- Other Legume Silage

- Mixed Forage Silage

- Other Specialty Silage

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Turkey

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America held 34.5% of the silage additives market share in 2025, making it the largest regional market. The United States maintains this lead because corn silage systems are highly mechanized, and large dairies closely monitor feed performance. The United States Department of Agriculture reported milk production at 222.6 billion pounds in 2025 in the United States and a milking herd of 9.06 million head, which keeps silage volumes and additive demand high. Regional growth is reflecting mature penetration but continued value expansion through multi-strain products. Canada and Mexico add incremental demand as intensive dairy and beef operations expand and suppliers widen access to premium formulations.

Asia-Pacific is projected to record the fastest 7.0% CAGR during 2026-2031 in the silage additives market, with China and India providing most of the new demand. China's 2025 Feed-Saving Action Plan promotes the use of silage to reduce grain dependence, strengthening the case for preservation inputs across commercial livestock systems. South America is projected to grow, led by Brazil, while the Middle East and Africa are also seeing rising demand as commercial dairy operations expand in hot climates that increase the risk of aerobic spoilage.

Europe is set to grow at a descent CAGR during 2026-2031 in the silage additives market, with Germany, France, the United Kingdom, and the Netherlands leading the way. The region remains mature yet remains active because aerobic stability and certification standards shape buying decisions. Germany's Deutsche Landwirtschafts-Gesellschaft testing framework acts as a quality filter, rewarding suppliers that can continue to demonstrate efficacy under defined silage protocols. The 2024 hexamine ban forced reformulation across part of the regional portfolio, and ADDCON completed the move to hexamine-free KOFASIL LP and KOFASIL Ultra by November 2024. Russia remains a sizable silage market, but import access and local production constraints slow the adoption of premium products.

- Archer-Daniels-Midland Company

- BASF SE

- Alltech, Inc.

- Lallemand Inc.

- Volac International Limited

- Novonesis A/S

- Corteva, Inc.

- Kemin Industries, Inc.

- ADDCON GmbH

- H. Wilhelm Schaumann GmbH

- Agri-King, Inc.

- EW Nutrition

- Josera GmbH & Co. KG

- Nutreco N.V.

- Cargill, Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying dairy and beef productivity targets

- 4.2.2 Scaling industrial livestock and forage systems

- 4.2.3 Feed shrink and dry matter loss reduction focus

- 4.2.4 Shift toward biological inoculants and precision fermentation

- 4.2.5 Mycotoxin risk control in high-moisture silage

- 4.2.6 Faster bunker turnaround and early feedout needs

- 4.3 Market Restraints

- 4.3.1 Raw material and organic acid price volatility

- 4.3.2 Regulatory approval and labeling burden

- 4.3.3 Live-microbe storage and application sensitivity

- 4.3.4 Performance variability from forage heterogeneity

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Additive Type

- 5.1.1 Inoculants

- 5.1.1.1 Homofermentative

- 5.1.1.2 Heterofermentative

- 5.1.1.3 Combination Inoculants

- 5.1.2 Organic Acids and Salts

- 5.1.2.1 Formic Acid and Formates

- 5.1.2.2 Propionic Acid and Propionates

- 5.1.2.3 Lactic Acid and Lactates

- 5.1.2.4 Buffered/Blended Acid Preservatives

- 5.1.3 Enzymes

- 5.1.3.1 Fiber-Digesting Enzymes

- 5.1.3.2 Starch-Digesting Enzymes

- 5.1.3.3 Multi-enzyme Blends

- 5.1.4 Adsorbents

- 5.1.4.1 Clay and Mineral Adsorbents

- 5.1.4.2 Fiber and Grain Carriers

- 5.1.5 Fermentation & Spoilage Control Additives

- 5.1.5.1 Mold Inhibitors (Non-Acid Based)

- 5.1.5.2 Aerobic Stability Enhancers

- 5.1.6 Other Types

- 5.1.6.1 Sugar-based Additives

- 5.1.6.2 Nutrient-based Additives

- 5.1.1 Inoculants

- 5.2 Silage Type

- 5.2.1 Grass Silage

- 5.2.2 Cereals

- 5.2.2.1 Corn

- 5.2.2.2 Sorghum

- 5.2.2.3 Oats

- 5.2.2.4 Barley

- 5.2.2.5 Other Cereal Silage

- 5.2.3 Legumes

- 5.2.3.1 Alfalfa

- 5.2.3.2 Clover

- 5.2.3.3 Other Legume Silage

- 5.2.4 Mixed Forage Silage

- 5.2.5 Other Specialty Silage

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Netherlands

- 5.3.3.7 Russia

- 5.3.3.8 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 New Zealand

- 5.3.4.6 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Turkey

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Archer-Daniels-Midland Company

- 6.4.2 BASF SE

- 6.4.3 Alltech, Inc.

- 6.4.4 Lallemand Inc.

- 6.4.5 Volac International Limited

- 6.4.6 Novonesis A/S

- 6.4.7 Corteva, Inc.

- 6.4.8 Kemin Industries, Inc.

- 6.4.9 ADDCON GmbH

- 6.4.10 H. Wilhelm Schaumann GmbH

- 6.4.11 Agri-King, Inc.

- 6.4.12 EW Nutrition

- 6.4.13 Josera GmbH & Co. KG

- 6.4.14 Nutreco N.V.

- 6.4.15 Cargill, Incorporated

- 6.5 Market Opportunities and Future Outlook