|

市場調查報告書

商品編碼

2066737

美國藥品倉庫:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

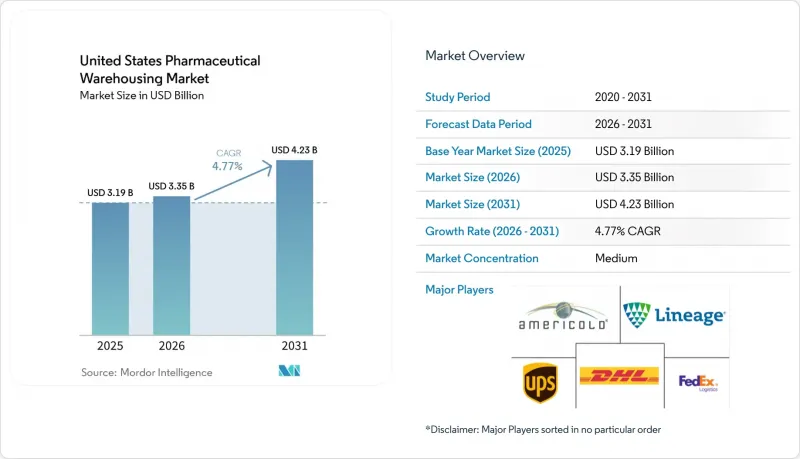

根據 Mordor Intelligence 預測,美國藥品倉庫市場規模將從 2025 年的 31.9 億美元和 2026 年的 33.5 億美元成長到 2031 年的 42.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.77%。

本報告按服務類型(倉儲、配送和庫存管理等)、倉庫類型(低溫運輸倉庫[冷藏、冷凍等]、非低溫運輸倉庫)、產品類型(處方藥、成藥等)和最終用戶(製藥公司、醫療保健機構等)進行細分。市場預測以美元計價。

美國藥品倉儲市場趨勢與洞察

外包給專門從事醫療領域的第三方物流公司(3PL)的做法正在迅速增加。

隨著製造商將資源集中在創新和產品開發,而非自建倉儲基礎設施,倉儲產業正經歷著向外包和合約模式的明顯轉變。大型物流整合商,尤其是那些在醫療保健物流領域拓展業務的公司,正在加速這項轉變。這些公司正在收購低溫運輸專家,並建立整合的端到端供應鏈解決方案。此類整合能夠更有效地管理對溫度敏感的藥品和生物製藥,同時滿足嚴格的合規要求。隨著監管要求日益嚴格,包括設施驗證和產品可追溯性,合規成本不斷攀升,小規模專業倉儲業者難以負擔。這進一步加速了規模更大、資金更雄厚的物流供應商的轉變。

國內疫苗和抗體生產能力的擴大正在推動物流中心。

美國製藥公司正在大幅擴展其生產基礎設施,其中生物製藥製造業尤其成為物流和倉儲需求的主要驅動力。先進生物製造技術的興起,推動了對能夠管理整個生產和分銷週期中溫度敏感材料的專用低溫運輸設施的需求成長。低溫儲存系統對於儲存mRNA和其他生物製藥至關重要。這不僅需要更高的能源容量,而且此類儲存服務的費用也更高,因此利潤豐厚。因此,低溫運輸倉儲已成為該產業資本策略的核心要素,生物製藥的成長與物流投資直接相關。

責任險和產品召回險的保費不斷上漲。

尤其是在細胞和基因療法的分銷領域,隨著保險公司應對日益成長的風險,圍繞藥品物流的保險環境正變得愈發嚴格。這些產品的高昂單價和複雜的處理要求導致召回保險費大幅上漲,迫使物流供應商加強品管和可追溯性措施。同時,序列化和可追溯性法規的實施也暴露了傳統倉儲系統的脆弱性。缺乏互通即時追蹤能力的設施將面臨高額的附加保費,這有力地推動了整個藥品供應鏈的快速數位轉型。

細分市場分析

到2025年,倉儲服務將保持在美國藥品倉儲市場66.38%的佔有率,但附加價值服務市場將以5.74%的複合年成長率成長,這主要得益於序列化、套件組裝和臨床試驗包裝等服務帶來的每平方英尺收入成長40%至60%。這些加值服務依賴小規模設施無法提供的檢驗IT和品管基礎設施,從而強化了產業的整合趨勢。能夠透過雲端儀錶板提供即時庫存可見性並實現無縫ERP整合的倉庫已被90%的客戶採用,從而建立了牢固的長期合作關係。此外,鑑於業界嚴格的重新序列化要求,與藥品供應鏈服務協議(DSCSA)相關的退貨處理正在成為一項永續的收入來源。

美國藥品倉儲市場正向高附加價值服務轉型,以患者為中心的客製化包裝和法規諮詢成為關鍵的差異化優勢。提供溫度映射、驗證和審計支援的供應商正在建立穩定的收入來源,同時鞏固其在合規和卓越分銷方面的合作夥伴地位。

至2025年,非低溫運輸設施將占美國藥品倉庫市場的75.06%,營運成本低廉,約每平方英尺9美元。同時,受生物製藥、疫苗和個人化療法等需要2°C至-196°C溫度控制的藥品需求驅動,低溫運輸市場預計到2031年將以5.91%的複合年成長率成長。雖然超低溫和低溫區域的利潤率比常溫區域高出數倍,但它們卻佔倉庫總電力消耗量的79%。因此,維修以提高能源效率和自動化檢索系統對於盈利和遵守永續性法規至關重要。

一體化營運商正在將常溫區和低溫運輸區合併在同一場地,以最大限度地提高周轉率,並透過物聯網驅動的預測性維護將意外停機時間減少了 60%。在美國藥品倉儲市場,超低溫儲存的佔有率仍然很小,但考慮到每個托盤 50 至 75 美元的費用,它所佔的利潤比例卻相當高。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 外包業務激增,主要外包給專注於醫療領域的第三方物流公司。

- 國內疫苗和抗體生產能力的擴大正在推動對樹突狀細胞的需求。

- 引入自動化和機器人技術以提高GMP準確性

- 擴大專科藥局的分銷網路

- 以ESG主導的低碳、高能源效率冷庫維修

- 在使用無人機/電動車的最後一公里示範計畫中,需要在前線部署微型冷庫。

- 市場限制因素

- 責任險和產品召回險的保費不斷上漲。

- 由於建築材料短缺,倉庫建設工程延誤。

- 各州新的資料隱私法各不相同,對物聯網分析有所限制。

- 極端天氣波動導致資本支出(CAPEX)增加,以確保暖通空調系統的冗餘性。

- 價值供應鏈分析

- 監管狀態(FDA、DSCSA、DEA、OSHA)

- 科技趨勢(倉庫管理系統、物聯網、自動化、機器人技術)

- 波特五力模型

- 地緣政治因素與疫情對倉儲業的影響

第5章 市場規模與成長預測

- 按服務類型

- 貯存

- 經銷和庫存管理

- 附加價值服務及其他

- 倉庫類型

- 低溫運輸倉庫

- 冷藏(0-5 度C)

- 冰點(-18 至 0°C)

- 常溫倉庫

- 深度冷凍/超低溫(低於-20 度C)

- 非低溫運輸倉庫

- 低溫運輸倉庫

- 依產品類型

- 處方藥

- 成藥

- 生物製劑和生物相似藥

- 疫苗和血液製品

- 臨床試驗材料

- 細胞和基因治療

- 特種藥品(非生物製藥)

- 動物用藥品

- 其他

- 最終用戶

- 製藥公司

- 醫療服務提供方

- 零售和藥房

- 銷售代理商和批發商

- 其他

第6章 競爭情勢

- 市場集中度

- 戰略措施和投資

- 市佔率分析

- 公司簡介

- United Parcel Service Inc.

- DHL Group

- FedEx Corp.

- GEODIS SA

- CEVA Logistics

- Lineage Logistics

- Americold Logistics

- Cencora

- BioPharma Logistics

- Rhenus SE & Co. KG

- Kuehne+Nagel

- XPO Logistics

- KRC Logistics

- GXO Logistics

- MD Logistics

- Langham Logistics

- Crown LSP Group

- LifeScience Logistics

- Go Freight

- DSV

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states pharmaceutical warehousing market size is projected to expand from USD 3.19 billion in 2025 and USD 3.35 billion in 2026 to USD 4.23 billion by 2031, registering a CAGR of 4.77% between 2026 and 2031.

This report is Segmented by Service Type (Storage, Distribution and Inventory Management, and More), by Warehouse Type (Cold-Chain Warehouse [Chilled, Frozen, and More], Non-Cold-Chain Warehouse), by Product Type (Prescription, OTC Drugs, and More), and by End User (Pharmaceutical Manufacturers, Healthcare Providers, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Pharmaceutical Warehousing Market Trends and Insights

Outsourcing Surge to Healthcare-Focused 3PLs

The warehousing landscape is witnessing a clear shift toward outsourced and contract-based models as manufacturers focus their resources on innovation and product development instead of owning storage infrastructure. This transition is being accelerated by major logistics integrators, particularly those expanding in healthcare logistics, who are acquiring cold-chain specialists to build integrated, end-to-end supply solutions. Such consolidation allows them to manage temperature-sensitive pharmaceuticals and biologics more effectively while meeting stringent compliance requirements. Increasing regulatory demands, such as those related to facility validation and product traceability, have raised the cost of compliance to levels that smaller, niche warehouse operators often find difficult to sustain, further reinforcing the move toward large, well-capitalized logistics providers.

Ramp-up of Domestic Vaccine & Antibody Capacity Fueling DC Demand

Pharmaceutical companies in the United States are significantly expanding their production infrastructure, particularly in biologics manufacturing, which is now a key driver of logistics and warehousing demand. The rise of advanced biomanufacturing has intensified the need for specialized cold-chain facilities capable of managing temperature-sensitive materials throughout the production and distribution cycle. Ultra-low-temperature storage systems are essential for supporting mRNA and other biologic formulations, not only requiring higher energy capacity but also generating strong returns due to the premium pricing of such storage services. As a result, cold-chain warehousing has become a central component of the sector's capital strategy, linking biomanufacturing growth directly with logistics investment.

Escalating Liability & Product-Recall Insurance Premiums

The insurance environment for pharmaceutical logistics is tightening as underwriters respond to rising exposure risks, particularly in cell and gene therapy distribution. High product values and complex handling requirements have made recall insurance significantly more expensive, pushing logistics operators to strengthen quality and traceability measures. At the same time, enforcement of serialization and traceability regulations is exposing weaknesses in legacy warehouse systems. Facilities lacking interoperable, real-time tracking capabilities are facing steep premium surcharges, creating strong incentives for rapid digital modernization across the pharmaceutical supply chain.

Other drivers and restraints analyzed in the detailed report include:

- Automation & Robotics Deployments Improving GMP Accuracy

- Expansion of Specialty-Pharmacy Distribution Networks

- Construction-Material Shortages Delaying Warehouse Build-outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage retained 66.38% of the United States Pharmaceutical Warehousing market share in 2025, but value-added services are expanding at a 5.74% CAGR as serialization, kitting, and clinical-trial packaging deliver 40-60% higher revenue per ft2. These premium services rely on validated IT and quality-management infrastructures that smaller facilities cannot match, reinforcing consolidation trends. Warehouses offering real-time inventory visibility through cloud dashboards and seamless ERP integrations report 90% client adoption, cementing sticky long-term contracts. Returns processing tied to DSCSA has also emerged as a sustainable profit pool, given the industry's strict re-serialization requirements.

The United States pharmaceutical warehousing is evolving toward higher-value services, with custom patient packaging and regulatory consulting becoming key differentiators. Providers offering temperature mapping, validation, and audit-readiness support are building recurring revenue streams while reinforcing their role as partners in compliance and distribution excellence.

Non-cold-chain sites accounted for 75.06% of the United States Pharmaceutical Warehousing market size in 2025, benefiting from lower operating expenses of roughly USD 9/ft2. Cold-chain, however, is set to post a 5.91% CAGR through 2031, pulled by biologics, vaccines, and personalized therapies that require temperatures from 2 °C down to -196 °C. Ultra-low and cryogenic zones yield margins several times higher than ambient space but consume 79% of total warehouse electricity. Energy-efficiency retrofits and automated retrieval systems are therefore critical for profitability and sustainability compliance.

Integrated operators blend ambient and cold-chain zones inside the same campus to maximize asset turns, while IoT-enabled predictive maintenance slashes unplanned downtime by 60%. The United States Pharmaceutical Warehousing market share in ultra-low storage remains small but represents a disproportionate share of profits given per-pallet fees of USD 50-75.

List of Companies Covered in this Report:

- United Parcel Service Inc.

- DHL Group

- FedEx Corp.

- GEODIS SA

- CEVA Logistics

- Lineage Logistics

- Americold Logistics

- Cencora

- BioPharma Logistics

- Rhenus SE & Co. KG

- Kuehne + Nagel

- XPO Logistics

- KRC Logistics

- GXO Logistics

- MD Logistics

- Langham Logistics

- Crown LSP Group

- LifeScience Logistics

- Go Freight

- DSV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outsourcing Surge to Healthcare-Focused 3PLs

- 4.2.2 Ramp-Up of Domestic Vaccine & Antibody Capacity Fueling DC Demand

- 4.2.3 Automation & Robotics Deployments Improving GMP Accuracy

- 4.2.4 Expansion of Specialty-Pharmacy Distribution Networks

- 4.2.5 ESG-Driven Retrofits for Low-Carbon, Energy-Efficient Cold Stores

- 4.2.6 Drone/EV Last-Mile Pilots Requiring Forward-Staged Micro Cold Sites

- 4.3 Market Restraints

- 4.3.1 Escalating Liability & Product-Recall Insurance Premiums

- 4.3.2 Construction-Material Shortages Delaying Warehouse Buildouts

- 4.3.3 Patchwork of New State Data-Privacy Laws Limiting IoT Analytics

- 4.3.4 Extreme-Weather Volatility Raising HVAC Redundancy CAPEX

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (FDA, DSCSA, DEA, OSHA)

- 4.6 Technological Outlook (WMS, IoT, Automation, Robotics)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics and Pandemic on Warehousing

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.2 By Warehouse Type

- 5.2.1 Cold-Chain Warehouse

- 5.2.1.1 Chilled (0-5°C)

- 5.2.1.2 Frozen (-18-0°C)

- 5.2.1.3 Ambient

- 5.2.1.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.2.2 Non-Cold-Chain Warehouse

- 5.2.1 Cold-Chain Warehouse

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Specialty Medicine (non-biologic)

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By End User

- 5.4.1 Pharmaceutical Manufacturers

- 5.4.2 Healthcare Providers

- 5.4.3 Retail and Pharmacies

- 5.4.4 Distributors and Wholesalers

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 United Parcel Service Inc.

- 6.4.2 DHL Group

- 6.4.3 FedEx Corp.

- 6.4.4 GEODIS SA

- 6.4.5 CEVA Logistics

- 6.4.6 Lineage Logistics

- 6.4.7 Americold Logistics

- 6.4.8 Cencora

- 6.4.9 BioPharma Logistics

- 6.4.10 Rhenus SE & Co. KG

- 6.4.11 Kuehne + Nagel

- 6.4.12 XPO Logistics

- 6.4.13 KRC Logistics

- 6.4.14 GXO Logistics

- 6.4.15 MD Logistics

- 6.4.16 Langham Logistics

- 6.4.17 Crown LSP Group

- 6.4.18 LifeScience Logistics

- 6.4.19 Go Freight

- 6.4.20 DSV

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

醫藥倉儲市場:按溫度類型、服務類型、儲存類型、自動化程度、產品類型和最終用戶分類 - 全球預測(2026-2032 年)

醫藥倉儲市場:按溫度類型、服務類型、儲存類型、自動化程度、產品類型和最終用戶分類 - 全球預測(2026-2032 年) 醫藥倉儲市場規模、佔有率及成長分析(依服務類型、運輸方式、最終用戶及地區分類)-2026-2033年產業預測

醫藥倉儲市場規模、佔有率及成長分析(依服務類型、運輸方式、最終用戶及地區分類)-2026-2033年產業預測 2025年全球醫藥倉儲市場報告

2025年全球醫藥倉儲市場報告 醫藥倉儲市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

醫藥倉儲市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年) 全球醫藥倉儲市場(2025-2029)

全球醫藥倉儲市場(2025-2029) 中國醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)德國醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)德國醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 全球藥品倉庫市場

全球藥品倉庫市場 全球藥品倉儲市場規模研究,按類型(冷鏈倉儲、非冷鏈倉儲)、按應用(藥廠、藥房、醫院等)以及 2022-2032 年區域預測

全球藥品倉儲市場規模研究,按類型(冷鏈倉儲、非冷鏈倉儲)、按應用(藥廠、藥房、醫院等)以及 2022-2032 年區域預測