|

市場調查報告書

商品編碼

2066734

雙組分纖維:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Bicomponent Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

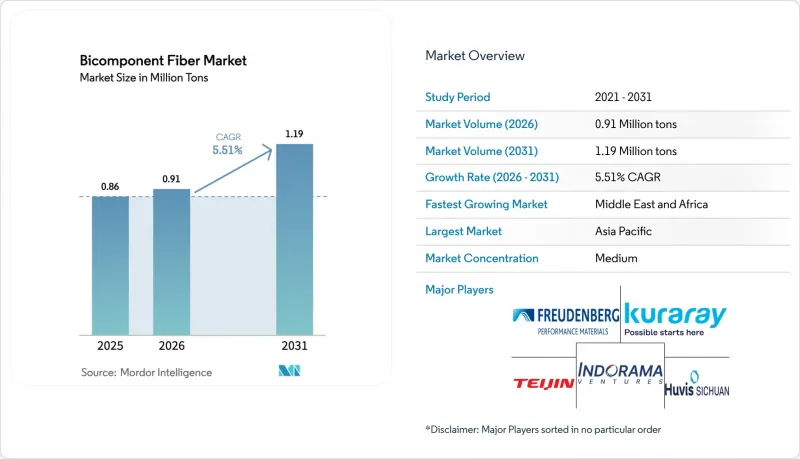

據 Mordor Intelligence 稱,雙組分纖維市場預計將從 2025 年的 86 萬噸成長到 2026 年的 91 萬噸,到 2031 年達到 119 萬噸,預計 2026 年至 2031 年的複合年成長率為 5.51%。

雙組分纖維市場報告按材料(例如,聚乙烯(PE)/聚丙烯(PP)、聚丙烯(PP)/聚對苯二甲酸乙二醇酯(PET))、結構類型(例如,鞘套結構、並排結構)、終端用戶產業(例如,不織布、汽車產業)和地區(亞太地區、北美地區、北美地區、歐洲地區、中東地區和歐洲地區進行細分。市場預測以噸為單位。

全球雙組分纖維市場趨勢與洞察

衛生用品的普及率不斷提高

尤其在歐洲、日本和北美,人口老化推動了成人失禁紙尿褲、護墊和襯墊的人均消費量成長。熱黏合PE/PP鞘套不織布能夠實現更薄的芯層、更快的吸收速度和更低的皮膚刺激性,為衛生用品品牌帶來成本績效優勢。跨國公司持續在印度、印尼和奈及利亞等地推進紙尿褲和女性用衛生用品的在地化生產,刺激了該地區對雙組分短纖維和紡黏纖維的需求。僅印度加工商預計在2025年至2026年間,紙尿褲的運作能將超過40億片,其吸收層和分散層均依賴國內的PE/PP供應鏈。由於單位成本降低,紙尿褲的滲透率正從大都會圈擴展到第二線城市和農村地區,為未來幾年的銷售量成長奠定了堅實的基礎。這些因素共同作用,不僅擴大了雙組分纖維在衛生用品行業的市場佔有率,也提高了亞太地區各條生產線的產能運轉率。

不織布產業的需求不斷成長

汽車內裝供應商正採用具有「海島」結構的雙組分超細纖維取代聚氨酯泡棉。這種材質重量更輕,同時也能實現類似絨面革的表面質感,滿足電動車的減重目標。產業數據顯示,預計2026年,汽車不織布的消費量將達到180萬噸,其中用於車頂內襯和門板的層壓材料比例將持續成長。過濾應用也是一個高附加價值領域。經鹼處理的「海島」結構長絲可形成亞微米級孔隙,從而提高暖通空調(HVAC)和液體過濾的效率。 TWE集團等區域性製造商計劃於2025年在博帕爾運作可擴展的紡粘生產平台,以滿足國內外的需求。中國西部地區對用於擦拭巾和醫用不織布的水針工藝的資本投資,進一步鞏固了亞太地區在不織布領域的領先地位,並推動了對具有可靠濕強度性能的鞘套芯粘合劑的需求成長。

生產成本高且資本投資集中

與單聚合物系統相比,雙擠出生產線、精密計量泵和客製化噴絲頭會使資本投資增加30%至50%,這使得中型加工商難以進行新的投資。帝人位於泰國TPL的擴建工程(已於2025年底完工)清晰地展現了這種財務規模。要實現每年700噸的共軛長絲產能,需要專門的冷卻系統和複雜的控制迴路,導致固定的長期折舊免稅額計畫。歐洲和南美部分地區的高利率進一步提高了專案的門檻,這有利於那些能夠將折舊成本分散到其衛生、醫療和過濾業務組合中的垂直整合型跨國公司。缺乏用於新型生物基或再生聚合物組合的標準化模具延長了研發週期,在首公斤商業化產品交付之前增加了工程成本。這些因素共同削弱了資本投資受限地區雙組分纖維市場的成長潛力。

細分市場分析

預計到2025年,PE/PP雙組分纖維市場規模將佔總市場的38.40%。這主要歸功於其在尿布面層、吸收/分散層和熱封膜等領域的廣泛應用。由於這些材料的熔點差異適中,既能確保纖維間牢固結合,又不影響其柔軟度,因此PE/PP仍然是通用衛生不織布領域的領先材料。然而,隨著品牌商對單一材料包裝和可回收電池隔膜的需求不斷成長,預計PE/PET組合材料在預測期(2026-2031年)內將以6.45%的複合年成長率成長。這些組合材料兼具PET的剛性和PE的低溫流動性,能夠滿足包裝袋、蓋子和重疊片等產品在搬運和使用後處理方面的要求。

此外,用於汽車頂棚的PP/PET吸音氈、用於電纜包覆和屋頂防水卷材的HDPE/LDPE透氣膜以及用於高溫過濾的聚酯/PBT共混物等領域均取得了逐步進展。 2025年至2026年間提交的專案專利申請提案了將生物基聚乙烯和PLA作為鞘套組件的技術,旨在將可再生材料含量提高到30%以上,儘管目前產量仍然小規模。隨著新的回收目標即將到來,材料選擇預計將轉向有利於化學或機械分離的結構。這種轉變已在歐洲加工商的測試中得到體現,他們採用的單聚烯結構符合10%的回收材料含量標準。

區域分析

到2025年,亞太地區將佔全球產量的46.50%。 2025年至2026年間,中國加工商擴大了水針和紡粘纖維的產能;同時,印度衛生用品製造商在古吉拉突邦和拉賈斯坦邦新建了數十億件的尿布工廠,提振了當地對PE/PP鞘套和芯材纖維的需求。日本東麗和帝人公司推動了「海中島」和共聚物長絲技術的研發,推動了特種產品向航太和過濾產業的客戶出口。韓國在電池隔膜領域的研發生態系統與這些優勢相輔相成,使該地區成為雙組分纖維市場的核心創新中心。

在北美,ANSI/AAMI PB70阻隔等級和ISO 10993生物相容性測試的實施提高了品質標準,使能夠保證批次級可追溯性的本土供應商更具優勢。 Indorama Ventures位於喬治亞的辦事處已融入FiberVisions網路,正在幫助實施精益庫存管理的衛生用品製造商縮短前置作業時間。汽車輕量化專案不斷開拓新市場,尤其是在電動車製造商指定使用超細纖維吸音材料和低VOC內裝紡織品的情況下。

在歐洲,2025年10月生效的生產者責任延伸(EPR)法規,強制推行環保定價和逐步提高再生材料含量標準(2028年達到10%,2030年達到15%,2035年達到30%),重塑了材料藍圖。歐瑞康-布爾馬格(Oerlikon-Burmag)與贏創(Evonik)的合作,旨在到2030年實現再生PET紡絲生產線的商業化,是供應商朝著循環經濟目標邁進的一個良好例證。該地區的汽車供應鏈也在向可分割的超細纖維座椅布料轉型,以滿足車載排放氣體和減重的目標。

中東和非洲地區目前規模較小,預計到2031年將達到6.56%的複合年成長率,與亞太地區相當。不斷上升的出生率、仍然較低的衛生用品普及率以及可支配收入的增加,正在推動尿布和女性用衛生用品消費的成長。波灣合作理事會(GCC)的產業政策鼓勵衛生用品成品在當地組裝,從而刺激了對區域紡織品生產能力的需求。同時,南非以出口為導向的汽車產業正擴大採用雙組分吸音氈,以符合歐洲的噪音標準。

南美市場佔有率的成長主要得益於巴西不斷擴大的衛生用品市場和阿根廷具有成本競爭力的紡粘薄膜出口。儘管外匯波動抑制了投資意願,但區域加工商正利用有利的勞動力和能源成本,向北美供應通用級產品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 衛生用品的普及應用範圍擴大

- 不織布產業的需求增加

- 永續發展驅動的向可回收纖維轉型

- 用於電池隔膜的低熔點鞘套和芯材纖維

- 應用於3D列印複合材料材料增強材料

- 市場限制因素

- 生產成本高,資本投資強度高

- 聚烯和PET原料價格波動劇烈

- 缺乏高溫雙組分紡絲能力

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 材料

- 聚乙烯(PE)/聚丙烯(PP)

- 聚丙烯(PP)/聚對苯二甲酸乙二醇酯(PET)

- 高密度聚苯乙烯(HDPE)/低密度聚乙烯(LDPE)

- 聚乙烯(PE)/聚對苯二甲酸乙二醇酯(PET)

- 聚酯(PET)/PBT

- 其他材料

- 依結構類型

- 鞘套芯結構

- 並排結構

- 海島結構

- 其他結構類型

- 按最終用戶行業分類

- 不織布

- 車

- 衛生

- 建造

- 醫學領域

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- Asahi Kasei Advanced Fibers

- CHA Technologies Group

- EMS-Chemie Holding AG

- Far Eastern New Century Corporation

- FiberVisions Corporation

- Fitesa SA

- Freudenberg Performance Materials

- Indorama Ventures Public Company Limited.

- JNC Corporation

- Kolon Glotech

- Kuraray Co., Ltd.

- OC Oerlikon Management AG

- PTT Global Chemical PCL

- Shandong Helon Co., Ltd.

- Shaoxing Yaolong Spunbonded Nonwoven Technology Co., Ltd.

- Sichuan Huvis

- Suominen Corporation

- Teijin Limited

- Toray Industries, Inc.

- WPT Nonwovens Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the bicomponent fiber market size is expected to increase from 0.86 million tons in 2025 to 0.91 million tons in 2026 and reach 1.19 million tons by 2031, growing at a CAGR of 5.51% over 2026-2031.

The Bicomponent Fiber Market Report is by Material (Polyethylene (PE)/Polypropylene (PP), Polypropylene (PP)/Polyethylene Terephthalate (PET), and More), Structure Type (Sheath-Core, Side-By-Side, and More), End-User Industry (Non-Woven Textiles, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Bicomponent Fiber Market Trends and Insights

Growing Adoption in Hygiene Products

Demographic aging, especially in Europe, Japan, and North America, is increasing per-capita uptake of adult-incontinence briefs, pads, and liners. Thermally bonded PE/PP sheath-core nonwovens enable thinner cores, faster fluid acquisition, and reduced skin irritation, giving hygiene brands a cost-performance edge. Multinationals continue to localize diaper and feminine-care production in India, Indonesia, and Nigeria, stimulating regional demand for bicomponent staple and spunbond fibers. Indian converters alone commissioned more than 4 billion diaper unit capacity between 2025 and 2026, relying on domestic PE/PP supply chains for acquisition and distribution layers. As unit costs fall, penetration is widening beyond metropolitan centers into tier-2 cities and rural districts, reinforcing a multiyear runway for volume growth. These vectors together lift hygiene's share of the bicomponent fiber market while improving capacity utilization across Asia-Pacific lines.

Rising Demand from Nonwoven Textiles

Automotive interior suppliers are substituting polyurethane foams with islands-in-the-sea bicomponent microfibers that offer suede-like surfaces at lower mass, satisfying electric-vehicle lightweighting goals. Industry data show automotive nonwoven consumption on track to reach 1.8 million tons in 2026, with headliners and door-panel laminates absorbing a growing share. Filtration is another high-value slot; after alkaline splitting, islands-in-the-sea filaments create sub-micron pores that boost efficiency in HVAC (heating, ventilation, and air conditioning) and liquid filtration. Regional manufacturers such as TWE Group commissioned scalable spunbond platforms in Bhopal during 2025, aiming to meet both domestic and export demand. Capital investment in spunlace for wipes and medical fabrics across Western China further cements Asia-Pacific's leadership in nonwovens, driving incremental demand for sheath-core binders with reliable wet-strength performance.

High Production Cost and CAPEX Intensity

Dual-extrusion lines, precision metering pumps, and custom spinnerets lift capital outlays 30%-50% above single-polymer alternatives, making greenfield investments difficult for mid-tier converters. Teijin's expansion at TPL Thailand, completed in late 2025, illustrates the financial scale, 700 tons per year of conjugate-filament capacity required specialized quench systems and advanced control loops, locking in lengthy depreciation schedules. High interest rates in Europe and parts of South America further stretch project hurdle rates, favoring vertically integrated multinationals that spread amortization across hygiene, medical, and filtration portfolios. The absence of standardized tooling for novel bio-based or recycled polymer pairs prolongs research and development cycles, adding engineering cost before a single commercial kilogram is shipped. These factors collectively shave growth potential off the bicomponent fiber market in capex-constrained regions.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability-Driven Shift to Recyclable Fibers

- Low-Melt Sheath-Core Fibers for Battery Separators

- Volatile Polyolefin and PET Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Bicomponent Fiber market size for PE/PP blends represented 38.40% of total volume in 2025, thanks to their dominant use in diaper topsheets, acquisition-distribution layers, and thermal-bonding webs. Their moderate melt-point gap ensures strong inter-fiber bonding without jeopardizing softness, keeping PE/PP the workhorse material in commodity hygiene nonwovens. Even so, PE/PET pairings are on track for a 6.45% CAGR during the forecast period (2026-2031) as brand owners seek monomaterial packaging and recyclable battery separators. These combinations merge PET's stiffness with PE's low-temperature flow, satisfying both handling and end-of-life criteria in pouch, lid, and overwrap formats.

Sequential advancements are also unfolding in PP/PET acoustic felts for automotive headliners, HDPE/LDPE breathable films for cable-wrap and roofing membranes, and Polyester/PBT blends for high-temperature filtration. Specialty patents filed during 2025-2026 introduced bio-based polyethylene and PLA as sheath components to raise renewable content above 30%, yet volumes remain small. As new recycling targets loom, material choices are expected to tilt toward constructions that ease chemical or mechanical separation, a pivot already visible in European converter trials adopting mono-polyolefin architectures that hit the 10% recycled-content threshold.

Geography Analysis

Asia-Pacific supplied 46.50% of global volume in 2025. Chinese converters expanded spunlace and spunbond capacity throughout 2025-2026, while Indian hygiene producers opened multi-billion-unit diaper plants in Gujarat and Rajasthan, lifting local offtake for PE/PP sheath-core fibers. Japan's Toray and Teijin advanced islands-in-the-sea and conjugate-filament technologies, powering specialty exports to aerospace and filtration customers. South Korea's battery-separator R&D ecosystem complements these strengths, positioning the sub-region as the innovation nucleus of the bicomponent fiber market

In North America, enforcement of ANSI/AAMI PB70 barrier levels and ISO 10993 biocompatibility tests elevates quality bars, favoring domestic suppliers who can assure lot-level traceability. Indorama Ventures' Georgia site, integrated into the FiberVisions network, shortens lead times for hygiene customers managing lean inventories. Automotive lightweighting programs continue to open new outlets, especially as electric-vehicle manufacturers specify microfiber acoustics and low-VOC interior textiles.

In Europe, the EPR regulation that took effect in October 2025 imposes eco-modulated fees and staged recycled-content thresholds, 10% by 2028, 15% by 2030, and 30% by 2035, reshaping material roadmaps. Oerlikon Barmag's partnership with Evonik to commercialize recycled-PET spinning lines by 2030 exemplifies supplier moves to align with circular-economy objectives. The region's automotive supply chain is also migrating toward splittable microfiber seat fabrics to meet interior emission and weight targets.

The Middle East and Africa, though smaller today, is projected to share Asia-Pacific's 6.56% CAGR through 2031. Rising birth rates and still-low hygiene penetration combine with growing disposable incomes to unlock diaper and feminine-care consumption. Gulf Cooperation Council industrial policy is encouraging localized assembly of hygiene finished goods, creating a pull effect for regional fiber capacity. South Africa's export-oriented auto industry, meanwhile, is adopting bicomponent acoustic felts to comply with European noise standards.

South America's market share is led by Brazil's expanding hygiene market and Argentina's cost-competitive spunbond exports. Currency volatility tempers investment enthusiasm, yet regional converters exploit favorable labor and energy economics to serve North American commodity grades.

- Asahi Kasei Advanced Fibers

- CHA Technologies Group

- EMS-Chemie Holding AG

- Far Eastern New Century Corporation

- FiberVisions Corporation

- Fitesa S.A.

- Freudenberg Performance Materials

- Indorama Ventures Public Company Limited.

- JNC Corporation

- Kolon Glotech

- Kuraray Co., Ltd.

- OC Oerlikon Management AG

- PTT Global Chemical PCL

- Shandong Helon Co., Ltd.

- Shaoxing Yaolong Spunbonded Nonwoven Technology Co., Ltd.

- Sichuan Huvis

- Suominen Corporation

- Teijin Limited

- Toray Industries, Inc.

- WPT Nonwovens Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption in hygiene products

- 4.2.2 Rising demand from non-woven textiles

- 4.2.3 Sustainability-driven shift to recyclable fibers

- 4.2.4 Low-melt sheath-core fibers for battery separators

- 4.2.5 Use in 3-D printed composite reinforcement

- 4.3 Market Restraints

- 4.3.1 High production cost and CAPEX intensity

- 4.3.2 Volatile polyolefin and PET feedstock prices

- 4.3.3 Limited high-temperature bi-component spinning capacity

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Material

- 5.1.1 Polyethylene (PE)/Polypropylene (PP)

- 5.1.2 Polypropylene (PP)/Polyethylene Terephthalate (PET)

- 5.1.3 High-density Polyethylene (HDPE)/Low-density Polyethylene (LDPE)

- 5.1.4 Polyethylene (PE)/Polyethylene Terephthalate (PET)

- 5.1.5 Polyester (PET)/PBT

- 5.1.6 Other Materials

- 5.2 By Structure Type

- 5.2.1 Sheath-core

- 5.2.2 Side-by-Side

- 5.2.3 Islands in the Sea

- 5.2.4 Other Structure Types

- 5.3 By End-user Industry

- 5.3.1 Non-woven Textiles

- 5.3.2 Automotive

- 5.3.3 Hygiene

- 5.3.4 Construction

- 5.3.5 Medical

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Asahi Kasei Advanced Fibers

- 6.4.2 CHA Technologies Group

- 6.4.3 EMS-Chemie Holding AG

- 6.4.4 Far Eastern New Century Corporation

- 6.4.5 FiberVisions Corporation

- 6.4.6 Fitesa S.A.

- 6.4.7 Freudenberg Performance Materials

- 6.4.8 Indorama Ventures Public Company Limited.

- 6.4.9 JNC Corporation

- 6.4.10 Kolon Glotech

- 6.4.11 Kuraray Co., Ltd.

- 6.4.12 OC Oerlikon Management AG

- 6.4.13 PTT Global Chemical PCL

- 6.4.14 Shandong Helon Co., Ltd.

- 6.4.15 Shaoxing Yaolong Spunbonded Nonwoven Technology Co., Ltd.

- 6.4.16 Sichuan Huvis

- 6.4.17 Suominen Corporation

- 6.4.18 Teijin Limited

- 6.4.19 Toray Industries, Inc.

- 6.4.20 WPT Nonwovens Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Future Applications of Recycled Bicomponent Fibers

連續纖維複合材料市場:按樹脂類型、產品類型、增強材料類型、產業和地區分類(2026-2034 年)

連續纖維複合材料市場:按樹脂類型、產品類型、增強材料類型、產業和地區分類(2026-2034 年) 纖維增強複合材料市場:依纖維類型、樹脂類型、製造流程、增強材料形式和應用分類-2026-2032年全球市場預測

纖維增強複合材料市場:依纖維類型、樹脂類型、製造流程、增強材料形式和應用分類-2026-2032年全球市場預測 碳纖維熱塑性複合材料市場規模、佔有率和趨勢分析報告:按原料、應用、地區和細分市場分類(2026-2033 年)CFRTP市場:2026-2032年全球市場預測(按樹脂類型、產品類型、纖維類型、製造流程、應用和最終用戶分類)雙組分纖維市場:依纖維類型、製造流程、應用和分銷管道分類-2026-2032年全球預測半導體CFC設備市場:按類型、技術和終端用戶產業分類,全球預測,2026-2032年

碳纖維熱塑性複合材料市場規模、佔有率和趨勢分析報告:按原料、應用、地區和細分市場分類(2026-2033 年)CFRTP市場:2026-2032年全球市場預測(按樹脂類型、產品類型、纖維類型、製造流程、應用和最終用戶分類)雙組分纖維市場:依纖維類型、製造流程、應用和分銷管道分類-2026-2032年全球預測半導體CFC設備市場:按類型、技術和終端用戶產業分類,全球預測,2026-2032年 全球雙組分纖維市場規模、佔有率、趨勢和成長分析報告:2026-2034年CFRT預浸料市場按樹脂類型、纖維類型、產品形式、製造流程、最終用途產業和應用分類-2026-2032年全球預測植物纖維增強複合材料市場:依應用、基體類型、纖維類型、製造流程及纖維處理方式分類-2026-2032年全球預測碳纖維增強熱塑性複合材料(CFRTP)市場-2025-2030年預測

全球雙組分纖維市場規模、佔有率、趨勢和成長分析報告:2026-2034年CFRT預浸料市場按樹脂類型、纖維類型、產品形式、製造流程、最終用途產業和應用分類-2026-2032年全球預測植物纖維增強複合材料市場:依應用、基體類型、纖維類型、製造流程及纖維處理方式分類-2026-2032年全球預測碳纖維增強熱塑性複合材料(CFRTP)市場-2025-2030年預測