|

市場調查報告書

商品編碼

2066731

原子鐘:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Atomic Clock - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

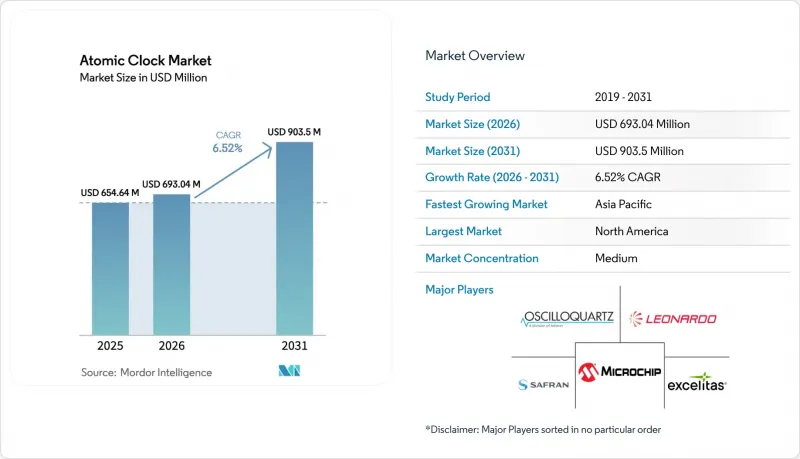

根據 Mordor Intelligence 預測,原子鐘市場規模將從 2025 年的 6.5464 億美元成長到 2026 年的 6.9304 億美元,然後在 2031 年達到 9.035 億美元,2026 年至 2031 年的複合年成長率為 5.4%。

本報告按類型(銣、銫、氫原子鐘)、最終用戶(國防、航太、民用/商業)、應用(導航、監視、電子戰、通訊、金融交易/資料中心、廣播/媒體等)和地區(北美、歐洲、亞太等)進行分類。市場預測以美元計價。

全球原子鐘市場趨勢及洞察

全球導航衛星系統(GNSS)衛星群的擴展

全球導航衛星系統(GNSS)衛星群的擴展和多頻接收器的設計提高了太空時鐘的長期穩定性和抗輻射能力,這持續推動著中高地球軌道對基於銣原子鐘和氫原子鐘的設備的需求。洛克希德馬丁公司計劃於2026年初在其第十顆GPS III衛星上進行數位原子鐘的飛行測試,這將使每日穩定性超越目前的銣原子鐘基準值,並標誌著GPS現代化在軌時間管理能力的又一次飛躍。在歐洲,兩顆伽利略衛星於2025年12月的發射增強了服務的連續性。專案簡報也確認,第二代伽利略系統將增加數位有效載荷、衛星間鏈路和實驗性時鐘技術,以提高其穩健性和精確度。 2024年9月,中國發射了搭載改良氫原子鐘的北斗59號和60號衛星,以支援北斗四號藍圖的實施。北斗四號旨在檢驗新一代時間和頻率的性能,並將覆蓋範圍擴展到更深的空間。各國的這些投資清楚地表明,原子鐘市場將繼續受益於衛星平台的更新換代以及用戶儀器中多衛星群的廣泛應用。

5G/6G網路的相位同步要求

5G Advanced 和早期 6G藍圖中的新型無線電功能正朝著亞奈秒網路同步和亞毫秒端到端延遲的方向發展,以實現定位、感知和互動式服務,從而推動對銣原子鐘和邊緣高精度時間傳輸的投資。廠商對 6G 的願景聲明強調了物理層高精度時間的重要性,以實現互動式地圖和分散式智慧。這項需求迫使通訊業者增強 GNSS 故障期間的維持能力並提高容錯能力。隨著通訊業者也正在為關鍵基礎設施組織替代和補充的 PNT(定位、導航和時間)方案,這推動了對來自多家供應商的高精度授時技術的評估和採購,尤其是在訊號遺失期間時間漂移不可接受的網路中。隨著相位連貫無線電、邊緣推理和時間敏感網路技術的擴展,原子鐘市場預計將吸引除主要國防領域參與者之外的更多公司參與。

單價高且資本投資高度集中

對於需要特殊組裝、長時間老化和廣泛認證的特定任務型原子鐘而言,價格仍然是阻礙因素,導致其成本曲線遠高於量產的通訊定時設備。光晶格鐘目前仍處於商業化初期,試生產單位的售價超過50萬美元。相比之下,用於網路同步的銣原子鐘售價低於5000美元。晶片級原子鐘在低功耗運行的同時,提高了便攜性,但長期穩定性和漂移之間的權衡通常需要採用混合架構,這會增加成本和整合複雜性。專案資訊披露強調了效能的提升,但缺乏明確的單價,這使得新參與企業和小規模整合商難以進行競爭性基準測試。 Frequency Electronics近期在航太定時領域的得標凸顯了市場需求的強勁,但公開文件中的單價數據仍保密。由於這些經濟因素,買家往往會考慮效能、SWaP(尺寸、重量和功耗)和生命週期支援之間的平衡,並選擇選擇性部署或分階段部署。

細分市場分析

預計到2025年,銫原子鐘將佔據40.50%的市場佔有率,並預計在2031年之前以5.90%的複合年成長率成長,這主要得益於其在計量、國防校準以及作為網路主時鐘等方面的廣泛應用。國家標準的升級進一步鞏固了銫原子鐘的地位。例如,NIST-F4標準在2025年4月達到了2.2/10^16的精度,主導UTC(美國國家標準與技術研究院)的運行,並為關鍵基礎設施的計時控制提供資料支援。供應商也致力於提升銫原子鐘平台的短期精度,例如Oscilloquartz公司對其光學銫原子鐘進行的改進,旨在實現亞奈秒的保持精度和飛秒級的穩定性(持續一秒)。在高可用性網路中,銫原子鐘仍是長期標準,而時間傳輸和網路架構提供的冗餘機制,使得原子鐘市場不再基於單一標準,而是基於多種原子鐘的混合陣列。由於銫原子鐘是監管合規和服務等級義務的基礎,尤其是在時間一致性具有法律和營運意義的領域,因此該領域的市場前景穩定。

銣原子鐘和晶片級原子鐘(CSAC)佔據了剩餘市場的主導地位,使其適用於對便攜性、能源效率和多年穩定性要求極高的航太和國防任務,且成本合理。 Microchip 的第二代低雜訊 CSAC 提高了功率和溫度耐受性,適用於現場應用,為無人系統和地面通訊提供了更多選擇,即使在 GNSS 故障的情況下,也能透過備用功能繼續運作。在航太計畫中,考慮到尺寸、重量和功耗 (SWaP) 與長期劣化和老化之間的權衡,銣原子鐘和氫原子鐘仍然被用作輔助有效載荷。在地面,操作人員結合使用銫原子鐘、銣原子鐘和基於網路的時間傳輸來控制成本和性能。中國的研究機構也致力於降低星載氫原子鐘的質量和功耗,從傳統的 23 公斤設計轉向適用於下一代衛星的 15 公斤新型配置。透過這些趨勢,銫原子鐘仍然是主要標準,而銣原子鐘和 CSAC 原子鐘正在擴展到受 SWaP 限制的角色,從而支援跨平台和任務剖面的平衡原子鐘市場。

區域分析

到2025年,北美將佔據31.91%的市場佔有率。這主要得益於國防、航太和關鍵基礎設施領域的現代化項目,這些項目為精密授時提供了大規模部署的基礎。國家標準的升級和太空時鐘實驗,包括美國國家標準與技術研究院(NIST)的各項舉措和美國國家航空航太局(NASA)的相關項目,正在鞏固該地區在計量學和深空導航領域的領先地位。飛機和衛星授時設備的合約活動持續進行,原始設備製造商(OEM)宣布了與可靠的定位、導航和授時(PNT)以及政府客戶高精度同步需求相關的額外訂單。這些投資不僅維持了原子鐘市場的需求基礎,也擴大了營運商在網路同步和時間傳輸方面的應用範圍。

亞太地區正處於最快的成長軌道上,預計2026年至2031年將以5.87%的複合年成長率成長。這主要得益於中國北斗四號計畫的推進,該計畫旨在檢驗下一代氫原子鐘在軌運行,並計劃於2035年覆蓋深空。印度及其區域夥伴正持續加強其定位、導航和授時(PNT)策略,投資於航太和通訊領域的授時增強型基礎設施。澳洲將於2024年根據AUKUS計畫的「第二支柱」資助研發用於國防的量子光鐘,並計畫於2025年交付。這顯示盟國的授時技術基礎正在多元化發展。隨著各國計畫將自主研發與選擇性進口結合,亞太地區的原子鐘市場正受益於政策主導的本土化和商業平台的擴張。

在歐洲,伽利略系統的部署以及基於空間的時間傳輸和計量實驗的擴展正在穩步推進。 2025年12月,兩顆伽利略衛星搭乘阿里安6號火箭發射升空,以增強衛星星系的容錯能力。此外,根據歐洲太空總署(ESA)的簡報,第二代伽利略系統將包含更先進的有效載荷和實驗性時鐘類型。 ESA在國際太空站(ISS)上的ACES任務正在推進高精度時間傳輸並與世界一流的地面時鐘連接,使歐洲計量技術能夠滿足新的科學和商業性應用需求。英國在2025年繼續資助利用量子技術的定位、導航和授時(PNT)研究,支援一系列用於未來基礎設施部署的光鐘和時間傳輸解決方案。這些活動為歐洲原子鐘市場在航太、通訊和科學領域的前景保持樂觀。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 衛星定位系統的擴展

- 5G/6G網路的相位同步要求

- 國防現代化計劃和超高精度計時

- 用於物聯網邊緣設備的晶片級原子鐘正在湧現。

- 量子感測技術的整合以及研發支出的增加

- 安全通訊和電子戰系統的發展

- 市場限制因素

- 單位成本高且資本投資高度集中

- 嚴格的出口限制

- 濃縮同位素供應瓶頸

- 專業基礎設施的複雜性和外部干擾

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 銣(Rb)原子鐘

- 銫原子鐘

- 氫原子鐘

- 最終用戶

- 防禦

- 戰鬥機和直升機

- 無人駕駛車輛

- 裝甲車輛

- 可攜式系統

- 海軍艦艇(驅逐艦、護衛艦)

- 潛水艇

- 巡邏艇

- 宇宙

- 公共/商業

- 防禦

- 透過使用

- 監視

- 導航

- 電子戰

- 遙測

- 電訊

- 金融交易與資料中心

- 廣播與媒體

- 工業和科學測量儀器

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 南美洲

- 巴西

- 其他南美國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AccuBeat Ltd.

- Excelitas Technologies Corp.

- IQD Frequency Products Limited

- Leonardo SpA

- Microchip Technology Incorporated

- Oscilloquartz SA(Adtran Networks SE)

- Stanford Research Systems

- VREMYA-CH JSC

- Safran SA

- MacQsimal(CSEM)(accelopment Schweiz AG)

- Thermo Fisher Scientific Inc.

- Frequency Electronics, Inc.

- Abracon LLC

- AOSense, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the atomic clock market size is expected to grow from USD 654.64 million in 2025 to USD 693.04 million in 2026 and is forecasted to reach USD 903.50 million by 2031 at a 5.44% CAGR over 2026-2031.

This report is Segmented by Type (Rubidium, Cesium, and Hydrogen Maser), End User (Defense, Space, and Civil and Commercial), Application (Navigation, Surveillance, Electronic Warfare, Telecommunication, Financial Trading and Data Centers, Broadcast and Media, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Atomic Clock Market Trends and Insights

Satellite Navigation Constellation Expansion

Expanding GNSS constellations and multi-frequency receiver design raise the bar on long-term stability and radiation tolerance for space-borne clocks, which sustains premium demand for rubidium and hydrogen-maser payloads across medium and high orbits. Lockheed Martin plans to flight test a digital atomic clock on the tenth GPS III satellite in early 2026 to push daily stability beyond the baseline for current rubidium clocks, signaling a next step in on-orbit timekeeping performance for GPS modernization. Europe strengthened service continuity when two Galileo spacecraft launched in December 2025, and program briefings confirm that Galileo Second Generation will add digital payloads, inter-satellite links, and experimental clock technologies to improve robustness and precision. China launched the 59th and 60th BeiDou satellites in September 2024 with upgraded hydrogen atomic clocks to validate next-generation time-frequency performance and support a BeiDou-4 roadmap toward deeper space coverage. These national investments send a clear signal that the atomic clock market will continue to benefit from satellite platform refresh cycles and broader multi-constellation adoption across user equipment.

5G/6G Network Phase-Synchronization Requirements

New radio features in 5G Advanced and early 6G roadmaps are converging on sub-nanosecond network synchronization and sub-millisecond end-to-end latency for positioning, sensing, and interactive services, directing spending toward rubidium references and high-grade time transfer at the edge. Vendor vision statements for 6G highlight the need for precise time at the physical layer to enable interactive maps and distributed intelligence. This requirement pushes operators to harden holdover and improve resilience during GNSS disruptions. This technical shift keeps the atomic clock market closely tied to telecom modernization cycles as operators upgrade base stations, deploy edge compute nodes, and extend time distribution into data centers. Public agencies also catalogue alternative and complementary PNT approaches for critical infrastructure, which sustains multi-vendor evaluation and uplifts procurement for precision timing in networks that cannot tolerate drift during signal loss. As phase-coherent radio, edge inference, and time-sensitive networking scale, the atomic clock market sees broader enterprise participation beyond defense primes.

High Unit Costs and Capital Expenditure Intensity

Pricing remains a limiting factor for mission-specific atomic clocks that require niche assemblies, long burn-in, and extensive qualification, which keeps the cost curve elevated relative to volume telecom timing. Optical lattice clocks are currently in the early stages of commercialization, with pilot production units priced at over USD 500,000. In contrast, rubidium atomic clocks used for network synchronization are available for less than USD 5,000. Chip-scale atomic clocks improve portability while operating on low power budgets, though long-term stability and drift trade-offs often require hybrid architectures that add cost and integration complexity. Program disclosures highlight performance improvements without transparent unit pricing, making competitive benchmarking difficult for new entrants and smaller integrators. Frequency Electronics' recent awards in airborne timing underscore the strength of demand, yet per-unit cost data remains proprietary in public filings. These economics encourage selective deployments and staged rollouts as buyers balance performance, SWaP, and lifecycle support.

Other drivers and restraints analyzed in the detailed report include:

- Defense Modernization Programs and Ultra-Precise Timing

- Quantum-Sensing Integration and Increased R&D Funding

- Strict Export-Control Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cesium atomic clocks held a 40.50% share in 2025 and are projected to grow at a 5.90% CAGR through 2031, supported by their role as the primary frequency reference in metrology, defense calibration, and network master-clock duties. Cesium's standing is reinforced by national-reference upgrades, including NIST-F4, which reached 2.2 parts in 10^16 accuracy in April 2025 and contributes data to steer UTC(NIST) and support critical infrastructure timing. Vendors also advance short-term precision on cesium platforms, as shown by Oscilloquartz's enhancements to optical cesium clocks that target sub-nanosecond holdover and femtosecond stability over 1 second. In high-availability networks, cesium remains the long-term anchor, while time transfer and network architecture handle redundancy, keeping the atomic clock market oriented around hybrid clock ensembles rather than a single standard. The segment's outlook is stable because cesium underpins regulatory compliance and service-level obligations in sectors where timing integrity carries legal and operational consequences.

Rubidium and chip-scale atomic clocks make up the balance and align with space and defense missions that prize portability, power efficiency, and multi-year stability at moderate cost. Microchip's second-generation low-noise CSAC improves power and temperature resilience for field use, broadening options for unmanned systems and dismounted communications that require holdover to survive GNSS outages. Space programs continue to use rubidium and hydrogen maser clocks as complementary payloads that trade SWaP against long-term drift and aging. At the same time, on the ground, operators mix cesium, rubidium, and network-based time transfer to manage cost and performance. Chinese research institutes also target mass and power reductions in space-borne hydrogen clocks, moving from legacy 23 kg designs to new 15 kg configurations to fit next-generation satellites. Across these paths, cesium remains the primary anchor, while rubidium and CSACs expand into SWaP-constrained roles, supporting a balanced atomic clock market across platforms and mission profiles.

Geography Analysis

North America secured a 31.91% share in 2025 as modernization programs in defense, space, and critical infrastructure anchored a large installed base of precision timing. National reference upgrades and space-clock experiments, including NIST efforts and NASA-linked programs, reinforce the region's leadership in metrology and deep-space navigation. Contract activity for airborne and satellite timing also continued, with OEMs announcing follow-on awards tied to assured PNT and high-precision synchronization requirements for government customers. These investments maintain demand depth in the atomic clock market while operators broaden network synchronization and time-transfer footprints.

Asia-Pacific charts the fastest trajectory, with a 5.87% CAGR from 2026 to 2031, as China validates next-generation hydrogen clocks in orbit and scales up plans for BeiDou-4 to achieve deep-space coverage by 2035. India and regional partners continue to strengthen sovereign PNT agendas and invest in timing-enhanced infrastructure across the aerospace and telecommunications sectors. Australia funded quantum-optical clock efforts for defense under AUKUS Pillar II in 2024, with deliveries planned through 2025, a signal that allied programs are diversifying their timing technology base. As national programs mix domestic development with selective imports, the atomic clock market in Asia-Pacific benefits from both policy-driven localization and commercial platform scaling.

Europe maintains steady progress with Galileo deployments and expanded experimentation in space-based time transfer and metrology. Two Galileo satellites were launched in December 2025 on an Ariane 6 to bolster constellation resilience, and ESA briefings confirm that Galileo Second Generation will add more advanced payloads and experimental clock types. ESA's ACES mission on the ISS advances precise time transfer and links world-leading ground clocks, which helps European metrology engage with new scientific and commercial use cases. The UK continued to fund quantum-enabled PNT research in 2025, which supports a pipeline of optical-clock and time-transfer solutions for future infrastructure deployments. These activities sustain a healthy outlook for the atomic clock market in Europe across space, telecoms, and scientific domains.

- AccuBeat Ltd.

- Excelitas Technologies Corp.

- IQD Frequency Products Limited

- Leonardo S.p.A.

- Microchip Technology Incorporated

- Oscilloquartz SA (Adtran Networks SE)

- Stanford Research Systems

- VREMYA-CH JSC

- Safran SA

- MacQsimal (CSEM) (accelopment Schweiz AG)

- Thermo Fisher Scientific Inc.

- Frequency Electronics, Inc.

- Abracon LLC

- AOSense, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Satellite navigation constellation expansion

- 4.2.2 5G/6G network phase-synchronization requirements

- 4.2.3 Defense modernization programs and ultra-precise timing

- 4.2.4 Emergence of chip-scale atomic clocks for IoT edge devices

- 4.2.5 Quantum-sensing integration and increased R&D funding

- 4.2.6 Growth of secure communications and electronic warfare systems

- 4.3 Market Restraints

- 4.3.1 High unit costs and capital expenditure intensity

- 4.3.2 Strict export-control regulations

- 4.3.3 Supply bottlenecks of enriched isotopes

- 4.3.4 Complexities in specialized infrastructure and external disruptions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Rubidium (Rb) Atomic Clock

- 5.1.2 Cesium (Cs) Atomic Clock

- 5.1.3 Hydrogen (H) Maser Atomic Clock

- 5.2 By End User

- 5.2.1 Defense

- 5.2.1.1 Combat Aircraft and Helicopters

- 5.2.1.2 Unmanned Vehicles

- 5.2.1.3 Armoured Vehicles

- 5.2.1.4 Portable Systems

- 5.2.1.5 Naval Ships (Destroyers, Frigates)

- 5.2.1.6 Submarines

- 5.2.1.7 Patrol Vessels

- 5.2.2 Space

- 5.2.3 Civil and Commercial

- 5.2.1 Defense

- 5.3 By Application

- 5.3.1 Surveillance

- 5.3.2 Navigation

- 5.3.3 Electronic Warfare

- 5.3.4 Telemetry

- 5.3.5 Telecommunication

- 5.3.6 Financial Trading and Data Centers

- 5.3.7 Broadcast and Media

- 5.3.8 Industrial and Scientific Instrumentation

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 AccuBeat Ltd.

- 6.4.2 Excelitas Technologies Corp.

- 6.4.3 IQD Frequency Products Limited

- 6.4.4 Leonardo S.p.A.

- 6.4.5 Microchip Technology Incorporated

- 6.4.6 Oscilloquartz SA (Adtran Networks SE)

- 6.4.7 Stanford Research Systems

- 6.4.8 VREMYA-CH JSC

- 6.4.9 Safran SA

- 6.4.10 MacQsimal (CSEM) (accelopment Schweiz AG)

- 6.4.11 Thermo Fisher Scientific Inc.

- 6.4.12 Frequency Electronics, Inc.

- 6.4.13 Abracon LLC

- 6.4.14 AOSense, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

原子鐘市場規模、佔有率和成長分析:按時鐘技術類型、系統平台配置、關鍵功能、最終用戶類別和地區分類-2026-2033年產業預測

原子鐘市場規模、佔有率和成長分析:按時鐘技術類型、系統平台配置、關鍵功能、最終用戶類別和地區分類-2026-2033年產業預測 2026年全球量子鐘市場報告

2026年全球量子鐘市場報告 手錶市場:按類型、技術、產品類型、組件、應用和最終用戶分類-2026-2032年全球預測航太級冷原子鐘市場:按應用、最終用戶、產品類型、部署類型分類,全球預測(2026-2032)

手錶市場:按類型、技術、產品類型、組件、應用和最終用戶分類-2026-2032年全球預測航太級冷原子鐘市場:按應用、最終用戶、產品類型、部署類型分類,全球預測(2026-2032) 全球手錶市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球手錶市場規模、佔有率、趨勢和成長分析報告(2026-2034) 手錶市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年全球手錶時鐘市場(按材料、部署方法、技術、應用和最終用戶):未來預測(2025-2030 年)

手錶市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年全球手錶時鐘市場(按材料、部署方法、技術、應用和最終用戶):未來預測(2025-2030 年)