|

市場調查報告書

商品編碼

2066730

電梯和電扶梯:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Elevator And Escalator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

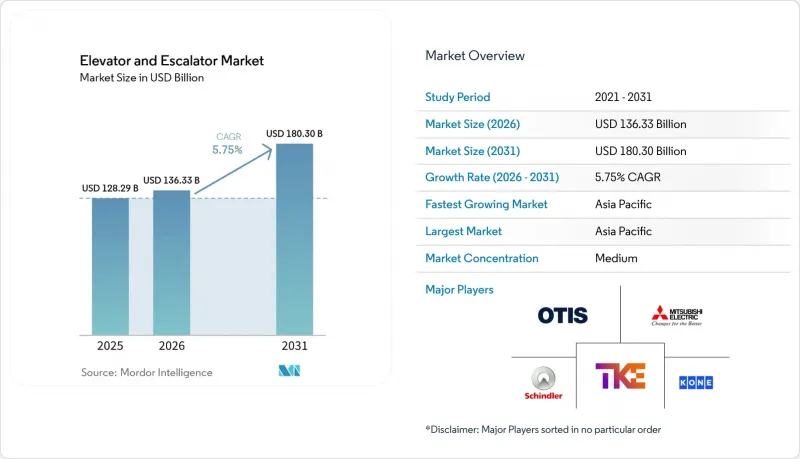

根據 Mordor Intelligence 預測,電梯和電扶梯市場規模將從 2025 年的 1,282.9 億美元成長到 2026 年的 1,363.3 億美元,到 2031 年將達到 1,803 億美元,2026 年至 2031 年的複合年成長率為 5.75%。

本報告按產品類型(電梯、電扶梯、電動平面步道)、技術(曳引式、液壓式、無機房式、真空/氣動式)、服務(新安裝、維修/維修、維修)、最終用戶(住宅、商業、基礎設施、工業)和地區(北美、歐洲、亞太、南美、中東和非洲)進行南美分類。

全球電梯及電扶梯市場趨勢及洞察

快速的都市化和高層建築的蓬勃發展

根據高層建築與居住環境委員會(CTBUH)的數據,預計到2025年將有141座超過200公尺高的建築竣工,儘管面臨宏觀經濟逆風,但2026年預計也將達到類似的數字。在中國,融資緊張抑制了新建工程,導致市場佔有率下降,但海灣合作理事會(GCC)的大型企劃在一定程度上彌補了這一缺口,推動了對電梯和電扶梯的穩定需求。光是在利雅德,到2030年就計劃新建34萬套住宅和480萬平方米的辦公空間,這使得未來的設備訂單似乎很有保障。在印度,2024年安裝了6萬套電梯和手扶梯,使其成為全球安裝量第二大的國家。這反映出印度全國正在從無序的郊區擴張轉向透過建造高層建築實現高密度開發。然而,全球有 259 個項目停滯不前,這削弱了整體預測,並凸顯了 OEM 短期獲利前景的不確定性。

需要現代化改造的破舊設施

根據奧的斯估計,到2024年,將有700萬部電梯使用運作超過20年,預計到2034年,這一數字將達到1500萬部,是目前的兩倍。在歐洲超過2.2億棟建築中,85%建於2001年之前,根據EN 81-80標準,這些建築存在74項安全缺陷,促使電梯進行現代化改造。通力(KONE)將其「MonoSpace 500」定位為「即插即用」的升級方案,與1990年代的機型相比,節能高達74%。在日本,超過30年的建築必須進行抗震加固,這進一步刺激了電梯的更換需求。現代化改造合約通常包含多年的維護服務,為原始設備製造商(OEM)提供了穩定的持續收入來源。

高初始資本投入

在印度,中層塔樓通常需要4到6部電梯,每部電梯的成本在4萬至8萬美元之間,但當開發商面臨資金短缺時,這筆費用往往會被推遲。在歐洲,更換整套電梯控制器的成本可能高達每台30萬美元,投資回收期長達20年。在南美洲,多邊融資瓶頸導致付款延遲,使得電梯採購被推遲到專案後期。基於績效的租賃模式將資本支出(CapEx)轉化為營運支出(OpEx),但這會加重原始設備製造商(OEM)的資產負債表負擔,使其成為小規模區域企業的障礙。

細分市場分析

到2025年,搭乘用電梯將佔電梯和電扶梯市場佔有率的64.1%。高層住宅和商業建築的興建推動了這一細分市場的發展,但電動平面步道預計將以7.4%的複合年成長率呈現最高成長,這主要得益於機場擴建,例如沙加緬度國際機場2026年的候機大廳維修。貨運電梯主要用於電商倉庫,而住宅電梯在無障礙維修中也越來越受歡迎。高速電梯目前仍屬於小眾市場,但佔有重要的戰略地位。通力(KONE)為吉達塔提供的10公尺/秒高速電梯就體現了高層建築的強勁需求。

電扶梯,尤其是平行排列的電扶梯,已成為購物中心和地鐵站的標準配備。傾斜式電動平面步道昂貴,因此除了在丘陵地區用於交通運輸外,用途有限。在高層建築中,高速電梯和空中大廳的普及率正在上升,預算也正從手扶梯轉向高速搭乘用。邁阿密國際機場等機場的電動平面步道(運作中)凸顯了基礎設施領域向水平交通運輸模式的轉變。

2025年,曳引式系統將佔據電梯和電扶梯市場70%的佔有率。預計無機房曳引式電梯的複合年成長率將達到7.8%,每個井道可節省10-15平方公尺的空間,並達到油壓式電梯無法企及的ISO 25745 A/B等級能源效率標準。通力(KONE)的「MonoSpace 500」將永磁馬達與能量回收驅動系統結合,可降低高達40%的年電力消耗量。

由於更嚴格的環保法規限制礦物油的使用,液壓電梯正在衰落。真空電梯因其極淺的井道深度而在住宅建築這一細分市場中備受青睞,但其載客量僅限於3-4人。像通力(KONE)的碳纖維「UltraRope」這樣的先進鋼絲繩可將鋼索重量減輕90%,使電梯運行高度超過500米,進一步增強了曳引式電梯在摩天大樓工程中的優勢。國際規範委員會(ICC)《建築標準法》的修訂允許使用井道內控制器,加速了多層曳引式電梯(MRL)在全球的普及。

區域分析

預計到2025年,亞太地區將佔全球電梯和電扶梯市場收入的62.8%,並預計到2031年將維持6.2%的年均成長率。在印度,二、三線城市目前佔全國電梯和電扶梯安裝量的一半;而在中國,現有設施現代化改造推動了新建需求的成長,抵消了因193個項目停工而導致的新建需求放緩。越南和印尼等東南亞國協正在吸引外商直接投資進入製造業,提振了對中層商業建築的需求。

在北美和歐洲,市場擴張主要由現代化驅動。在歐洲,EN 81-80 安全標準和能源法規支撐著穩定的更新週期;而在美國,加州第 24 號法規和紐約市第 97 號地方法律正在推動節能維修。中東和非洲地區是各地區中複合年成長率最高的,這得益於沙烏地阿拉伯「2030 願景」下的大規模開發以及阿拉伯聯合大公國旅遊基礎設施的建設。僅 NEOM 項目就計劃建造 382,500 套住宅和 300 萬平方米的辦公空間。南美洲的情況則是喜憂參半。在智利,地鐵擴建項目正在投資,而在巴西,一些項目由於貨幣波動而延期。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速的都市化和高層建築的蓬勃發展

- 需要現代化改造的老舊設施

- 更嚴格的安全標準正在加速更新換代進程。

- 綠色標籤產品的需求不斷成長

- 引入人工智慧驅動的預測性維護

- 對非接觸式和抗菌界面的需求

- 市場限制因素

- 高初始資本投入

- 原物料價格波動(鋼鐵、半導體)

- 半導體元件供不應求

- 二、三線城市合格技術人員短缺

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 電梯(搭乘用電梯、貨用電梯、住宅電梯、高速/高層電梯)

- 手扶梯(平行式、多平行式、交叉式)

- 電動平面步道(水平式和傾斜式)

- 透過技術

- 拖著

- 油壓

- 無機房(MRL)

- 真空/氣壓

- 按服務

- 新推出

- 維護/修理

- 現代化

- 最終用戶

- 住宅

- 商業設施(辦公室、零售商店/購物中心、飯店)

- 基礎建設(機場、地鐵、鐵路)

- 產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和市場佔有率)

- 公司簡介

- Otis Worldwide Corporation

- Kone Oyj

- Schindler Group

- TK Elevator(ThyssenKrupp)

- Mitsubishi Electric Corp.

- Hitachi Ltd.

- Fujitec Co. Ltd.

- Toshiba Elevator & Building Systems

- Hyundai Elevator Co. Ltd.

- Sigma Elevator(CJ Corporation)

- Canny Elevator Co. Ltd.

- Johnson Lifts Pvt Ltd.

- Orona S. Coop.

- Wittur Group

- Kleemann Hellas

- Stannah Lifts Holdings Ltd.

- Eita Elevator(M)Sdn Bhd

- Gulf Elevator & Escalator Co.

- Alpine Elevator Co.

- Savaria Corporation

- Hitachi-Yungtay Elevator(Taiwan)

第7章 市場機會與未來展望

According to Mordor Intelligence, the elevator and escalator market size is expected to increase from USD 128.29 billion in 2025 to USD 136.33 billion in 2026 and reach USD 180.30 billion by 2031, growing at a CAGR of 5.75% over 2026-2031.

This report is Segmented by Product Type (Elevators, Escalators, and Moving Walkways), Technology (Traction, Hydraulic, Machine-Room-Less, and Vacuum/Pneumatic), Service (New Installation, Maintenance and Repair, and Modernisation), End-User (Residential, Commercial, Infrastructure, and Industrial), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Elevator And Escalator Market Trends and Insights

Rapid Urbanization & High-Rise Construction Boom

The Council on Tall Buildings and Urban Habitat counted 141 buildings over 200 m completed in 2025 and anticipates a similar tally for 2026 despite macro headwinds. China's share is slipping as liquidity strains curb new starts, yet Gulf Cooperation Council mega-projects fill part of the gap, driving steady demand for the elevator & escalator market. Riyadh alone schedules 340,000 new homes and 4.8 million m2 of offices by 2030, locking in future equipment orders. India installed 60,000 units in 2024 and now ranks second worldwide by volume, reflecting a nationwide pivot from suburban sprawl to vertical densification. However, 259 global stalled projects temper headline forecasts, underscoring near-term revenue visibility issues for OEMs.

Ageing Installed Base Requiring Modernisation

Otis estimates 7 million elevators surpassed 20 years of service in 2024 and projects 15 million by 2034, twice today's pool. Europe's 220 million-plus buildings, 85% of which pre-date 2001, face 74 safety deficiencies under EN 81-80 that trigger modernization. KONE positions its MonoSpace 500 as a drop-in upgrade offering 74% energy savings over 1990s models. Japan's mandatory seismic retrofits for 30-year-old structures further spur replacements. Modernization contracts bundle multi-year service, cementing recurring revenue for OEMs.

High Upfront Capital Expenditure

Mid-rise towers in India need 4-6 elevators costing USD 40,000-80,000 each, a bill often deferred when developers face funding gaps. Full controller replacements in Europe cost up to USD 300,000 per unit, stretching 20-year amortization schedules. In South America, multilateral lending bottlenecks delay disbursements, pushing elevator procurement to later project phases. Performance-based leasing converts CapEx into OpEx but burdens OEM balance sheets, a hurdle for smaller regional players.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Safety Codes Accelerating Replacements

- AI-Driven Predictive Maintenance Adoption

- Volatile Raw-Material Prices (Steel, Chips)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger elevators captured 64.1% of the elevator & escalator market share in 2025. The segment benefits from residential high-rises and commercial towers, but moving walkways are forecast to post the fastest 7.4% CAGR, buoyed by airport expansions such as Sacramento International's 2026 concourse upgrades. Freight elevators serve e-commerce warehouses, while home elevators gain traction in accessibility retrofits. High-speed units remain niche but strategic: KONE's 10 m/s lifts for Jeddah Tower illustrate demand for ultra-tall applications.

Escalators, especially parallel layouts, dominate retail malls and metro stations. Inclined moving walkways see limited use outside hillside transits due to higher costs. Supertall buildings increasingly adopt express lifts and sky lobbies, reallocating budgets away from escalators toward high-speed passenger elevators. Moving walkways in airports like Miami International, which operates 96 units under a 2025 Otis contract, underscore the infrastructure segment's tilt toward horizontal conveyance.

Traction systems commanded 70% of the elevator & escalator market share in 2025. Machine-room-less traction units are projected to expand at a 7.8% CAGR, reclaiming 10-15 m2 per shaft and winning Class A/B ISO 25745 ratings that hydraulic rivals cannot match. KONE's MonoSpace 500 pairs permanent-magnet motors with regenerative drives, cutting annual electricity by up to 40%.

Hydraulic elevators retreat under tighter environmental rules that restrict mineral oils. Vacuum lifts occupy a residential niche, prized for minimal pit depth but limited to 3-4 passengers. Advanced ropes such as KONE's carbon-fiber UltraRope reduce cable weight 90%, enabling >500 m travel heights and reinforcing traction's dominance in supertall projects. Building-code updates from the ICC allow in-hoistway controllers, accelerating global MRL adoption.

Geography Analysis

Asia-Pacific produced 62.8% of 2025 revenue for the elevator & escalator market and is forecast to grow 6.2% through 2031. India's tier-2 and tier-3 cities now deliver half of domestic installations, while China's modernization opportunity offsets new-build slowdowns linked to 193 stalled projects. ASEAN nations such as Vietnam and Indonesia attract manufacturing FDI that boosts mid-rise commercial demand.

North America and Europe grow mainly via modernization. EN 81-80 safety mandates and energy codes underpin steady replacement cycles in Europe, while California's Title 24 and NYC's Local Law 97 drive efficiency-based retrofits in the United States. The Middle East & Africa posts the highest regional CAGR, propelled by Saudi Vision 2030 mega-developments and UAE tourism infrastructure; NEOM alone envisions 382,500 homes and 3 million m2 offices. South America is mixed: Chile invests in metro extensions, whereas Brazil's currency volatility delays some projects.

- Otis Worldwide Corporation

- Kone Oyj

- Schindler Group

- TK Elevator (ThyssenKrupp)

- Mitsubishi Electric Corp.

- Hitachi Ltd.

- Fujitec Co. Ltd.

- Toshiba Elevator & Building Systems

- Hyundai Elevator Co. Ltd.

- Sigma Elevator (CJ Corporation)

- Canny Elevator Co. Ltd.

- Johnson Lifts Pvt Ltd.

- Orona S. Coop.

- Wittur Group

- Kleemann Hellas

- Stannah Lifts Holdings Ltd.

- Eita Elevator (M) Sdn Bhd

- Gulf Elevator & Escalator Co.

- Alpine Elevator Co.

- Savaria Corporation

- Hitachi-Yungtay Elevator (Taiwan)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation & high-rise construction boom

- 4.2.2 Ageing installed base requiring modernisation

- 4.2.3 Stricter safety codes accelerating replacements

- 4.2.4 Escalating demand for green-labelled products

- 4.2.5 AI-driven predictive maintenance adoption

- 4.2.6 Touch-less & antimicrobial interface demand

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure

- 4.3.2 Volatile raw-material prices (steel, chips)

- 4.3.3 Semiconductor-grade component shortages

- 4.3.4 Scarcity of certified technicians in Tier-2/3 cities

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Elevators (Passenger Elevators, Freight Elevators, Home Elevators and High-speed/High-rise Elevators)

- 5.1.2 Escalators (Parallel, Multi-Parallel and Criss-Cross)

- 5.1.3 Moving Walkways (Horizontal and Inclined)

- 5.2 By Technology

- 5.2.1 Traction

- 5.2.2 Hydraulic

- 5.2.3 Machine-Room-Less (MRL)

- 5.2.4 Vacuum/Pneumatic

- 5.3 By Service

- 5.3.1 New Installation

- 5.3.2 Maintenance and Repair

- 5.3.3 Modernisation

- 5.4 By End-user

- 5.4.1 Residential

- 5.4.2 Commercial (Offices, Retail and Malls and Hospitality)

- 5.4.3 Infrastructure (Airports and Metro and Rail)

- 5.4.4 Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Otis Worldwide Corporation

- 6.4.2 Kone Oyj

- 6.4.3 Schindler Group

- 6.4.4 TK Elevator (ThyssenKrupp)

- 6.4.5 Mitsubishi Electric Corp.

- 6.4.6 Hitachi Ltd.

- 6.4.7 Fujitec Co. Ltd.

- 6.4.8 Toshiba Elevator & Building Systems

- 6.4.9 Hyundai Elevator Co. Ltd.

- 6.4.10 Sigma Elevator (CJ Corporation)

- 6.4.11 Canny Elevator Co. Ltd.

- 6.4.12 Johnson Lifts Pvt Ltd.

- 6.4.13 Orona S. Coop.

- 6.4.14 Wittur Group

- 6.4.15 Kleemann Hellas

- 6.4.16 Stannah Lifts Holdings Ltd.

- 6.4.17 Eita Elevator (M) Sdn Bhd

- 6.4.18 Gulf Elevator & Escalator Co.

- 6.4.19 Alpine Elevator Co.

- 6.4.20 Savaria Corporation

- 6.4.21 Hitachi-Yungtay Elevator (Taiwan)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

全球電梯和電扶梯市場:按類型、電梯技術、服務、最終用途產業和地區分類-預測至2031年

全球電梯和電扶梯市場:按類型、電梯技術、服務、最終用途產業和地區分類-預測至2031年 能力評估技術市場預測至2034年—按評估類型、部署模式、技術、應用、最終用戶和地區分類的全球分析

能力評估技術市場預測至2034年—按評估類型、部署模式、技術、應用、最終用戶和地區分類的全球分析 電梯和電扶梯市場:2026-2032年全球市場預測(按產品類型、安裝配置、最終用戶、技術、速度和應用分類)

電梯和電扶梯市場:2026-2032年全球市場預測(按產品類型、安裝配置、最終用戶、技術、速度和應用分類) 電梯和電扶梯市場規模、佔有率、趨勢和預測:按類型、服務、最終用途和地區分類,2026-2034年

電梯和電扶梯市場規模、佔有率、趨勢和預測:按類型、服務、最終用途和地區分類,2026-2034年 電梯和電扶梯市場:按產品和地區分類

電梯和電扶梯市場:按產品和地區分類 2026年全球太空電梯市場報告

2026年全球太空電梯市場報告 2026-2030年全球電梯及手扶梯市場2026年全球電梯和電扶梯市場報告

2026-2030年全球電梯及手扶梯市場2026年全球電梯和電扶梯市場報告 全球電梯和電扶梯市場:市場規模、佔有率、成長率、行業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034年)電梯和電扶梯市場-2025-2030年預測

全球電梯和電扶梯市場:市場規模、佔有率、成長率、行業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034年)電梯和電扶梯市場-2025-2030年預測