|

市場調查報告書

商品編碼

2066725

北美低壓感應電動機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Low Voltage Induction Motors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

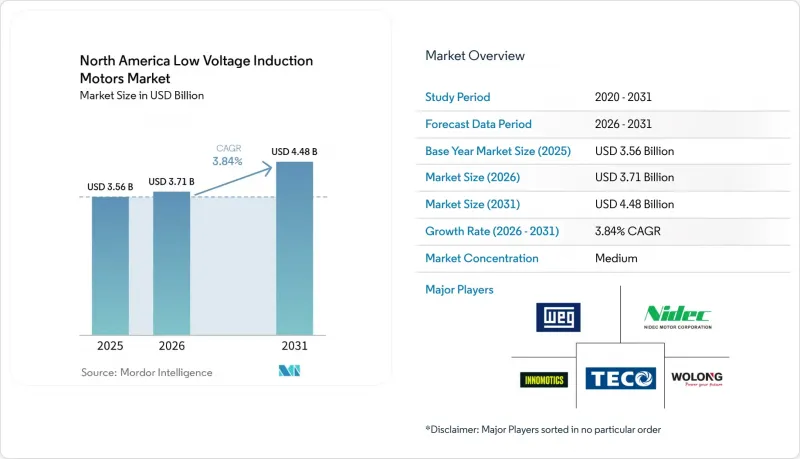

根據 Mordor Intelligence 預測,北美低壓感應電動機市場規模將從 2025 年的 35.6 億美元成長到 2026 年的 37.1 億美元,然後在 2031 年達到 44.8 億美元,2026 年至 2031 年的複合年成長率為 3.84%。

本報告按馬達類型(單相和多相)、應用領域(泵浦和風扇、壓縮機、輸送機和物料輸送、暖通空調和冷凍、其他)、能源效率等級(IE1/標準能源效率、其他)、終端用戶行業(石油和天然氣、用水和污水、食品和飲料、其他)以及國家/地區進行細分。市場預測以美元(USD)計價。

北美低壓感應電動機市場趨勢與洞察

美國能源局(DOE) 正在收緊應用範圍擴大的馬達的能源效率標準。

聯邦能源效率法規對北美低壓感應電動機市場的短期前景影響最大,超過了其他任何結構性因素。 2025年1月,美國能源局(DOE) 發布了針對額定功率為0.25至3馬力的單相和多相感應感應電動機的「擴展範圍馬達」最終規則,要求在2029年1月1日前達到合規標準。同時,針對100至250馬力的電機,則存在另一套監管路徑,迫使買家在2027年6月合規截止日期前過渡到IE4級設計。這正在加速工業設施的規劃和更換決策。能源部也表示,擴展範圍標準預計將顯著降低終端用戶的年度營運成本,進一步增強了企業儘早更換現有老舊馬達的經濟動力,而不是推遲升級。事實上,在北美低壓感應電動機市場,人們越來越關注經過認證的高效型號、合規時間以及供應商的準備情況,尤其是在採購團隊希望避免在最後一刻面臨供應瓶頸的情況下。

工業自動化和棕地維修的支出

北美低壓感應電動機市場正受到老舊工廠改造升級的推動。這是因為在老舊工廠中,馬達和驅動器通常無需重新設計周圍的電氣系統即可更換。維修專案擴大與預測性維護和數位化監控相結合,使工廠團隊能夠測量能源損耗,並根據更清晰的投資回收期來論證更換的合理性。 ABB 的 SP4 系列馬達以符合美國能源局(DOE) 標準的超高性能為核心定位,迎合了市場對符合標準的馬達日益成長的需求,這種需求不僅適用於新建工廠,也適用於升級改造項目。在連續運轉的泵浦、風扇和輸送機應用中,升級需求尤其旺盛,因為這些應用的能耗佔生命週期成本的很大一部分。這導致全部區域的馬達更換活動持續活躍,即使在待開發區投資波動的情況下,也促進了北美低壓感應電動機市場的穩定成長。

銅鋁價格波動

原物料價格波動仍是北美低壓感應電動機市場最主要的阻礙因素。銅和鋁的價格會影響製造商的利潤率、分銷商的定價以及終端用戶的更換週期,尤其是在專案對價格敏感且資金核准週期短的情況下。這在從IE2過渡到IE3或IE4的過程中尤其關鍵,因為高效設計本身初始成本就很高,在原物料價格波動的情況下,要證明其合理性就變得更加困難。因此,即使買家了解長期的節能效益,低價產品和高價產品之間的價格差距也不斷擴大。儘管北美低壓感應電動機市場持續成長,但在一些工廠,從簡單的替換採購轉向高效設計的計畫速度正在放緩。

細分市場分析

到2025年,多相馬達將佔據北美低壓感應電動機市場90.23%的佔有率,在區域銷售組成中顯著超越單相馬達。這一地位反映了多相馬達與三相電力系統的高度相容性、卓越的轉矩特性以及連續運轉下較低的維護需求。此外,預計到2031年,該細分市場將以4.43%的複合年成長率保持最高成長率,顯示這一成長不僅得益於現有優勢,也得益於向新規格過渡帶來的強勁勢頭。在食品加工、飲料製造和工業冷凍產業,可靠性和穩定運作與效率提升同等重要,因此工廠團隊繼續選擇多相IE3和IE4馬達作為新生產線的標準配置。因此,北美低壓感應電動機市場仍以工業應用為主,而非分散的小負載應用場景。

在需要連續運作的工業環境中,功率超過 5 馬力的多相馬達通常是更實用的選擇,因為該功率範圍內的單相電源會導致更高的轉換損耗、更複雜的結構以及更多的維護點。這些實際運作支撐了泵浦、輸送機、壓縮機以及整個工廠公用設施系統的穩定需求。同時,在三相電源不可用或安裝成本過高的輕型商業、農業和住宅泵浦應用中,單相馬達仍然非常有用。此外,美國能源局(DOE) 於 2025 年 1 月發布的關於「擴展功率範圍馬達」的最終規則,透過提高 0.25 至 3 匹馬力範圍內許多馬達的性能標準,正在改變低功率單相馬達產業。因此,儘管多相馬達在銷售方面仍然主導,但單相馬達的銷售越來越受到旨在符合法規的設計升級的驅動,而不是銷量的大幅成長。

到2025年,泵浦和風扇將佔北美低壓感應電動機市場35.78%的佔有率,成為該地區最大的應用領域。這一主導地位源自於其在眾多應用領域(包括水處理、石油和天然氣加工、暖通空調冷水機組迴路、冷卻系統和化工廠)的廣泛應用。由於許多系統無法承受長時間停機,如此龐大的裝機量催生了對定期更換的需求,而這些更換項目受資本支出突變的影響較小。此外,當設施需要提高可靠性、降低發熱量以及增強變頻驅動應用的性能時,升級到更高效率的型號也具有充分的理由。因此,即使其他應用領域呈現週期性波動,北美低壓感應電動機市場仍能持續吸引來自泵浦和風扇相關服務產業的穩定需求。

預計到2031年,壓縮機將以4.25%的複合年成長率保持最高成長率,這主要得益於低溫運輸(TEFC)變頻器相容型封閉式聯軸泵浦馬達產品線也表明,供應商在設計產品時已考慮到了與泵浦和壓縮機應用類似的高電力消耗量應用。隨著工廠自動化和物流的蓬勃發展,美國和墨西哥對電機密集輸送系統的需求持續成長,輸送機和物料輸送仍然是重要的應用領域。在37千瓦以下的暖通空調和冷凍領域,節能型(EC)馬達和永磁馬達技術正日益被用作替代方案,但在大型和高要求系統中,由於可維護性和重繞成本更為重要,感應電動機仍佔據著穩固的地位。儘管買家更容易受到供應鏈和價格壓力的影響,但通用工業機械和小規模應用的「長尾」市場仍然支撐著廣泛的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 美國能源部已收緊了應用範圍擴大的馬達的能源效率標準。

- 工業自動化與現有設施維修投資

- 用水和污水基礎設施維修

- 墨西哥的近岸外包和工廠本地化

- 擴展人工智慧資料中心的冷卻迴路

- 半導體和電池公用系統開發

- 市場限制因素

- 銅鋁價格波動

- 高效節能維修面臨的高昂初始成本障礙。

- 暖通空調產業中EC馬達和永磁馬達的更換

- 關稅導致零件採購不穩定

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 市場宏觀經濟趨勢的評估

第5章 市場規模與成長預測

- 依馬達類型

- 單相

- 多相

- 透過使用

- 水泵和風扇

- 壓縮機

- 輸送機和物料輸送

- 暖通空調和製冷

- 通用工業機械

- 其他用途

- 能源效率等級

- IE1/標準效率

- IE2 / 高效

- IE3 / 高效節能

- IE4 / 超高效

- 按最終用戶行業分類

- 石油和天然氣

- 水和污水處理

- 化工/石油化工

- 食品/飲料

- 離散製造

- 金屬和採礦

- 其他終端用戶產業

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- WEG SA

- Nidec Motor Corporation

- Innomotics GmbH

- TECO Electric & Machinery Co., Ltd.

- Wolong Electric Group Co., Ltd.

- Regal Rexnord Corporation

- Brook Crompton UK Ltd.

- VEM GmbH

- Hoyer Motors A/S

- Lafert SpA

- Cantoni Motor SA

- CG Power and Industrial Solutions Limited

- ABB Ltd.

- Bharat Bijlee Limited

- Bonfiglioli Riduttori SpA

- SEW-EURODRIVE GmbH & Co KG

- Getriebebau NORD GmbH & Co. KG

- Neri Motori Srl

- OME Motors Srl

- TT Electric Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america low voltage induction motors market size is expected to grow from USD 3.56 billion in 2025 to USD 3.71 billion in 2026 and is forecast to reach USD 4.48 billion by 2031 at 3.84% CAGR over 2026-2031.

This report is Segmented by Motor Type (Single Phase, and Poly Phase), Application (Pumps and Fans, Compressors, Conveyors and Material Handling, HVAC and Refrigeration, and More), Efficiency Class (IE1/Standard Efficiency, and More), End-User Industry (Oil and Gas, Water and Wastewater, Food and Beverage, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Low Voltage Induction Motors Market Trends and Insights

Tightening DOE Efficiency Standards for Expanded-Scope Motors

Federal efficiency regulation is shaping the near-term outlook of the North America low voltage induction motors market more than any other structural driver. The U.S. Department of Energy published a final rule in January 2025 for expanded-scope electric motors that covers single-phase and poly phase induction motors rated 0.25 to 3 horsepower, with compliance required by January 1, 2029. A separate rule path for 100-250 horsepower motors is pushing buyers toward IE4-class designs ahead of the June 2027 compliance date, which is pulling forward planning and replacement decisions across industrial sites. DOE also said the expanded-scope standards would generate material annual operating cost savings for end users, which strengthens the financial case for replacing older installed motors instead of delaying upgrades. The practical effect is that the North America low voltage induction motors market is seeing more attention on certified premium-efficiency models, compliance timing, and supplier readiness, especially where procurement teams do not want to face bottlenecks closer to the deadline.

Industrial Automation and Brownfield Retrofit Spending

Brownfield modernization is supporting the North America low voltage induction motors market because older plants can often replace motors and drives without redesigning the surrounding electrical system. Retrofit projects are increasingly tied to predictive maintenance and digital monitoring, which helps plant teams measure energy losses and justify changeouts on a clearer payback basis. ABB has positioned its SP4 line around DOE-ready super-premium performance, and that aligns with the growing preference for compliant motors in upgrade cycles rather than only in new facilities. The upgrade case is especially strong in continuous-duty pump, fan, and conveyor services where electricity use dominates lifecycle cost. This is keeping replacement activity active across manufacturing corridors in the United States and helping the North America low voltage induction motors market hold steady growth even when greenfield spending is uneven.

Copper and Aluminum Cost Volatility

Raw material volatility remains the clearest cost-side restraint for the North America low voltage induction motors market. Copper and aluminum costs affect manufacturer margins, distributor pricing, and end-user replacement timing, especially when projects are price-sensitive and capital approval windows are narrow. This matters most in the move from IE2 to IE3 or IE4, because higher-efficiency designs already carry a higher upfront cost and become harder to justify when input prices are unstable. The result is a wider price gap between lower-tier and premium-tier products, even when buyers understand the energy savings case over time. That keeps the North America low voltage induction motors market growing, but it slows the speed at which some facilities move from basic replacement buying to planned premium-efficiency upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Water and Wastewater Infrastructure Upgrades

- Mexico Nearshoring and Plant Localization

- Higher First-Cost Barrier for Premium-Efficiency Retrofits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Poly phase motors held 90.23% of the North America low voltage induction motors market share in 2025, which kept them far ahead of single phase designs in the regional revenue mix. Their position reflects strong compatibility with three-phase power systems, better torque characteristics, and lower maintenance demands in continuous-duty operations. The segment is also forecast to post the fastest 4.43% CAGR through 2031, which shows that growth is not only coming from base dominance but also from new specification momentum. In food processing, beverage production, and industrial refrigeration, plant teams continue to make poly phase IE3 and IE4 motors the default choice for new lines because reliability and stable operation matter as much as efficiency gains. This keeps the North America low voltage induction motors market centered on industrial duty cycles rather than on fragmented small-load use cases.

Poly phase units above 5 horsepower are often the practical choice in continuous-duty industrial settings because single phase supply in that range adds conversion losses, more complexity, and extra maintenance points. That operating reality supports steady demand across pumps, conveyors, compressors, and plant utility systems. Single phase motors still serve light commercial, agricultural, and residential pump applications where three-phase power is unavailable or too costly to install. DOE's January 2025 final rule for expanded-scope motors is also reshaping the lower-horsepower single phase segment by raising the performance threshold for many designs in the 0.25-3 horsepower range. The result is that volume leadership remains with poly phase motors, while single phase revenue is being influenced more by compliance-driven design upgrades than by broad unit growth.

Pumps and fans accounted for 35.78% of the North America low voltage induction motors market size in 2025, making them the largest application group in the region. Their lead comes from the depth of installed motors across water treatment, oil and gas processing, HVAC chiller loops, cooling systems, and chemical plants. This installed base creates repeat replacement demand that is less exposed to abrupt changes in capital spending because many systems cannot tolerate long outages. It also supports the case for premium-efficiency upgrades when facilities need better reliability, lower heat generation, and stronger inverter-duty performance. The North America low voltage induction motors market, therefore, continues to draw stable demand from pump and fan services even when other applications move in cycles.

Compressors are projected to grow at the fastest 4.25% CAGR through 2031, supported by rising use in cold-chain systems, natural gas handling, and liquid cooling systems tied to AI-linked data center buildouts. Nidec's November 2025 launch of its TEFC Inverter Duty Closed Coupled Pump motor line also shows how suppliers are designing around variable-speed, utility-heavy applications that sit close to both pumping and compression duties. Conveyors and material handling remain important because factory automation and distribution growth continue to add motor-intensive movement systems across the United States and Mexico. HVAC and refrigeration below 37 kW face some substitution from EC and permanent-magnet technologies, but induction motors remain well placed in larger-frame and harsher-duty systems where serviceability and rewind economics matter more. General industrial machinery and the long tail of smaller applications continue to provide a broad demand floor, even if those buyers are more exposed to supply chain and pricing pressure.

List of Companies Covered in this Report:

- WEG S.A.

- Nidec Motor Corporation

- Innomotics GmbH

- TECO Electric & Machinery Co., Ltd.

- Wolong Electric Group Co., Ltd.

- Regal Rexnord Corporation

- Brook Crompton UK Ltd.

- VEM GmbH

- Hoyer Motors A/S

- Lafert S.p.A.

- Cantoni Motor S.A.

- CG Power and Industrial Solutions Limited

- ABB Ltd.

- Bharat Bijlee Limited

- Bonfiglioli Riduttori S.p.A.

- SEW-EURODRIVE GmbH & Co KG

- Getriebebau NORD GmbH & Co. KG

- Neri Motori S.r.l.

- OME Motors S.r.l.

- T-T Electric Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening DOE Efficiency Standards for Expanded-Scope Motors

- 4.2.2 Industrial Automation and Brownfield Retrofit Spending

- 4.2.3 Water and Wastewater Infrastructure Upgrades

- 4.2.4 Mexico Nearshoring and Plant Localization

- 4.2.5 AI Data Center Cooling Loop Expansion

- 4.2.6 Semiconductor and Battery Utility System Build-Out

- 4.3 Market Restraints

- 4.3.1 Copper and Aluminum Cost Volatility

- 4.3.2 Higher First-Cost Barrier for Premium-Efficiency Retrofits

- 4.3.3 EC and Permanent-Magnet Motor Substitution in HVAC

- 4.3.4 Tariff-Driven Component Sourcing Instability

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Single Phase

- 5.1.2 Poly Phase

- 5.2 By Application

- 5.2.1 Pumps and Fans

- 5.2.2 Compressors

- 5.2.3 Conveyors and Material Handling

- 5.2.4 HVAC and Refrigeration

- 5.2.5 General Industrial Machinery

- 5.2.6 Other Applications

- 5.3 By Efficiency Class

- 5.3.1 IE1/Standard Efficiency

- 5.3.2 IE2/High Efficiency

- 5.3.3 IE3/Premium Efficiency

- 5.3.4 IE4/Super-Premium Efficiency

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Water and Wastewater

- 5.4.3 Chemicals and Petrochemicals

- 5.4.4 Food and Beverage

- 5.4.5 Discrete Manufacturing

- 5.4.6 Metal and Mining

- 5.4.7 Other End-User Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 WEG S.A.

- 6.4.2 Nidec Motor Corporation

- 6.4.3 Innomotics GmbH

- 6.4.4 TECO Electric & Machinery Co., Ltd.

- 6.4.5 Wolong Electric Group Co., Ltd.

- 6.4.6 Regal Rexnord Corporation

- 6.4.7 Brook Crompton UK Ltd.

- 6.4.8 VEM GmbH

- 6.4.9 Hoyer Motors A/S

- 6.4.10 Lafert S.p.A.

- 6.4.11 Cantoni Motor S.A.

- 6.4.12 CG Power and Industrial Solutions Limited

- 6.4.13 ABB Ltd.

- 6.4.14 Bharat Bijlee Limited

- 6.4.15 Bonfiglioli Riduttori S.p.A.

- 6.4.16 SEW-EURODRIVE GmbH & Co KG

- 6.4.17 Getriebebau NORD GmbH & Co. KG

- 6.4.18 Neri Motori S.r.l.

- 6.4.19 OME Motors S.r.l.

- 6.4.20 T-T Electric Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球感應電動機市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球感應電動機市場規模、佔有率、趨勢和成長分析報告(2026-2034) 感應馬達市場:2026-2032年全球市場預測(按類型、安裝方式、能源效率等級、功率輸出、應用、終端用戶產業和銷售管道)

感應馬達市場:2026-2032年全球市場預測(按類型、安裝方式、能源效率等級、功率輸出、應用、終端用戶產業和銷售管道) 2026-2034年感應電動機市場規模、佔有率、趨勢及預測(依產品類型、最終用途產業及地區分類)以相數、機殼、電壓、額定功率、轉速、安裝方式和應用分類的鼠籠式感應電動機市場-2026-2032年全球預測

2026-2034年感應電動機市場規模、佔有率、趨勢及預測(依產品類型、最終用途產業及地區分類)以相數、機殼、電壓、額定功率、轉速、安裝方式和應用分類的鼠籠式感應電動機市場-2026-2032年全球預測 感應電動機市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

感應電動機市場機會、成長要素、產業趨勢分析及預測(2026年至2035年) 感應馬達市場-全球產業規模、佔有率、趨勢、機會及預測(細分、按類型、按應用、按地區、按競爭,2020-2030 年預測)

感應馬達市場-全球產業規模、佔有率、趨勢、機會及預測(細分、按類型、按應用、按地區、按競爭,2020-2030 年預測) 亞太地區感應電動機:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)北美感應馬達:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)感應馬達:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲感應電動機:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

亞太地區感應電動機:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)北美感應馬達:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)感應馬達:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲感應電動機:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)