|

市場調查報告書

商品編碼

2066722

北美家庭能源管理系統(HEMS):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)North America Home Energy Management System (HEMS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

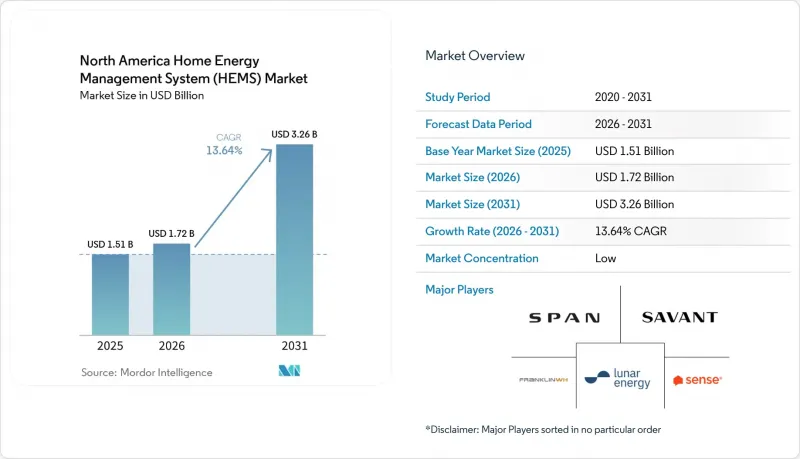

根據 Mordor Intelligence 預測,北美家庭能源管理系統 (HEMS) 市場規模將從 2025 年的 15.1 億美元成長到 2026 年的 17.2 億美元,然後在 2031 年達到 32.6 億美元,2026 年至 2031 年的複合成長率為 13.64%。

本報告按組件(硬體(智慧電錶、智慧恆溫器、能源儲存系統等)、軟體、服務)、通訊技術(ZigBee、Wi-Fi、Z-Wave 等)、最終用戶(住宅、商業)、部署模式(雲端託管平台、本地/內部閘道)和國家/地區進行細分。市場預測以美元計價。

北美家庭能源管理系統(HEMS)市場趨勢與洞察

智慧電錶和支援即時控制的高級計量基礎設施(AMI)的普及

隨著智慧電錶的普及,家庭能源管理正從單純的用電量視覺化轉向即時設備控制。這在北美家庭能源管理系統 (HEMS) 市場至關重要,因為高級計量基礎設施 (AMI) 數據為平台提供持續的家庭用電量訊號,從而實現自動調度、負載調節和對費率方案的快速響應。隨著公用事業公司從以計費為中心的基礎設施轉向電網邊緣智慧,能夠解讀電錶資料並將其轉化為家電級決策的軟體價值也在不斷提升。這種轉變降低了進入門檻,因為一些家庭無需在家中安裝全新的感測器設備即可獲得更深入的能源資訊。北美家庭能源管理系統市場正受益於進入門檻的降低,因為它擴大了平台供應商和公用事業公司主導專案的目標基本客群。這也強化了公用事業公司、軟體開發商和設備供應商之間夥伴關係的重要性,這種合作可以將現有的電網基礎設施轉化為實用的家庭編配平台。

太陽能發電+儲能和家庭電氣化的普及

太陽能和儲能系統的普及是北美家庭能源管理系統市場最顯著的需求支柱之一。這是因為擁有多種能源資產的家庭需要主動調節,而非被動監控。預計到2025年,美國住宅儲能市場將年增51%,自2019年以來累計裝置容量將超過50吉瓦,累計儲能容量將超過144吉瓦時。這顯著擴大了可與家庭能源控制軟體整合的部署基礎。報告顯示,預計2026年至2031年間,美國將新增500吉瓦時的儲能系統,這將在整個預測期內持續為家庭能源平台創造新的整合點。從實際角度來看,隨著每套新電池系統的安裝,能夠根據一天中的不同時段最佳化家庭充電、備用電源優先級、自用電量和負載轉移的軟體的價值也將隨之提升。正因如此,北美家庭能源管理系統(HEMS)市場正朝著「全端式編配」的方向發展,也就是把溫控器、智慧面板、儲能系統和連接的負載整合到一個統一協調的能源系統中。隨著家用電器的普及和住宅維修的加快,更多靈活的負載被引入家庭,使得電力流動變得更加複雜,這種需求也隨之成長。

較高的初始系統和安裝成本

高昂的初始系統成本仍是北美家庭能源管理系統市場普及的最大障礙。一套完整的住宅系統,包括智慧面板、電池、溫控器、軟體和電動車充電設備,在享受補貼前的價格可能在 15,000 美元到 35,000 美元之間,這導致許多中等收入家庭推遲採用。安裝成本也是高價的原因之一,因為電路級控制和線路改造通常需要經過訓練的電工和特定平台的試運行。在多用戶住宅、補貼計畫進展緩慢的市場或公用事業公司支持有限的市場,這個成本問題更為嚴重。這也影響了產品組合,因為單一家庭最初可能只選擇配備溫控器或太陽能的系統,而將其他能源相關設備的安裝推遲到資金籌措和補貼條件改善之後。在以服務為基礎的資金籌措和低成本安裝模式得到更廣泛的應用之前,北美家庭能源管理系統市場從消費者興趣到實際安裝的轉變過程可能仍將緩慢。

細分市場分析

到2025年,硬體將佔北美家庭能源管理系統市場佔有率的64.56%,反映出實體設備在系統總支出中仍扮演著重要角色。智慧溫控器仍然是最常見的入門級產品,因為它們為節能提供了清晰的路徑,並且可以連接到更全面的家庭控制系統。北美家庭能源管理系統市場也持續依賴智慧配電盤、能源儲存系統、智慧插座和室內顯示器來建構協調能源管理所需的實體控制和感測層。 2025年美國住宅電費的上漲進一步加劇了對硬體主導的需求控制的需求,尤其是對於那些希望更主動管理電力尖峰時段的家庭而言。 2025年2月,SPAN推出了“SPAN Panel MAIN 40+MID”和“SPAN Panel MLO 48”,進一步鞏固了其硬體優勢,這兩款產品將斷路器容量增加了25%至50%。同時,該公司強調該產品能夠避免全電住宅升級到 400 安培服務所帶來的成本。

在北美家庭能源管理系統 (HEMS) 市場中,軟體是成長最快的細分市場,預計從 2026 年到 2031 年將以 14.89% 的複合年成長率成長。這一成長反映了市場正從一次性設備銷售轉向人工智慧驅動的負載預測、費率方案最佳化、電池控制邏輯和週期性平台使用費。北美家庭能源管理系統軟體市場規模的成長主要得益於住宅儲能系統安裝數量的增加。這導致需要發電、儲能和靈活的即時負載調節的住宅數量不斷增加。 Enphase 於 2026 年 2 月推出了適用於基於 IQ9 和 IQ8 微型逆變器的小規模商用系統的 Power Control 軟體,進一步強化了這一趨勢,展示了軟體如何在現有硬體基礎設施的基礎上提升經濟效益。隨著已部署資產基礎的複雜性增加,服務細分市場也在不斷擴大,這需要專家支援多供應商整合、試運行、監控以及參與公用事業專案的管理。

預計到2025年,Wi-Fi將佔北美家庭能源管理系統市場銷售額的38.76%,並因其能與現有家庭寬頻網路無縫整合,仍將是該市場最大的通訊層。 Wi-Fi支援雲端連線儀錶板、遠端設定、軟體更新和高頻寬資料交換,且大多數家庭無需單獨的通訊骨幹網路。 ZigBee在公用事業營運和計量環境中繼續發揮至關重要的作用,其低功耗網狀通訊仍然非常適合大規模分散式設備部署。藍牙在短距離設定和控制方面仍然非常有用,尤其是在簡單的插座級和行動裝置配置中。 HomePlug在一些特定的維修案例中仍然得到應用,例如老住宅由於線路狀況或建材原因導致無線連接不穩定時。

Z-Wave 是成長最快的通訊協定,預計從 2026 年到 2031 年的複合年成長率將達到 14.21%,尤其在電池供電的多感測器環境中表現出色。連結標準聯盟 (CSA) 於 2025 年 11 月發布了 Matter 1.5 版本。此次更新新增了「電費」設備類型,並增強了對跨協議更一致地共用價格和能源數據的支援。這對北美家庭能源管理系統市場意義重大,因為互通性降低了單一家庭被迫選擇單一封閉式通訊協定堆疊的風險。它還支援一種實用的共存模式:Wi-Fi 負責高頻寬的雲端處理,而 Z-Wave 則支援邊緣的低功耗感測和控制。於 2026 年 3 月發布的 Matter 1.5.1 版本進一步改進了跨平台設備的操作,並加強了對更流暢的多設備相容性的追求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧電錶和支援即時控制的高級計量基礎設施(AMI)的普及

- 電力公司擴大分時電價和動態電價的實施

- 太陽能發電+儲能系統和家庭電氣化的普及。

- 從保險和韌性角度來看,備用能源編配的需求日益成長。

- 透過將 HEMS 與與 IRA 掛鉤的住宅範圍內的退款相結合,縮短其投資回收期。

- 透過 Matter 1.5 和公用事業訊號標準化來降低整合障礙。

- 市場限制因素

- 系統和安裝的初始成本較高。

- 網路安全與家庭資料隱私問題

- 為多供應商住宅能源資產試運行安裝人員的複雜性。

- 價格和方案的波動正在削弱消費者對投資報酬率的信心。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 市場宏觀經濟趨勢的評估

第5章 市場規模與成長預測

- 按組件

- 硬體

- 智慧電錶

- 智慧型恆溫器

- 能源儲存系統

- 智慧插頭和智慧插座

- 家庭顯示器 (IHD)

- 其他硬體

- 軟體

- 服務

- 硬體

- 透過通訊技術

- Zigbee

- Wi-Fi

- Z-Wave

- Bluetooth

- HomePlug

- 其他通訊技術

- 最終用戶

- 住宅

- 獨立式住宅

- 多用戶住宅

- 商業

- 小規模辦公室/家庭辦公室

- 零售和酒店

- 住宅

- 部署模式

- 雲端託管平台

- 本地/本地閘道器

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SPAN.io, Inc.

- Savant Systems, Inc.

- FranklinWH Energy Storage Inc.

- Lunar Energy, Inc.

- Sense Labs, Inc.

- Emporia Corp

- Lumin Systems, Inc.

- ecobee Inc.

- sonnen GmbH

- Resideo Technologies, Inc.

- Itron, Inc.

- Generac Holdings, Inc.

- ChargePoint Holdings, Inc.

- Sigenergy Technology Co., Ltd.

- EcoFlow Technology Inc.

- Anker Innovations Technology Co., Ltd.

- Enphase Energy, Inc.

- SolarEdge Technologies, Inc.

- AutoGrid, Inc.

- OhmConnect, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america home energy management system (HEMS) market size is expected to grow from USD 1.51 billion in 2025 to USD 1.72 billion in 2026 and is forecast to reach USD 3.26 billion by 2031 at 13.64% CAGR over 2026-2031.

This report is Segmented by Component (Hardware (Smart Meters, Smart Thermostats, Energy Storage Systems, and More), Software, Services), Communication Technology (ZigBee, Wi-Fi, Z-Wave, and More), End-User (Residential, Commercial), Deployment Mode (Cloud-Hosted Platforms, On-Premises / Local Gateway), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Home Energy Management System (HEMS) Market Trends and Insights

Smart Meter and AMI Saturation Supporting Real-Time Control

Smart meter saturation is pushing household energy management away from simple usage visibility and toward real-time device control. In the North America home energy management system (HEMS) market, this matters because AMI data gives platforms a constant stream of household consumption signals that can support automated scheduling, load disaggregation, and tariff response. As utilities move from billing-focused infrastructure to grid-edge intelligence, the value of software that can interpret meter data and translate it into appliance-level decisions rises with it. This shift also lowers the friction of adoption because some households can receive better energy insight without adding a full set of new sensing hardware inside the home. The North America home energy management system market benefits from that lower entry barrier because it expands the addressable base for platform vendors and utility-led programs. It also strengthens the case for partnerships between utilities, software developers, and device providers that can turn existing grid infrastructure into a practical household orchestration layer.

Solar-Plus-Storage and Home Electrification Adoption

Solar-plus-storage adoption is one of the clearest demand anchors for the North America home energy management system market because households with multiple energy assets need active coordination rather than passive monitoring. The US residential storage segment grew 51% year over year in 2025, and cumulative deployments since 2019 exceeded 50GW and 144GWh, which materially expanded the installed base that can be paired with household energy control software. The same report indicates the United States is expected to deploy 500GWh of storage from 2026 to 2031, which keeps creating new integration points for home energy platforms over the forecast period. In practical terms, each new battery system raises the value of software that can optimize charging, backup priority, self-consumption, and time-based load shifting inside the home. This is why the North America home energy management system (HEMS) market is moving closer to full-stack orchestration, where thermostats, smart panels, storage systems, and connected loads operate as one coordinated energy system. The adoption of electric appliances and home electrification upgrades further deepens this need because household power flows become more complex as more flexible loads enter the home.

High Upfront System and Installation Costs

High upfront system cost remains the clearest barrier to mass adoption in the North America home energy management system market. A fully integrated residential setup that includes a smart panel, battery storage, thermostat, software, and EV charging can require USD 15,000 to USD 35,000 before rebates, which keeps many middle-income households on the sidelines. Installation also adds cost because circuit-level control and electrical reconfiguration often require trained electricians and platform-specific commissioning. This cost issue is more severe in multi-family settings and in markets where rebate rollout is slower or utility support is limited. It also affects product mix because households may choose a thermostat or a solar-only setup first, then delay the rest of the energy stack until financing or rebates improve. Until service-based financing and lower-cost deployment models scale more broadly, the North America HEMS market will continue to face slower conversion from consumer interest to completed installations.

Other drivers and restraints analyzed in the detailed report include:

- Utility Time-Of-Use and Dynamic Pricing Expansion

- IRA-Linked Whole-Home Rebate Stacking Improving HEMS Payback

- Cybersecurity and Household Data Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware held 64.56% of the North America home energy management system market share in 2025, which reflects the still heavy role of physical equipment in total system spending. Smart thermostats remain the most common first step because they offer a visible path to energy savings and can connect later to a broader household control stack. The North America home energy management system market also continues to rely on smart electrical panels, energy storage systems, smart plugs, and in-home displays to create the physical control and sensing layer required for coordinated energy management. Rising US residential electricity prices in 2025 reinforced the need for hardware-led demand control, especially for households looking to manage peak usage more actively. SPAN strengthened that hardware case in February 2025 when it launched the SPAN Panel MAIN 40+MID and SPAN Panel MLO 48 with 25-50% more breaker spaces, while also positioning the products around avoiding 400-ampere service upgrade costs in all-electric homes.

Software is the fastest-growing component in the North America home energy management system (HEMS) market, with a 14.89% CAGR expected from 2026 to 2031. That expansion reflects the move toward AI-based load forecasting, tariff optimization, battery dispatch logic, and recurring platform subscriptions rather than one-time device revenue. The North America home energy management system market size for software is gaining support from the rising installed base of residential storage, which creates a larger pool of homes that need real-time orchestration across generation, storage, and flexible loads. Enphase reinforced this direction in February 2026 when it introduced Power Control software for IQ9 and IQ8 microinverter-based small commercial systems, showing how software can improve economics on top of an existing hardware base. Services are also expanding because multi-vendor integration, commissioning, monitoring, and managed participation in utility programs require specialized support as the installed asset base becomes more complex.

Wi-Fi accounted for 38.76% of revenue in 2025 and remained the largest communication layer in the North America home energy management system market because it fits naturally into existing home broadband networks. It supports cloud-connected dashboards, remote configuration, software updates, and high-bandwidth data exchange without requiring a separate communication backbone in most homes. ZigBee continues to matter in utility-linked and meter-adjacent environments because low-power mesh communication still suits large distributed device deployments. Bluetooth maintains relevance for short-range setup and control, especially in simpler outlet-level or portable device configurations. HomePlug still serves certain retrofit cases where wiring conditions or building materials reduce the reliability of wireless links inside older homes.

Z-Wave is the fastest-growing communication protocol, with a 14.21% CAGR projected for 2026 to 2031, and it benefits from strong performance in battery-powered, multi-sensor environments. The Connectivity Standards Alliance released Matter 1.5 in November 2025, and the update added an Electrical Energy Tariff device type along with broader support that helps devices share pricing and energy data more consistently across protocols. That matters for the North America home energy management system market because interoperability reduces the risk that any one household must choose a single closed communication stack. It also allows a practical coexistence model where Wi-Fi handles high-bandwidth cloud tasks while Z-Wave supports low-power sensing and control at the edge. Matter 1.5.1, released in March 2026, further improved cross-platform device behavior and reinforced the push toward smoother multi-device compatibility.

List of Companies Covered in this Report:

- SPAN.io, Inc.

- Savant Systems, Inc.

- FranklinWH Energy Storage Inc.

- Lunar Energy, Inc.

- Sense Labs, Inc.

- Emporia Corp

- Lumin Systems, Inc.

- ecobee Inc.

- sonnen GmbH

- Resideo Technologies, Inc.

- Itron, Inc.

- Generac Holdings, Inc.

- ChargePoint Holdings, Inc.

- Sigenergy Technology Co., Ltd.

- EcoFlow Technology Inc.

- Anker Innovations Technology Co., Ltd.

- Enphase Energy, Inc.

- SolarEdge Technologies, Inc.

- AutoGrid, Inc.

- OhmConnect, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smart Meter and AMI Saturation Supporting Real-Time Control

- 4.2.2 Utility Time-of-Use and Dynamic Pricing Expansion

- 4.2.3 Solar-Plus-Storage and Home Electrification Adoption

- 4.2.4 Insurance and Resiliency Demand for Backup-Oriented Energy Orchestration

- 4.2.5 IRA-Linked Whole-Home Rebate Stacking Improving HEMS Payback

- 4.2.6 Matter 1.5 and Utility Signal Standardization Lowering Integration Friction

- 4.3 Market Restraints

- 4.3.1 High Upfront System and Installation Costs

- 4.3.2 Cybersecurity and Household Data Privacy Concerns

- 4.3.3 Installer Commissioning Complexity Across Multi-Vendor Home Energy Assets

- 4.3.4 Tariff and Program Volatility Weakening Consumer ROI Confidence

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Smart Meters

- 5.1.1.2 Smart Thermostats

- 5.1.1.3 Energy Storage Systems

- 5.1.1.4 Smart Plugs and Outlets

- 5.1.1.5 In-Home Displays (IHDs)

- 5.1.1.6 Other Hardwares

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Communication Technology

- 5.2.1 ZigBee

- 5.2.2 Wi-Fi

- 5.2.3 Z-Wave

- 5.2.4 Bluetooth

- 5.2.5 HomePlug

- 5.2.6 Other Communication Technologies

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.1.1 Single-Family Homes

- 5.3.1.2 Multi-Family Housing

- 5.3.2 Commercial

- 5.3.2.1 Small Office / Home Office

- 5.3.2.2 Retail and Hospitality

- 5.3.1 Residential

- 5.4 By Deployment Mode

- 5.4.1 Cloud-Hosted Platforms

- 5.4.2 On-Premises / Local Gateway

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SPAN.io, Inc.

- 6.4.2 Savant Systems, Inc.

- 6.4.3 FranklinWH Energy Storage Inc.

- 6.4.4 Lunar Energy, Inc.

- 6.4.5 Sense Labs, Inc.

- 6.4.6 Emporia Corp

- 6.4.7 Lumin Systems, Inc.

- 6.4.8 ecobee Inc.

- 6.4.9 sonnen GmbH

- 6.4.10 Resideo Technologies, Inc.

- 6.4.11 Itron, Inc.

- 6.4.12 Generac Holdings, Inc.

- 6.4.13 ChargePoint Holdings, Inc.

- 6.4.14 Sigenergy Technology Co., Ltd.

- 6.4.15 EcoFlow Technology Inc.

- 6.4.16 Anker Innovations Technology Co., Ltd.

- 6.4.17 Enphase Energy, Inc.

- 6.4.18 SolarEdge Technologies, Inc.

- 6.4.19 AutoGrid, Inc.

- 6.4.20 OhmConnect, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

建築併網技術市場:依技術、組件、應用、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測

建築併網技術市場:依技術、組件、應用、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測 智慧恆溫器系統市場預測至2034年-按產品、組件、通路、技術、應用、最終用戶和地區分類的全球分析

智慧恆溫器系統市場預測至2034年-按產品、組件、通路、技術、應用、最終用戶和地區分類的全球分析 建築能源管理系統市場:按組件、系統、建築類型、部署模式、最終用途和最終用戶分類-2026-2032年全球市場預測

建築能源管理系統市場:按組件、系統、建築類型、部署模式、最終用途和最終用戶分類-2026-2032年全球市場預測 2026年全球建築併網技術市場報告2034 年前全球建築併網技術的市場機會與策略

2026年全球建築併網技術市場報告2034 年前全球建築併網技術的市場機會與策略 下一代建築能源管理系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、通訊技術、地區和競爭格局分類,2021-2031年建築能源管理解決方案市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、組件、應用、地區和競爭格局分類,2021-2031年預測)建築能源管理系統市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、組件、部署方式、地區和競爭格局分類,2020-2030年預測建築到電網技術市場-全球產業規模、佔有率、趨勢、機會和預測,按技術、組件、建築類型、應用、地區和競爭進行細分,2020-2030 年預測

下一代建築能源管理系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、通訊技術、地區和競爭格局分類,2021-2031年建築能源管理解決方案市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、組件、應用、地區和競爭格局分類,2021-2031年預測)建築能源管理系統市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、組件、部署方式、地區和競爭格局分類,2020-2030年預測建築到電網技術市場-全球產業規模、佔有率、趨勢、機會和預測,按技術、組件、建築類型、應用、地區和競爭進行細分,2020-2030 年預測 建築能源管理系統市場:2025-2030 年預測

建築能源管理系統市場:2025-2030 年預測