|

市場調查報告書

商品編碼

2066703

中國風力發電機葉輪:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)China Wind Turbine Rotor Blade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

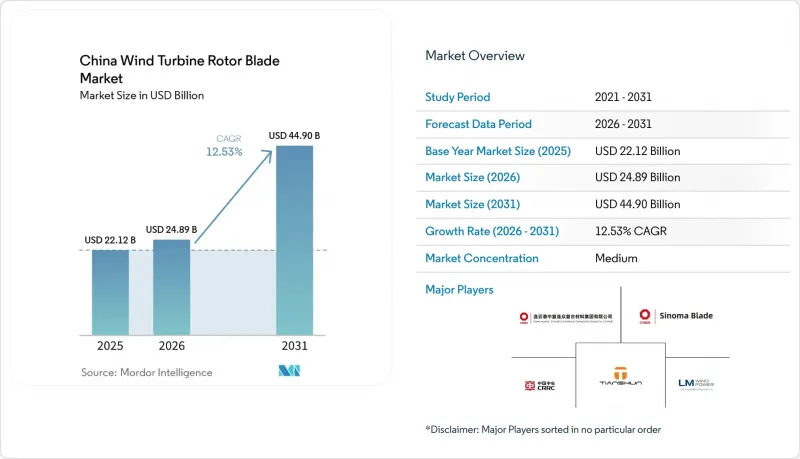

據 Mordor Intelligence 稱,2025 年中國風力發電機葉輪市場規模為 221.2 億美元,預計到 2031 年將從 2026 年的 248.9 億美元成長至 449 億美元,預測期(2026-2031 年)複合年成長率為 12.53%。

本報告按安裝地點(陸上和海上)、葉片材料(碳纖維、玻璃纖維、混合複合複合材料及其他葉片材料)、葉片長度(小於45米、46-60米、61-75米及大於75米)和製造程序(手工積層、真空灌注、預浸料及其他)進行細分。市場規模和預測以美元計價。

中國風力發電機葉輪市場的趨勢與洞察

雄心勃勃的2030年風電裝置容量目標

中國計劃在2030年將累積風電裝置容量擴大至400吉瓦,預計僅2025年就將實現140吉瓦的裝置容量。這項政策的確定性推動了對更大尺寸風力渦輪機葉片的長期採購,目前直徑超過180公尺的葉片佔比已達58.6%。市電平價的目標迫使原始設備製造商(OEM)最佳化葉片的空氣動力學特性,以適應包括內陸和沿海地區在內的各種環境條件。政府的持續支持帶動了資本不斷流入新的葉片工廠,刺激了技術創新,並使中國風力發電機葉輪市場保持快速成長。

碳玻璃複合材料葉片成本降低超過 80 米

與純玻璃纖維設計相比,混合複合材料葉片重量減輕38%,成本降低14%,同時保持了剛性。自動化纖維鋪放和熱塑性樹脂加工技術的進步,使得大規模生產成為可能,鞏固了中國在離岸風力發電機葉片市場的領先地位,尤其是在長度超過80公尺的葉片領域。本土聚氨酯樹脂系統供應商正在推動混合材料的應用,引領中國風力發電機葉輪市場朝向輕量化、高性能解決方案發展,以滿足16兆瓦級風力發電機的需求。

環氧樹脂和PET泡沫的價格波動給利潤率帶來了壓力。

由於供應有限的輕木被PET泡沫塑膠取代,石化產品價格波動的影響日益加劇。樹脂價格上漲已導致OEM廠商的利潤率下降高達3個百分點。外匯波動和進口關稅使預算編制更加複雜,迫使企業尋求供應鏈多元化,並試行引入生質塑膠(也稱為生物樹脂)。在風力發電機激烈的競標競爭下,價格傳導受到限制,整個中國風力發電機葉輪市場的盈利壓力依然巨大。

細分市場分析

2025年,陸域風力發電機葉片將佔總裝置容量的92.12%,預計2031年將維持13.05%的複合年成長率。這主要得益於中國風力發電機葉輪市場在該領域的快速擴張,而大規模的改造升級正是推動這一成長的主要因素。內蒙古和新疆的風電場業主正在用最新的5兆瓦機組替換2兆瓦以下的舊機組,使其電廠的發電能力提高了70%以上。

近期省級競標對平準化電力成本(LCOE)設定了嚴格的限制,促使原始設備製造商(OEM)採用更長的轉子,以在固定電價框架內最大限度地提高兆瓦時發電量。空氣動力學性能的提升和混合材料的應用降低了機艙重量,確保了即使在複雜的內陸運輸路線上也能實現物流可行性。這形成了一個良性循環,提高了產能利用率並降低了成本,鞏固了陸上風電在中國風力發電機葉輪市場的主導地位。

離岸風力發電雖然目前規模較小,但卻是成長最快的領域,預計從2025年起年新增裝置容量將超過10吉瓦。 2025年,江蘇省深海海域進行了一項開創性的240公尺轉子測試,預示著未來將採購能夠抵禦海浪飛濺的超長葉片。目前正在福建省進行測試的浮體式基礎將有助於向南方深海域拓展,增加地理多樣性,並重振整個中國風力發電機葉輪市場。

碳纖維目前佔50.72%的市場佔有率,尤其是在10兆瓦以上的離岸風力發電發電機組中,這主要得益於其優異的剛度重量比。然而,預計到2031年,混合材料的複合年成長率將達到13.28%,並可能在2032年超越碳纖維的市場佔有率,從而重塑中國風力發電機葉輪市場的格局。

製造商透過將單層碳纖維與玻璃纖維混合,在保持關鍵彎曲剛度的同時降低了成本。熱塑性樹脂的使用使得大型零件能夠回收利用,符合中國2030年循環經濟標準。由此,混合材料彌合了成本與永續性的差距,擴大了潛在需求,並鞏固了市場成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 雄心勃勃的2030年風電裝置容量目標

- 降低長度超過 80 公尺的碳玻璃複合材料葉片的成本

- 沿海各州離岸風力發電快速擴張

- 2010年代製造的陸上風力發電機的更換速度正在加快。

- 利用普魯特林法實現自動化葉片生產線的商業化

- 利用數位雙胞胎的產品壽命延長和保固模式

- 市場限制因素

- 環氧樹脂和PET泡沫價格的波動給利潤率帶來了壓力。

- 中國北方風電設施面臨電網約束風險

- 對新計畫的土地使用和環境核准提出更嚴格的要求。

- 熟練的複合材料工程師短缺

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- PESTLE分析

第5章 市場規模與成長預測

- 按部署位置

- 陸上

- 離岸

- 按刀片材質

- 玻璃纖維

- 碳纖維

- 混合複合材料

- 其他

- 按刀片長度

- 小於45米

- 46~60 m

- 61~75 m

- 75米或以上

- 透過製造程序

- 手工積層

- 真空輸液

- 預孕

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

- Sinoma Wind Power Blade Co. Ltd

- Zhuzhou Times New Material Technology Co. Ltd

- Tianshun Wind Energy(Suzhou)Co. Ltd

- LM Wind Power(GE Renewable Energy)

- TPI Composites Inc.(China)

- Nordex SE(Jiangsu Facility)

- Vestas Wind Systems A/S(Tianjin)

- Siemens Gamesa Renewable Energy(Tianjin)

- Goldwind Science & Technology Co. Ltd

- Dongfang Electric Wind Blade Co. Ltd

- Shanghai Aeolon Wind Energy Technology

第7章 市場機會與未來展望

According to Mordor Intelligence, the china wind turbine rotor blade market size was valued at USD 22.12 billion in 2025 and estimated to grow from USD 24.89 billion in 2026 to reach USD 44.9 billion by 2031, at a CAGR of 12.53% during the forecast period (2026-2031).

This report is Segmented by Location of Deployment (Onshore and Offshore), Blade Material (Carbon Fiber, Glass Fiber, Hybrid Composites, and Other Blade Materials), Blade Length (Below 45 M, 46 To 60 M, 61 To 75 M, and Above 75 M), and Manufacturing Process (Hand Lay-Up, Vacuum Infusion, Pre-Preg, and Others). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

China Wind Turbine Rotor Blade Market Trends and Insights

Ambitious 2030 Wind-Power Capacity Targets

China plans to hit 400 GW of cumulative wind by 2030, with 140 GW slated for 2025 alone. This policy certainty drives the long-term procurement of ever-larger rotors, 58.6% of which now exceed 180 m in diameter. Grid-parity objectives force OEMs to optimize blade aerodynamics for diverse inland and coastal conditions. Consistent government backing sustains capital inflows into new blade factories, sparking technology upgrades that keep the Chinese wind turbine rotor blade market on a steep growth curve.

Cost Decline in > 80 m Carbon-Glass Hybrid Blades

Hybrid composites reduce blade weight by 38% and costs by 14% compared to glass-only designs, while maintaining stiffness. Automated fiber placement and thermoplastic processing now enable serial manufacture, anchoring China's leadership in blades exceeding 80 m in length for offshore use. Local suppliers of polyurethane resin systems are strengthening hybrid adoption, pushing the China wind turbine rotor blade market toward lightweight, high-performance solutions suited for 16 MW-class turbines.

Volatile Epoxy & PET Foam Prices Squeezing Margins

Shift from scarce balsa to PET foam magnifies exposure to petrochemical swings; resin spikes already compress OEM margins by up to 3 percentage points. Currency shifts and import tariffs complicate budgeting, compelling supply-chain diversification and trials of bioplastics, also known as bio-resins. Price pass-through is limited amid cut-throat turbine bidding, keeping profitability pressure high across the Chinese wind turbine rotor blade market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Offshore Wind Build-Out Along Coastal Provinces

- Accelerating Replacement of 2010-Era Onshore Turbines

- Grid Curtailment Risk in Northern China Wind Bases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Onshore blades contribute 92.12% of 2025 installations and are projected to log a 13.05% CAGR to 2031, driven by large-scale repowering that rapidly expands the China wind turbine rotor blade market size for this segment. Fleet owners in Inner Mongolia and Xinjiang swap out sub-2 MW units for modern 5 MW designs that increase site yields by more than 70%

Latest province-level auctions include strict LCOE caps, prompting OEMs to opt for longer rotors to maximize megawatt-hours within fixed tariffs. Enhanced aerodynamics and hybrid materials keep nacelle mass in check, ensuring logistics feasibility across rugged inland transport routes. The result is a virtuous cycle of capacity factor gains and declining costs that entrenches onshore leadership in the Chinese wind turbine rotor blade market.

Offshore arrays, though smaller today, represent the fastest-growing slice, adding more than 10 GW annually after 2025. Jiangsu's deep-sea sites pioneered 240-m rotor trials in 2025, signalling future procurement of extra-long, splash-zone-resistant blades. Floating foundations under test in Fujian could unlock Southern deep-water zones, expanding geographical diversity and boosting the overall China wind turbine rotor blade market.

Carbon fiber's 50.72% share stems from its stiffness-to-weight edge, especially for > 10 MW offshore machines. Yet, hybrids will see a 13.28% CAGR to 2031 and could overtake carbon by volume before 2032, reshaping the China wind turbine rotor blade market share landscape.

Producers blend carbon unis with glass fabrics, lowering cost while retaining critical bending stiffness. Thermoplastic resins make large-part recycling feasible, aligning with China's 2030 circular-economy standards. Hybrids thus bridge the cost and sustainability gap, widening the addressable demand and anchoring market expansion.

List of Companies Covered in this Report:

- Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

- Sinoma Wind Power Blade Co. Ltd

- Zhuzhou Times New Material Technology Co. Ltd

- Tianshun Wind Energy (Suzhou) Co. Ltd

- LM Wind Power (GE Renewable Energy)

- TPI Composites Inc. (China)

- Nordex SE (Jiangsu Facility)

- Vestas Wind Systems A/S (Tianjin)

- Siemens Gamesa Renewable Energy (Tianjin)

- Goldwind Science & Technology Co. Ltd

- Dongfang Electric Wind Blade Co. Ltd

- Shanghai Aeolon Wind Energy Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ambitious 2030 wind-power capacity targets

- 4.2.2 Cost decline in >80 m carbon-glass hybrid blades

- 4.2.3 Rapid offshore wind build-out along coastal provinces

- 4.2.4 Accelerating replacement of 2010-era onshore turbines

- 4.2.5 Commercialisation of pultrusion-based automated blade lines

- 4.2.6 Digital-twin enabled life-extension & warranty models

- 4.3 Market Restraints

- 4.3.1 Volatile epoxy & PET foam prices squeezing margins

- 4.3.2 Grid curtailment risk in Northern China wind bases

- 4.3.3 Stricter land-use & ecological approvals for new projects

- 4.3.4 Shortage of skilled composites technicians

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 By Blade Material

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.2.3 Hybrid Composites

- 5.2.4 Others

- 5.3 By Blade Length

- 5.3.1 Below 45 m

- 5.3.2 46 to 60 m

- 5.3.3 61 to 75 m

- 5.3.4 Above 75 m

- 5.4 By Manufacturing Process

- 5.4.1 Hand Lay-Up

- 5.4.2 Vacuum Infusion

- 5.4.3 Pre-Preg

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

- 6.4.2 Sinoma Wind Power Blade Co. Ltd

- 6.4.3 Zhuzhou Times New Material Technology Co. Ltd

- 6.4.4 Tianshun Wind Energy (Suzhou) Co. Ltd

- 6.4.5 LM Wind Power (GE Renewable Energy)

- 6.4.6 TPI Composites Inc. (China)

- 6.4.7 Nordex SE (Jiangsu Facility)

- 6.4.8 Vestas Wind Systems A/S (Tianjin)

- 6.4.9 Siemens Gamesa Renewable Energy (Tianjin)

- 6.4.10 Goldwind Science & Technology Co. Ltd

- 6.4.11 Dongfang Electric Wind Blade Co. Ltd

- 6.4.12 Shanghai Aeolon Wind Energy Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

風力發電機葉片檢測服務市場:2026-2032年全球市場預測(依服務類型、服務交付方式、渦輪機功率、自動化程度及安裝位置分類)

風力發電機葉片檢測服務市場:2026-2032年全球市場預測(依服務類型、服務交付方式、渦輪機功率、自動化程度及安裝位置分類) 離岸風力發電渦輪機葉輪市場-全球產業規模、佔有率、趨勢、機會、預測:按葉片材料、地區和競爭格局分類,2021-2031年風力發電機葉片市場 - 全球產業規模、佔有率、趨勢、機會、預測:葉片長度、材料、部署、區域及競爭格局,2021-2031年

離岸風力發電渦輪機葉輪市場-全球產業規模、佔有率、趨勢、機會、預測:按葉片材料、地區和競爭格局分類,2021-2031年風力發電機葉片市場 - 全球產業規模、佔有率、趨勢、機會、預測:葉片長度、材料、部署、區域及競爭格局,2021-2031年 風力發電機葉片檢測服務市場:依安裝地點、服務類型和區域分類

風力發電機葉片檢測服務市場:依安裝地點、服務類型和區域分類 全球風力發電機葉片回收市場

全球風力發電機葉片回收市場 風力發電機葉輪市場規模、佔有率、趨勢和預測:按葉片材質、葉片長度、安裝位置和地區分類,2026-2034年風力發電機葉片市場:依材料、葉片長度、功率輸出、安裝方式及地區分類風力發電機葉輪市場:按渦輪機容量、葉片材質、渦輪機類型、風力等級、塗層類型分類,全球預測(2026-2032年)

風力發電機葉輪市場規模、佔有率、趨勢和預測:按葉片材質、葉片長度、安裝位置和地區分類,2026-2034年風力發電機葉片市場:依材料、葉片長度、功率輸出、安裝方式及地區分類風力發電機葉輪市場:按渦輪機容量、葉片材質、渦輪機類型、風力等級、塗層類型分類,全球預測(2026-2032年) 風力渦輪機葉片回收市場分析及預測至 2035 年:按類型、產品、服務、技術、組件、應用、製程、最終用戶、安裝類型和解決方案分類。

風力渦輪機葉片回收市場分析及預測至 2035 年:按類型、產品、服務、技術、組件、應用、製程、最終用戶、安裝類型和解決方案分類。 風力發電機葉輪市場規模、佔有率和成長分析(按葉片材質、葉片設計、終端用戶產業、長度類別和地區分類)-2026-2033年產業預測

風力發電機葉輪市場規模、佔有率和成長分析(按葉片材質、葉片設計、終端用戶產業、長度類別和地區分類)-2026-2033年產業預測