|

市場調查報告書

商品編碼

2066656

北美鉛酸蓄電池市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)North America Lead Acid Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

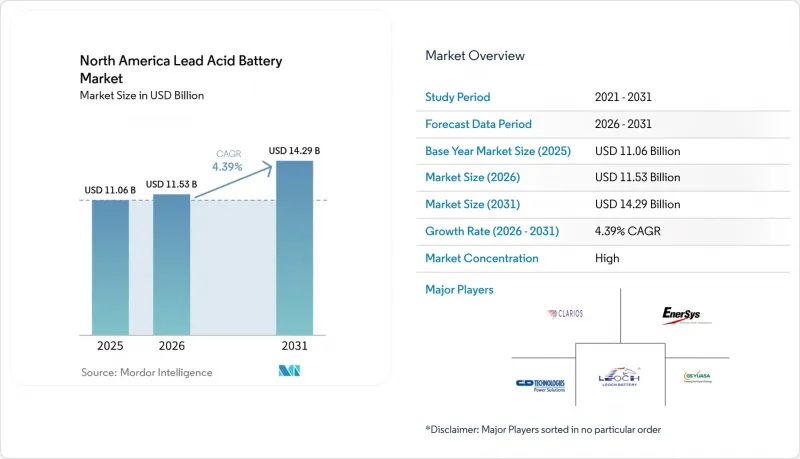

據 Mordor Intelligence 稱,北美鉛酸電池市場預計將從 2025 年的 110.6 億美元成長到 2026 年的 115.3 億美元,到 2031 年達到 142.9 億美元,2026 年至 2031 年的複合年成長率為 4.39%。

本報告按結構類型(液壓式、閥控式鉛酸蓄電池)、應用領域(啟動、照明和點火 (SLI)、固定式、動力和牽引(堆高機、高爾夫球車)、可攜式及其他)和地區(美國、加拿大、墨西哥)進行細分。市場預測以美元 (USD) 為單位。

北美鉛酸蓄電池市場趨勢與洞察

車隊中老舊內燃機車輛的更換需求

美國車輛的平均使用壽命已達到創紀錄的12.6年,引發了一波結構性的電池更換需求。這是因為車齡超過11年的車輛的電池更換率已達到每年37%。根據國際電池協會(BCI)的研究,2024年鉛酸電池的出貨量為1.59億塊,其中大部分是由於更換需求而非原廠安裝。啟動停止技術和駕駛輔助功能帶來的更高功率負載正在加速從液態電解質電池轉向吸附式玻璃纖維隔板(AGM)閥控式鉛酸電池(VRLA)的轉變。標普全球預測,到2027年,AGM電池將佔所有售後市場安裝量的19%。歐萊利汽車配件公司(O'Reilly Auto Parts)將東賓州公司(East Penn)評為2025年度最佳供應商,以表彰該公司擴大DIN尺寸AGM電池的生產規模,其產品可覆蓋超過40%的在運作中車輛。重要的是,農村和低收入買家往往會更長時間地使用內燃機汽車,這減緩了電動車的市場擴張速度,延長了北美鉛酸電池市場的壽命。

UPS在資料中心和通訊領域的蓬勃發展。

為因應人工智慧 (AI) 工作負載而進行的超大規模建設預計將使全球資料中心電力需求從 2022 年的 460 太瓦時 (TWh) 增至 2030 年的 945 太瓦時。即使到了 2025 年,VRLA 電池,尤其是 AGM 型電池,仍佔據全球 UPS 電池市場 58% 的佔有率,該市場價值 43.3 億美元。 2024 年德克薩斯州參議院第 6 號法案 (SB 6) 強制要求現場備用電源,隨著現有設施的維修,VRLA 電池的採購量也隨之增加。同時,由於鋰離子電池具有高能量密度優勢,新計畫正傾向選擇鋰離子電池。同樣,在 5G 基地台部署中,密封免維護的 VRLA 電池被用於偏遠地區,以減少維護次數。儘管鋰離子電池在 10 年內的總擁有成本 (TCO) 比 VRLA 電池低 39%,但由於 VRLA 電池的資本投資預算和完善的回收管道,其在龐大的部署基礎中仍然佔據重要地位。

鋰離子電池成本快速下降

根據美國能源局(DOE) 的數據,鋰離子電池的價格預計將從 2022 年的每千瓦時 150 美元降至 2024 年的每千瓦時 128-133 美元,較 2014 年的水準下降 85%。在不斷電系統(UPS) 領域,鋰離子電池 8-15 年的使用壽命和 3000-5000 次充放電循環次數,與閥控式鉛酸蓄電池 (VRLA) 相比,10 年總擁有成本 (TCO) 可降低 39%。堆高機產業也出現了類似的變化。鋰離子電池可在 1-2 小時內充滿電,並可進行高達 4000 次的充放電循環,從而降低了電池更換室和備用電池庫存的成本。全球電動堆高機鋰離子電池的普及率可望從2024年的32%躍升至2034年的70%以上。然而,在美國,鋰離子電池的普及速度預計會更慢,因為50%至60%的設施仍需要昂貴的電氣設備維修。不過,一旦鋰離子電池與鉛酸電池的初始成本持平,鉛酸電池將不得不依靠其安全性和對循環經濟的貢獻來維持其在高運轉率領域的市場佔有率。

細分市場分析

預計到2025年,VRLA(密閉式鉛酸電池)將佔據北美鉛酸蓄電池市場64.3%的佔有率,並將以5.7%的複合年成長率持續成長至2031年,其性能將優於傳統的電解式鉛酸蓄電池。這項優勢源自於其密封設計,無需加水,減少了氣體排放,並有助於符合美國職業安全與健康管理局(OSHA)的室內空氣品質法規。在VRLA類別中,AGM(自動綠色大容量電池)正迅速發展,因為其更快的充電速度顯著減少了每年經歷數百次充放電循環的送貨車和共享汽車的運作。 2025年,EnerSys公司在南卡羅來納州薩姆特投資670萬美元,用於擴建其薄片純鉛(TPPL)和AGM產品的生產線。這些產品的使用壽命可達 8 至 10 年,而同類液態電解質電池的使用壽命僅為 3 至 5 年。

在注重成本的售後市場和重型運輸卡車領域,液態電解質電池仍然很受歡迎,因為在這些領域,深迴圈電池的耐用性和低成本至關重要。鉛碳混合電池正在逐步推進技術進步,這種電池將碳摻入負極板中,以提高部分充電狀態的性能。加拿大北極微電網的先導計畫驗證了這種化學成分的性能,它無需外部加熱器即可承受-40 度C的環境溫度。監管標準也悄悄提升密封式VRLA電池的UL 1989認證標準,VRLA電池的防漏外殼滿足了當地消防部門對資料中心維修日益嚴格的要求。這些因素共同作用,使得VRLA電池在北美鉛酸電池市場中的佔有率持續擴大,即使電解電解質鉛酸電池的銷量下降。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於內燃機車輛老化而產生的更換需求

- 資料中心和電信業的UPS擴張熱潮

- SLI應用情境的成本競爭力及其與鋰基替代材料的比較

- 為48V輕混車輛採用輔助電池。

- 用於偏遠地區微電網的鉛碳電池(加拿大北極地區、離網礦區)

- 強制推行閉合迴路回收正在加速國內供應的穩定。

- 市場限制因素

- 鋰離子電池組成本快速下降

- 鉛中毒引發的環境與健康問題

- 美國環保署(EPA)即將提高大氣中鉛含量的規定。

- 廢鉛出口量波動導致再生鉛供應量波動。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 透過施工方法

- 潛水器

- VRLA

- 透過使用

- 啟動、照明和點火 (SLI)

- 固定式

- 動力/驅動系統(堆高機、高爾夫球車)

- 可攜式及其他

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Clarios

- East Penn Manufacturing

- EnerSys

- Exide Technologies

- C&D Technologies

- GS Yuasa Corporation

- Leoch International

- Power-Sonic Corporation

- Panasonic Holdings Corp

- Crown Battery Manufacturing

- Trojan Battery Company

- NorthStar Battery Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america lead acid battery market size is expected to increase from USD 11.06 billion in 2025 to USD 11.53 billion in 2026 and reach USD 14.29 billion by 2031, growing at a CAGR of 4.39% over 2026-2031.

This report is Segmented by Construction Method (Flooded, VRLA), Application (Starting-Lighting-Ignition (SLI), Stationary, Motive/Traction (Forklifts, Golf-Carts), Portable and Others), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Lead Acid Battery Market Trends and Insights

Replacement Demand from Aging ICE-Vehicle Fleet

The U.S. fleet's record 12.6-year average age underpins a structural replacement wave because vehicles 11 years or older post a 37% annual battery swap rate. Battery Council International tracked 159 million lead acid units shipped in 2024, the bulk tied to replacement rather than factory-install volume. Growing electrical loads from start-stop technology and driver-assistance features hasten the shift from flooded batteries to absorbed-glass-mat (AGM) VRLA designs, which S&P Global projects will reach 19% of all aftermarket installs by 2027. O'Reilly Auto Parts named East Penn its 2025 Supplier of the Year after the vendor scaled DIN-size AGM output that could cover over 40% of vehicles in operation. Crucially, rural and lower-income buyers who retain internal-combustion vehicles longer slow EV cannibalization, extending the tail of the North America lead acid battery market.

Data-Center & Telecom UPS Expansion Boom

Hyperscale builds to serve artificial-intelligence workloads are lifting global data-center electricity demand toward 945 TWh by 2030, up from 460 TWh in 2022. VRLA batteries, especially AGM variants, still held 58% of the USD 4.33 billion global UPS battery segment in 2025. Texas Senate Bill 6 of 2024 requires on-site backup, which is spurring retrofit purchases even while greenfield projects choose lithium-ion for densification advantages. 5G tower roll-outs likewise favor VRLA at remote sites where sealed, maintenance-free units cut service visits. Although lithium-ion offers a 39% lower 10-year TCO, capital budgets and well-established recycling channels preserve VRLA relevance across a large installed base.

Rapid Cost Decline of Lithium-Ion Packs

DOE data show lithium-ion pack prices fell to USD 128-133 per kWh in 2024 from USD 150 per kWh in 2022, an 85% drop versus 2014 levels. In UPS service, that translates to a 39% lower 10-year TCO relative to VRLA, thanks to 8-15 year service life and 3,000-5,000 charge cycles. Forklift fleets mirror the shift: lithium-ion units recharge in 1-2 hours and deliver up to 4,000 cycles, saving on battery-swap rooms and spare-pack inventory. Global lithium-ion penetration in electric forklifts could jump from 32% in 2024 to over 70% by 2034, with the U.S. lagging because 50-60% of facilities still need costly electrical upgrades. Nonetheless, once upfront cost parity is crossed, lead acid must lean on its safety and circular-economy image to defend share in high-utilization segments.

Other drivers and restraints analyzed in the detailed report include:

- 48 V Mild-Hybrid Auxiliary Battery Adoption

- Closed-Loop Recycling Mandates Accelerating Supply Security

- Environmental & Health Concerns over Lead Toxicity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

VRLA units captured 64.3% of the North America lead acid battery market in 2025 and are expected to compound at 5.7% annually through 2031, outpacing conventional flooded cells. This leadership stems from sealed architectures that eliminate watering labor, reduce gas emissions, and simplify compliance with OSHA indoor-air rules. Within VRLA, AGM variants command momentum because faster charge acceptance slashes turnaround time for delivery vans and ride-hail vehicles that cycle hundreds of times per year. EnerSys invested USD 6.7 million in Sumter, South Carolina, during 2025 to expand thin-plate-pure-lead (TPPL) and AGM lines that promise 8-10 year life versus 3-5 years for flooded rivals.

Flooded batteries still serve cost-sensitive aftermarket channels and heavy-duty haul trucks where buyers prize deep-cycle robustness and lower list prices. Incremental innovation is emerging through lead-carbon hybrids that embed carbon in negative plates to boost partial-state-of-charge performance; pilot projects in Canadian Arctic micro-grids illustrate the chemistry's tolerance of -40 °C ambient temperatures without external heaters. Regulatory codes also tilt subtly toward VRLA UL 1989 certification, which is simpler for sealed units, and VRLA's spill-proof shell satisfies increasingly stringent local fire marshals overseeing data-center retrofit work. These factors collectively sustain VRLA's expanding role inside the North America lead acid battery market size even as flooded sales taper.

List of Companies Covered in this Report:

- Clarios

- East Penn Manufacturing

- EnerSys

- Exide Technologies

- C&D Technologies

- GS Yuasa Corporation

- Leoch International

- Power-Sonic Corporation

- Panasonic Holdings Corp

- Crown Battery Manufacturing

- Trojan Battery Company

- NorthStar Battery Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Replacement demand from aging ICE-vehicle fleet

- 4.2.2 Data-center & telecom UPS expansion boom

- 4.2.3 Cost competitiveness vs. lithium alternatives in SLI use-cases

- 4.2.4 48 V mild-hybrid auxiliary battery adoption

- 4.2.5 Lead-carbon batteries for remote micro-grids (Canada Arctic, off-grid mining)

- 4.2.6 Closed-loop recycling mandates accelerating domestic supply security

- 4.3 Market Restraints

- 4.3.1 Rapid cost decline of lithium-ion packs

- 4.3.2 Environmental & health concerns over lead toxicity

- 4.3.3 Impending tighter U.S. EPA ambient-lead limits

- 4.3.4 Recycled-lead supply volatility from scrap-export flows

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Construction Method

- 5.1.1 Flooded

- 5.1.2 VRLA

- 5.2 By Application

- 5.2.1 Starting-Lighting-Ignition (SLI)

- 5.2.2 Stationary

- 5.2.3 Motive/Traction (Forklifts, Golf-carts)

- 5.2.4 Portable and Others

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Clarios

- 6.4.2 East Penn Manufacturing

- 6.4.3 EnerSys

- 6.4.4 Exide Technologies

- 6.4.5 C&D Technologies

- 6.4.6 GS Yuasa Corporation

- 6.4.7 Leoch International

- 6.4.8 Power-Sonic Corporation

- 6.4.9 Panasonic Holdings Corp

- 6.4.10 Crown Battery Manufacturing

- 6.4.11 Trojan Battery Company

- 6.4.12 NorthStar Battery Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

VRLA電池市場規模、佔有率和成長分析:按類型、電壓、容量、應用、最終用戶、銷售管道和地區分類-2026-2033年產業預測

VRLA電池市場規模、佔有率和成長分析:按類型、電壓、容量、應用、最終用戶、銷售管道和地區分類-2026-2033年產業預測 住宅鉛酸蓄電池市場-全球產業規模、佔有率、趨勢、機會和預測:按產品、安裝方式、銷售管道、地區和競爭格局分類,2021-2031年商用鉛酸蓄電池市場-全球產業規模、佔有率、趨勢、機會與預測:按產品、結構、銷售管道、地區和競爭格局分類,2021-2031年閥控式鉛酸蓄電池市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、技術、應用、地區和競爭格局分類,2021-2031年

住宅鉛酸蓄電池市場-全球產業規模、佔有率、趨勢、機會和預測:按產品、安裝方式、銷售管道、地區和競爭格局分類,2021-2031年商用鉛酸蓄電池市場-全球產業規模、佔有率、趨勢、機會與預測:按產品、結構、銷售管道、地區和競爭格局分類,2021-2031年閥控式鉛酸蓄電池市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、技術、應用、地區和競爭格局分類,2021-2031年 鉛酸蓄電池市場:按類型、電壓範圍、技術、分銷方式及最終用戶分類-2026-2032年全球市場預測

鉛酸蓄電池市場:按類型、電壓範圍、技術、分銷方式及最終用戶分類-2026-2032年全球市場預測 鉛酸蓄電池市場:依產品類型、構造方法、應用和地區分類。

鉛酸蓄電池市場:依產品類型、構造方法、應用和地區分類。 2026-2034年全球鉛酸蓄電池市場規模、佔有率、趨勢及成長分析報告

2026-2034年全球鉛酸蓄電池市場規模、佔有率、趨勢及成長分析報告 鉛酸蓄電池市場報告:按產品、製造方法、銷售管道、應用和地區分類(2026-2034年)

鉛酸蓄電池市場報告:按產品、製造方法、銷售管道、應用和地區分類(2026-2034年) 2026年全球固定式鉛酸蓄電池市場報告2026年全球摩托車鉛酸蓄電池市場報告

2026年全球固定式鉛酸蓄電池市場報告2026年全球摩托車鉛酸蓄電池市場報告