|

市場調查報告書

商品編碼

2066639

非洲電池市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Africa Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

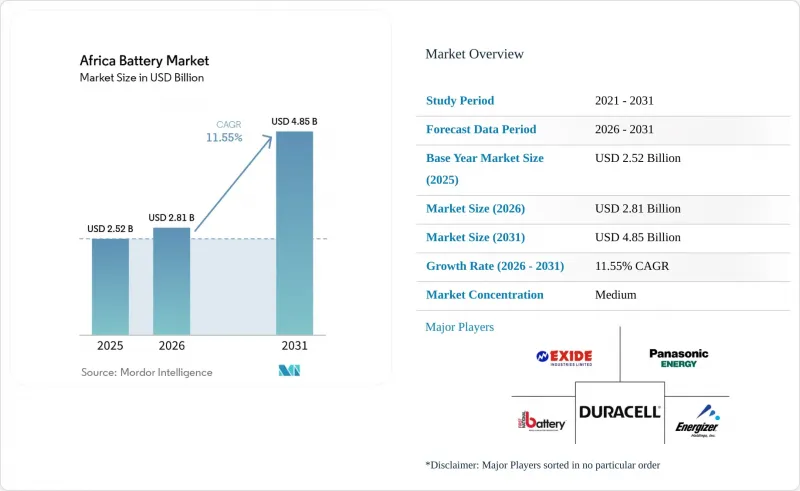

據 Mordor Intelligence 稱,2025 年非洲電池市場價值 25.2 億美元,預計到 2031 年將從 2026 年的 28.1 億美元成長至 48.5 億美元,預測期(2026-2031 年)複合年成長率為 11.55%。

本報告按電池類型(一次電池)、技術(鉛酸電池、鋰離子電池、鎳氫電池、鎳鎘電池、鈉硫電池、全固體電池、液流電池和新興化學品電池)、應用(汽車、工業、攜帶式、電動工具、SLI 和其他應用)和地區(南非、埃及、肯亞、奈及利亞、摩洛哥、衣索比亞和非洲其他地區)進行分類。

非洲電池市場趨勢與洞察

鋰離子電池價格正在下降。

到2024年,全球電池組價格已降至每千瓦時115美元,中國市場更是降至每千瓦時94美元。這最終使其價格低於非洲通訊塔和微電網所用柴油發電機的價格。 MTN和Airtel等業者正在對其設施維修,採用壽命長達10年的鋰離子電池系統,從而將總擁有成本降低約30%,並大幅減少維護次數。南非和埃及的電力公司目前正在將按小時計費的儲能系統與太陽能發電廠結合。一個典型的例子是540兆瓦的肯哈特項目,該項目整合了1140兆瓦時的電池,以滿足晚間用電高峰需求。一家中國正負極材料工廠在摩洛哥投產,正在形成良性循環,進一步壓縮供應鏈成本,使其更經濟實惠。

離網太陽能發電+BESS(建築能源管理系統)的採用率正在迅速提高。

在電網擴建成本效益仍不高的地區,結合離網太陽能發電和儲能系統的微電網正迅速普及。衣索比亞正利用儲能容量為4-8小時的太陽能發電系統,目標是到2030年實現35%的離網電氣化。埃及、波札那和尚比亞也採用了類似的模式,並從多邊銀行獲得了融資,這些銀行現在認可儲能系統產生的現金流符合貸款條件。通訊業者和農產品低溫運輸業者可以證明增加初始投資的合理性,因為正常運作的提高將改善農村地區的能源取得和經濟活動。

原料供應瓶頸

剛果民主共和國(剛果(金))的「30%加工規則」導致鈷的運輸停滯,造成4至6週的延誤,並使亞洲買家的收貨成本增加了12%。在辛巴威,鐵路運輸能力成為鋰出口的瓶頸,導致運費是澳洲同類產品的兩倍。同時,由於鐵路運輸的不可靠性,南非的錳礦商不得不使用卡車運輸礦石。小規模鈷礦開採約佔全球鈷供應量的20%,目前在歐盟盡職調查法下,其合規性尚不明確,使買家面臨法律和聲譽風險。

細分市場分析

預計到2025年,可充電電池將佔總銷售額的86.5%,其市場主導地位預計將以12.1%的複合年成長率進一步鞏固。汽車和工業領域的客戶看重可充電電池較低的生命週期成本,鋰離子電池正在高循環應用中取代鉛酸電池。一次電池仍保持13.5%的市場佔有率,主要應用於低功率設備。預計到2031年,非洲可充電電池市場規模將超過40億美元,其中鋰離子電池預計將貢獻大部分成長。

隨著肯亞和南非擴大生產者責任制(EPR)機制下的費用提高,預計一次電池在非洲電池市場的佔有率將持續下降。雖然像First National Battery這樣的鉛回收商可以回收96%的鉛,但鋰離子電池的回收利用仍然有限,這表明存在投資機會。 Gotion在摩洛哥的工廠將透過縮短交貨時間和對沖外匯,進一步鼓勵買家轉向充電電池。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 鋰離子電池的價格正在下降。

- 離網太陽能發電和建築能源管理系統 (BESS) 的應用正在迅速增加。

- 政府對國內電池製造的獎勵措施

- 兩輪和三輪車輛的快速電氣化

- 通訊塔維修週期

- 中國資本擴建鋰加工廠

- 市場限制因素

- 原料供應瓶頸

- 不均衡的電網和充電基礎設施

- 假冒偽劣電池大量湧入

- 政策碎片化和執行不力

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依電池類型

- 一次電池

- 輔助電池

- 透過技術

- 鉛酸

- Li-ion

- 鎳氫電池

- 鎳和鎘

- 鈉和硫

- 固態電池

- 液流電池

- 新興化學技術

- 透過使用

- 汽車(混合動力車、插電式混合動力車、電動車)

- 工業用途(移動式、固定式(通訊、UPS、ESS 等))

- 可攜式(家用電子電器等)

- 電動工具

- SLI

- 其他用途

- 按地區

- 南非

- 埃及

- 肯亞

- 奈及利亞

- 摩洛哥

- 衣索比亞

- 其他非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和市場佔有率)

- 公司簡介

- CATL

- BYD Co. Ltd.

- Panasonic Energy

- Duracell Inc.

- Energizer Holdings Inc.

- Exide Industries Ltd.

- First National Battery(Metair)

- Solar MD

- Uganda Batteries Ltd.

- Chloride Exide Kenya Ltd.

- Luminous Power Technologies

- Murata Manufacturing Co. Ltd.

- East Penn Manufacturing

- EnerSys

- GS Yuasa Corp.

- Gotion High-Tech

- BSL Battery

- Felicity Solar

- Orbit Batteries

- Saft(TotalEnergies)

第7章 市場機會與未來展望

According to Mordor Intelligence, the africa battery market size was valued at USD 2.52 billion in 2025 and is estimated to grow from USD 2.81 billion in 2026 to reach USD 4.85 billion by 2031, at a CAGR of 11.55% during the forecast period (2026-2031).

This report is Segmented by Battery Type (Primary Batteries and Secondary Batteries), Technology (Lead-Acid, Li-Ion, Nickel-Metal Hydride, Nickel-Cadmium, Sodium-Sulfur, Solid-State, Flow Battery, and Emerging Chemistries), Application (Automotive, Industrial, Portable, Power Tools, SLI, and Other Applications), and Geography (South Africa, Egypt, Kenya, Nigeria, Morocco, Ethiopia, and Rest of Africa).

Africa Battery Market Trends and Insights

Declining Lithium-Ion Prices

Global pack prices slipped to USD 115 per kWh in 2024 and to USD 94 per kWh in China, finally undercutting diesel gensets for African telecom towers and microgrids. Operators such as MTN and Airtel retrofit sites with lithium-ion systems that last up to 10 years, trimming the total cost of ownership by about 30% and slashing maintenance trips. South African and Egyptian utilities now pair multi-hour storage with solar farms, exemplified by the 540 MW Kenhardt project that integrates 1,140 MWh of batteries to meet evening peaks. Chinese cathode and anode plants opening in Morocco further compress supply-chain costs, creating a virtuous circle of affordability.

Surge in Off-Grid Solar + BESS Deployments

Off-grid solar-plus-storage microgrids are proliferating where extending grids remains uneconomic. Ethiopia targets 35% off-grid electrification by 2030 using solar arrays with 4-8 hour battery reserves. Egypt, Botswana, and Zambia adopted similar models, securing debt from multilateral banks that now view storage cash flows as bankable. Telecom and agricultural cold-chain operators gain uptime improvements that justify higher upfront spend, advancing rural energy access and economic activity.

Raw-Material Supply Bottlenecks

The DRC's 30% processing rule idled cobalt shipments, adding 4-6 week delays and 12% to Asian buyers' landed costs. Zimbabwe's rail capacity caps lithium exports, doubling freight versus Australian peers, while South African manganese miners truck ore because of rail unreliability. Artisanal cobalt, roughly 20% of global supply, now sits in compliance limbo under the EU due diligence law, exposing buyers to legal and reputational risk.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Local Battery Manufacturing

- Rapid Electrification of Two-/Three-Wheelers

- Counterfeit / Low-Quality Battery Influx

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Secondary batteries delivered 86.5% of 2025 revenues, and their 12.1% CAGR is set to reinforce that dominance. Automotive and industrial clients value rechargeability's lower lifetime cost, while lithium-ion replaces lead-acid in high-cycle roles. Primary cells cling to a 13.5% share mainly in low-drain devices. The Africa battery market size for secondary chemistries is projected to eclipse USD 4 billion by 2031, with lithium-ion securing most gains.

The Africa battery market share of primary cells will keep shrinking as extended producer responsibility fees rise in Kenya and South Africa. Lead recyclers such as First National Battery recover 96% of materials, yet lithium-ion recycling remains scarce, signaling an investment opportunity. Gotion's Moroccan plant will shorten delivery times and hedge currency swings, further tilting buyers toward rechargeables.

List of Companies Covered in this Report:

- CATL

- BYD Co. Ltd.

- Panasonic Energy

- Duracell Inc.

- Energizer Holdings Inc.

- Exide Industries Ltd.

- First National Battery (Metair)

- Solar MD

- Uganda Batteries Ltd.

- Chloride Exide Kenya Ltd.

- Luminous Power Technologies

- Murata Manufacturing Co. Ltd.

- East Penn Manufacturing

- EnerSys

- GS Yuasa Corp.

- Gotion High-Tech

- BSL Battery

- Felicity Solar

- Orbit Batteries

- Saft (TotalEnergies)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining lithium-ion prices

- 4.2.2 Surge in off-grid solar + BESS deployments

- 4.2.3 Government incentives for local battery manufacturing

- 4.2.4 Rapid electrification of two-/three-wheelers

- 4.2.5 Telecom-tower retrofit cycle

- 4.2.6 Chinese-backed lithium-processing build-out

- 4.3 Market Restraints

- 4.3.1 Raw-material supply bottlenecks

- 4.3.2 Patchy grid & charging infrastructure

- 4.3.3 Counterfeit/low-quality battery influx

- 4.3.4 Policy fragmentation & weak enforcement

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Primary Batteries

- 5.1.2 Secondary Batteries

- 5.2 By Technology

- 5.2.1 Lead-acid

- 5.2.2 Li-ion

- 5.2.3 Nickel-metal hydride

- 5.2.4 Nickel-cadmium

- 5.2.5 Sodium-sulfur

- 5.2.6 Solid-state

- 5.2.7 Flow Battery

- 5.2.8 Emerging chemistries

- 5.3 By Application

- 5.3.1 Automotive (HEV, PHEV, and EV)

- 5.3.2 Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.)

- 5.3.3 Portable (Consumer Electronics, etc.)

- 5.3.4 Power Tools

- 5.3.5 SLI

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 South Africa

- 5.4.2 Egypt

- 5.4.3 Kenya

- 5.4.4 Nigeria

- 5.4.5 Morocco

- 5.4.6 Ethiopia

- 5.4.7 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 CATL

- 6.4.2 BYD Co. Ltd.

- 6.4.3 Panasonic Energy

- 6.4.4 Duracell Inc.

- 6.4.5 Energizer Holdings Inc.

- 6.4.6 Exide Industries Ltd.

- 6.4.7 First National Battery (Metair)

- 6.4.8 Solar MD

- 6.4.9 Uganda Batteries Ltd.

- 6.4.10 Chloride Exide Kenya Ltd.

- 6.4.11 Luminous Power Technologies

- 6.4.12 Murata Manufacturing Co. Ltd.

- 6.4.13 East Penn Manufacturing

- 6.4.14 EnerSys

- 6.4.15 GS Yuasa Corp.

- 6.4.16 Gotion High-Tech

- 6.4.17 BSL Battery

- 6.4.18 Felicity Solar

- 6.4.19 Orbit Batteries

- 6.4.20 Saft (TotalEnergies)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

物聯網電池市場規模、佔有率和成長分析:按電池類型、充電方式、應用、連接方式、終端用戶產業、容量和地區分類-2026-2033年產業預測

物聯網電池市場規模、佔有率和成長分析:按電池類型、充電方式、應用、連接方式、終端用戶產業、容量和地區分類-2026-2033年產業預測 2026-2030年全球圓柱形電池市場

2026-2030年全球圓柱形電池市場 2026-2030年全球電池護照合規平台市場

2026-2030年全球電池護照合規平台市場 2026-2030年全球電池護照軟體市場

2026-2030年全球電池護照軟體市場 丁基鋰:全球市場佔有率和排名、總收入和需求預測(2026-2032 年)

丁基鋰:全球市場佔有率和排名、總收入和需求預測(2026-2032 年) 2026年全球電池護照市場報告

2026年全球電池護照市場報告 軟性超薄電池電極解決方案市場預測至2034年-全球電極類型、材料類型、製造方法、電池類型、應用、最終用戶和地區分析

軟性超薄電池電極解決方案市場預測至2034年-全球電極類型、材料類型、製造方法、電池類型、應用、最終用戶和地區分析 電池市場規模、佔有率和成長分析:按電池類型、應用、技術、最終用戶、分銷管道和地區分類-2026-2033年產業預測

電池市場規模、佔有率和成長分析:按電池類型、應用、技術、最終用戶、分銷管道和地區分類-2026-2033年產業預測 BETA伏電池市場-全球產業規模、佔有率、趨勢、機會和預測,按同位素類型、形狀、終端用戶產業、地區和競爭格局分類,2021-2031年

BETA伏電池市場-全球產業規模、佔有率、趨勢、機會和預測,按同位素類型、形狀、終端用戶產業、地區和競爭格局分類,2021-2031年 發電機電池市場報告:按產品類型、銷售管道、最終用戶和地區分類(2026-2034 年)

發電機電池市場報告:按產品類型、銷售管道、最終用戶和地區分類(2026-2034 年)