|

市場調查報告書

商品編碼

2066629

汽車LiDAR:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Automotive LiDAR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

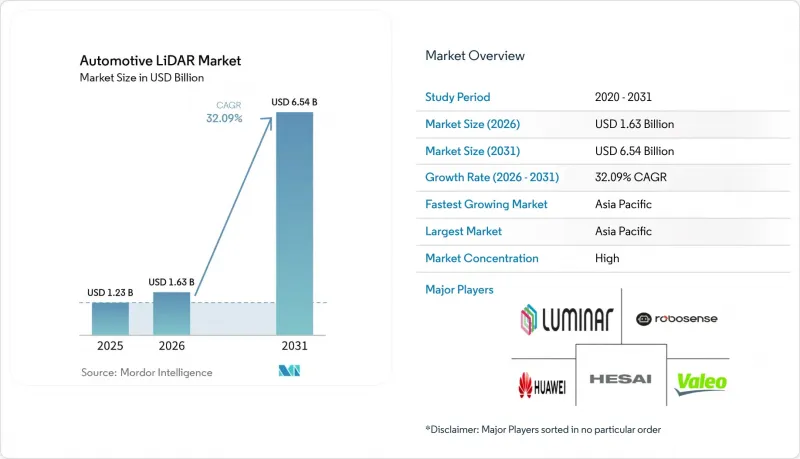

據 Mordor Intelligence 稱,2025 年汽車LiDAR市場價值為 12.3 億美元,預計到 2031 年將達到 65.4 億美元,而 2026 年為 16.3 億美元,預測期(2026-2031 年)的複合年成長率為 32.09%。

本報告按應用領域(自動駕駛汽車和高級駕駛輔助系統[L2+/L2++以上級別])、技術類型(機械式/旋轉式等)、車輛類型(乘用車和商用車)、檢測範圍(短程/中程/遠端)、安裝位置(車頂安裝等)和地區進行細分。市場預測以美元計價。

全球汽車LiDAR市場趨勢及洞察

平均售價(ASP)的急劇下降正在推動中價位車輛的普及。

2023年至2025年間,固態雷射雷達的平均售價下降超過30%,完全適用於汽車應用的閃光感測器價格低於400美元。成本的降低得益於矽光電、晶圓級光學技術和自動化後端測試的整合,使得此類產品能夠應用於高階緊湊型轎車以及豪華旗艦車型。 PreAct Technologies和多家中國晶圓廠的月產量均達到六位數,展現出顯著的規模經濟效益。價格的下降趨勢正在擴大汽車LiDAR市場的整體潛力,使消費者能夠以低於1500美元的價格購買到選配包。隨著應用範圍的擴大,將帶來進一步的學習效應,並在中期內進一步降低成本。

早期FMCW感測器的技術突破

FMCW架構發射連續的低功率光,並採用連貫檢測技術來測量距離和徑向速度。 Aurora Innovation的FirstLight感測器能夠可靠地探測400公尺外反射率為10%的物體,這對於高速公路駕駛至關重要。由於FMCW能夠隔離每個單元的頻率啁啾,即使在交通堵塞的情況下,串擾也幾乎完全消除;此外,其對陽光干擾的更強抵抗力也提高了在各種天氣條件下的運轉率。根據OEM廠商的藍圖,FMCW計劃於2027年在北美和中國的高階車型上投入使用,目前已有幾家OSAT合作夥伴正在開發生產模具。這些進展表明,在預測期內,FMCW將在汽車LiDAR市場增量收入成長中佔據非常大的佔有率。

峰值輸出的眼部安全標準持續受到限制

IEC 60825-1 1級標準限制了最大允許照射劑量,同時也限制了遠程屋頂雷射雷達的光輸出。因此,廠商們不再簡單地提高發射功率,而是依賴更大的接收孔徑、崩光二極體和先進的訊號處理技術。雖然安全標準能夠保護公眾健康,但它們也限制了設計的靈活性,並增加了精密光學元件和溫度控管的成本。這些技術上的權衡取捨減緩了超遠程產品的部署速度,並略微抑制了汽車LiDAR市場的成長前景。

細分市場分析

到2025年,ADAS將佔據汽車LiDAR市場85.12%的佔有率,這反映出其主流化趨勢。此外,ADAS是成長最快的細分市場,複合年成長率高達37.88%,這主要得益於城市層面的核准和共乘行業者的車輛訂單。 ADAS L3和L4項目正在填補市場空白。德國豪華汽車製造商已開始批量交付L3高速公路試點系統,而中國出行公司已在十多個大都會圈營運有監管的L4服務。更高等級的自動駕駛需要多個感測器、冗餘系統和全端檢驗,這增加了每輛車的平均負載,並推動了下一波市場規模的擴張。

隨著我們朝著完全自動駕駛邁進,價值重心正從硬體轉向持續的空中下載(OTA)升級。高速公路自動駕駛的訂閱模式正成為新的收入來源,足以支撐不斷上漲的感測器成本,而L5級車輛車隊收集的數據將有助於迭代式地提升感知能力。隨著這些平台的成熟,良性循環將得到強化:更廣泛的數據覆蓋將支援更安全的演算法,進而推動更廣泛的部署並獲得認證。儘管目前出貨量較低,但這種良性循環支撐著長期的樂觀預測。

到2025年,機械旋轉單元(FMCW)將佔據汽車LiDAR市場62.15%的佔有率。這主要歸功於其成熟的現場性能、360度全方位覆蓋以及完善的生產線。然而,由於存在運動部件,其可靠性在汽車10年的設計壽命內令人擔憂,而外形規格限制也增加了整合到設計中的難度。固態技術,例如MEMS光束控制、光學相控陣和快閃記憶體拓撲結構,為實現全封閉模組和降低成本提供了途徑。在這些固態技術中,FMCW是一個快速成長的子類別,預計到2031年將達到兩位數的市場佔有率,複合年成長率(CAGR)高達47.46%。

法雷奧持續改進第二代「Scala」混合掃描器,而Luminar則正在量產高通道脈衝飛行時間(TOF)掃描器。華為和合賽科技正大力投資其905奈米脈衝和1550奈米FMCW製程,力求分散其在不同車輛類別中的技術風險。這種多元化的格局意味著,儘管FMCW工藝在性能上主導,但沒有任何一種架構能夠主導所有應用場景。

區域分析

預計到2025年,亞太地區將在汽車LiDAR市場佔據主導地位,銷量佔比高達41.75%,其中中國將成為感測器部署中心。地方政府將每輛L3級自動駕駛汽車最高補貼1萬元人民幣的政策延長至2027年,推動了純電動SUV和轎車的普及。從晶圓製造到最終組裝,國內供應鏈的最佳化降低了成本並縮短了前置作業時間,進一步鞏固了該地區的優勢。韓國和新加坡由於示範區和智慧高速公路計畫的建設,市場需求也不斷成長。預計亞太市場將以25.9%的複合年成長率成長,在所有地區中位居榜首。

消費者對連接德克薩斯州、亞利桑那州和加州的自動駕駛卡車路線以及免手持高速公路輔助功能的需求,推動了23.2%的複合年成長率。 Aurora、Auster和Ava均在美國本土運作工廠,降低了對進口的依賴。同時,美國對某些1550奈米VCSEL外延材料的出口限制,促進了本地替代供應商的湧現。在加拿大冬季測試場地,全天候FMCW產品的需求正在顯現。

歐洲緊追在後,複合年成長率達20.4%,反映其監管體系較為完善,但消費者接受度較低。儘管聯合國歐洲經濟委員會(UNECE)的法規起源於歐洲,但各國的型式認證流程仍然十分嚴格,阻礙了大規模交付。然而,來自德國、瑞典和法國的高階品牌正在部署多雷射雷達配置,以滿足L3級高速公路試點計畫的要求,使該地區成為引領技術潮流的先鋒。海灣合作理事會(GCC)地區也湧現出一些較小但值得關注的機遇,該地區正在將自動駕駛班車融入智慧城市大型企劃的新型城市設計中。非洲和拉丁美洲的複合年成長率分別為21.3%和19.6%,基數較低,主要得益於礦業運輸的自動化和公共部門車輛的現代化。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 平均售價(ASP)的急劇下降推動了中價位汽車的成長。

- FMCW LiDAR感測器早期階段的技術突破將探測範圍擴展到了400公尺以上。

- UNECE R157 和 China NCAP 2026 自動駕駛評估標準要求更高的感知能力解析度。

- 一級製造商與雲端音影片技術堆疊簽訂大量生產合約

- 中國各省對支援L3功能的感測器套件提供的補貼

- 汽車製造商的OTA經營模式:高速公路雷射雷達訂閱收入來源

- 市場限制因素

- 現有的眼部安全法規限制了遠端屋頂機組的峰值輸出功率。

- 雷達/攝影機感測器融合的成本降低藍圖正在減緩搭載率。

- 對 1550 奈米 GaAs VCSEL 的出口管制更加嚴格,正在限制跨境供應鏈。

- 對動態光束控制 MEMS 反射鏡在超過 10 年的工作週期內的可靠性表示擔憂。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- LiDAR組件生態系統

- 將LiDAR整合到ADAS車輛中

- 汽車LiDAR技術藍圖(2020-2030)

- 價格趨勢分析

- 波特五力模型

第5章 市場規模與成長預測

- 透過使用

- 機器人車輛

- ADAS

- 2+/2++級

- 3/4級

- 5級

- 依技術類型

- 機械/紡紗

- 固態(MEMS、快閃記憶體)

- FMCW

- 車輛類型

- 搭乘用車

- 商用車輛

- 按範圍

- 短距離和中距離(最遠 150 公尺)

- 長距離(超過150公尺)

- 按安裝位置

- 屋頂安裝型

- 格柵/保險桿

- 一體式大燈

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 其他亞太國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Hesai Technology(Hesai Group)

- RoboSense Technology Co., Ltd.

- Huawei Technologies Co., Ltd.

- Valeo SA

- Luminar Technologies Inc.

- Continental AG

- ZF Friedrichshafen AG

- Innoviz Technologies Ltd.

- Ouster Inc.

- Velodyne LiDAR Inc.

- Aeva Inc.

- AEye Inc.

- LeddarTech Holdings Inc.

- Seyond

- LIVOX

- Blickfeld GmbH

- SiLC Technologies Inc.

- Insight LiDAR

第7章 市場機會與未來展望

According to Mordor Intelligence, the automotive LiDAR market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.63 billion in 2026 to reach USD 6.54 billion by 2031, at a CAGR of 32.09% during the forecast period (2026-2031).

This report is Segmented by Application (Robotic Vehicles and ADAS [Level 2+ / 2++ and More]), Technology Type (Mechanical/Spinning and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Range (Short/Mid-Range and Long-Range), Installation Position (Roof-Mounted and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive LiDAR Market Trends and Insights

Rapid ASP Decline Unlocking Mid-Priced Vehicle Adoption

Average selling prices for solid-state units fell more than 30% between 2023 and 2025, bringing fully automotive-qualified flash sensors below USD 400. Cost reduction stems from silicon photonics integration, wafer-level optics, and back-end test automation, enabling installation on premium compact cars instead of only luxury flagships. PreAct Technologies and several Chinese fabs report six-figure monthly output volumes, illustrating economies of scale. The downward price curve broadens the total addressable automotive LiDAR market by enabling optional packages at sub-USD 1,500 price points for consumers. A greater installed base further drives learning effects that compress cost over the medium term.

Early-stage FMCW Sensor Breakthroughs

FMCW architectures emit continuous low-power light and use coherent detection to measure both distance and radial velocity. Aurora Innovation's FirstLight sensor shows reliable detection of 10% reflectivity objects at 400 meters, a critical requirement for highway speeds. Because FMCW separates each unit's frequency chirp, crosstalk is virtually eliminated in dense traffic, and immunity to solar interference improves all-weather uptime. OEM roadmaps indicate FMCW deployment on 2027-model premium vehicles in North America and China, with production tooling already underway at several OSAT partners. These advances suggest FMCW will command an outsized share of incremental revenue growth in the automotive LiDAR market through the forecast period.

Persistent Eye-Safety Limits on Peak Power

IEC 60825-1 Class 1 rules cap maximum permissible exposure, limiting optical power for long-range roof units. Vendors, therefore, rely on larger receiver apertures, avalanche photodiodes, and advanced signal processing rather than raw transmit power. While safety guarantees protect public health, design latitude narrows and drives up cost for precision optics and thermal management. These engineering trade-offs slow the rollout of ultra-long-range products and marginally dampen the automotive LiDAR market growth outlook.

Other drivers and restraints analyzed in the detailed report include:

- UNECE R157 and China NCAP 2026 Autonomy Mandates

- Mass-Production Deals Between Tier-1s and Cloud AV Stacks

- Radar/Camera Fusion Roadmaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, ADAS accounted for 85.12% of the Automotive LiDAR Market, reflecting its mainstream adoption. Additionally, ADAS is the fastest-growing segment, with a 37.88% CAGR, driven by city-level permits and ride-hailing fleet orders. ADAS Level 3 and Level 4 programs bridge the gap: German premium OEMs already ship production Level 3 highway pilots, and Chinese mobility companies operate supervised Level 4 services in over 10 metropolitan areas. Higher autonomy levels require multiple sensors, redundancy, and full-stack validation, raising average content per vehicle and powering the next wave of the market size expansion.

Scaling to full autonomy shifts value from hardware to continuous OTA upgrades. Subscription models for highway self-driving add revenue streams that justify higher sensor bills, and data collected by Level 5 fleets feeds iterative perception improvements. As these platforms mature, they reinforce a virtuous cycle: wider data coverage supports safer algorithms, in turn unlocking permits for broader operations. This flywheel underpins bullish long-range forecasts despite early-stage volumes.

In 2025, mechanical spinning units captured 62.15% of the revenue share in the Automotive LiDAR Market, due to their proven field performance, comprehensive 360-degree coverage, and established manufacturing lines. Yet their moving parts create reliability concerns for a 10-year automotive design life, and form-factor constraints complicate stylistic integration. Solid-state approaches, including MEMS beam steering, optical phased arrays, and flash topologies, step in with fully sealed modules and lower cost trajectories. Within this solid-state cohort, FMCW is the breakout sub-category, projected at 47.46% CAGR and expected to reach double-digit share before 2031.

Valeo continues to iterate its second-generation Scala hybrid scanner, while Luminar brings high-channel-count pulsed time-of-flight into series production. Huawei and Hesai invest heavily in 905-nm pulsed and 1,550-nm FMCW pipelines, seeking to hedge technology bets across different vehicle classes. This pluralistic landscape ensures that no single architecture dominates all use cases, even as FMCW captures the performance leadership narrative.

Geography Analysis

In 2025, the Automotive LiDAR Market saw Asia-Pacific commanding a dominant revenue share of 41.75%, with China as the epicenter of sensor deployment. Provincial subsidies worth up to CNY 10,000 per L3-ready vehicle, extended through 2027, increase penetration of battery electric SUVs and sedans. Domestic supply chains spanning wafer fab to final assembly compress cost and shorten lead times, reinforcing regional dominance. South Korea and Singapore add pilot zones and smart-highway projects, further expanding regional demand. The market in Asia-Pacific is forecast to grow at a 25.9% CAGR, the highest across all regions.

Autonomous trucking corridors linking Texas, Arizona, and California, and consumer appetite for hands-free highway assist, push a 23.2% CAGR. Aurora, Ouster, and Aeva operate domestic facilities that reduce import reliance, while U.S. export control on certain 1,550 nm VCSEL epitaxy encourages local alternative suppliers. Canada's winter testing grounds add niche demand for all-weather FMCW products.

Europe follows with a 20.4% CAGR, reflecting advanced regulation and conservative consumer uptake. UNECE-based rules originate in Europe, but national type-approval processes remain stringent, slowing high-volume delivery. However, German, Swedish, and French premium brands install multi-LiDAR configurations to meet L3 highway pilot requirements, making the region an influential technology trendsetter. Smaller yet notable opportunities arise in the Gulf Cooperation Council, where smart-city mega-projects embed autonomous shuttles into new urban designs. Africa and Latin America post CAGRs of 21.3% and 19.6% respectively on lower bases, driven by mining haulage automation and public-sector fleet modernization.

- Hesai Technology (Hesai Group)

- RoboSense Technology Co., Ltd.

- Huawei Technologies Co., Ltd.

- Valeo SA

- Luminar Technologies Inc.

- Continental AG

- ZF Friedrichshafen AG

- Innoviz Technologies Ltd.

- Ouster Inc.

- Velodyne LiDAR Inc.

- Aeva Inc.

- AEye Inc.

- LeddarTech Holdings Inc.

- Seyond

- LIVOX

- Blickfeld GmbH

- SiLC Technologies Inc.

- Insight LiDAR

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid ASP decline unlocking mid-priced vehicle adoption

- 4.2.2 Early-stage FMCW LiDAR sensor breakthroughs extend detection range above 400 m

- 4.2.3 UNECE R157 and China NCAP 2026 autonomy ratings mandate higher-resolution perception

- 4.2.4 Mass-production deals between tier-1s and cloud AV stacks

- 4.2.5 Chinese provincial subsidies for L3-ready sensor suites

- 4.2.6 Automaker OTA business models monetising highway LiDAR subscriptions

- 4.3 Market Restraints

- 4.3.1 Persistent eye-safety rules limit peak power on long-range, roof-mounted units

- 4.3.2 Radar/Camera sensor fusion cost-down roadmap slows LiDAR attach-rate in sub-USD25k cars

- 4.3.3 Export-control scrutiny on 1,550 nm GaAs VCSELs restricts cross-border supply chains

- 4.3.4 Reliability concerns of dynamic beam-steering MEMS mirrors in above 10-year duty cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 LiDAR Component Ecosystem

- 4.8 Integration of LiDAR in ADAS Vehicles

- 4.9 Automotive LiDAR Technology Roadmap (2020-2030)

- 4.10 Pricing Trend Analysis

- 4.11 Porter's Five Forces

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Buyers

- 4.11.3 Bargaining Power of Suppliers

- 4.11.4 Threat of Substitutes

- 4.11.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Application

- 5.1.1 Robotic Vehicles

- 5.1.2 ADAS

- 5.1.2.1 Level 2+ / 2++

- 5.1.2.2 Level 3 / 4

- 5.1.2.3 Level 5

- 5.2 By Technology Type

- 5.2.1 Mechanical/Spinning

- 5.2.2 Solid-State (MEMS, Flash)

- 5.2.3 FMCW

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Range

- 5.4.1 Short / Mid-Range (Up to 150 m)

- 5.4.2 Long-Range (Above 150 m)

- 5.5 By Installation Position

- 5.5.1 Roof-Mounted

- 5.5.2 Grille / Bumper

- 5.5.3 Headlamp-Integrated

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Hesai Technology (Hesai Group)

- 6.4.2 RoboSense Technology Co., Ltd.

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Valeo SA

- 6.4.5 Luminar Technologies Inc.

- 6.4.6 Continental AG

- 6.4.7 ZF Friedrichshafen AG

- 6.4.8 Innoviz Technologies Ltd.

- 6.4.9 Ouster Inc.

- 6.4.10 Velodyne LiDAR Inc.

- 6.4.11 Aeva Inc.

- 6.4.12 AEye Inc.

- 6.4.13 LeddarTech Holdings Inc.

- 6.4.14 Seyond

- 6.4.15 LIVOX

- 6.4.16 Blickfeld GmbH

- 6.4.17 SiLC Technologies Inc.

- 6.4.18 Insight LiDAR

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

LiDAR晶片市場預測至2034年-全球LiDAR類型、晶片類型、波長、應用、最終用戶和地區分析

LiDAR晶片市場預測至2034年-全球LiDAR類型、晶片類型、波長、應用、最終用戶和地區分析 汽車LiDAR市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、技術、範圍、車輛類型、地區和競爭格局分類,2021-2031年

汽車LiDAR市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、技術、範圍、車輛類型、地區和競爭格局分類,2021-2031年 汽車LiDAR感測器市場機會、成長要素、產業趨勢分析及2026-2035年預測

汽車LiDAR感測器市場機會、成長要素、產業趨勢分析及2026-2035年預測 汽車LiDAR感測器市場:按組件、偵測範圍、LiDAR類型、應用、車輛類型和銷售管道分類-2026-2032年全球市場預測汽車LiDAR系統晶片市場:2026-2032年全球市場預測(依LiDAR技術、推進方式、偵測範圍、感知方式、應用及車輛類型分類)

汽車LiDAR感測器市場:按組件、偵測範圍、LiDAR類型、應用、車輛類型和銷售管道分類-2026-2032年全球市場預測汽車LiDAR系統晶片市場:2026-2032年全球市場預測(依LiDAR技術、推進方式、偵測範圍、感知方式、應用及車輛類型分類) 2026年全球汽車LiDAR市場報告

2026年全球汽車LiDAR市場報告 北美汽車專利演變策略分析:1976-2025年

北美汽車專利演變策略分析:1976-2025年 針對自動駕駛汽車的4D雷射雷達市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、部署類型、最終用戶、功能、安裝類型和解決方案分類汽車LiDAR感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、應用、技術、影像類型、位置、地區和競爭格局分類,2021-2031年)

針對自動駕駛汽車的4D雷射雷達市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、部署類型、最終用戶、功能、安裝類型和解決方案分類汽車LiDAR感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、應用、技術、影像類型、位置、地區和競爭格局分類,2021-2031年) 全球汽車雷射雷達市場:依技術類型、成像類型、內燃機車輛類型、檢測範圍、自動駕駛等級、電動車類型和地區劃分-市場規模、產業趨勢、機會分析和預測(2026-2035 年)

全球汽車雷射雷達市場:依技術類型、成像類型、內燃機車輛類型、檢測範圍、自動駕駛等級、電動車類型和地區劃分-市場規模、產業趨勢、機會分析和預測(2026-2035 年)