|

市場調查報告書

商品編碼

2066603

熱處理鋼板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Heat-treated Steel Plates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

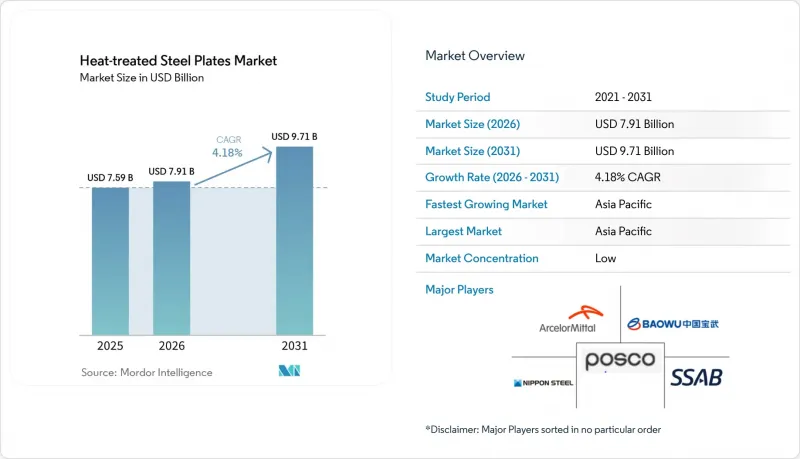

根據 Mordor Intelligence 預測,熱處理鋼板的市場規模預計將從 2025 年的 75.9 億美元成長到 2026 年的 79.1 億美元,並將從 2026 年到 2031 年以 4.18% 的複合年成長率成長,到 2031 億美元達到 97.1 億美元。

本報告按鋼材類型(碳鋼、合金鋼、不銹鋼)、熱處理類型(退火、回火等)、最終用途行業(汽車和重型機械、建築等)以及地區(北美、南美、歐洲、中東和非洲、亞太地區)進行細分。市場預測以美元計價。

全球熱處理鋼板市場趨勢及洞察

離岸風力發電的單樁基礎正在推動市場需求。

用於15兆瓦級風力發電機的單樁基礎直徑正擴大至11米,壁厚增至150毫米,這推動了對符合DNV斷裂韌性標準的正火或TMCP鋼板的需求。台灣中鋼集團獲得了一份為期五年的訂單,將採購18萬噸S355G10+N鋼板,該鋼板在-20 度C下的夏比衝擊韌性為100焦耳,用於緩解颱風引起的脆性斷裂,預計將於2025年交付。 2024年,迪林格(Dillinger)和沃旭能源(Orsted)達成協議,將共同開發一種採用淬火回火S690QL鋼板的12公尺單樁基礎,這將使每兆瓦的鋼材用量減少18%,並降低安裝成本。全球風力發電理事會(GWEC)預測,到2030年,新增離岸風力發電裝置容量將達到110吉瓦,如果單樁基礎維持65%的市場佔有率,這將需要約800萬噸鋼板。據估計,每1吉瓦離岸風力發電需要消耗7萬噸厚鋼板,凸顯了該產業對熱處理能力的巨大需求。

無人礦用卡車的貨廂採用耐磨鋼板。

由於自動駕駛運輸卡車全天候運作,襯板磨損日益加劇,導致對布氏硬度500的鋼板需求增加,這種鋼板可將更換週期從8000小時延長至14000小時。 SSAB公司將於2025年推出的「Hardox 500 Tuf」鋼板,其夏比衝擊韌性高達45J,即使220噸的重物衝擊卡車貨廂,也能有效防止裂紋擴展。 JFE公司將於2024年推出的「EVERHARD 450」鋼板,透過添加微量磷合金元素,減少了淬火變形,並允許在無需預熱的情況下進行雷射切割。根據奧斯汀工程公司的報告顯示,2025年自動駕駛汽車的訂單將成長32%,其中耐磨鋼板將佔材料成本的68%。力拓集團皮爾巴拉地區營運的 220 輛小松 930E 卡車透過改用 Hardox 襯裡,減少了 22% 的維護停機時間。

在下一代施工機械中,複合材料將取代耐磨鋼板。

到2025年,超高分子量聚乙烯(UHMWPE)襯裡與玄武岩纖維黏合,將佔卡車貨箱維修的18%,重量減輕40%,並消除焊接飛濺導致的疲勞裂紋。Caterpillar794 AC卡車於2024年推出,其複合材料貨箱的耐磨性相當於布氏硬度400,使用壽命延長至16,000小時。 2025年,小松公司推出了碳纖維增強鏟鬥邊緣,使鏟鬥重量減輕35%,油耗降低2.1%。沃爾沃建築設備公司透露,到2025年,複合材料起重機複合材料耐磨件的成本佔比將從2023年的4%提高到12%。布魯斯岩石工程公司已證明,改用UHMWPE襯裡可在三年內為每輛車節省31,000美元,加速了成本敏感型礦山對UHMWPE襯裡的採用。

細分市場分析

2025年,碳鋼佔熱處理鋼板市場的45.58%,但隨著雙相不銹鋼和馬氏體鋼在電解槽和海底管線領域的應用日益廣泛,預計到2031年,合金鋼市場將以5.05%的複合年成長率成長。受歐盟綠氫能計畫推動,雙相不銹鋼,特別是EN 1.4462標準,在2025年約佔合金鋼總噸位的8%。不銹鋼板材目前仍屬於小眾市場,但在低溫和製藥應用領域至關重要,因此其價格溢價足以彌補銷售量上的不足。

成本差異解釋了碳鋼的耐用性。 S355 的正火價格約為每噸 650 美元,而雙相鋼的價格約為每噸 2400 美元。儘管如此,諸如安賽樂米塔爾的 Usibor 2000 冷壓硬化鋼(抗張強度達 2000 MPa,適用於電動汽車電池機殼)和浦項製鐵的 PosMAC(耐海洋腐蝕性能是鍍鋅產品的 10 倍)等創新合金配方正在擴大其市場佔有率。日本製鐵的 NSGP1 正火合金在 -60 度C 的低溫下仍能達到夏比衝擊韌性標準,適用於北極海上鑽油平臺,進一步拓展了高規格合金鋼板的應用領域。

區域分析

預計到2025年,亞太地區將佔全球銷售額的52.95%,並在2031年之前以5.74%的年均成長率成長,這主要得益於中國風力發電機供應鏈、印度基礎設施建設規劃以及東南亞造船業的蓬勃發展。中國2025年粗鋼產量將達到約5.8億噸,其中熱處理鋼約佔1.8%,顯示中國在轉型為高附加價值產品方面擁有巨大空間。印度耗資111兆盧比(約1.3兆美元)的國家基礎設施計畫預計將為JSW和塔塔集團新增220萬噸鋼板產能。

儘管歐洲在市場佔有率上落後,但在利潤豐厚的雙相鋼生產領域卻佔據主導地位。 H2 Green Steel位於博登的工廠計劃於2026年投產,屆時將每年供應50萬噸不含石化燃料的鋼板,目標客戶是願意為每噸支付50至80歐元綠色溢價的消費者。德國蒂森克虜伯公司正在共同開發氫直接還原鐵(DRI),而英國的離岸風力發電項目,例如多格爾灘項目,預計將在2026年至2031年間消耗120萬噸正火和熱機械腐蝕(TMCP)鋼板。

在北美,強制性抗震準備措施和液化天然氣(LNG)的成長將為東海岸的建築商和墨西哥灣沿岸的能源發電廠新增30萬噸產能,這得益於紐柯公司(Nucor)新建的標準化生產線。以沙烏地阿拉伯的NEOM新城、海水淡化和石化計畫為中心的中東地區,預計到2031年鋼鐵消費量將以每年6.2%的速度成長。以巴西和阿根廷為首的南美洲,正受惠於鋰礦開採和農業機械生產,而浦項鋼鐵(POSCO)正在興建的氫氧化鋰工廠需要雙相鋼壓力容器。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 離岸風力發電的單樁基礎正在推動市場需求。

- 自動駕駛礦用卡車車身使用的耐磨板

- 符合新建築規範的標準化抗震板材。

- 歐洲用於綠氫電解槽的雙相不銹鋼板

- 利用熱處理鋼板設計輕型貨船

- 市場限制因素

- 複合材料可取代下一代土木工程和施工機械中的耐磨板

- 能源價格波動導致反應爐運轉率下降。

- 反應爐氮氧化物和二氧化碳排放的更嚴格限制將增加合規成本。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 鋼型

- 碳鋼

- 合金鋼

- 不銹鋼

- 熱處理類型

- 退火

- 回火

- 正常化

- 熱機械控制過程(TMCP)

- 硬化

- 按最終用途行業分類

- 汽車和重型機械

- 建築/施工

- 造船和海洋工程結構

- 能源與電力(石油、天然氣、可再生能源)

- 其他(金屬加工、運輸)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 土耳其

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ArcelorMittal

- Baosteel Co.,Ltd.

- China Ansteel Group Corporation Limited

- China BaoWu Steel Group Corporation Limited

- Dillinger Hutte Saarstahl AG

- Essar

- Hyundai Steel

- JFE Steel Corporation

- JSW Steel Ltd.

- Nippon Steel Corporation

- Nucor Corporation

- POSCO

- SSAB AB

- thyssenkrupp Steel Europe

- Voestalpine AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the heat-treated steel plates market size is expected to grow from USD 7.59 billion in 2025 to USD 7.91 billion in 2026 and is forecast to reach USD 9.71 billion by 2031 at 4.18% CAGR over 2026-2031.

This report is Segmented by Steel Type (Carbon Steel, Alloy Steel, and Stainless Steel), Heat-Treatment Type (Annealing, Tempering, and More), End-Use Sector (Automotive and Heavy Machinery, Building and Construction, and More), and Geography (North America, South America, Europe, Middle East and Africa, Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Global Heat-treated Steel Plates Market Trends and Insights

Offshore-Wind Monopile Foundations Driving Demand

Monopile diameters have climbed to 11 m and wall thicknesses to 150 mm for 15-MW turbines, pushing demand for normalized or TMCP plate that meets DNV fracture-toughness rules. Taiwan's China Steel Corporation secured a 5-year order for 180,000 tons of S355G10+N plate in 2025, specifying 100 J Charpy toughness at -20 °C to mitigate typhoon-induced brittle fracture. Dillinger and Orsted agreed in 2024 to co-develop 12-m monopiles using quenched-and-tempered S690QL, reducing steel weight per MW by 18% and cutting installation costs. The Global Wind Energy Council foresees 110 GW of new offshore capacity by 2030, equal to about 8 million tons of plate if monopiles keep a 65% share. Each GW of offshore wind consumes an estimated 70,000 tons of heavy plate, underlining the sector's pull on heat-treatment capacity.

Abrasion-Resistant Plates Adopted in Autonomous Mining Truck Bodies

Autonomous haul trucks run 24 h per day, intensifying liner wear and raising demand for 500-Brinell quenched plate that stretches replacement cycles from 8,000 h to 14,000 h. SSAB's Hardox 500 Tuf, launched in 2025, delivers 45-J Charpy toughness, avoiding crack propagation when 220-t payloads strike the bed. JFE's EVERHARD 450 debuted in 2024 with phosphorus micro-alloying that cuts quenching distortion and lets users laser-cut without preheating. Austin Engineering reported a 32% jump in autonomous-fleet orders in 2025, with abrasion-resistant plate making up 68% of material spend. Rio Tinto's Pilbara fleet of 220 Komatsu 930E trucks switched to Hardox liners and reduced maintenance downtime by 22%.

Composites Replacing Wear Plate in Next-Generation Earth-Moving Equipment

Ultra-high-molecular-weight polyethylene liners bonded to basalt fiber captured 18% of haul-truck bed retrofits in 2025, lowering weight by 40% and eliminating weld spatter that seeds fatigue cracks. Caterpillar's 794 AC truck, launched in 2024, offers composite beds rated to 400-Brinell equivalent abrasion resistance and extends life to 16,000 h. Komatsu introduced a carbon-fiber reinforced bucket edge in 2025 that trims tip weight by 35% and cuts fuel burn by 2.1%. Volvo Construction Equipment disclosed that composite wear parts climbed to 12% of its articulated-hauler material spend in 2025, up from 4% in 2023. Bruce Rock Engineering demonstrated a USD 31,000 three-year savings per truck when switching to UHMWPE liners, accelerating adoption in cost-focused mines.

Other drivers and restraints analyzed in the detailed report include:

- Seismic-Resilient Normalized Plate Mandated by New Building Codes

- Duplex Stainless Plates for Green-Hydrogen Electrolyzer Pressure Vessels

- Energy-Price Volatility Reducing Furnace Utilization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The carbon steel accounted for 45.58% of the heat-treated steel plates market share in 2025, while alloy steel is forecast to expand at a 5.05% CAGR to 2031 as duplex stainless and martensitic grades penetrate electrolyzer vessels and subsea lines. Duplex stainless, notably EN 1.4462, covered about 8% of alloy tonnage in 2025, propelled by EU green-hydrogen projects. Stainless plate stays niche but essential in cryogenic and pharmaceutical uses, commanding price premiums that offset lower volume.

Cost differentials explain carbon steel's resilience-S355 normalized sells near USD 650/ton, versus duplex plate at roughly USD 2,400/ton. Even so, alloy formulations gain ground through innovations such as ArcelorMittal's Usibor 2000 press-hardening steel, which enables 2,000-MPa tensile strength for EV battery enclosures, and POSCO's PosMAC, which offers tenfold marine corrosion resistance relative to galvanized alternatives. Nippon Steel's NSGP1 normalized alloy meets -60 °C Charpy toughness for Arctic offshore rigs, further widening the addressable field for high-specification alloy plates.

Geography Analysis

Asia-Pacific held 52.95% of global revenue in 2025 and is forecast to grow at 5.74% through 2031, driven by Chinese wind-turbine supply chains, India's infrastructure pipeline, and Southeast Asian shipbuilding. China produced around 580 million tons of crude steel in 2025, with heat-treated variants accounting for close to 1.8%, indicating ample headroom for value-added migration. India's National Infrastructure Pipeline, worth INR 111 trillion (USD 1.3 trillion), is triggering 2.2 million tons of fresh plate capacity from JSW and Tata.

Europe trails in share but leads on margin-rich duplex output. H2 Green Steel's Boden mill, coming online in 2026, will supply 500,000 tons of fossil-free plate annually, aiming at users willing to pay EUR 50-80/ton green premiums. Germany's thyssenkrupp is co-developing hydrogen DRI, and UK offshore wind projects such as Dogger Bank are set to consume 1.2 million tons of normalized and TMCP plate from 2026 to 2031.

North America combines seismic mandates and LNG growth. Nucor's new normalizing line adds 300,000 tons of capacity for East Coast builders and Gulf Coast energy plants. The Middle East pivots on Saudi Arabia's NEOM, desalination, and petrochemical projects, anticipating a 6.2% annual steel-consumption rise to 2031. South America, led by Brazil and Argentina, benefits from lithium mining and farm-equipment production, with POSCO building a lithium-hydroxide plant requiring duplex pressure vessels.

- ArcelorMittal

- Baosteel Co.,Ltd.

- China Ansteel Group Corporation Limited

- China BaoWu Steel Group Corporation Limited

- Dillinger Hutte Saarstahl AG

- Essar

- Hyundai Steel

- JFE Steel Corporation

- JSW Steel Ltd.

- Nippon Steel Corporation

- Nucor Corporation

- POSCO

- SSAB AB

- thyssenkrupp Steel Europe

- Voestalpine AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Offshore-wind monopile foundations driving demand

- 4.2.2 Abrasion-resistant plates adopted in autonomous mining truck bodies

- 4.2.3 Seismic-resilient normalized plate mandated by new building codes

- 4.2.4 Duplex stainless plates for green-hydrogen electrolyzer pressure vessels in Europe

- 4.2.5 Lightweight cargo-ship designs utilising heat treated steel plate

- 4.3 Market Restraints

- 4.3.1 Composites replacing wear plate in next-gen earth-moving equipment

- 4.3.2 Energy-price volatility reducing furnace utilisation

- 4.3.3 Stricter NOx/CO2 furnace-emission caps raising compliance cost

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Steel Type

- 5.1.1 Carbon Steel

- 5.1.2 Alloy Steel

- 5.1.3 Stainless Steel

- 5.2 By Heat-Treatment Type

- 5.2.1 Annealing

- 5.2.2 Tempering

- 5.2.3 Normalizing

- 5.2.4 Thermo-Mechanical Controlled Process (TMCP)

- 5.2.5 Quenching

- 5.3 By End-Use Sector

- 5.3.1 Automotive and Heavy Machinery

- 5.3.2 Building and Construction

- 5.3.3 Shipbuilding and Offshore Structures

- 5.3.4 Energy and Power (Oil, Gas, Renewables)

- 5.3.5 Others (Metalworking, Transportation)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Russia

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Egypt

- 5.4.5.5 South Africa

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 Baosteel Co.,Ltd.

- 6.4.3 China Ansteel Group Corporation Limited

- 6.4.4 China BaoWu Steel Group Corporation Limited

- 6.4.5 Dillinger Hutte Saarstahl AG

- 6.4.6 Essar

- 6.4.7 Hyundai Steel

- 6.4.8 JFE Steel Corporation

- 6.4.9 JSW Steel Ltd.

- 6.4.10 Nippon Steel Corporation

- 6.4.11 Nucor Corporation

- 6.4.12 POSCO

- 6.4.13 SSAB AB

- 6.4.14 thyssenkrupp Steel Europe

- 6.4.15 Voestalpine AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

鋼板市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局(2021-2031年)

鋼板市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局(2021-2031年) 扁鋼市場:2026-2032年全球市場預測(依產品類型、形狀、材質、厚度、最終用途產業及分銷通路分類)熱處理鋼板市場:2026-2032年全球市場預測(依鋼材類型、厚度、加工方法、應用、最終用途及通路分類)

扁鋼市場:2026-2032年全球市場預測(依產品類型、形狀、材質、厚度、最終用途產業及分銷通路分類)熱處理鋼板市場:2026-2032年全球市場預測(依鋼材類型、厚度、加工方法、應用、最終用途及通路分類) 扁鋼市場規模、佔有率、趨勢及預測(依產品、材質、應用及地區分類),2026-2034年

扁鋼市場規模、佔有率、趨勢及預測(依產品、材質、應用及地區分類),2026-2034年 2026年全球扁鋼市場報告2026年全球熱處理鋼市場報告全球耐磨堆焊鋼板市場(依材質類型、製程類型、焊接技術、塗層厚度、最終用途產業和應用分類)-2026-2032年預測按木材類型、處理方法、用途和通路分類的熱處理木材市場-2026年至2032年全球預測按連接方式、材料組合、應用、通路和最終用途產業分類的複合鋼板市場-2026年至2032年全球預測碳化矽耐磨板市場:依製造流程、終端應用產業及通路分類-2026-2032年全球預測

2026年全球扁鋼市場報告2026年全球熱處理鋼市場報告全球耐磨堆焊鋼板市場(依材質類型、製程類型、焊接技術、塗層厚度、最終用途產業和應用分類)-2026-2032年預測按木材類型、處理方法、用途和通路分類的熱處理木材市場-2026年至2032年全球預測按連接方式、材料組合、應用、通路和最終用途產業分類的複合鋼板市場-2026年至2032年全球預測碳化矽耐磨板市場:依製造流程、終端應用產業及通路分類-2026-2032年全球預測