|

市場調查報告書

商品編碼

2066600

英國資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United Kingdom Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

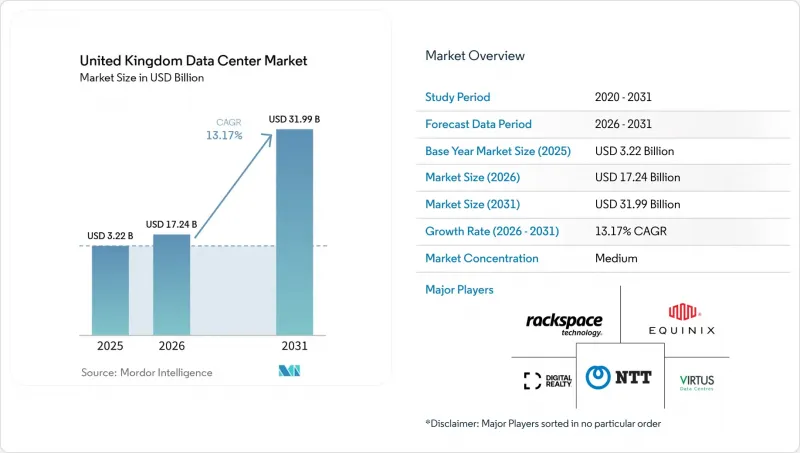

據 Mordor Intelligence 稱,英國資料中心市場在 2025 年的價值為 152.3 億美元,預計到 2031 年將達到 319.9 億美元,而 2026 年為 172.4 億美元,預測期(2026-2031 年)的複合成長率為 13.17%。

本報告按資料中心規模(小規模、中型、大型、超大型)、層級(Tier 1 和 Tier 2、Tier 3、Tier 4)、資料中心類型(超大規模/本地部署、企業/邊緣、託管)、最終用戶(銀行、金融服務和保險 (BFSI)、IT 和 ITES、電子商務、政府、製造業、媒體和娛樂、其他)以及其他熱點。市場預測以 IT 負載容量 (MW) 為單位。

英國資料中心市場的趨勢與洞察

對超大規模雲端運算和人工智慧運算的需求激增。

隨著人工智慧訓練工作負載向專用園區轉移,超大規模營運商正在推動機架功率密度的結構性成長。亞馬遜到2028年投資80億英鎊(107.3億美元)的項目、微軟的多區域設施擴建以及谷歌的水冷叢集部署,將在總合內新增超過1吉瓦的容量。如今,設施設計方案中明確規定採用100-150千瓦的機架、晶片直接液冷迴路以及現場燃氣渦輪機,以避免耗時數年的電網連接。因此,英國資料中心市場正在推動資本流入深度科技領域,創造就業機會,並促進開關設備、冷卻器和模組化發電廠等供應鏈的在地化。

英國5G和邊緣運算的發展

5G在全國的推廣應用,推動了對分散式處理需求的成長,而中小型邊緣節點能夠以低於10毫秒的延遲滿足這項需求。沃達豐曼徹斯特邊緣實驗室和英國電信波長聯盟正在為通訊業者提供一種可在整個都市區複製的參考架構。在物流和製造業領域部署私有5G網路的公司,目前正在園區內建置微型資料中心,從而拓展了英國資料中心市場中10兆瓦以下的細分市場,以支援物聯網分析和擴增實境驅動的維護。

倫敦可用區電網連接出現延誤

英國國家電網公司警告稱,到2035年,倫敦資料中心的電力需求可能達到6吉瓦,但產能擴張滯後,導致已承諾的建設項目延期數年。因此,開發商正在考慮在用戶側燃氣渦輪機和電池能源儲存系統,同時也在探索輸電能力充足的北部位置。

細分市場分析

預計到2025年,大型資料中心將佔據英國資料中心市場佔有率的37.05%,這主要得益於雲端區域和大型企業導向的多租戶託管機房。該細分市場憑藉著成熟的光纖線路、成熟的營運團隊和一體化的互聯生態系統,維持著規模經濟效益。然而,隨著人工智慧工作負載需要連續的場地和能夠提供400千伏電壓的現場變電站,預計到2031年,容量超過250兆瓦的超大型園區計畫將以31.45%的複合年成長率(CAGR)實現最高成長。預計到2031年,英國超大型園區資料中心市場規模將超過6140兆瓦,這反映出投資者正在尋求與超大規模租戶簽訂長期契約,從而推動了戰略轉型。

如今,大型資料中心的設計採用模組化機房、液冷歧管和屋頂乾式冷卻器,取代了耗水量龐大的塔式冷卻系統。這些項目受益於設備採購和購電協議 (PPA) 的規模經濟,通常會協商簽訂 15 年的再生能源購電協議以穩定營運成本。相較之下,中小型資料中心則服務於邊緣應用和受監管的特定市場,這些市場需要接近性用戶,從而佔據了英國資料中心市場中穩定但成長較慢的需求細分領域。

到2025年,Tier 3將佔據英國資料中心市場佔有率的77.92%,構成核心託管服務的基礎,從而實現高冗餘度和具成本效益的並發維護。然而,超大規模人工智慧訓練、高頻交易和受監管工作負載正在增強Tier 4的商業價值。預計到2031年,英國資料中心市場中Tier 4的容量將從2026年的892兆瓦成長到3,474兆瓦,複合年成長率(CAGR)為31.25%。

Tier 4 的實施依賴於完全獨立的雙電源路徑、容錯冷卻系統以及保證 99.995%運轉率的服務等級協定 (SLA),從而最大限度地減少因人工智慧模型重新訓練或財務訂單延誤而導致的每小時數百萬美元的停機成本。營運商正在積極升級 Tier 3 資料中心機房,增加 UPS 串和循環式冷水系統,以彌補維修缺口,同時維持現有資本投資。這一趨勢在倫敦正在加速發展,因為監管機構已將倫敦的資料中心指定為“關鍵國家基礎設施”,關鍵任務型租戶需要最高級別的網路安全和營運彈性保障。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義 - 研究範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對超大規模雲端運算和人工智慧運算的需求激增。

- 英國5G和邊緣運算的發展

- 擴大混合IT在銀行、金融服務和保險(BFSI)及企業領域的應用。

- 政府對數位基礎設施的支持措施和國家規劃框架

- 英國。

- 將英格蘭北部的前工業園區改造為人工智慧賦能型園區

- 市場限制因素

- 倫敦可用區電網連線延遲

- 建築和能源成本不斷上漲

- 嚴格的永續發展和碳減排法規

- 倫敦以外地區液冷和高密度運作領域技術純熟勞工短缺

- 市場展望

- IT處理能力

- 高架空間

- 託管收入

- 已安裝機架

- 機架空間利用率

- 海底電纜

- 主要行業趨勢

- 智慧型手機用戶

- 每部智慧型手機的資料通訊

- 行動資料通訊速度

- 寬頻資料通訊速度

- 光纖網路

- 法律規範

- 大倫敦地區

- 英國其他地區

- 價值鍊和通路分析

- 波特五力分析

第5章 市場規模及成長預測(兆瓦)

- 按資料中心規模

- 小規模

- 中等的

- 大規模

- 百萬

- 大規模

- 層級特定

- 一級和二級

- 三級

- 第四級

- 依資料中心類型

- 超大規模/自建

- 企業/邊緣運算

- 搭配

- 未使用的

- 用過的

- 零售共址

- 批發託管

- 最終用戶

- BFSI

- 資訊科技與資訊科技服務

- 電子商務

- 政府

- 製造業

- 媒體與娛樂

- 溝通

- 其他最終用戶

- 透過熱點

- 大倫敦地區

- 英國其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Digital Realty Trust Inc.

- Equinix, Inc.

- VIRTUS Data Centres Ltd(ST Telemedia Global Data Centres)

- IBM Corporation

- Ark Data Centres

- Vantage Data Centers Management Company, LLC

- NTT Corporation

- CyrusOne LLC

- Redcentric Data Centres

- Rackspace Technology Inc.

- Green Mountain AS

- Global Switch Holdings Limited

- Amazon Web Services, Inc.

- Telehouse International Corporation of Europe Ltd

- Oracle Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom data center market size was valued at USD 15.23 billion in 2025 and estimated to grow from USD 17.24 billion in 2026 to reach USD 31.99 billion by 2031, at a CAGR of 13.17% during the forecast period (2026-2031).

This report is Segmented by Data Center Size (Small, Medium, Large, Mega, and Massive), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

United Kingdom Data Center Market Trends and Insights

Surge in hyperscale cloud and AI compute demand

Hyperscale operators drive a structural uplift in rack power density as AI training workloads migrate into purpose-built campuses. Amazon's GBP 8 billion (USD 10.73 billion) program through 2028, Microsoft's multi-region estate expansion, and Google's liquid-cooled cluster roll-outs collectively add more than 1 GW of near-term capacity. Facility blueprints now specify 100-150 kW racks, direct-to-chip liquid loops, and on-site gas turbines to bypass multi-year grid queues The United Kingdom data center market therefore absorbs deep-tech capital inflows, job creation, and supply-chain localization across switchgear, chillers, and modular power plants.

Growth of 5G and edge computing across the United Kingdom

Nationwide 5G coverage stimulates distributed processing needs that small and medium edge nodes satisfy within a 10 ms latency envelope. Vodafone's Manchester Edge Lab and BT's Wavelength alliance furnish reference architectures that operators replicate across urban corridors. Enterprises deploying private 5G in logistics and manufacturing now co-locate micro-data rooms inside campuses, spurring a sub-10 MW segment of the United Kingdom data center market serving IoT analytics and AR-enabled maintenance

Power-grid connection delays in London availability zones

National Grid warns that London data center demand could reach 6 GW by 2035, yet capacity expansions lag, adding multi-year delays to already committed builds. Developers therefore weigh behind-the-meter gas turbines and battery energy-storage systems while scoping northern sites with spare transmission headroom

Other drivers and restraints analyzed in the detailed report include:

- Rising adoption of hybrid IT among BFSI and enterprise segments

- Government incentives for digital infrastructure and the National Planning Framework

- Escalating construction and energy costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Massive facilities dominated with 37.05% United Kingdom data center market share in 2025 on the back of multi-tenant colocation halls catering to cloud regions and large enterprises. The segment maintains scale advantages through established fiber routes, mature operations teams, and embedded cross-connect ecosystems. However, mega-campus projects exceeding 250 MW are projected to capture the highest 31.45% CAGR to 2031 as AI workloads necessitate contiguous plots and on-site substations capable of delivering 400 kV feeds. The United Kingdom data center market size for mega campuses is forecast to surpass 6,140 MW by 2031, reflecting strategic pivots by investors seeking long-duration contracts with hyperscale tenants.

Mega-campus design typologies now feature modular power rooms, liquid-cooling manifolds, and roof-mounted dry-coolers that displace water-intensive towers. These projects benefit from economies of scale in equipment procurement and power-purchase agreements, often negotiating 15-year renewable PPAs that stabilize operating costs. In contrast, small and medium data centers align with edge applications and regulatory niches that demand geographic proximity to users, capturing resilient albeit slower-growing demand pockets within the broader United Kingdom data center market.

Tier 3 accounted for 77.92% United Kingdom data center market share in 2025, underpinning the core colocation offer of concurrent maintainability at a cost-effective redundancy level. Nevertheless, hyperscale AI training, high-frequency trading, and regulated workloads elevate the business case for Tier 4. The United Kingdom data center market size attributable to Tier 4 is set to expand from 892 MW in 2026 to 3,474 MW by 2031, reflecting a 31.25% CAGR.

Tier 4 adoption hinges on fully independent dual power paths, fault-tolerant cooling, and 99.995% uptime SLAs that minimize downtime costs measured in millions per hour for AI model retraining or financial order-book slippage. Operators proactively retrofit Tier 3 halls with additional UPS strings and looped chilled-water rings to bridge the redundancy gap while preserving sunk capex. London's regulatory recognition of data centers as Critical National Infrastructure accelerates this trend, as mission-critical tenants demand the highest assurance levels for cybersecurity and operational resilience.

List of Companies Covered in this Report:

- Digital Realty Trust Inc.

- Equinix, Inc.

- VIRTUS Data Centres Ltd (ST Telemedia Global Data Centres)

- IBM Corporation

- Ark Data Centres

- Vantage Data Centers Management Company, LLC

- NTT Corporation

- CyrusOne LLC

- Redcentric Data Centres

- Rackspace Technology Inc.

- Green Mountain AS

- Global Switch Holdings Limited

- Amazon Web Services, Inc.

- Telehouse International Corporation of Europe Ltd

- Oracle Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition - Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in hyperscale cloud and AI compute demand

- 4.2.2 Growth of 5G and edge computing across the United Kingdom

- 4.2.3 Rising adoption of hybrid IT among BFSI and enterprise segments

- 4.2.4 Government incentives for digital infrastructure and the National Planning Framework

- 4.2.5 Proliferation of new submarine-cable landings on the United Kingdom east coast

- 4.2.6 Repurposing of legacy industrial estates into AI-ready campuses in northern England

- 4.3 Market Restraints

- 4.3.1 Power-grid connection delays in London availability zones

- 4.3.2 Escalating construction and energy costs

- 4.3.3 Stringent sustainability and carbon-reduction regulations

- 4.3.4 Skilled-labour shortage for liquid-cooling and high-density operations outside London

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.5.6.1 Greater London

- 4.5.6.2 Rest of United Kingdom

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

- 5.1 By Data Center Size

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

- 5.1.4 Mega

- 5.1.5 Massive

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale / Self-built

- 5.3.2 Enterprise / Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Hotspot

- 5.5.1 Greater London

- 5.5.2 Rest of United Kingdom

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Digital Realty Trust Inc.

- 6.4.2 Equinix, Inc.

- 6.4.3 VIRTUS Data Centres Ltd (ST Telemedia Global Data Centres)

- 6.4.4 IBM Corporation

- 6.4.5 Ark Data Centres

- 6.4.6 Vantage Data Centers Management Company, LLC

- 6.4.7 NTT Corporation

- 6.4.8 CyrusOne LLC

- 6.4.9 Redcentric Data Centres

- 6.4.10 Rackspace Technology Inc.

- 6.4.11 Green Mountain AS

- 6.4.12 Global Switch Holdings Limited

- 6.4.13 Amazon Web Services, Inc.

- 6.4.14 Telehouse International Corporation of Europe Ltd

- 6.4.15 Oracle Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球資料中心市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料中心市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 資料中心基礎設施管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、部署類型、垂直市場、地區和競爭對手分類,2021-2031 年資料中心市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、密度、最終用戶、地區和競爭格局分類,2021-2031年

資料中心基礎設施管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、部署類型、垂直市場、地區和競爭對手分類,2021-2031 年資料中心市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、密度、最終用戶、地區和競爭格局分類,2021-2031年 2026年全球水下資料中心市場報告

2026年全球水下資料中心市場報告 資料中心測試市場規模、佔有率和趨勢分析報告:按服務類型、部署模式、最終用途、地區和細分市場預測(2026-2033 年)2026年全球光纖連接服務工具市場報告2026年全球行動雙倍數據速率(DDR)市場報告

資料中心測試市場規模、佔有率和趨勢分析報告:按服務類型、部署模式、最終用途、地區和細分市場預測(2026-2033 年)2026年全球光纖連接服務工具市場報告2026年全球行動雙倍數據速率(DDR)市場報告 永續資料中心市場預測至2034年-全球分析(按組件、資料中心類型、容量、部署模式、永續發展舉措、冷卻技術、最終用戶和地區分類)

永續資料中心市場預測至2034年-全球分析(按組件、資料中心類型、容量、部署模式、永續發展舉措、冷卻技術、最終用戶和地區分類) 資料中心基礎設施管理 (DCIM) 軟體市場:全球和區域分析:按產品、應用和國家分類 - 分析和預測 (2026–2036)美國資料中心市場規模、佔有率和趨勢分析報告:按組件、類型、伺服器機架密度、冗餘、PUE、設計、層級、企業規模、最終用途和細分市場進行預測(2026-2033 年)

資料中心基礎設施管理 (DCIM) 軟體市場:全球和區域分析:按產品、應用和國家分類 - 分析和預測 (2026–2036)美國資料中心市場規模、佔有率和趨勢分析報告:按組件、類型、伺服器機架密度、冗餘、PUE、設計、層級、企業規模、最終用途和細分市場進行預測(2026-2033 年)