|

市場調查報告書

商品編碼

2066598

隱私管理軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Privacy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

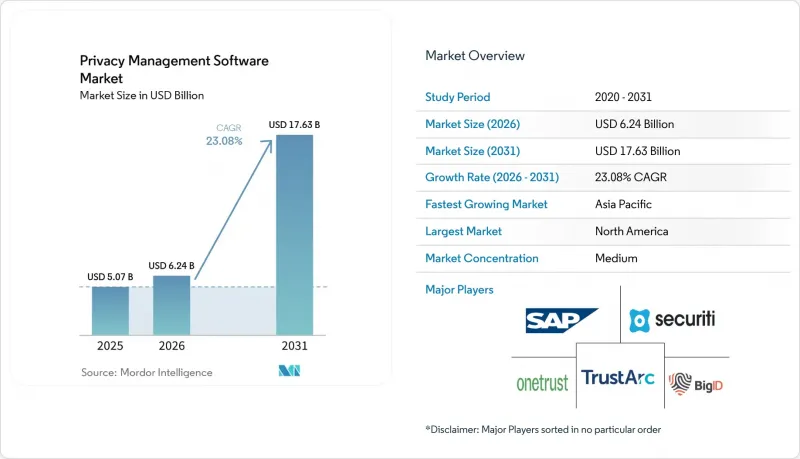

根據 Mordor Intelligence 預測,隱私管理軟體市場規模將從 2025 年的 50.7 億美元成長到 2026 年的 62.4 億美元,然後在 2031 年達到 176.3 億美元,2026 年至 2031 年的複合年成長率為 23.08%。

本報告按組件(解決方案、服務)、部署類型(本地部署等)、組織規模(中小企業等)、功能(同意和偏好管理等)、最終用戶行業(銀行、金融服務和保險、醫療保健和生命科學等)以及地區進行細分。所有細分市場的規模和預測均以美元計價。

全球隱私管理軟體市場趨勢與洞察

全球隱私法規的加強正在促進市場擴張。

隨著資料保護法律的不斷完善,管治藍圖也在進行重組。印度的《2023年數位個人資料保護法》收緊了資料儲存和跨國資料傳輸的監管,強制要求企業部署能夠同時協調多個監管工作流程的平台。巴西和一些非洲國家也正在效仿,跨國公司越來越傾向於選擇能夠透過一次更新就將監管變化反映到其所有業務部門的解決方案。監管機構的關注點也從個人資料權利擴展到演算法透明度,這增加了對能夠根據傳統隱私實踐監控人工智慧流程活動的整合軟體的需求。

雲端運算和SaaS交付模式正在改變市場動態。

雲端原生部署滿足了企業對快速法規更新、跨境效能和彈性擴展的需求。預計到 2024 年,雲端原生部署的市場佔有率將達到 67%,雲端採用已不再只是一種選擇,而是一種標準做法。共用的合規基礎設施降低了准入門檻,並可在法律法規變更時立即提供新的管理功能。然而,對雲端的依賴迫使企業考慮主權限制。因此,在資料本地化法律要求在國內進行處理,而企業又希望獲得集中管理效率的情況下,混合拓樸結構正日益受到青睞。

複雜的多司法管轄區合規性是推廣應用的一大障礙。

跨境資料傳輸和儲存法規的差異迫使企業笨拙地將本地環境和全球環境融合在一起,從而延長專案週期並增加成本。在印尼等市場,嚴格的資料在地化要求與集中式SaaS的吸引力相衝突,迫使企業採用難以維護的混合部署模式。對於缺乏內部法律和工程人才的中型企業而言,這種負擔更為沉重。

細分市場分析

預計到2025年,隱私管理軟體解決方案市場將佔總營收的71.20%,凸顯了集中式編配套件的關鍵角色。目前,成長重點正轉向配置和最佳化方面的專業知識,專業服務和託管服務的年成長率高達24.3%,這體現了企業不斷最佳化規則引擎並整合相關管治模組的需求。在首次引入隱私立法的地區,由於當地企業依賴外部專家來應對陌生的框架,服務需求曲線甚至更為陡峭。

向更高附加價值服務需求的轉變反映出基本客群日趨成熟,已從基礎實施階段過渡到持續改善週期。託管服務包透過整合監管監控、政策更新和運行時分析等功能,成功贏得契約,有效緩解了內部人員短缺的挑戰。將深厚的法律知識與自動化工具包結合的服務供應商,正在獲得多年期長期合作協議,並增強客戶轉換的門檻。

到2025年,雲端採用將佔隱私管理軟體市場66.30%的佔有率,年複合成長率將達到26.1%,這主要得益於企業對即時升級和彈性運算的迫切需求。私有雲端配置對那些既需要隔離又希望獲得編配優勢的嚴格監管行業極具吸引力。在資料無法跨國的地區,本地部署環境仍然普遍存在,但趨勢正在轉向混合雲架構,將本地資料儲存庫與全球策略引擎同步。

創新正朝著微服務和 API 擴展的方向發展,這些擴展能夠將隱私控制直接整合到 DevSecOps 管線中。推動「一次部署,到處運行」的獨立於基礎設施的叢集的供應商,正在降低服務中斷風險,並透過幫助客戶在無需重寫程式碼的情況下滿足不斷變化的本地化要求,加快價值實現速度。

區域分析

到2025年,北美將佔全球整體收入的37.60%。這主要得益於加州不斷完善的隱私法、特定產業法規以及圍繞國家隱私立法的聯邦層面日益激烈的討論。科技、零售和醫療保健等行業的大型企業正將隱私承諾作為產品差異化優勢,並持續重塑其資料貨幣化模式,從而推動供應商對整合式編配套件的需求。各州在演算法課責的進步,也促使企業投資於能夠管理人工智慧訓練資料和推理輸出以及傳統記錄儲存庫的平台。

預計到2025年,歐洲將佔據28.80%的市場佔有率,這主要得益於GDPR的持續影響以及歐盟對跨境資料傳輸合規性的嚴格立場。企業買家優先考慮「隱私設計」功能,並傾向於選擇符合嚴格資料保護影響評估(DPIA)標準的負責人。歐盟法規與英國脫歐後法規之間的差異使情況更加複雜,也因此,能夠維護端到端審計追蹤且無需重複建設基礎設施的多區域政策引擎越來越受到關注。 GDPR下的罰款進一步提高了董事會層面的合規意識,促使企業持續為合規現代化項目預留預算。

亞太地區正以27.2%的複合年成長率快速成長,這主要得益於印度的《資料保護和資料保護法》(DPDP)、印尼的在地化義務以及東南亞消費市場的廣泛數位化。各國政府正在現有隱私規範的基礎上疊加人工智慧倫理準則,並加速對能夠動態調整規則集的平台的投入。混合部署策略使企業既能柔軟性擴展SaaS規模,又能滿足主權要求。電子商務滲透率的不斷提高以及跨國公司對超大規模雲端的投資進一步推動了需求,預計未來五年內,該地區與北美地區的收入差距將進一步縮小。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 隱私管理解決方案的核心隱私要求和功能

- 市場促進因素

- 加強全球隱私權法規(GDPR、CCPA、LGPD、2023 年 DPDP 法案)

- 需要避免因違規行為而受到嚴厲處罰

- 向雲端和SaaS交付模式遷移

- 新興數位經濟體的中小企業快速採用SaaS

- 國家級資料在地化義務(印度、印尼、奈及利亞)

- 隱私工具與 Gen-AI管治架構的整合

- 市場限制因素

- 複雜的跨司法管轄區合規要求

- 中小企業在資訊科技支出減少期間面臨預算限制

- 由於與更廣泛的 GRC 套件重疊,平台出現疲勞。

- 經驗豐富的隱私工程師和資料保護官短缺

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 部署模式

- 雲/SaaS

- 現場

- 按組織規模

- 小型企業

- 大公司

- 按功能

- 同意和偏好管理

- 數據發現與映射

- DSAR/自動索賠

- 初步影響評估/資料保護影響評估與風險評估

- 事件回應工作流程

- 按最終用戶分類的行業

- BFSI

- 醫療保健和生命科學

- 資訊科技/通訊

- 零售與電子商務

- 政府/公共部門

- 其他終端使用者產業(媒體、教育等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- OneTrust LLC

- TrustArc Inc.

- Securiti Inc.

- SAI360(Pty Ltd)

- SAP SE

- Syrenis Ltd

- Crownpeak Technology Inc.

- Exterro Inc.

- WireWheel Inc.

- BigID Inc.

- Smart Global Governance

- Privacy Company

- Nymity(by TrustArc)

- Collibra NV

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Informatica LLC

- DataGuard GmbH

- 2B Advice GmbH

- Privacera Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the privacy management software market size is expected to grow from USD 5.07 billion in 2025 to USD 6.24 billion in 2026 and is forecast to reach USD 17.63 billion by 2031 at 23.08% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, Services), Deployment Type (On-Premises, and More), Organization Size (Small and Medium Enterprises, and More), Size Functionality (Consent and Preference Management and More), End-User Vertical Industry (BFSI, Healthcare and Life Sciences and More) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Segments.

Global Privacy Management Software Market Trends and Insights

Escalating Global Privacy Regulations Drive Market Acceleration

The widening net of data-protection statutes is reshaping governance roadmaps. India's Digital Personal Data Protection Act 2023, which tightens rules on model storage and cross-border data transfers, obliges companies to deploy platforms that can choreograph multiple regulatory workflows simultaneously. Brazil and several African nations are following suit, causing multinationals to favor solutions that update once and syndicate rule changes to every business unit. Regulators are also moving beyond personal-data rights into algorithmic transparency, reinforcing the need for unified software that can monitor AI pipeline activities in lockstep with classic privacy tasks.

Cloud and SaaS Delivery Models Transform Market Dynamics

Cloud-native rollouts answer the demand for rapid rule updates, cross-border performance, and elastic scaling. With 67% share in 2024, cloud deployment became the baseline rather than an alternative. Shared-compliance infrastructure lowers entry costs and delivers instant access to new controls when laws change. Nevertheless, cloud reliance forces firms to weigh sovereignty constraints; hybrid topologies are therefore rising where data-localization laws require in-country processing yet the enterprise still wants the efficiency of centralized orchestration.

Complex Multi-Jurisdiction Compliance Creates Implementation Barriers

Divergent rules on cross-border transfers and storage force enterprises to bolt together localized and global instances, inflating project timelines and costs. In markets such as Indonesia, strict localization mandates clash with the appeal of centralized SaaS, pushing firms toward hybrid deployments that are harder to maintain. The burden is heavier for mid-market companies that lack in-house legal and engineering talent.

Other drivers and restraints analyzed in the detailed report include:

- SMB Market Expansion in Emerging Digital Economies

- AI Governance Integration Reshapes Privacy Management Architecture

- Budget Constraints in SMB Segment Limit Market Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Privacy management software market size for solutions commanded 71.20% of revenue in 2025, underscoring the indispensable role of centralized orchestration suites. Growth now pivots toward configuration and optimization expertise, evidenced by professional and managed services expanding 24.3% annually as enterprises fine-tune rule engines and integrate adjacent governance modules. The services curve steepens in regions introducing first-time privacy laws, where local firms rely on external specialists to navigate unfamiliar frameworks.

The up-market shift in service demand reflects a maturing customer base that has moved from basic deployment to continuous-improvement cycles. Managed-service packages are winning contracts by bundling regulatory monitoring, policy updates, and runtime analytics, easing internal head-count constraints. Providers that combine deep legal knowledge with automation toolkits are securing multi-year retainer agreements, strengthening switching barriers

Cloud implementations represented 66.30% of the privacy management software market in 2025 and are expanding at a 26.1% CAGR as firms chase instant upgrades and elastic compute. Private-cloud configurations appeal to highly regulated verticals that need isolation yet still want orchestration benefits. On-premise estates persist in pockets where data cannot exit national borders, but the pattern is shifting toward hybrid overlays that sync local vaults with global policy engines.

Innovation is clustering around micro-services and API extensions that let privacy controls embed directly into DevSecOps pipelines. Vendors promoting infrastructure-agnostic clusters-deploy-once, run-anywhere-lower exit barriers and help customers comply with evolving localization clauses without rewriting code, accelerating time-to-value.

Geography Analysis

North America captured 37.60% of global revenue in 2025, propelled by California's evolving privacy statutes, sector-specific rules, and escalating federal discourse on a national privacy bill. Large enterprises in technology, retail, and healthcare continue to recalibrate data-monetization models by using privacy credentials to differentiate products, reinforcing vendor demand for integrated orchestration suites. State-level advances in algorithmic accountability are steering investment toward platforms that can govern AI training data and inference outputs side by side with conventional record repositories.

Europe held 28.80% share in 2025 on the back of GDPR's continued influence and the bloc's strict approach to cross-border transfer adequacy. Corporate buyers prioritize privacy-by-design capabilities and favor suppliers that pass rigorous data-protection-impact-assessment benchmarks. Divergence between EU rules and post-Brexit UK provisions adds complexity, stimulating interest in multi-regime policy engines that maintain end-to-end audit trails without duplicating infrastructure. Fines issued under GDPR have sharpened board-level focus, translating into sustained budget protection for compliance modernisation projects.

Asia-Pacific is expanding at a 27.2% CAGR, underpinned by India's DPDP Act, Indonesia's localization mandates, and broad digitization across Southeast Asian consumer markets. Governments are layering AI ethics guidelines onto existing privacy norms, accelerating spending on platforms that can adapt rule sets dynamically. Hybrid deployment strategies satisfy sovereignty clauses while giving companies the flexibility of scale-out SaaS. Rising e-commerce penetration and multinational hyperscale cloud investments are further amplifying demand, positioning the region to narrow the revenue gap with North America over the next five years.

- OneTrust LLC

- TrustArc Inc.

- Securiti Inc.

- SAI360 (Pty Ltd)

- SAP SE

- Syrenis Ltd

- Crownpeak Technology Inc.

- Exterro Inc.

- WireWheel Inc.

- BigID Inc.

- Smart Global Governance

- Privacy Company

- Nymity (by TrustArc)

- Collibra NV

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Informatica LLC

- DataGuard GmbH

- 2B Advice GmbH

- Privacera Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Core Privacy Requirements and Functions of a Privacy Management Offering

- 4.3 Market Drivers

- 4.3.1 Escalating global privacy regulations (GDPR, CCPA, LGPD, DPDP Act 2023)

- 4.3.2 Need to avoid heavy non-compliance penalties

- 4.3.3 Shift to cloud and SaaS delivery models

- 4.3.4 Rapid SaaS adoption by SMBs in emerging digital economies

- 4.3.5 Country-level data-localization mandates (India, Indonesia, Nigeria)

- 4.3.6 Integration of privacy tooling with Gen-AI governance frameworks

- 4.4 Market Restraints

- 4.4.1 Complex multi-jurisdiction compliance requirements

- 4.4.2 Budget constraints for SMB segment during tech-spend pullbacks

- 4.4.3 Platform fatigue due to overlap with broader GRC suites

- 4.4.4 Shortage of experienced privacy engineers and DPO talent

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud / SaaS

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Functionality

- 5.4.1 Consent and Preference Management

- 5.4.2 Data Discovery and Mapping

- 5.4.3 DSAR / Rights-Request Automation

- 5.4.4 PIA / DPIA and Risk Assessment

- 5.4.5 Incident Response Workflow

- 5.5 By End-User Vertical Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 IT and Telecom

- 5.5.4 Retail and e-Commerce

- 5.5.5 Government and Public Sector

- 5.5.6 Other End-User Vertical Industries (Media, Education, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 OneTrust LLC

- 6.4.2 TrustArc Inc.

- 6.4.3 Securiti Inc.

- 6.4.4 SAI360 (Pty Ltd)

- 6.4.5 SAP SE

- 6.4.6 Syrenis Ltd

- 6.4.7 Crownpeak Technology Inc.

- 6.4.8 Exterro Inc.

- 6.4.9 WireWheel Inc.

- 6.4.10 BigID Inc.

- 6.4.11 Smart Global Governance

- 6.4.12 Privacy Company

- 6.4.13 Nymity (by TrustArc)

- 6.4.14 Collibra NV

- 6.4.15 IBM Corporation

- 6.4.16 Microsoft Corporation

- 6.4.17 Cisco Systems Inc.

- 6.4.18 Informatica LLC

- 6.4.19 DataGuard GmbH

- 6.4.20 2B Advice GmbH

- 6.4.21 Privacera Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

資料恢復軟體市場:2026-2032年全球市場預測(按組件、作業系統、復原類型、檔案類型、定價模式、部署模式、組織規模和最終用戶產業分類)

資料恢復軟體市場:2026-2032年全球市場預測(按組件、作業系統、復原類型、檔案類型、定價模式、部署模式、組織規模和最終用戶產業分類) 人力資源合規與GDPR平台:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

人力資源合規與GDPR平台:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球VIP票務市場報告

2026年全球VIP票務市場報告 2026-2030年全球資料保護與恢復軟體市場

2026-2030年全球資料保護與恢復軟體市場 資料保護即服務市場報告:按服務類型、部署類型、組織規模、最終用戶產業和地區分類(2026-2034 年)2026年全球加密狗市場報告

資料保護即服務市場報告:按服務類型、部署類型、組織規模、最終用戶產業和地區分類(2026-2034 年)2026年全球加密狗市場報告 軟體保護加密狗市場:按產品類型、最終用戶和地區分類隱私管理軟體市場:按類型、部署方式、產業和地區分類2026年全球資料居住驗證平台市場報告2026年全球一般資料保護規則服務市場報告

軟體保護加密狗市場:按產品類型、最終用戶和地區分類隱私管理軟體市場:按類型、部署方式、產業和地區分類2026年全球資料居住驗證平台市場報告2026年全球一般資料保護規則服務市場報告