|

市場調查報告書

商品編碼

2066596

中國固態硬碟市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)China Solid-State Drive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

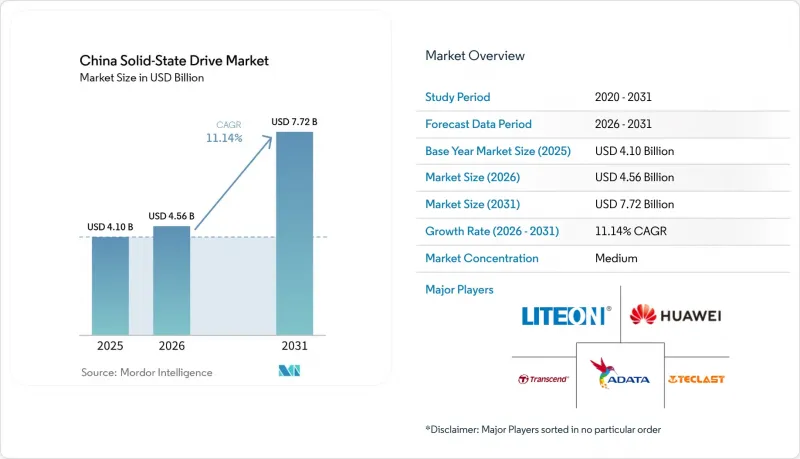

根據 Mordor Intelligence 預測,中國固態硬碟 (SSD) 市場規模將從 2025 年的 41 億美元成長到 2026 年的 45.6 億美元,然後在 2031 年達到 77.2 億美元,2026 年至 2031 年的複合年成長率為 11.14%。

本報告按介面(串列ATA (SATA)、PCI Express (PCIe/NVMe) 等)、外形規格(2.5吋硬碟、M.2模組等)、NAND技術(SLC/MLC、TLC等)、應用領域(企業級、用戶端)以及最終用戶產業(雲端服務供應商、超大規模和託管資料中心等)進行細分。市場預測以美元計價。

中國固態硬碟(SSD)市場趨勢及洞察。

面向人工智慧工作負載的資料中心擴展

預計到2025年,中國的人工智慧運算能力將超過300 exaflops,這將使模型訓練伺服器的固態硬碟(SSD)容量需求從目前的30 TB成長到本季末的100 TB。金山雲基於Solidigm QLC裝置的「KS3極速」部署方案,目前已能維持每Petabyte 1 Tbps的處理速度,比同類機械硬碟陣列快100倍。推理工作負載的成長速度更快,預計到2030年,儲存需求將達到447 Exabyte。為了確保即使在出口限制下也能穩定供應,雲端服務供應商正在轉向國產PCIe 5.0 NVMe SSD。因此,隨著每增加一個AI伺服器機架,中國固態硬碟市場銷售量都會直接成長。

消費性設備中從 HDD 到 SSD 的遷移

隨著內容創作工作負載向 4K 和 8K 格式轉變,消費者對配備固態硬碟 (SSD) 的筆記型電腦和桌上型電腦的接受度正在加速提升。三星西安工廠已於 2024 年恢復 70% 的運轉率,穩定了本地智慧型手機 OEM 廠商的 NAND 快閃記憶體供應。國內廠商優尼思 (UNIS) 目前正在出貨傳輸速度達 14.9 GB/s 的 PCIe 5.0 固態硬碟,縮小了與海外產品的性能差距,同時為銷售合作夥伴提供了成本優勢。儘管疫情期間受 PC 市場低迷的影響,零售價格受到抑制,但預計生產計畫管理的改進將使 2025 年下半年市場趨於穩定,中國固態硬碟消費通路預計將持續成長。

NAND價格週期波動

2024年,筆記型電腦需求疲軟,加上鎧俠和西部數據等廠商運轉率持續高企,導致現貨價格劇烈波動。中國二線固態硬碟品牌面臨利潤率壓力,被迫延後主控升級並削減促銷預算。儘管與長江實業的期貨合約已成為一種避險工具,但庫存錯配仍可能阻礙中國固態硬碟市場短期銷售成長。

細分市場分析

2025年,PCIe/NVMe設備將佔據中國固態硬碟市場61.35%的佔有率,年複合成長率達14.32%,這主要得益於人工智慧叢集對低延遲吞吐量的需求。企業用戶傾向於選擇PCIe 4.0和5.0通道以縮短變壓器模型的學習時間,這也推高了國內供應商的平均售價(ASP)。 SATA介面在入門筆記型電腦中仍佔有一定佔有率,但隨著消費者轉向基於PCIe的筆記型電腦,其佔有率正在逐季下降。 SAS介面則繼續應用於傳統的關鍵任務陣列,在這些陣列中,雙埠的可靠性比單純的速度更為重要。因此,介面升級仍是中國固態硬碟市場產品差異化的關鍵要素。

Innogrit 和 Maxio 的第二代 PCIe 5.0 控制器新增了一個用於硬碟內 AI 快取的協處理器模組。隨著 ODM 廠商在雲端規模上對這些晶片進行認證,中國固態硬碟 (SSD) 產業正在突破性能極限,同時又不犧牲功耗控制。 PCIe 6.0 的藍圖預計將帶來兩位數的能源效率提升,這與國家減少資料中心排放的目標相契合。這些進步不僅幫助中國提升儲存價值鏈,同時也擴大了國產 IP 模組的出口潛力。

到2025年,M.2模組將佔據中國固態硬碟市場47.20%的佔有率,主要得益於OEM廠商對輕薄設計的需求。然而,隨著超大規模資料中心業者優先考慮AI機架的可維護性和氣流,預計到2031年,U.2/E1.S固態硬碟將以每年15.55%的速度成長。 E1.S固態硬碟支援25W的功耗預算,從而緩解了PCIe 5.0環境下的熱節流問題。此外,熱插拔功能的便利性也加快了災難復原速度,而災難復原是雲端服務等級協定(SLA)中的關鍵指標。

阿里巴巴張北園區正在進行將2.5吋硬碟更換為EDSFF托架的工作,這表示現有設施(棕地)正在經歷遷移。同時,擴充卡固態硬碟在專用加速器節點中仍保持一定的市場佔有率,在這些節點中,頻寬飽和度比密度更重要。總而言之,這種外形尺寸的轉變清晰地表明,機架級設計選擇正在如何影響中國固態硬碟市場的整個供應鏈。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 面向人工智慧工作負載的資料中心擴展

- 消費性電子產品中從 HDD 到 SSD 的遷移

- 政府主導的「東西方資料計算」發展

- NAND供應鏈本地化

- 工業物聯網中的邊緣處理和儲存內部處理

- 市場限制因素

- NAND價格週期的波動性

- 對先進設備的出口管制限制

- 超大規模資料中心的電源限制

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- By Interface

- 串行ATA(SATA)

- PCI Express(PCIe/NVMe)

- 串行連接 SCSI (SAS)

- USB/其他嵌入式系統

- 按外形規格

- 2.5吋驅動盤

- M.2模組

- U.2/E1.S

- 擴充卡

- 透過NAND技術

- SLC/MLC

- TLC

- QLC

- PLC(原型)

- 透過使用

- 公司

- 客戶

- 按最終用戶行業分類

- 雲端服務供應商

- 超大規模和託管資料中心

- 家用電子電器OEM製造商

- 工業和製造業

- 汽車和運輸業

- 航太/國防

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Samsung Electronics Co., Ltd.

- Yangtze Memory Technologies Co., Ltd.(YMTC)

- Western Digital Corporation

- Kingston Technology Company, Inc.

- SK Hynix Inc.

- Huawei Technologies Co., Ltd.

- ADATA Technology Co., Ltd.

- Transcend Information Inc.

- Lenovo Group Limited

- Memblaze Technology Co., Ltd.

- Shenzhen Longsys Electronics Co., Ltd.

- Dapu Microelectronics Co., Ltd.

- Kimtigo Technology Co., Ltd.

- BIWIN Storage Technology Co., Ltd.

- Kioxia Holdings Corporation

- Micron Technology Inc.

- Intel Corporation(Solidigm)

- Seagate Technology Holdings plc

- LITE-ON Technology Corporation

- Maxiotek Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the china solid-state drive market size is expected to grow from USD 4.10 billion in 2025 to USD 4.56 billion in 2026 and is forecast to reach USD 7.72 billion by 2031 at 11.14% CAGR over 2026-2031.

This report is Segmented by Interface (Serial ATA (SATA), PCI Express (PCIe/NVMe) and More), Form Factor (2. 5-Inch Drives. M. 2 Modules, and More), NAND Technology (SLC / MLC, TLC, and More), Application (Enterprise, Client), End-User Industry (Cloud Service Providers, Hyperscale and Colocation Data Centres, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Solid-State Drive Market Trends and Insights

Data-centre Expansion for AI Workloads

China's AI computing footprint is on track to exceed 300 exaflops by 2025, lifting SSD capacity requirements for model training servers from 30 TB today to 100 TB by decade-end. Kingsoft Cloud's KS3 Extreme Speed deployment, built on Solidigm QLC devices, already sustains 1 Tbps per petabyte-100X faster than comparable HDD arrays. Inference workloads are expanding even faster, with storage demand forecast to reach 447 exabytes by 2030. Cloud providers are switching to domestically packaged PCIe 5.0 NVMe SSDs to secure supply amid export controls. As a result, the China solid-state drive market enjoys a direct volume lift from every incremental rack of AI servers commissioned.

Shift from HDD to SSD in Consumer Devices

Consumer adoption of SSD-equipped laptops and desktops is accelerating as content-creation workloads move to 4K and 8K formats. Samsung's Xi'an plant rebounded to 70% utilization in 2024, stabilizing local NAND supply for smartphone OEMs. Domestic player UNIS now ships PCIe 5.0 drives at 14.9 GB/s, narrowing the performance gap with international alternatives while offering cost relief to channel partners. Though pandemic-era PC weakness tempered retail pricing, controlled production schedules signal firmer conditions in late 2025, sustaining the China solid-state drive market's consumer channel.

NAND Price-cycle Volatility

Spot prices swung sharply in 2024 as weak laptop demand met elevated fab utilization at Kioxia and Western Digital. Chinese tier-2 SSD brands faced squeezed margins, delaying controller upgrades and tightening promotional budgets. Forward contracts with YMTC are emerging as a hedge, but inventory misalignment can still hinder near-term sell-in volumes across the China solid-state drive market.

Other drivers and restraints analyzed in the detailed report include:

- East-Data-West-Compute" Government Build-out

- Localization of NAND Supply Chain

- Export-control Limits on Advanced Tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PCIe/NVMe devices accounted for 61.35% of the China solid-state drive market size in 2025 and are on pace for a 14.32% CAGR, propelled by AI clusters that demand low-latency throughput. Enterprise buyers favour PCIe 4.0 and 5.0 lanes to cut training time on transformer models, lifting blended ASPs for domestic suppliers. SATA maintains a toehold in entry-level notebooks, but its share slides each quarter as consumers migrate to PCIe-based laptops. SAS continues in legacy mission-critical arrays where dual-port reliability trumps raw speed. Interface upgrades therefore remain a centerpiece of product differentiation across the China solid-state drive market.

Second-generation PCIe 5.0 controllers from Innogrit and Maxio add co-processing blocks for on-drive AI caching. As ODMs qualify these chips at cloud scale, the China solid-state drive industry unlocks fresh performance tiers without sacrificing power budgets. PCIe 6.0 roadmaps promise double-digit efficiency gains, aligning with the national goal of curbing data-center emissions. These advances reinforce China's ambition to climb the storage value chain while enlarging export potential for indigenous IP blocks.

M.2 modules held 47.20% of the China solid-state drive market share in 2025, favoured by OEMs for thin-and-light designs. Yet the U.2/E1.S category is forecast to grow 15.55% annually through 2031 as hyperscalers prioritize serviceability and airflow in AI racks. E1.S drives support 25 W envelopes, easing thermal throttling in PCIe 5.0 deployments. Their hot-swap convenience accelerates failure recovery, a key metric in cloud SLAs.

Converters from 2.5-inch bays to EDSFF trays are underway at Alibaba's Zhangbei campus, signalling a migration path for brownfield sites. Meanwhile, add-in-card SSDs retain a niche in specialized accelerator nodes where bandwidth saturation overrides density concerns. Collectively, the form-factor shift exemplifies how rack-level design choices ripple across the China solid-state drive market supply chain.

List of Companies Covered in this Report:

- Samsung Electronics Co., Ltd.

- Yangtze Memory Technologies Co., Ltd. (YMTC)

- Western Digital Corporation

- Kingston Technology Company, Inc.

- SK Hynix Inc.

- Huawei Technologies Co., Ltd.

- ADATA Technology Co., Ltd.

- Transcend Information Inc.

- Lenovo Group Limited

- Memblaze Technology Co., Ltd.

- Shenzhen Longsys Electronics Co., Ltd.

- Dapu Microelectronics Co., Ltd.

- Kimtigo Technology Co., Ltd.

- BIWIN Storage Technology Co., Ltd.

- Kioxia Holdings Corporation

- Micron Technology Inc.

- Intel Corporation (Solidigm)

- Seagate Technology Holdings plc

- LITE-ON Technology Corporation

- Maxiotek Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-centre expansion for AI workloads

- 4.2.2 Shift from HDD to SSD in consumer devices

- 4.2.3 East-Data-West-Compute government build-out

- 4.2.4 Localization of NAND supply chain

- 4.2.5 Edge and in-storage processing for IIoT

- 4.3 Market Restraints

- 4.3.1 NAND price-cycle volatility

- 4.3.2 Export-control limits on advanced tools

- 4.3.3 Power-supply caps for hyperscale DCs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Interface

- 5.1.1 Serial ATA (SATA)

- 5.1.2 PCI Express (PCIe/NVMe)

- 5.1.3 Serial-Attached SCSI (SAS)

- 5.1.4 USB/Other Embedded

- 5.2 By Form Factor

- 5.2.1 2.5-inch Drives

- 5.2.2 M.2 Modules

- 5.2.3 U.2 / E1.S

- 5.2.4 Add-in Cards

- 5.3 By NAND Technology

- 5.3.1 SLC / MLC

- 5.3.2 TLC

- 5.3.3 QLC

- 5.3.4 PLC (Prototype)

- 5.4 By Application

- 5.4.1 Enterprise

- 5.4.2 Client

- 5.5 By End-User Industry

- 5.5.1 Cloud Service Providers

- 5.5.2 Hyperscale & Colocation Data Centres

- 5.5.3 Consumer Electronics OEMs

- 5.5.4 Industrial & Manufacturing

- 5.5.5 Automotive & Transportation

- 5.5.6 Aerospace & Defence

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Yangtze Memory Technologies Co., Ltd. (YMTC)

- 6.4.3 Western Digital Corporation

- 6.4.4 Kingston Technology Company, Inc.

- 6.4.5 SK Hynix Inc.

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 ADATA Technology Co., Ltd.

- 6.4.8 Transcend Information Inc.

- 6.4.9 Lenovo Group Limited

- 6.4.10 Memblaze Technology Co., Ltd.

- 6.4.11 Shenzhen Longsys Electronics Co., Ltd.

- 6.4.12 Dapu Microelectronics Co., Ltd.

- 6.4.13 Kimtigo Technology Co., Ltd.

- 6.4.14 BIWIN Storage Technology Co., Ltd.

- 6.4.15 Kioxia Holdings Corporation

- 6.4.16 Micron Technology Inc.

- 6.4.17 Intel Corporation (Solidigm)

- 6.4.18 Seagate Technology Holdings plc

- 6.4.19 LITE-ON Technology Corporation

- 6.4.20 Maxiotek Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

固態硬碟 (SSD) 市場:按類型、外形規格、儲存容量、技術類型、最終用戶和通路分類-2026-2032 年全球市場預測

固態硬碟 (SSD) 市場:按類型、外形規格、儲存容量、技術類型、最終用戶和通路分類-2026-2032 年全球市場預測 固態硬碟 (SSD) 市場報告:按類型、介面、外形規格、儲存容量、應用程式和地區分類 (2026–2034)

固態硬碟 (SSD) 市場報告:按類型、介面、外形規格、儲存容量、應用程式和地區分類 (2026–2034) 固態硬碟市場-全球產業規模、佔有率、趨勢、機會、預測:按介面、技術、儲存、最終用戶、地區和競爭格局分類,2021-2031年

固態硬碟市場-全球產業規模、佔有率、趨勢、機會、預測:按介面、技術、儲存、最終用戶、地區和競爭格局分類,2021-2031年 企業級固態硬碟市場規模、佔有率和成長分析:按產品類型、儲存容量、快閃記憶體類型、應用、介面、最終用戶和地區分類-2026-2033年產業預測

企業級固態硬碟市場規模、佔有率和成長分析:按產品類型、儲存容量、快閃記憶體類型、應用、介面、最終用戶和地區分類-2026-2033年產業預測 企業級外接可攜式硬碟市場報告:趨勢、預測及競爭分析(至2035年)

企業級外接可攜式硬碟市場報告:趨勢、預測及競爭分析(至2035年) 固態硬碟 (SSD) 市場:按 SSD 介面、應用和地區分類

固態硬碟 (SSD) 市場:按 SSD 介面、應用和地區分類 ZNS SSD全球市場報告2026

ZNS SSD全球市場報告2026 固態硬碟 (SSD) 市場規模、佔有率和成長分析:按介面、外形規格、技術、儲存容量和地區分類-2026-2033 年產業預測

固態硬碟 (SSD) 市場規模、佔有率和成長分析:按介面、外形規格、技術、儲存容量和地區分類-2026-2033 年產業預測 固態硬碟市場分析及預測(至2035年):依類型、產品、應用、技術、組件、外形、設備、最終用戶、部署方式及功能分類全球固態硬碟市場:依儲存類型、介面、技術、最終用戶、國家及地區分類-產業分析、市場規模、佔有率及預測(2025-2032年)

固態硬碟市場分析及預測(至2035年):依類型、產品、應用、技術、組件、外形、設備、最終用戶、部署方式及功能分類全球固態硬碟市場:依儲存類型、介面、技術、最終用戶、國家及地區分類-產業分析、市場規模、佔有率及預測(2025-2032年)