|

市場調查報告書

商品編碼

2066585

不飽和聚酯樹脂(UPR):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Unsaturated Polyester Resin (UPR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

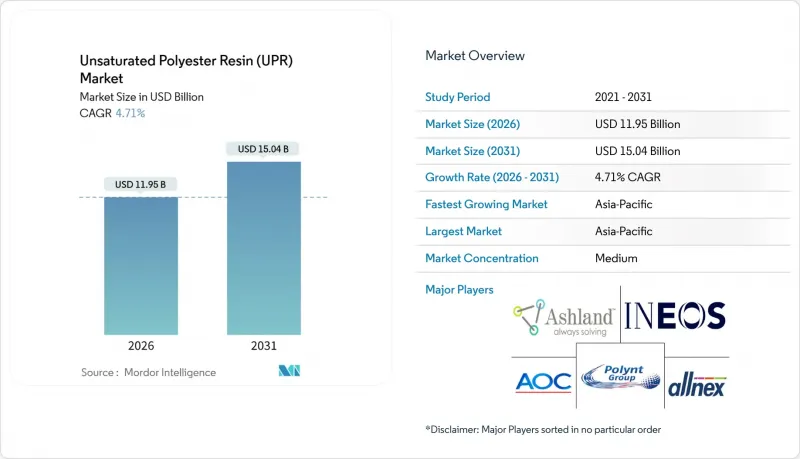

據 Mordor Intelligence 稱,2026 年不飽和聚酯樹脂市場規模估計為 119.5 億美元,預計到 2031 年將達到 150.4 億美元,在預測期(2026-2031 年)內複合年成長率為 4.71%。

本報告按原料(馬來酸酐、鄰苯二甲酸酐等)、產品類型(鄰苯二甲酸酐、異構體樹脂、DCPD 及其他類型)、形態(液體和粉末)、終端應用產業(建築、化學及其他)以及地區(亞太、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以美元計價。

全球不飽和聚酯樹脂(UPR)市場趨勢及洞察

風力發電機葉片的應用正在迅速增加。

在不飽和聚酯樹脂市場,隨著北海和台灣海峽離岸風力發電設施平均轉子長度超過85公尺[1],預計到2025年,全球對葉片複合材料的需求將增加22%。由於真空灌注製程中,不飽和聚酯樹脂的每千瓦成本比環氧樹脂系統更具優勢,因此它仍然是葉片頂蓋和殼體層壓板的標準基體。歐洲循環經濟法規要求2030年建立廢舊葉片的回收途徑,促使人們測試含有再生PET多元醇的UPR共混物。這可以將與退役相關的物流成本降低高達15%。中國國家能源局已撥款180億美元用於2025年新增離岸風力發電裝置容量,並確認亞太地區是2031年之前的主要成長引擎。因此,葉片製造商正在尋找經過驗證的可回收樹脂、低生熱樹脂以及具有適用於20年運作的疲勞耐久性樹脂。

汽車和運輸業的成長

到2025年,汽車製造商將在不飽和聚酯樹脂市場加工約180萬噸複合樹脂,其中40%的產量將用於製造底盤護板、電池托盤和A級車身面板等零件,這些零件均採用不飽和聚酯樹脂基片狀片狀成型塑膠(SMC)。電動車(EV)平台需要在保持輕量化的同時具備電磁干擾(EMI)屏蔽和阻燃性能,因此異戊二烯基樹脂的市場佔有率不斷擴大。通用汽車和Stellantis計劃在2025年將其SMC壓機產能提高30%,以支持其降低整車重量、提升續航里程10%至15%的目標。這些封閉式壓平機消除了苯乙烯排放,並且已經符合加州關於複合材料部件中揮發性有機化合物(VOC)含量限制在50 g L⁻¹的法規。供應合約擴大規定了 UL 94 V-0 阻燃性和在 -40 度C至 120 度C溫度範圍內 10 年使用壽命內的尺寸穩定性。

順丁烯二酸酐的價格波動

2025年,受原油和苯供應鏈中斷的影響,不飽和聚酯樹脂市場現貨價格在每噸1,400美元至2,100美元之間波動,整個價值鏈均受到影響。沒有長期供應合約的樹脂生產商利潤率下降了200至300個基點,這加速了垂直整合的進程,例如Polint收購了義大利年產5萬噸馬來酸酐的產能。中國佔全球順丁烯二酸酐產能的55%,而歐美買家則面臨美國301條款下的運費和關稅風險。其他生物基製造流程仍處於試點階段,由於成本溢價高達40%至60%,難以廣泛應用。

細分市場分析

到2025年,馬來酸酐將佔不飽和聚酯樹脂市場銷售額的51.26%,凸顯了其在鄰苯二甲酸和間苯二甲酸骨架中的核心地位,這些骨架能夠平衡成本和機械強度。丙二醇的年複合成長率預計到2031年將達到5.70%,這主要得益於加工商對低黏度和優異潤濕性的需求,尤其是在風力發電機支管帽的真空灌注製程。鄰苯二甲酸酐繼續用於通用正交樹脂應用,而苯乙烯單體儘管面臨引入回收系統以減少排放的壓力,但仍作為交聯稀釋劑至關重要。

丙二醇的成長反映了以新戊二醇和二丙二醇等共反應物取代丙二醇的廣泛趨勢,這些共反應物能夠提高船舶和化學設施中的水解穩定性。在中國,受煤製烯烴製程的推動,預計到2025年,丙二醇的產能將成長18%,進而降低亞洲地區的交付成本。目前,OEM審核要求原料供應商提供ISO 9001認證和批次可追溯性,面向航太和醫療零件的原料供應商的品質要求也日益提高。

2025年,在不飽和聚酯樹脂市場中,鄰位樹脂的銷售額佔比高達53.31%。這主要得益於其高度的混配彈性,使其在建築和衛浴設備應用領域保持價格競爭力。同時,受船舶、海水淡化廠和化學設備等產業對耐高溫和耐腐蝕性能需求的推動,異構樹脂預計到2031年將以6.56%的複合年成長率成長。雙環戊二烯樹脂在風力發電機機艙和大型儲存槽等領域佔據著獨特的市場地位,其低發熱量特性使其能夠進行厚壁澆鑄而不產生裂縫。

隨著液化天然氣 (LNG) 接收站、海上生產平台和工業污水處理設施的擴建,異構樹脂的應用也日益廣泛。這些設施對玻璃纖維增強材料的要求越來越高,需要符合 EN 13121 抗彎強度標準。 AOC 和 Ashland 等供應商於 2025 年推出了“iso-NPG”牌號,該牌號具有耐腐蝕性,並且無需加熱模具即可成型,因此對於資本投入有限的製造商而言也易於採用。

區域分析

到2025年,亞太地區將佔全球不飽和聚酯樹脂銷售額的43.45%,成為該市場的主要驅動力。受中國基礎設施投資、印度住宅市場繁榮以及東南亞工業擴張的推動,預計到2031年,亞太地區市場將以5.78%的複合年成長率成長。中國計劃在2025年投入8,000億美元用於城市軌道交通、供水系統和可再生能源設施建設,這些項目都需要使用耐腐蝕複合材料來製造管道和支撐結構。印度的生產連結獎勵計畫吸引了300億美元的外國投資,刺激了對電動摩托車、家用電器和電信設備零件的需求。儘管該地區的法規結構仍有差異,但精通GB和BIS標準的本地複合材料生產商正在與老牌跨國公司競爭,不斷擴大市場佔有率。

北美市場佔有率主要受美國對汽車複合材料、風力渦輪機葉片和化學加工設備的需求所驅動。 《通膨控制法案》已將複合材料相關資本投資金額提升至2025年的150億美元,用於樹脂混煉、SMC壓機及葉片成型廠。加州空氣資源委員會 (CARB) 的法規正在加速向封閉式模成型和低聚苯乙烯樹脂系統的轉型,為擁有超低排放產品組合的供應商進入高階市場創造了更多機會。預計到2025年,墨西哥的汽車組裝將超過400萬輛,當地一級供應商已擴大SMC產能,以滿足北美和歐洲電動車 (EV) 專案的需求。

在歐洲,不飽和聚酯樹脂市場主要集中在船舶、汽車和風力發電等高附加價值應用領域。到2025年,德國汽車製造商將消耗18萬噸複合樹脂。這主要歸功於福斯、寶馬和賓士等公司採用SMC電池機殼和結構零件。 「循環經濟行動計畫」和更嚴格的工業排放法規正迫使供應商轉型使用可回收和生物基化學品。南美洲、中東和非洲的不飽和聚酯樹脂市場規模雖小,但成長迅速,這主要得益於巴西對衛生基礎設施的投資、沙烏地阿拉伯化學工業的多元化發展以及南非採礦基礎設施的建設。在這些地區,玻璃纖維增強設備更受歡迎,因為與金屬相比,它可以降低整體生命週期成本。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 風力發電機葉片採用率迅速提高

- 汽車和運輸業的成長

- 新興亞洲的建築和基礎設施蓬勃發展

- 歐盟REACH法規對低聚苯乙烯樹脂的壓力

- OEM廠商向閉封閉式SMC/BMC轉型,用於電動車

- 市場限制因素

- 順丁烯二酸酐的價格波動

- 環境和監管方面的挑戰

- 對生命週期評估(LCA)的日益關注正在推動生物環氧樹脂材料的發展。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按成分

- 順丁烯二酸酐

- 鄰苯二甲酐

- 丙二醇

- 苯乙烯單體

- 其他(添加物、引髮劑)

- 依產品類型

- 正畸樹脂

- 異氰酸酯基樹脂

- 二環戊二烯(DCPD)

- 其他類型

- 按形式

- 液體

- 粉末

- 按最終用途行業分類

- 建築/施工

- 化學品

- 電氣和電子設備

- 油漆和塗料

- 運輸

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Allnex GmbH

- AOC

- Ashland

- BASF SE

- Covestro AG

- Crystic Resins India Pvt. Ltd.

- DIC Corporation

- INEOS

- Interplastic Corporation

- Polynt SpA

- Scott Bader Company Ltd

- SWANCOR

- U-Pica Company

- Xinyang Technology Group

- Zhangzhou Yabang Chemical Co., Ltd.

- Zhejiang Tianhe Resin Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the unsaturated polyester resin market size is estimated at USD 11.95 billion in 2026, and is expected to reach USD 15.04 billion by 2031, at a CAGR of 4.71% during the forecast period (2026-2031).

This report is Segmented by Raw Material (Maleic Anhydride, Phthalic Anhydride, and More), Product Type (Ortho-Resins, Isoresins, DCPD, and Other Types), Form (Liquid and Powder), End-Use Industry (Building and Construction, Chemical, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Unsaturated Polyester Resin (UPR) Market Trends and Insights

Surging Adoption in Wind-Turbine Blades

Offshore installations lifted global blade-composite demand by 22% in 2025 as average rotor lengths moved beyond 85 meters in the North Sea andthe Taiwan Strait in the unsaturated polyester resin market [1]. Unsaturated polyester resin remains the default matrix for spar-cap and shell laminates because vacuum-infusion delivers attractive cost-per-kilowatt figures versus epoxy systems. European circular-economy mandates now require end-of-life blade recovery pathways by 2030, which is prompting trials of UPR blends incorporating recycled-PET polyols that can cut decommissioning logistics costs by up to 15%. China's National Energy Administration allocated USD 18 billion for new offshore capacity in 2025, confirming Asia-Pacific as the primary growth engine through 2031. Blade makers therefore seek resins with documented recyclability, low exotherm, and fatigue durability suitable for 20-year service intervals.

Growth of Automotive and Transportation Sectors

Automotive manufacturers processed roughly 1.8 million t of composite resins in 2025 in the unsaturated polyester resin market, and 40% of that volume relied on unsaturated polyester resin-based sheet-molding-compound for underbody shields, battery trays, and Class-A body panels. Electric-vehicle platforms need electromagnetic-interference shielding and flame retardancy while maintaining low mass; isoresin and dicyclopentadiene grades therefore gain share. General Motors and Stellantis lifted SMC press capacity by 30% during 2025 to support curb-weight reduction targets that improve driving range by 10-15%. Closed-mold presses eliminate styrene emissions and already comply with California rules that limit volatile-organic compounds to 50 g L-1 for composite parts. Supply contracts increasingly stipulate UL 94 V-0 flame-retardant performance and dimensional stability from -40 °C to 120 °C across a decade of service.

Maleic Anhydride Price Volatility

Spot prices swung between USD 1,400 and USD 2,100 t-1 in 2025 in the unsaturated polyester resin market as crude-oil and benzene disruptions rippled through the value chain. Resin makers without long-term supply contracts faced margin compression of 200-300 basis points, prompting vertical-integration moves such as Polynt's 50,000 t y-1 maleic-anhydride acquisition in Italy. China controls 55% of global maleic-anhydride capacity, exposing Western buyers to freight and tariff risks under Section 301 measures in the United States. Alternative bio-based pathways remain pilot-scale and carry 40-60% cost premiums, limiting broad adoption.

Other drivers and restraints analyzed in the detailed report include:

- Construction and Infrastructure Boom in Emerging Asia

- OEM Shift to Closed-Mold SMC/BMC for E-Mobility

- Environmental and Regulatory Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Maleic Anhydride held 51.26% of 2025 revenue within the unsaturated polyester resin market share, underscoring its central role in ortho-phthalic and iso-phthalic backbones that balance cost and mechanical strength. Propylene Glycol is expanding at a 5.70% CAGR through 2031, driven by processors who seek lower viscosity and better wet-out during vacuum-infusion of wind-turbine spar caps. Phthalic Anhydride continues to serve general-purpose ortho grades, while Styrene Monomer remains indispensable as a cross-linking diluent, despite pressure for recovery systems that cap emissions.

Propylene Glycol growth mirrors wider substitution toward neopentyl glycol and dipropylene glycol co-reactants that enhance hydrolytic stability in marine and chemical-processing equipment. China expanded propylene-glycol capacity by 18% in 2025 on the back of coal-to-olefin routes, reducing delivered costs within Asia. OEM audits now require ISO 9001 certification and batch traceability, reinforcing quality expectations for raw-material suppliers targeting aerospace and medical components.

Ortho-resins captured 53.31% of 2025 revenue in the unsaturated polyester resin market because broad formulation latitude keeps prices competitive across construction and sanitary-ware uses. Isoresins, however, are projected to climb 6.56% CAGR through 2031, propelled by marine vessels, desalination plants, and chemical-processing equipment that demand elevated temperature and corrosion resistance. Dicyclopentadiene resin occupies a niche in wind-turbine nacelles and large storage tanks, where low exotherm enables thick-section casting without cracking.

Isoresin uptake aligns with the expansion of liquefied-natural-gas terminals, offshore production platforms, and industrial wastewater facilities that specify fiberglass-reinforced equipment meeting EN 13121 flexural-strength thresholds. Suppliers such as AOC and Ashland launched iso-NPG grades in 2025 that provide corrosion resistance while processing on unheated molds, enabling adoption by fabricators with limited capital investment.

Geography Analysis

Asia-Pacific led the unsaturated polyester resin market with a delivered 43.45% of global revenue in 2025 and is forecast to grow at a 5.78% CAGR to 2031, driven by Chinese infrastructure outlays, India's housing boom, and Southeast Asian industrial expansion. China allocated USD 800 billion in 2025 for urban rail, water systems, and renewable energy installations that consume corrosion-resistant piping and blade-grade composites. India's production-linked incentives attracted USD 30 billion in foreign investment, spurring component demand in electric two-wheelers, appliances, and telecom equipment. Regulatory frameworks in the region remain fragmented, yet local compounders adept at navigating GB and BIS standards win share against multinational incumbents.

North America's share is anchored by United States demand in automotive composites, wind-energy blades, and chemical-processing equipment. The Inflation Reduction Act unlocked USD 15 billion in composite capital expenditure during 2025 across resin compounding, SMC presses, and blade-molding plants. California Air Resources Board rules speed the migration to closed-mold and low-styrene resin systems, opening premium segments for suppliers with ultra-low emission portfolios. Mexico's vehicle assemblies exceeded 4 million units in 2025, and local Tier-1s expanded SMC capacity to serve North American and European electric-vehicle programs.

Europe focuses on high-value marine, automotive, and wind-energy uses in the unsaturated polyester resin market. Germany's carmakers consumed 180,000 t of composite resins in 2025 as Volkswagen, BMW, and Mercedes-Benz integrated SMC battery enclosures and structural components. The Circular Economy Action Plan and stricter Industrial Emissions rules push suppliers toward recyclable, bio-based chemistries. South America and Middle East and Africa remain smaller but fast-growing in the unsaturated polyester resin market, buoyed by Brazilian sanitation investments, Saudi chemical diversification, and South African mining infrastructure, each favoring fiberglass-reinforced equipment that lowers total life-cycle costs versus metals.

- Allnex GmbH

- AOC

- Ashland

- BASF SE

- Covestro AG

- Crystic Resins India Pvt. Ltd.

- DIC Corporation

- INEOS

- Interplastic Corporation

- Polynt S.p.A.

- Scott Bader Company Ltd

- SWANCOR

- U-Pica Company

- Xinyang Technology Group

- Zhangzhou Yabang Chemical Co., Ltd.

- Zhejiang Tianhe Resin Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption in Wind-Turbine Blades

- 4.2.2 Growth of Automotive and Transportation Sectors

- 4.2.3 Construction And Infrastructure Boom in Emerging Asia

- 4.2.4 EU REACH Pressure for Low-Styrene Resins

- 4.2.5 OEM Shift to Closed-Mold SMC/BMC for E-Mobility

- 4.3 Market Restraints

- 4.3.1 Maleic Anhydride Price Volatility

- 4.3.2 Environmental and Regulatory Challenges

- 4.3.3 Rising LCA Scrutiny Favouring Bio-Epoxy Systems

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Maleic Anhydride

- 5.1.2 Phthalic Anhydride

- 5.1.3 Propylene Glycol

- 5.1.4 Styrene Monomer

- 5.1.5 Others (Additives, Initiators)

- 5.2 By Product Type

- 5.2.1 Ortho-resins

- 5.2.2 Isoresins

- 5.2.3 Dicyclopentadiene (DCPD)

- 5.2.4 Other Types

- 5.3 By Form

- 5.3.1 Liquid

- 5.3.2 Powder

- 5.4 By End-use Industry

- 5.4.1 Building and Construction

- 5.4.2 Chemical

- 5.4.3 Electrical and Electronics

- 5.4.4 Paints and Coatings

- 5.4.5 Transportation

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Allnex GmbH

- 6.4.2 AOC

- 6.4.3 Ashland

- 6.4.4 BASF SE

- 6.4.5 Covestro AG

- 6.4.6 Crystic Resins India Pvt. Ltd.

- 6.4.7 DIC Corporation

- 6.4.8 INEOS

- 6.4.9 Interplastic Corporation

- 6.4.10 Polynt S.p.A.

- 6.4.11 Scott Bader Company Ltd

- 6.4.12 SWANCOR

- 6.4.13 U-Pica Company

- 6.4.14 Xinyang Technology Group

- 6.4.15 Zhangzhou Yabang Chemical Co., Ltd.

- 6.4.16 Zhejiang Tianhe Resin Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emergence of Bio-based Unsaturated Polyester Resins

高分子量分散劑市場按形態、類型、最終用途產業和應用方法分類-2026-2032年全球預測

高分子量分散劑市場按形態、類型、最終用途產業和應用方法分類-2026-2032年全球預測 不飽和聚酯樹脂市場規模、佔有率和趨勢分析報告:按產品、應用、形態、地區和細分市場預測(2026-2033 年)

不飽和聚酯樹脂市場規模、佔有率和趨勢分析報告:按產品、應用、形態、地區和細分市場預測(2026-2033 年) 高分子量聚酯樹脂:全球市佔率及排名、總收入及需求預測(2025-2031年)高分子量聚酯樹脂市場(依產品類型、形式、應用、最終用途產業和分銷管道)—2025-2030 年全球預測

高分子量聚酯樹脂:全球市佔率及排名、總收入及需求預測(2025-2031年)高分子量聚酯樹脂市場(依產品類型、形式、應用、最終用途產業和分銷管道)—2025-2030 年全球預測 雙環戊二烯聚酯樹脂的全球市場

雙環戊二烯聚酯樹脂的全球市場 聚酯樹脂:全球市場

聚酯樹脂:全球市場 飽和聚酯樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

飽和聚酯樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 管道和儲槽不飽和聚酯樹脂複合材料市場報告:到2030年的趨勢、預測和競爭分析電氣電子領域不飽和聚酯樹脂複合材料市場報告:到2030年的趨勢、預測和競爭分析

管道和儲槽不飽和聚酯樹脂複合材料市場報告:到2030年的趨勢、預測和競爭分析電氣電子領域不飽和聚酯樹脂複合材料市場報告:到2030年的趨勢、預測和競爭分析 雙環戊二烯聚酯樹脂市場,規模,佔有率,趨勢,產業分析報告:各類型樹脂,各最終用途,各地區 - 市場預測 2025年~2034年

雙環戊二烯聚酯樹脂市場,規模,佔有率,趨勢,產業分析報告:各類型樹脂,各最終用途,各地區 - 市場預測 2025年~2034年