|

市場調查報告書

商品編碼

2066581

玻璃基板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Glass Substrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

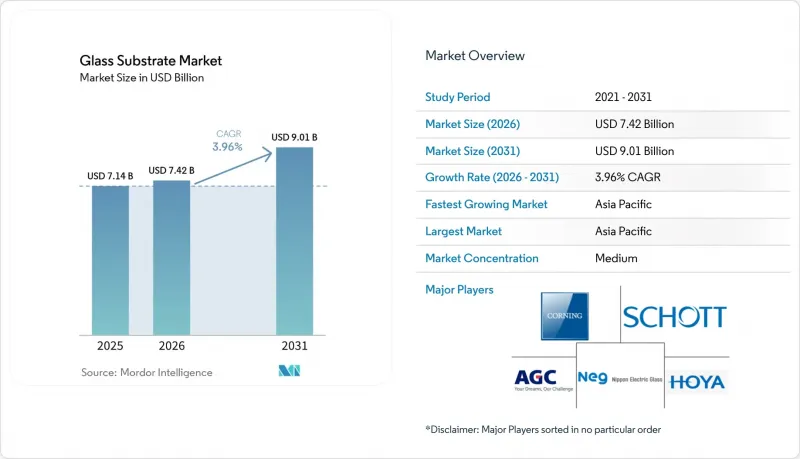

據 Mordor Intelligence 稱,2025 年玻璃基板市值為 71.4 億美元,預計到 2031 年將達到 90.1 億美元,而 2026 年為 74.2 億美元,預測期(2026-2031 年)的複合年成長率為 3.96%。

本報告按材料類型(硼矽酸玻璃、矽及其他)、應用領域(顯示面板、半導體等)、終端用戶產業(電子、汽車、航太與國防、醫療等)以及地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球玻璃基板市場趨勢及洞察

家用電子電器中液晶顯示器(LCD)的應用日益廣泛

隨著中階智慧型手機、平板電腦和顯示器液晶面板出貨量的強勁成長,亞太地區各製造地的玻璃基板市場已穩固確立。大螢幕遊戲顯示器和專業顯示器擴大採用更薄更輕的基板,以實現無邊框設計,從而減輕運輸重量並防止面板破損。這種向高價值液晶面板的轉變有利於那些既具備通用生產能力又能進行精確減薄和表面處理的供應商。這種雙重能力鞏固了垂直整合製造商的現有地位,他們可以將研發成本分攤到多個應用領域。此外,顯示器OEM廠商的藍圖表明,汽車資訊娛樂系統後市場對玻璃的需求將逐步成長,促使現有液晶面板工廠將產能重新分配給曲面駕駛座叢集。

半導體生產線擴建

英特爾、三星和台積電宣布,2030年將投資1,500億美元新建晶圓廠,這股浪潮正在重塑玻璃基板市場。市場需求在三個領域不斷成長:用於極紫外光刻的石英光圖形化坯、用於2.5D和3D封裝的玻璃芯基板,以及用於極端潔淨室環境的化學惰性檢測窗口。 Rapidus公司展示的600mm x 600mm玻璃面板預計將使晶片良率比矽中介層提高10倍,凸顯了矩形玻璃面板相對於圓形晶圓的面積效率優勢。在這個生態系統中,早期採用該設計將使供應商陷入漫長的認證週期,而那些能夠根據晶圓代工廠產量調整產能的公司將從中受益。

高昂的製造成本和資本投資

新建浮法或熔融拉絲生產線的建造成本在2億至5億美元之間,其中熔爐的成本可佔初始投資的40%。肖特公司在美因茨對其電熔工廠進行的4000萬歐元維修,凸顯了脫碳帶來的資本投資溢價,而一體化企業認為脫碳對於規避能源價格波動至關重要。在超薄玻璃和石英坯料等特殊產品領域,還需要對化學強化、拋光和一級無塵室進行額外投資,使工程總成本超過3億美元。這一障礙正導致玻璃基板市場整合,主要集中在現有企業之間,這些企業可以利用其廣泛的產品系列來抵消在其他領域投資(這些領域的投資回報期更長)。

細分市場分析

到2025年,硼矽酸玻璃將佔玻璃基板市場規模的45.76%,憑藉其熱穩定性和成本優勢,它仍然是TFT-LCD生產的基礎。儘管隨著傳統LCD產能轉向汽車和工業顯示器,其市佔率成長放緩,但8.5代和10.5代晶圓廠的巨大產能仍使硼矽酸玻璃的產量保持在高位。供應商正在擴展其精密減薄和表面處理生產線,以確保更高的利潤率,尤其是在曲面資訊娛樂顯示器和大型遊戲顯示器領域。同時,受EUV光刻技術不斷將尺寸縮小至3奈米以下的推動,石英基基板預計到2031年將維持4.41%的複合年成長率。由於石英的熱膨脹係數(CTE)接近零,且金屬雜質含量低於ppb級,其單價是硼矽酸玻璃的數倍,從而保護了利潤率免受產品價格波動的影響。

對石英的需求不斷成長,正在改變供應鏈格局。合成石英領域的兩大壟斷企業HOYA和信越化學目前正在投資擴建其CVD反應器,而半導體OEM廠商也在聯合投資提高產能,以避免EUV光刻基板短缺。因此,玻璃基板市場正呈現兩極化的局面:一方面是成本效益高、大規模生產的硼矽酸玻璃工廠,另一方面是注重無缺陷品質的小批量石英工廠。雖然這兩種材料都至關重要,但利潤來源正從石英轉向用於折疊式設備的新型玻璃陶瓷混合材料,這些材料兼具柔軟性和耐刮擦性。

區域分析

預計到2025年,亞太地區將以48.82%的市佔率主導玻璃基板市場,並將在2031年之前維持最高的複合年成長率(CAGR),達到4.19%。中國的京東方(BOE)、華星光電(CSOT)和香港晶圓廠(HKC)佔據了全球TFT-LCD產能的很大一部分,從而產生了對硼矽酸玻璃的巨大需求。日本繼續主導EUV光刻掩模坯的合成石英供應,而韓國則在超薄玻璃和折疊式OLED的創新方面處於領先地位。台灣的晶圓代工廠叢集消耗石英坯和玻璃基板,台積電(TSMC)在亞利桑那州和熊本縣的擴張正在亞太地區以外建立第二生產基地。 Vedanta-AvanStrate在印度的投資表明,新興的本土基板生產基地正在形成,旨在服務當地的智慧型手機和電視組裝。

北美市場的成長主要由半導體封裝和汽車顯示器項目驅動,而非通用液晶顯示器(LCD)生產。英特爾位於俄亥俄州和亞利桑那州的晶圓廠計畫進行面板級玻璃芯基板檢驗,而Absolix在CHIPS計畫支援下建造的工廠將成為美國首個此類製造地。康寧位於紐約州和北卡羅來納州的工廠為區域電子和汽車OEM製造商供應大猩猩玻璃、超薄玻璃(UTG)和精密光學元件。美國、加拿大和墨西哥的汽車製造商正在其2026-2027款車型中整合全擋風玻璃抬頭顯示器(HUD),這將推動對曲面玻璃鏡和全像層壓板的需求成長。

歐洲對玻璃基板的需求主要由德國、法國和英國的強勁消費所驅動。肖特公司對其電熔爐維修,象徵歐洲在脫碳方面的努力;該公司於2024年收購石英玻璃專家QSIL,進一步鞏固了其在極紫外光刻領域的戰略擴張。 BMW和賓士等汽車製造商正在採用採用蔡司和Panasonic光學元件層壓在高透明度玻璃上的防反射擋風玻璃。能源成本上漲和日益嚴格的排放法規正在擠壓通用硼矽酸玻璃的利潤空間,促使歐洲製造商轉向高利潤的利基產品和節能型熔煉技術。

在南美洲、中東和非洲,對玻璃基板(主要是浮法玻璃)的需求不斷成長,主要用於建築和汽車應用,但它們在半導體和先進顯示器市場的參與度有限。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 液晶顯示器(LCD)在家用電子電器。

- 半導體生產線擴建

- 汽車和AR/VR顯示器的需求不斷成長

- 高效率太陽能電池的發展

- 先進封裝中玻璃芯基板的興起

- 市場限制因素

- 高昂的製造成本和資本成本

- 持續的供應鏈波動和不斷上漲的能源價格

- 嚴格的硼排放環境法規

- 價值鏈分析

- 波特五力模型

- 技術概述

第5章 市場規模與成長預測

- 材料類型

- 硼矽酸玻璃

- 矽

- 陶瓷製品

- 石英

- 其他類型(藍寶石、鋁矽酸鹽等)

- 透過使用

- 顯示面板

- 半導體

- 太陽能電池

- 其他用途

- 按最終用戶行業分類

- 電子設備

- 車

- 航太/國防

- 醫學領域

- 太陽能

- 其他終端用戶產業(設備製造、電信等)

- 按地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 南非

- 奈及利亞

- 埃及

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- AGC Inc.

- AvanStrate Inc.

- Corning Incorporated

- HOYA Corporation

- Irico Group New Energy Company Limited

- Kyocera Corporation

- Nippon Electric Glass Co., Ltd.

- Nitto Boseki Co., Ltd.

- Ohara Inc.

- Planoptik AG

- Saint-Gobain

- Samtec

- SCHOTT AG

- SHENZHEN LAIBAO HI-TECH CO., LTD

- TOPPAN Holdings Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the glass substrate market size was valued at USD 7.14 billion in 2025 and is estimated to grow from USD 7.42 billion in 2026 to reach USD 9.01 billion by 2031, at a CAGR of 3.96% during the forecast period (2026-2031).

This report is Segmented by Material Type (Borosilicate, Silicon, and Other Types), Application (Display Panels, Semiconductors, and More), End-User Industry (Electronics, Automotive, Aerospace and Defense, Medical, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Glass Substrate Market Trends and Insights

Growing Usage of LCDs in Consumer Electronics

Persistent LCD volumes in mid-range smartphones, tablets, and monitors keep the glass substrates market firmly anchored in Asia-Pacific manufacturing hubs. Large-format gaming and professional monitors are now adopting thinner, lighter substrates to enable borderless designs that cut shipping weight and curb panel breakage. The mix shift toward higher value LCD panels favors suppliers capable of precision thinning and surface treatments alongside commodity-scale output. These dual capabilities strengthen incumbent positions for vertically integrated producers that can amortize R&D across multiple applications. Display OEM roadmaps also signal incremental glass demand from automotive infotainment retrofits, where existing LCD fabs redeploy capacity toward curved cockpit clusters.

Expansion of Semiconductor Fabrication Lines

The USD 150 billion wave of new fabs announced by Intel, Samsung, and TSMC through 2030 is reshaping the glass substrates market. Demand is ramping across three vectors: quartz photomask blanks for EUV patterning, glass-core substrates for 2.5D and 3D packages, and chemically inert inspection windows used in extreme-clean-room environments. Rapidus's demonstration of a 600 mm X 600 mm glass panel promises 10-fold chip yield relative to silicon interposers, highlighting the area-economy edge of rectangular glass panels over round wafers. Early design wins in this ecosystem lock suppliers into long qualification cycles, rewarding those who scale capacity in tandem with foundry outputs.

High Manufacturing and Capital Costs

Greenfield float or fusion-draw lines cost USD 200 million-USD 500 million, with melting furnaces consuming up to 40% of initial outlays. SCHOTT's EUR 40 million electric-melting retrofit at Mainz highlights the capex premium of decarbonization, yet integrated players deem it essential to hedge energy volatility. Specialty paths-ultra-thin glass, quartz blanks-stack extra investments in chemical strengthening, polishing, and Class 1 clean rooms, pushing fully loaded project costs above USD 300 million. This barrier consolidates the glass substrates market around incumbents capable of cross-subsidizing long paybacks with broad product portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Automotive and AR/VR Displays

- Emergence of Glass Core Substrates in Advanced Packaging

- Persistent Supply-Chain Volatility and Energy Price Spikes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Borosilicate glass accounted for 45.76% of the glass substrates market size in 2025 and continues to underpin TFT-LCD production due to its thermal stability and cost advantage. Its share growth is slowing as legacy LCD capacity pivots toward automotive and industrial displays, yet the sheer throughput of Gen 8.5 and Gen 10.5 fabs keeps borosilicate volumes high. Suppliers are adding precision thinning and surface-treatment lines to command better margins, particularly for curved infotainment and larger gaming monitors. Meanwhile, quartz substrates are projected to post a 4.41% CAGR through 2031 on the back of EUV lithography's relentless scaling below 3 nm. Near-zero CTE and sub-ppb metallic purity push quartz unit pricing multiples higher than borosilicate, insulating margins from commodity swings.

Quartz's rising demand transforms supply chains: HOYA and Shin-Etsu's synthetic-quartz duopoly now invests in additional CVD reactors, while semiconductor OEMs co-fund capacity to avoid EUV blank shortages. The glass substrates market, therefore, bifurcates into high-volume borosilicate workshops chasing cost efficiencies and low-volume quartz operations emphasizing defect-free quality. Both materials remain indispensable, but profit pools skew toward quartz and emerging glass-ceramic hybrids for foldables that blend flexibility with scratch resistance.

Geography Analysis

Asia-Pacific dominated the glass substrates market with a 48.82% share in 2025 and is projected to post the highest 4.19% CAGR through 2031. China's BOE, CSOT, and HKC run the bulk of global TFT-LCD capacity, generating massive demand for borosilicate glass. Japan maintains control of the synthetic-quartz supply for EUV mask blanks, while South Korea spearheads ultra-thin glass and foldable OLED innovations. Taiwan's foundry cluster consumes quartz blanks and glass carriers, with TSMC's expansion in Arizona and Kumamoto creating secondary hubs outside the region. India's Vedanta-AvanStrate investment signals an emerging domestic substrate base aimed at local smartphone and TV assembly.

North America market growth is buoyed by semiconductor packaging and automotive display projects rather than commodity LCD output. Intel's Ohio and Arizona fabs will validate panel-scale glass-core substrates, and Absolics' CHIPS Act-supported plant anchors the first U.S. manufacturing footprint in this field. Corning's New York and North Carolina sites supply Gorilla Glass, UTG, and precision optics to regional electronics and vehicle OEMs. Automotive makers in the United States, Canada, and Mexico are integrating windshield-wide HUDs into 2026-2027 models, intensifying demand for curved glass mirrors and holographic laminates.

The European glass substrates demand is anchored by significant consumption in Germany, France, and the United Kingdom. SCHOTT's electric-melting retrofit showcases Europe's decarbonization push, while its 2024 acquisition of quartz-glass specialist QSIL strengthens strategic exposure to EUV lithography. Automotive OEMs such as BMW and Mercedes-Benz deploy AR windshields that rely on ZEISS and Panasonic optics laminated in high-clarity glass. Elevated energy costs and tighter emission norms pressure commodity borosilicate margins, driving European producers toward high-margin specialty segments and energy-efficient melting technologies.

South America and the Middle East & Africa are witnessing a rising demand for glass substrates, mostly float-glass for construction and autoglass, with limited exposure to semiconductor or advanced display markets.

- AGC Inc.

- AvanStrate Inc.

- Corning Incorporated

- HOYA Corporation

- Irico Group New Energy Company Limited

- Kyocera Corporation

- Nippon Electric Glass Co., Ltd.

- Nitto Boseki Co., Ltd.

- Ohara Inc.

- Planoptik AG

- Saint-Gobain

- Samtec

- SCHOTT AG

- SHENZHEN LAIBAO HI-TECH CO., LTD

- TOPPAN Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing usage of LCDs in consumer electronics

- 4.2.2 Expansion of semiconductor fabrication lines

- 4.2.3 Rising demand for automotive and AR/VR displays

- 4.2.4 Growth of high-efficiency photovoltaic cells

- 4.2.5 Emergence of glass core substrates in advanced packaging

- 4.3 Market Restraints

- 4.3.1 High manufacturing and capital costs

- 4.3.2 Persistent supply-chain volatility and energy price spikes

- 4.3.3 Stringent environmental regulations on boron emissions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

- 4.6 Technological Snapshot

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Borosilicate

- 5.1.2 Silicon

- 5.1.3 Ceramic

- 5.1.4 Quartz

- 5.1.5 Other Types (Sapphire, Aluminosilicate, etc.)

- 5.2 By Application

- 5.2.1 Display Panels

- 5.2.2 Semiconductors

- 5.2.3 Solar Cells

- 5.2.4 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace and Defense

- 5.3.4 Medical

- 5.3.5 Solar Power

- 5.3.6 Other End-user Industries (Equipment Manufacturing, Telecommunication, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 South Korea

- 5.4.1.4 India

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 AvanStrate Inc.

- 6.4.3 Corning Incorporated

- 6.4.4 HOYA Corporation

- 6.4.5 Irico Group New Energy Company Limited

- 6.4.6 Kyocera Corporation

- 6.4.7 Nippon Electric Glass Co., Ltd.

- 6.4.8 Nitto Boseki Co., Ltd.

- 6.4.9 Ohara Inc.

- 6.4.10 Planoptik AG

- 6.4.11 Saint-Gobain

- 6.4.12 Samtec

- 6.4.13 SCHOTT AG

- 6.4.14 SHENZHEN LAIBAO HI-TECH CO., LTD

- 6.4.15 TOPPAN Holdings Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

玻璃芯基板市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、裝置、製程、最終用戶、功能

玻璃芯基板市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、裝置、製程、最終用戶、功能 全球玻璃基板市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球玻璃基板市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球玻璃基板市場:按類型、終端應用產業和地區分類-預測(至2031年)

全球玻璃基板市場:按類型、終端應用產業和地區分類-預測(至2031年) 玻璃基板市場:按類型、類別、應用程式和最終用戶分類-2026-2032年全球市場預測玻璃基板印刷基板市場按材料類型、層數、技術、應用和終端用戶產業分類,全球預測(2026-2032)

玻璃基板市場:按類型、類別、應用程式和最終用戶分類-2026-2032年全球市場預測玻璃基板印刷基板市場按材料類型、層數、技術、應用和終端用戶產業分類,全球預測(2026-2032) 玻璃基板市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

玻璃基板市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 玻璃基板市場規模、佔有率和成長分析(按類型、晶圓直徑、應用、最終用途和地區分類)-2025-2032年產業預測

玻璃基板市場規模、佔有率和成長分析(按類型、晶圓直徑、應用、最終用途和地區分類)-2025-2032年產業預測 顯示玻璃基板:全球市佔率及排名、總收入及需求預測(2025-2031年)玻璃通孔 (TGV) 晶圓:全球市場佔有率和排名、總銷售額和需求預測 (2025-2031)硬碟玻璃基板市場(按材料類型、技術、尺寸、驅動功能、應用和分銷管道)—2025-2030 年全球預測

顯示玻璃基板:全球市佔率及排名、總收入及需求預測(2025-2031年)玻璃通孔 (TGV) 晶圓:全球市場佔有率和排名、總銷售額和需求預測 (2025-2031)硬碟玻璃基板市場(按材料類型、技術、尺寸、驅動功能、應用和分銷管道)—2025-2030 年全球預測