|

市場調查報告書

商品編碼

2066579

連網汽車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Connected Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

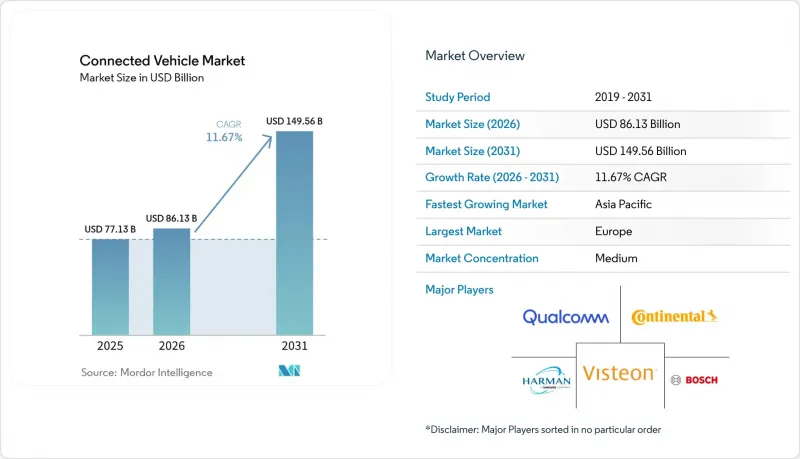

根據 Mordor Intelligence 預測,連網汽車市場規模將從 2025 年的 771.3 億美元成長到 2026 年的 861.3 億美元,然後在 2031 年達到 1,495.6 億美元,2026 年至 2031 年的複合年成長率為 11.67%。

本報告按技術類型(5G/C-V2X、4G/LTE、3G、2G)、應用領域(駕駛輔助、安全防護、車載資訊服務與診斷、其他)、連接方式(整合、嵌入式、網路共享)、車對車連接方式(V2V、V2I、V2P、V2C、V2G)、車輛類型和地區進行細分。市場預測以價值(美元)和數量(單位)兩種形式呈現。

全球連網汽車市場趨勢與洞察

全球 5G 部署將實現高頻寬V2X 服務。

自2024年起,3GPP Release 16的側鏈功能將實現極低延遲的車對車(V2V)直接通訊。到2025年底,中國憑藉其龐大的5G基地台運作中將發揮主導作用,許多基地台將支援C-V2X路側功能。為提升行人安全,韓國在2025年投入大量資金,升級眾多路口,部署低延遲V2X技術。同時,美國聯邦公路管理局(FHMA)強調了其致力於貨運走廊數位化建設的決心,計劃在2025年沿著主要州際公路安裝多個路側設備。由於這些技術進步,車輛現在可以享受空中韌體更新、高清地圖資訊和及時的危險預警。

eCall 和安全遠端資訊處理的監管要求

歐盟委員會授權條例2024/1180將於2025年1月生效,該條例強制要求所有新型輕型車輛從電路交換的eCall網路過渡到分封交換的IMS網路,並要求將2G和3G數據機更換為4G或5G晶片組。印度的AIS-140修正案3將於2026年4月前將即時追蹤和緊急按鈕的要求擴展到乘用車,進一步提高了合規要求。俄羅斯的ERA-GLONASS升級將於2024年增加LTE定位功能,進一步加強了法規的最低標準。雖然這些法規保證了最低連接性,但也導致工程成本增加,因為聯合國歐洲經濟委員會WP.29條例155強制要求在型式認證前安裝經認證的網路安全管理系統。為了保持競爭力,中小型原始設備製造商(OEM)需要與已獲得ISO/SAE 21434認證的一級供應商合作。

網路安全和資料隱私漏洞

近期,歐洲網路安全局報告了多起針對連網汽車閘道的攻擊事件,包括針對遠端解鎖和防盜系統的攻擊,這些攻擊影響了多種車型。儘管 ISO/SAE 21434 標準提供了一個流程框架,但 TÜV SÜD 的審計發現,相當一部分二級供應商並未完全合規,這凸顯了潛在的安全漏洞。 《一般資料保護規則》(GDPR) 透過高額罰款來阻礙力過度的資料貨幣化行為。同時,《加州消費者隱私法案》(CCPA) 賦予車主要求刪除其里程記錄的權利,這使得基於里程的保險模式變得更加複雜。為了應對這個問題,原始設備製造商 (OEM) 正在實施基於硬體的信任根模組和端對端加密。然而,合規的負擔正在減緩新功能的部署,並將研發預算轉移到防禦性技術措施。

細分市場分析

由於成熟的組件價格和全球網路覆蓋,4G/LTE 市場在 2025 年仍將佔據連網汽車市場 43.47% 的佔有率。然而,隨著原始設備製造商 (OEM) 致力於降低延遲,以滿足自動駕駛和高級駕駛輔助系統的需求,配備 5G/C-V2X 的汽車正以 11.69% 的複合年成長率快速成長,直至 2031 年。高通公司於 2025 年發布的「驍龍 X85」採用 4 奈米製程整合了側鍊和毫米波無線電功能,與傳統的獨立設計相比,功耗略有降低,組件成本也降低了 35 美元。傳統的 3G 和 2G 設備正根據美國和歐盟的服務終止計畫逐步淘汰,因此難以繼續運作。

儘管豪華轎車的 5G 普及率是輕型商用車的兩倍,但貨運公司仍然更傾向於使用功能強大的 4G 晶片組搭配電子行車記錄器。由於新能源車強制部署 LTE-V2X,中國對 4G 的需求依然旺盛,而歐洲正快速向 5G NR-V2X 過渡。支援 Release 14 側鍊和 Release 17 定位的雙模半導體成本已從 2023 年的 50 美元降至 15 美元,加速了跨區域全球平台的標準化進程。隨著規模經濟的擴大,預計到 2028 年,5G 數據機在連網汽車市場的佔有率將超過 4G,這將需要對供應鏈和半導體藍圖進行重組。

到2025年,安全相關服務將佔連網汽車市場規模的38.13%,eCall緊急呼叫系統的監管要求鞏固了潛在需求。空中下載(OTA)更新成長最快,複合年成長率達11.77%,這反映了汽車產業正向軟體定義型汽車轉型,這類汽車能夠接收數GB的韌體。到2025年,光是特斯拉車隊就將上傳超過Petabyte的感測器數據,從而實現基於雲端的訓練和快速的功能發布。駕駛輔助功能正在與V2X資料流整合;例如,BMW的高速公路輔助系統現在將從路邊單元即時傳輸的施工區域資料整合到其自適應速度曲線中。

在蘋果 CarPlay 和安卓 Auto 的主導地位下,車載資訊娛樂和人機互動 (HMI) 功能正趨於同質化,降低了原始設備製造商 (OEM) 之間的差異化優勢。移動出行和車隊管理應用正向大型供應商集中,這些供應商為數百萬輛商用車最佳化路線、合規性和維護。同時,遠端資訊處理和診斷技術正從售後市場適配器轉向原廠閘道器,這些閘道器將車輛狀態資料傳輸到雲端進行分析,從而減少了計劃外維修次數。透過一次更新即可在單一有效載荷中解決安全性、性能和娛樂問題,這打破了傳統的應用孤島,整合軟體管道的重要性日益凸顯。

區域分析

預計到2025年,歐洲將佔據連網汽車市場34.57%的主導地位。這一成長主要得益於eCall向分封交換過渡的最後期限以及大量C-Roads路邊設備的部署。這些設備在德國、奧地利和荷蘭提供危險警報。德國擁有最高的部署密度,高速公路沿線安裝了大量運作中的設備。相較之下,英國由於脫歐後監管差異,部署速度較慢。南歐國家的部署速度也較為緩慢,主要是因為消費者對使用費的抗拒。

預計到2031年,亞太地區的年複合成長率(CAGR)將達到11.75%,位居全球之首。這主要得益於中國強制新能源車安裝LTE-V2X技術,以及在無錫、長沙和重慶等城市部署V2X基礎設施的進展。無錫已安裝的1200套路側設備已展現出顯著的安全效益,預計到2025年將有效減少十字路口交通事故。日本和韓國正在資助都市區V2X試點項目,以維修數百個十字路口。同時,印度的AIS-140第三次修訂案將於2026年擴大乘用車即時追蹤的範圍,為合規性增添了新的推動因素。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球 5G 部署將實現高頻寬V2X 服務。

- eCall 和安全遠端資訊處理的監管要求

- 美國、歐盟和中國的智慧基礎設施資金籌措

- 消費者對車載資訊娛樂和連網功能的需求

- 以電動車為中心的軟體定義車輛架構

- 保險公司和汽車製造商 (OEM) 在基於里程的保險方面合作

- 市場限制因素

- 網路安全和資料隱私漏洞

- 高昂的行動資料通訊費用以及OEM廠商和MNO廠商之間的收入糾紛。

- 半導體調變解調器供不應求

- DSRC 與 C-V2X:頻段選擇的不確定性

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依技術類型

- 5G/C-V2X

- 4G/LTE

- 3G

- 2G

- 透過使用

- 駕駛輔助系統(ADAS)

- 安全保障

- 遠端資訊處理與診斷

- 資訊娛樂和人機交互

- 移動性和車隊管理

- 空中下載 (OTA) 更新

- 連結性別

- 融合的

- 嵌入式

- 繫繩

- 車輛連接性別

- Vehicle-to-Vehicle(V2V)

- Vehicle-to-Infrastructure(V2I)

- Vehicle-to-Pedestrian(V2P)

- Vehicle-to-Cloud(V2C)

- Vehicle-to-Grid(V2G)

- 車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型商用車輛

- 按終端市場分類

- OEM配備型

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Visteon Corporation

- Samsung Electronics(HARMAN)

- Qualcomm Technologies Inc.

- NXP Semiconductors

- Aptiv PLC

- ZF Friedrichshafen AG

- Magna International

- Infineon Technologies AG

- AT&T Inc.

- Verizon Communications Inc.

- TomTom NV

- Tesla Inc.

- Toyota Motor Corporation

- BMW Group

- Ford Motor Company

- General Motors Company

- Huawei Technologies Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the connected vehicle market size is expected to grow from USD 77.13 billion in 2025 to USD 86.13 billion in 2026 and is forecast to reach USD 149.56 billion by 2031 at an 11.67% CAGR over 2026-2031.

This report is Segmented by Technology Type (5G/C-V2X, 4G/LTE, 3G, and 2G), Application (Driver Assistance, Safety and Security, Telematics and Diagnostics, and More), Connectivity (Integrated, Embedded, and Tethered), Vehicle Connectivity (V2V, V2I, V2P, V2C, and V2G), Vehicle Type, and Geography. Market Forecasts are Provided in Value (USD) and Volume (Units).

Global Connected Vehicle Market Trends and Insights

Global 5G Roll-Outs Enabling High-Bandwidth V2X Services

Since 2024, the 3GPP Release 16 sidelink feature has enabled direct vehicle-to-vehicle messaging with extremely low latency. By the end of 2025, China, with a significant number of active 5G base stations, will lead the charge, with many stations facilitating C-V2X roadside functions . In a bid to enhance pedestrian safety, South Korea allocated substantial funding in 2025 to upgrade numerous intersections with low-latency V2X technology. Meanwhile, in the U.S., the Federal Highway Administration underscored its commitment to digitizing freight corridors by adding several roadside units along a major interstate in 2025 . Due to these advancements, vehicles can now benefit from over-the-air firmware updates, high-definition mapping, and timely hazard alerts.

Regulatory Mandates For eCall & Safety Telematics

European Commission Delegated Regulation 2024/1180, effective January 2025, compels all new light vehicles to migrate from circuit-switched eCall to packet-switched IMS networks, forcing the replacement of 2G and 3G modems with 4G or 5G chipsets . India's AIS-140 Amendment 3 extends real-time tracking and panic-button requirements to passenger cars by April 2026, deepening compliance demand. Russia's ERA-GLONASS upgrade added LTE positioning in 2024, further solidifying the regulatory floor. These rules guarantee baseline connectivity but also raise engineering costs, since UNECE WP.29 Regulation 155 mandates a certified cyber-security management system before type approval. Smaller OEMs must now partner with tier-1 suppliers that already hold ISO/SAE 21434 certification to stay competitive.

Cyber-Security & Data-Privacy Vulnerabilities

In recent times, the European Union Agency for Cybersecurity reported several exploits targeting connected-vehicle gateways. These included remote unlock and immobilizer attacks affecting multiple vehicle models. While ISO/SAE 21434 provides a framework for processes, a TUV SUD audit revealed that a significant portion of tier-2 suppliers were not fully compliant, highlighting potential vulnerabilities. The General Data Protection Regulation (GDPR) imposes substantial fines, acting as a deterrent against aggressive data monetization. Meanwhile, the California Consumer Privacy Act empowers drivers to request the deletion of their trip records, adding complexity to usage-based insurance models. In response, Original Equipment Manufacturers (OEMs) are implementing hardware root-of-trust modules and end-to-end encryption. However, the weight of compliance is delaying the rollout of new features and redirecting R&D budgets towards defensive engineering measures.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Infrastructure Funding In United States, European Union, And China

- Consumer Demand for In-Car Infotainment & Connectivity

- High Cellular Data Costs And OEM-MNO Revenue Conflicts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 4G/LTE segment maintained a 43.47% slice of the connected vehicle market size in 2025, benefiting from mature component pricing and global network coverage. However, 5G/C-V2X units are scaling fast with an 11.69% CAGR through 2031 as OEMs chase latency improvements vital for autonomous driving and advanced driver assistance. Qualcomm's Snapdragon X85, announced in 2025, integrates sidelink and millimeter-wave radios on a 4-nanometer node, cutting power draw by a minimal amount and reducing bill-of-materials by USD 35 relative to earlier discrete designs. Legacy 3G and 2G devices are being sunset, aligning with U.S. and EU shutdown schedules that make continued operation unsustainable.

Premium passenger cars adopt 5G twice as often as light commercial vehicles, but freight operators still favor robust 4G chipsets paired with electronic logging devices. China's mandate for LTE-V2X in new-energy vehicles keeps 4G volumes high, while Europe leans straight into 5G NR-V2X. Dual-mode silicon that supports Release 14 sidelink and Release 17 positioning now adds only USD 15, down from USD 50 in 2023, helping global platforms standardize across regions. As economies of scale build, the connected vehicle market expects 5G modems to overtake 4G share before 2028, reshaping supply chains and semiconductor roadmaps.

Safety and security services held 38.13% of the connected vehicle market size in 2025 as regulatory eCall mandates locked in baseline demand. Over-the-air updates post the quickest climb at an 11.77% CAGR, reflecting the move to software-defined vehicles capable of receiving multi-gigabyte firmware packages. Tesla's fleet alone uploaded more than 4 petabytes of sensor data in 2025, enabling cloud training and rapid feature releases. Driver assistance merges with V2X feeds, as BMW's Highway Assistant now factors real-time work-zone data streamed from roadside units into adaptive speed profiles.

Infotainment and human-machine interface functions are commoditizing under Apple CarPlay and Android Auto dominance, compressing OEM differentiation. Mobility and fleet-management applications consolidate around scaled providers that optimize routing, compliance, and maintenance for millions of commercial vehicles. Meanwhile, telematics and diagnostics shift from aftermarket dongles to factory-installed gateways that stream health data to cloud analytics, cutting unscheduled service visits. Traditional application silos blur as a single update can address security, driveability, and entertainment in one payload, underscoring the growing importance of unified software pipelines.

Geography Analysis

Europe dominated with 34.57% of the connected vehicle market share in 2025. This surge was driven by the eCall packet-switched migration deadlines and the deployment of numerous C-Roads roadside units. These units stream hazard alerts across Germany, Austria, and the Netherlands. Germany boasts the highest density with a significant number of active units along its Autobahn corridors. In contrast, the United Kingdom faces delays, grappling with post-Brexit regulatory differences. Southern European nations are adopting at a slower pace, hindered by consumer resistance to subscription fees.

Asia Pacific posts the fastest 11.75% CAGR through 2031 as China mandates LTE-V2X on new-energy vehicles and channels into V2X infrastructure across Wuxi, Changsha, and Chongqing. Wuxi's 1,200 roadside units cut intersection accidents in 2025, proving safety dividends. Japan and South Korea fund urban V2X pilots that retrofit hundreds of intersections, while India's AIS-140 Amendment 3 extends real-time tracking to passenger cars by 2026, adding a compliance driver.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Visteon Corporation

- Samsung Electronics (HARMAN)

- Qualcomm Technologies Inc.

- NXP Semiconductors

- Aptiv PLC

- ZF Friedrichshafen AG

- Magna International

- Infineon Technologies AG

- AT&T Inc.

- Verizon Communications Inc.

- TomTom N.V.

- Tesla Inc.

- Toyota Motor Corporation

- BMW Group

- Ford Motor Company

- General Motors Company

- Huawei Technologies Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global 5G Roll-Outs Enabling High-Bandwidth V2X Services

- 4.2.2 Regulatory Mandates for Ecall & Safety Telematics

- 4.2.3 Smart-Infrastructure Funding in US, EU, China

- 4.2.4 Consumer Demand for In-Car Infotainment & Connectivity

- 4.2.5 EV-Centric Software-Defined Vehicle Architectures

- 4.2.6 Insurance-OEM Usage-Based-Insurance Partnerships

- 4.3 Market Restraints

- 4.3.1 Cyber-Security & Data-Privacy Vulnerabilities

- 4.3.2 High Cellular Data-Costs And OEM - MNO Revenue Conflicts

- 4.3.3 Semiconductor Modem Shortages

- 4.3.4 DSRC Vs C-V2X Spectrum Uncertainty

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Technology Type

- 5.1.1 5G / C-V2X

- 5.1.2 4G / LTE

- 5.1.3 3G

- 5.1.4 2G

- 5.2 By Application

- 5.2.1 Driver Assistance (ADAS)

- 5.2.2 Safety and Security

- 5.2.3 Telematics & Diagnostics

- 5.2.4 Infotainment & HMI

- 5.2.5 Mobility & Fleet Management

- 5.2.6 Over-the-Air (OTA) Updates

- 5.3 By Connectivity

- 5.3.1 Integrated

- 5.3.2 Embedded

- 5.3.3 Tethered

- 5.4 By Vehicle Connectivity

- 5.4.1 Vehicle-to-Vehicle (V2V)

- 5.4.2 Vehicle-to-Infrastructure (V2I)

- 5.4.3 Vehicle-to-Pedestrian (V2P)

- 5.4.4 Vehicle-to-Cloud (V2C)

- 5.4.5 Vehicle-to-Grid (V2G)

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles

- 5.5.3 Medium and Heavy Commercial Vehicles

- 5.6 By End Market

- 5.6.1 OEM-Fitted

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Turkey

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 Visteon Corporation

- 6.4.5 Samsung Electronics (HARMAN)

- 6.4.6 Qualcomm Technologies Inc.

- 6.4.7 NXP Semiconductors

- 6.4.8 Aptiv PLC

- 6.4.9 ZF Friedrichshafen AG

- 6.4.10 Magna International

- 6.4.11 Infineon Technologies AG

- 6.4.12 AT&T Inc.

- 6.4.13 Verizon Communications Inc.

- 6.4.14 TomTom N.V.

- 6.4.15 Tesla Inc.

- 6.4.16 Toyota Motor Corporation

- 6.4.17 BMW Group

- 6.4.18 Ford Motor Company

- 6.4.19 General Motors Company

- 6.4.20 Huawei Technologies Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

全球聯網汽車市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球聯網汽車市場規模、佔有率、趨勢和成長分析報告(2026-2034) 互聯行動平台市場預測至2034年-按平台類型、部署模式、應用、最終用戶和地區分類的全球分析聯網汽車資訊服務市場預測至2034年-按服務類型、資料類型、部署模式、車輛類型、最終使用者和地區分類的全球分析

互聯行動平台市場預測至2034年-按平台類型、部署模式、應用、最終用戶和地區分類的全球分析聯網汽車資訊服務市場預測至2034年-按服務類型、資料類型、部署模式、車輛類型、最終使用者和地區分類的全球分析 聯網汽車市場規模、佔有率、趨勢和預測:按技術、互聯解決方案、服務、終端市場和地區分類,2026-2034 年

聯網汽車市場規模、佔有率、趨勢和預測:按技術、互聯解決方案、服務、終端市場和地區分類,2026-2034 年 聯網汽車生態系統市場規模、佔有率和成長分析:按連接類型、技術、應用、車輛類型、銷售管道和地區分類-2026-2033年產業預測

聯網汽車生態系統市場規模、佔有率和成長分析:按連接類型、技術、應用、車輛類型、銷售管道和地區分類-2026-2033年產業預測 聯網汽車市場規模、佔有率和成長分析:按連接技術、服務類型、通訊方式、車輛類型、最終用戶和地區分類-2026-2033年產業預測

聯網汽車市場規模、佔有率和成長分析:按連接技術、服務類型、通訊方式、車輛類型、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球聯網汽車市場

2026-2030年全球聯網汽車市場 聯網汽車市場:2026-2032年全球市場預測(按組件類型、連接技術、通訊方式、網路類型、應用、車輛類型和最終用戶分類)聯網汽車市場:按連接類型、通訊技術、車輛類型、提供的服務和應用分類-2026-2032年全球市場預測

聯網汽車市場:2026-2032年全球市場預測(按組件類型、連接技術、通訊方式、網路類型、應用、車輛類型和最終用戶分類)聯網汽車市場:按連接類型、通訊技術、車輛類型、提供的服務和應用分類-2026-2032年全球市場預測 聯網汽車市場:按車輛類型、最終用戶行業、通訊類型、連接性別和地區分類

聯網汽車市場:按車輛類型、最終用戶行業、通訊類型、連接性別和地區分類