|

市場調查報告書

商品編碼

2066537

MEMS能源採集裝置:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)MEMS Energy Harvesting Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

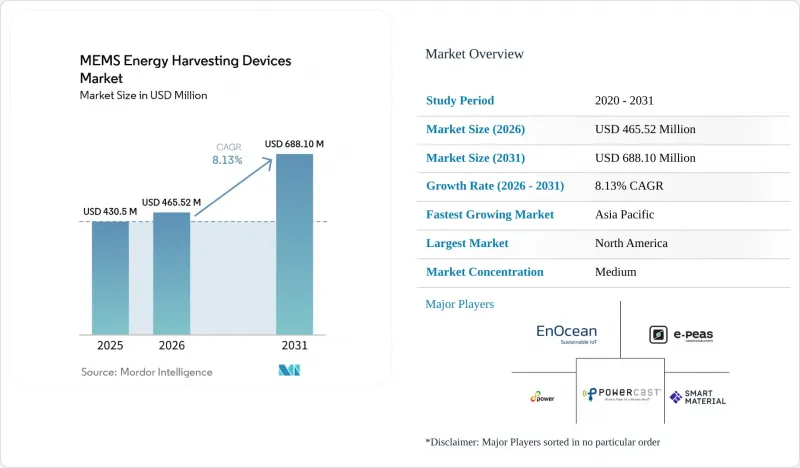

根據 Mordor Intelligence 預測,MEMS能源採集設備市場預計將從 2025 年的 4.305 億美元成長到 2026 年的 4.6552 億美元,然後在 2031 年達到 6.881 億美元,2026 年至 2031 年的複合年成長率為 8.13%。

本報告按技術(太陽能能源採集、能源採集等)、部署類型(有線系統、無線系統)、供電範圍(低功率設備、中高功率設備)、終端用戶產業(建築和家庭自動化、家用電子電器等)以及地區進行細分。市場預測以美元計價。

全球MEMS能源採集元件市場趨勢及洞察

無電池無線感測網路。

MEMS能源採集元件市場的發展主要得益於無電池無線感測網路的廣泛部署。即使在小規模工業環境中,無線通訊也已實現,但由於維護依賴儲存化學能的感測器節點需要耗費大量人力,大規模更換電池仍然是一項隱性的營運負擔。環境物聯網架構透過將能源採集與低佔空比通訊相結合來解決此問題,使節點無需傳統電池即可進行傳輸。 2026年的一項研究表明,採用自適應資料分配的能源採集無線感測器節點能夠以12µJ的能量傳輸128位元資料包,比始終運作的節點能耗降低了88%。 IEEE 802.11 TGbp中關於環境電源通訊的標準化工作正在規範無電池終端的認證流程,從而推動MEMS能源採集元件市場生態系統的進一步發展。這項變化意義重大。這是因為在 MEMS能源採集設備市場,從有限的先導計畫到在建築物、工廠和基礎設施中可複製的大規模部署的路徑已經變得更加清晰。

工業狀態監測和預測性維護的發展

MEMS能源採集元件市場成長的最直接驅動力是無電池無線感測網路的廣泛部署。大規模電池更換仍然是一項隱性的運作負擔,因為即使在小規模工業設施中,工作人員也需要花費大量時間來維護依賴儲存化學能的感測器節點,即便通訊是無線的。環境物聯網架構透過將能源採集與低佔空比通訊相結合來解決此問題,使節點無需傳統電池即可進行傳輸。根據2026年發表在《感測器》(Sensors)雜誌上的一項研究,採用自適應資料分配的能源採集無線感測器節點可以以12µJ的能耗傳輸128位元資料包,比始終運作的節點能耗降低88%。 IEEE 802.11 TGbp中關於環境電源通訊的標準化工作正在明確無電池終端的認證流程,這正在推動MEMS能源採集元件市場更廣泛生態系統的形成。這一轉變意義重大,因為它使 MEMS能源採集設備市場從有限的先導計畫到在建築物、工廠和基礎設施中可複製的大規模部署的道路更加清晰。

電力輸出有限,間歇性依賴環境能源

輸出功率限制仍是MEMS能源採集元件市場面臨的最大限制因素。工業環境中典型的環境能源採集元件只能產生數十到幾百微瓦的功率,足以滿足週期性的低資料速率通訊需求,但無法滿足持續的高運算負載操作。當環境能量損失時,例如夜間室內照明變暗、設備停機導致溫度梯度消失或機器運作期間振動中斷能源採集,這個問題會變得更加嚴重。設計人員可以透過採用混合能源採集或大容量儲能緩衝器來解決這個問題,但這兩種方案都會增加成本、系統體積和設計複雜性。因此,在需要在波動的工作條件下保持可靠性能的應用中,完全消除電池是困難的。在能夠更穩定地預測和儲存能量之前,MEMS能源採集元件市場對低佔空比應用場景的需求可能仍將高於持續高負載運行的需求。

細分市場分析

到2025年,振動和壓電能源採集將佔MEMS能源採集元件市場44.23%的佔有率,成為最大的技術領域。這一主導地位源自於大量可產生機械能的機械設備,以及壓電轉換與旋轉設備監控之間極佳的兼容性。 2025年發表在《智慧材料與結構》(Smart Materials and Structures)期刊上的一項研究表明,可變截面多模態壓電採集器可透過結構最佳化提高寬頻能量採集性能,並直接解決諧振失配導致的實際部署限制。光電發電仍是重要的輔助技術途徑。 2026年1月,Dracula Technologies公司宣布,其有機太陽能電池平台LAYER V2.0在室內應用的效能比上一代產品提升了30%。

熱能能源採集佔據了一個雖小但具有重要戰略意義的細分市場,該市場適用於周圍存在穩定溫差的高發熱設備。能源採集是MEMS能源採集元件市場中成長最快的技術,預計到2031年將以8.78%的年成長率成長,因為物聯網標籤將擴大利用現有的無線基礎設施供電。 2026年1月,Wiliot宣布其「第三代物聯網像素」採用雙頻架構,涵蓋2.4 GHz和1 GHz以下頻段,與上一代產品相比,提高了能源採集效率和供電範圍。此外,2026年發表在《Micromachines》期刊上的一篇論文展示了一種基於BQ25504供電路徑的射頻能源採集物聯網網路架構。同時,IEEE 802.11 TGbp正在持續建構經認證的環境電源通訊框架。

到2025年,無線系統將佔據部署市場佔有率的72.45%,並將成為成長最快的類別,預計到2031年將維持9.23%的年均成長率。這種主導地位體現了無線系統最大的價值,因為它無需電池維護,同時也能消除電源線和數據線。在能源採集設備市場,這意味著無線連接將成為在建築物和分散式工業環境中部署大規模感測器集群的事實標準。 Atmosic公司表示,其平台支援超低功耗連接,整合了能源採集和IEEE 802.15.4功能,減輕了系統開發人員的整合負擔。

當延遲、頻寬或電磁干擾等限制導致無線連線不適用時,有線系統仍然發揮著至關重要的作用。在某些工業環境中,電源和通訊功能是分離的,例如在感測器端使用能源採集來供電,同時保持有線資料路徑以確保可靠性。由於應用需求特殊且相對有限, 能源採集元件市場的這一細分領域保持穩定。因此,市場呈現出兩極化的格局:無線方案佔據了新部署的大部分佔有率,而有線設計仍僅限於對效能要求較高的應用場景。

區域分析

2025年,北美持續維持領先地位,佔據MEMS能源採集元件市場32.78%的佔有率。美國仍然是主要的收入來源,因為工業狀態監測、智慧建築維修和資料中心感測等技術的商業性進程早於許多其他地區。 2025年,EnOcean宣布其能源採集解決方案已入選DesignLights聯盟的合格產品清單,從而可以申請美國公共產業公司的補貼。加拿大和墨西哥在該地區仍然是相對小規模的市場,但兩國在採礦、石油天然氣和製造業等行業的應用案例支撐了市場需求,這些行業非常適合基於振動的感測技術。北美在能源採集元件市場的區域主導地位得益於其完善的數位基礎設施和鼓勵高效能無線建築控制的法規環境。

歐洲仍然是重要的區域市場,主要由德國、英國、法國、義大利和西班牙推動。歐洲的需求與能源效率和工業法令遵循密切相關,這些法規正在推動建築和製程環境中低維護感測器的應用。 2025年11月,歐盟委員會通過了(EU) 2025/2363號指令,為壓電PZT陶瓷中的鉛設立了第7(c)-VI條豁免條款,有效期至2027年12月31日。這為供應商提供了明確的規劃期,同時促進了無鉛替代品的推廣。瑞典也成為重要的太陽能收集中心,瑞典能源署於2025年向Exeger公司津貼1.3億瑞典克朗(約1,220萬美元),用於擴展其室內太陽能電池技術。雖然南美洲、中東和非洲的市場規模仍然較小,但採礦和智慧城市計畫正在創造對免維護感測技術的實際需求。

亞太地區是MEMS能源採集元件市場成長最快的地區,預計到2031年將以年均8.94%的速度成長。這一成長趨勢得益於中國大規模物聯網基礎設施的建設、日本在壓電材料領域的優勢、韓國的電源管理積體電路(PMIC)生態系統以及印度建築和製造業數位化進程的推進。 CiNii發布的2026年調查說明指出,可以透過玻璃表面向建築管理感測器模組進行無線電力傳輸,這與日本傾向於在維修設計中盡量減少對現有設施的影響的理念相契合。新加坡、馬來西亞和泰國等東南亞國協也正在將物流和製造場所的環境物聯網感測技術從試點階段推進到生產規模。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 無電池無線感測器網路的廣泛應用

- 智慧建築的擴展和現有建築控制系統的維修。

- 工業狀態監測和預測性維護的發展

- 超低功耗電源管理積體電路和無線系統單晶片技術的進步

- 環境聯網協定的標準化催生了一類新型的認證自供電設備。

- 需要消除電池卡車在難以接近的旋轉資產中的移動。

- 市場限制因素

- 產量限制和對間歇性環境能源的依賴

- 壓電MEMS設計中的窄頻寬和諧振失配

- 關於壓電陶瓷不受 RoHS 鉛法規限制的不確定性

- 微型儲能路徑中的洩漏損失和冷啟動瓶頸

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 市場宏觀經濟趨勢的評估

第5章 市場規模與成長預測

- 透過技術

- 太陽能(太陽能發電)能源採集

- 振動和壓電式能量採集

- 能源回收

- 射頻能源採集

- 依部署類型

- 有線系統

- 無線系統

- 透過供電方式

- 低功耗設備

- 中高功率設備

- 按最終用戶行業分類

- 建築和家庭自動化

- 工業和製造業

- 家用電子產品

- 運輸/物流

- 醫療保健和醫療設備

- 航太/國防

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- EnOcean GmbH

- e-peas SA

- 8power Limited

- Powercast Corporation

- Smart Material Corporation

- EH4 GmbH

- Smart Material GmbH

- ReVibe Energy AB

- MEMSYS BV

- Enervibe Ltd.

- Pyro-E, Inc.

- WePower Technologies LLC

- Everactive, Inc.

- Atmosic, Inc.

- Wiliot Ltd.

- Dracula Technologies SAS

- Exeger Sweden AB(publ)

- EPISHINE AB

- Cymbet Corporation

- MicroGen Systems, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the mEMS energy harvesting devices market size is expected to grow from USD 430.50 million in 2025 to USD 465.52 million in 2026 and is forecast to reach USD 688.10 million by 2031 at 8.13% CAGR over 2026-2031.

This report is Segmented by Technology (Solar (Photovoltaic) Energy Harvesting, Thermal Energy Harvesting, and More), Deployment Type (Wired Systems, and Wireless Systems), Powering Range (Low-Power Devices, and Medium-To-High Power Devices), End-User Industry (Building and Home Automation, Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global MEMS Energy Harvesting Devices Market Trends and Insights

Rising Adoption of Battery-Free Wireless Sensor Networks

The MEMS energy harvesting devices market has been pushed most directly by the wider rollout of battery-free wireless sensor networks. Battery replacement at scale remains a hidden operating burden because even modest industrial sites spend large amounts of staff time servicing sensor nodes that are wireless in communication but still dependent on stored chemical energy. Ambient IoT architectures address this issue by pairing energy harvesting with low-duty-cycle communication so nodes can transmit without carrying a conventional battery. A 2026 study showed that energy-harvesting wireless sensor nodes using adaptive data allocation transmitted a 128-bit packet with 12 µJ of energy, which was 88% lower than continuously active nodes. Standardization work around ambient power communication in IEEE 802.11 TGbp is creating clearer certification pathways for battery-free endpoints, which supports broader ecosystem formation for the MEMS energy harvesting devices market. That shift matters because the MEMS energy harvesting devices market now has a clearer route from limited pilots to repeatable fleet deployments in buildings, factories, and infrastructure.

Growth in Industrial Condition Monitoring and Predictive Maintenance

The MEMS energy harvesting devices market is being pushed most directly by the wider rollout of battery-free wireless sensor networks. Battery replacement at scale remains a hidden operating burden because even modest industrial sites spend large amounts of staff time servicing sensor nodes that are wireless in communication but still dependent on stored chemical energy. Ambient IoT architectures address this issue by pairing energy harvesting with low-duty-cycle communication so nodes can transmit without carrying a conventional battery. A 2026 study in Sensors shows that energy-harvesting wireless sensor nodes using adaptive data allocation transmit a 128-bit packet with 12 µJ of energy use, which is 88% lower than continuously active nodes. Standardization work around ambient power communication in IEEE 802.11 TGbp is creating clearer certification pathways for battery-free endpoints, which supports broader ecosystem formation for the MEMS energy harvesting devices market. That shift matters because the MEMS energy harvesting devices market now has a clearer route from limited pilots to repeatable fleet deployments in buildings, factories, and infrastructure.

Limited Power Output and Dependence on Intermittent Ambient Energy

Limited power output remains the most binding restraint on the MEMS energy harvesting devices market. Typical ambient harvesters in industrial settings generate tens to hundreds of microwatts, which supports periodic low-data-rate transmission but not sustained compute-heavy operation. The problem becomes harder when ambient energy disappears, because indoor light drops at night, thermal gradients collapse when equipment stops, and vibration harvesting pauses during machine downtime. Designers can respond with hybrid harvesting or larger storage buffers, but both options add cost, system volume, and design complexity. That makes full battery elimination difficult in applications that require reliable performance across variable operating conditions. Until energy availability can be predicted and buffered with greater consistency, the MEMS energy harvesting devices market will remain strongest in low-duty-cycle use cases rather than continuous high-load operation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Smart Buildings and Retrofit Building Controls

- Advances In Ultra-Low-Power PMICs and Wireless SoCs

- Narrow Bandwidth and Resonance Mismatch in Piezoelectric MEMS Designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vibration and piezoelectric energy harvesting held 44.23% of the MEMS energy harvesting devices market size in 2025, making it the largest technology segment. This lead arose from the large installed base of machines that generate usable mechanical energy and from the strong fit between piezoelectric conversion and rotating asset monitoring. A 2025 study in "Smart Materials and Structures" showed that variable-section multimodal piezoelectric harvesters improved broadband capture through structural optimization, directly addressing real deployment limits caused by resonance mismatch. Solar harvesting remained the main secondary technology path, and Dracula Technologies stated in January 2026 that its LAYER V2.0 organic photovoltaic platform delivered a 30% performance increase over the prior generation for indoor applications.

Thermal harvesting served a smaller but strategically important niche where stable temperature differentials existed around heat-intensive equipment. RF energy harvesting is the fastest-growing technology segment in the MEMS energy harvesting devices market and is projected to expand at 8.78% through 2031 as ambient IoT tags draw power from existing wireless infrastructure. Wiliot stated in January 2026 that its Gen3 IoT Pixel uses a dual-band architecture across 2.4 GHz and sub-1 GHz to improve harvesting efficiency and energizing range over the prior generation. A 2026 "Micromachines" paper also demonstrated an RF energy-harvesting IoT network architecture using a BQ25504-based power path, while IEEE 802.11 TGbp continues to build a certified ambient power communications framework.

Wireless systems held 72.45% of the deployment type segment in 2025 and are also the fastest-growing category at 9.23% through 2031. That lead shows that removing battery maintenance is most valuable when the same design also removes power and data cabling. In the MEMS energy harvesting devices market, this makes wireless deployment the practical default for large sensor fleets in buildings and distributed industrial settings. Atmosic states that its platform supports ultra-low-power connectivity with integrated energy harvesting and IEEE 802.15.4 capability, which reduces integration burden for system developers.

Wired systems kept a meaningful role where latency, bandwidth, or electromagnetic interference limits made wireless less suitable. Some industrial environments still separate power and communication functions, using harvested energy at the sensor while keeping a wired data path for reliability. This portion of the MEMS energy harvesting devices market remains stable because the application requirements are specific rather than broad. The result is a two-speed structure where wireless captures most new installations while wired designs remain in a narrower set of performance-sensitive deployments.

Geography Analysis

North America retained 32.78% of the MEMS energy harvesting devices market share in 2025, which kept it in the leading regional position. The United States remained the main revenue center because industrial condition monitoring, smart building retrofits, and data center sensing all reached earlier commercial maturity than in many other regions. EnOcean stated in 2025 that its energy-harvesting solutions achieved listing on the DesignLights Consortium Qualified Products List, which opened a pathway for utility rebate access in the United States. Canada and Mexico stayed smaller within the region, but both supported demand through mining, oil and gas, and manufacturing use cases that align well with vibration-based sensing. For the MEMS energy harvesting devices market, this regional lead rested on both installed digital infrastructure and a regulatory setting that rewarded efficient wireless building controls.

Europe remained a substantial regional market led by Germany, the United Kingdom, France, Italy, and Spain. Demand in Europe is closely tied to energy efficiency and industrial compliance rules, which favor low-maintenance sensor deployments in both buildings and process environments. The European Commission adopted Directive (EU) 2025/2363 in November 2025 and created exemption 7(c)-VI for lead in piezoelectric PZT ceramics until December 31, 2027, which gave suppliers a defined planning window while pushing lead-free substitution work. Sweden also emerged as a notable photovoltaic harvesting center after the Swedish Energy Agency awarded Exeger SEK 130 million, or USD 12.2 million, in 2025 to scale indoor solar cell technology. South America and Middle East, and Africa remained smaller, but mining sites and smart city programs created targeted openings for maintenance-free sensing.

Asia-Pacific is the fastest-growing region in the MEMS energy harvesting devices market and is forecast to expand at 8.94% through 2031. China's large IoT infrastructure buildout, Japan's strength in piezoelectric materials, South Korea's PMIC ecosystem, and India's rising building and manufacturing digitalization are supporting this growth pattern. A 2026 study indexed by CiNii Research described wireless power transfer for building management sensor modules through glass surfaces, which fits Japan's preference for low-disruption retrofit design. ASEAN countries such as Singapore, Malaysia, and Thailand are also moving from pilots toward production-scale ambient IoT sensing in logistics and manufacturing settings.

- EnOcean GmbH

- e-peas S.A.

- 8power Limited

- Powercast Corporation

- Smart Material Corporation

- EH4 GmbH

- Smart Material GmbH

- ReVibe Energy AB

- MEMSYS B.V.

- Enervibe Ltd.

- Pyro-E, Inc.

- WePower Technologies LLC

- Everactive, Inc.

- Atmosic, Inc.

- Wiliot Ltd.

- Dracula Technologies SAS

- Exeger Sweden AB (publ)

- EPISHINE AB

- Cymbet Corporation

- MicroGen Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Battery-Free Wireless Sensor Networks

- 4.2.2 Expansion of Smart Buildings and Retrofit Building Controls

- 4.2.3 Growth in Industrial Condition Monitoring and Predictive Maintenance

- 4.2.4 Advances in Ultra-Low-Power PMICs and Wireless SoCs

- 4.2.5 Ambient IoT Protocol Standardization Opening Certified Self-Powered Device Classes

- 4.2.6 Need to Eliminate Battery Truck Rolls in Hard-to-Reach Rotating Assets

- 4.3 Market Restraints

- 4.3.1 Limited Power Output and Dependence on Intermittent Ambient Energy

- 4.3.2 Narrow Bandwidth and Resonance Mismatch in Piezoelectric MEMS Designs

- 4.3.3 RoHS Lead-Exemption Uncertainty for Piezoelectric Ceramics

- 4.3.4 Leakage Losses and Cold-Start Bottlenecks in Micro-Power Storage Paths

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Solar (Photovoltaic) Energy Harvesting

- 5.1.2 Vibration and Piezoelectric Energy Harvesting

- 5.1.3 Thermal Energy Harvesting

- 5.1.4 Radio Frequency Energy Harvesting

- 5.2 By Deployment Type

- 5.2.1 Wired Systems

- 5.2.2 Wireless Systems

- 5.3 By Powering Range

- 5.3.1 Low-Power Devices

- 5.3.2 Medium-to-High Power Devices

- 5.4 By End-User Industry

- 5.4.1 Building and Home Automation

- 5.4.2 Industrial and Manufacturing

- 5.4.3 Consumer Electronics

- 5.4.4 Transportation and Logistics

- 5.4.5 Healthcare and Medical Devices

- 5.4.6 Aerospace and Defense

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 EnOcean GmbH

- 6.4.2 e-peas S.A.

- 6.4.3 8power Limited

- 6.4.4 Powercast Corporation

- 6.4.5 Smart Material Corporation

- 6.4.6 EH4 GmbH

- 6.4.7 Smart Material GmbH

- 6.4.8 ReVibe Energy AB

- 6.4.9 MEMSYS B.V.

- 6.4.10 Enervibe Ltd.

- 6.4.11 Pyro-E, Inc.

- 6.4.12 WePower Technologies LLC

- 6.4.13 Everactive, Inc.

- 6.4.14 Atmosic, Inc.

- 6.4.15 Wiliot Ltd.

- 6.4.16 Dracula Technologies SAS

- 6.4.17 Exeger Sweden AB (publ)

- 6.4.18 EPISHINE AB

- 6.4.19 Cymbet Corporation

- 6.4.20 MicroGen Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

MEMS能源採集元件市場規模、佔有率及成長分析(依技術、應用、組件、終端用戶產業及地區分類)-2026-2033年產業預測

MEMS能源採集元件市場規模、佔有率及成長分析(依技術、應用、組件、終端用戶產業及地區分類)-2026-2033年產業預測 IoT能源採集PMIC

IoT能源採集PMIC MEMS能源採集設備的全球市場(2024-2028)

MEMS能源採集設備的全球市場(2024-2028)