|

市場調查報告書

商品編碼

2066524

種子加工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Seed Processing Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

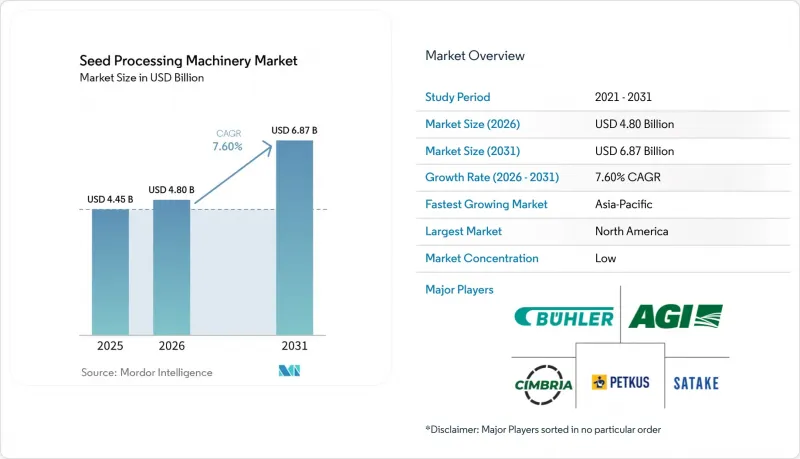

據 Mordor Intelligence 稱,2025 年種子加工機械市場價值為 44.5 億美元,預計將從 2026 年的 48 億美元成長到 2031 年的 68.7 億美元,2026 年至 2031 年的複合年成長率為 7.6%。

本報告按機器類型(預清理機、清理機、乾燥機、分類機、磨床、光學分類機、種子包裝機等)、運作模式(全自動和半自動)、最終用戶(商業種子加工廠、種子生產商、農場設施等)和地區(北美、歐洲等)進行細分。市場預測以美元(USD)計價。

全球種子加工機械市場趨勢與洞察

光學分選自動化提高了效率並降低了人事費用。

自動化透過最大限度地減少分類和缺陷去除過程中的人工干預,正在提升種子加工機械市場的性能標準。人工智慧 (AI) 驅動的光學系統能夠識別單粒種子在顏色、紋理和形狀上的差異,使加工商能夠在不影響生產線速度的前提下提高種子純度。布勒公司將於 2025 年推出 SORTEX AI700,這標誌著種子和穀物應用領域正向深度學習分類系統轉型,旨在提高檢測品質。隨著市場從多個機械流程轉向更少的智慧分類單元,每條生產線的生產效率雖然有所提高,但意外停機的風險也隨之增加。這一趨勢凸顯了預測性維護、遠距離診斷和完善的服務合約在種子加工機械市場商業採購中的重要性日益凸顯。

加工種子和加值種子的需求增加

種子加工機械市場正經歷成長,這主要得益於基礎殺菌劑處理以外的技術進步,例如生物活性接種劑、微量營養素包衣和特種聚合物薄膜。這些高價值種子產品需要精確的包衣均勻性、更佳的乾燥控制和更有效率的批次分離,因為加工品質的波動會影響整個認證批次的性能。 2024年10月,印度國家食用油和油籽任務署撥款101.03億印度盧比(約11.9億美元)用於建立65個新的種子中心。這直接帶動了下游市場對種子加工、包覆和包裝設備的需求。此外,為了在整個加工鏈中保持批次完整性,對分類機、包裝機和貼標系統等輔助設備的需求也不斷成長。生物加工技術的日益普及進一步推動了設備需求,因為加工商需要低剪切力和溫控的包覆和乾燥系統來確保微生物的活性。

智慧機器的初始成本很高

高昂的初始成本仍然是採用先進種子加工機械的主要障礙。買家通常會將先進的光學分選系統與傳統機械設備的成本進行比較,發現前者價格高出40%至60%。此外,自動化分類機、連接基礎設施以及監控與資料採集(SCADA)系統的相關成本進一步增加了專案的總投資。在農業融資管道有限且設備更換週期長的地區,這些財務挑戰尤其突出。因此,大量資本投資的需求仍阻礙合作社、農場級加工商以及中小商業企業採用先進的種子加工機械。

細分市場分析

到2025年,清潔設備將佔據種子加工機械市場42.7%的最大佔有率。清潔設備將繼續主導市場,因為在進行分類、加工、乾燥、包衣和包裝等後續工序之前,種子初次清洗至關重要。氣篩分類機因其擴充性強、易於維護以及與各種作物類型和下游設備系統的兼容性而廣受歡迎。此外,在面臨收穫後水分管理挑戰的地區以及生物種子加工技術日益普及的地區,乾燥機和加工系統的重要性也日益凸顯。來自全球商業種子廠、糧食加工商和負責大規模多產品加工流程的綜合種子加工廠的持續需求,將推動分類機設備市場的發展。

在種子加工機械市場中,光學分分類機市場預計將以7.6%的複合年成長率(CAGR)從2026年成長至2031年,成為成長最快的細分市場。這一成長主要受出口種子純度需求、數位化品管以及自動化缺陷檢測技術發展趨勢的推動。隨著人工智慧(AI)影像處理系統提高加工精度並最大限度降低高價值種子業務中的污染風險,光學分類機的應用範圍正在不斷擴大。製造商也在分選平台中整合合規性監控、可追溯性和資料管理功能,以滿足認證要求。儘管先進的分選系統發展迅速,但清洗機仍然是重要的設備類別,因為種子清洗是全球商業種子加工工作流程的基礎。

區域分析

到2025年,北美將佔據全球種子加工機械市場最大的佔有率,達到34.1%。該地區受益於成熟的商業種子產業、精準種子加工技術的廣泛應用以及大規模的行栽作物種植系統。玉米和大豆的大規模種植推動了對先進的種子清洗、分級和光學分選系統的強勁需求。美國和加拿大的商業種子企業正在加大對整合加工基礎設施的投資,以提高可追溯性、確保符合純度標準並保證出口合規性。強勁的設備更新需求、數位化流程的整合以及完善的種子認證體系,正推動北美在全球商業種子加工設備和基礎設施發展領域保持主導。

預計2026年至2031年間,亞太地區種子加工機械市場將以8.1%的複合年成長率(CAGR)實現最高成長。這一成長主要得益於中國、印度和整個東南亞地區認證種子的擴張、政府支持的農業現代化舉措以及對商業加工基礎設施投資的增加。政府對種子中心、加工設施和糧食處理基礎設施的投入,正在加速全部區域採用最先進的清洗、乾燥和分類系統。此外,商業農業的興起和對高品質認證種子日益成長的需求,也推動了加工流程的現代化。日本、澳洲和韓國等農業領先國家正著力在其商業種子生產網路中應用光學分類、數位化合規系統和自動化加工技術。

南美洲仍然是一個重要的成長區域,這主要得益於巴西和阿根廷大規模糧食和油籽產量的成長,而這與出口導向農業密切相關。根據聯合國糧食及農業組織(糧農組織)的數據,埃塞俄比亞的「2024-2030年收穫後管理策略」撥款143億埃塞俄比亞比爾(約2.66億美元)用於引進收穫後機械化和加工技術。這項措施旨在支持種子和糧食基礎設施的全面現代化。在中東和非洲,人們越來越關注糧食安全、可控環境農業和高效率的收穫後後處理。這些趨勢正逐步提升開發中國家對先進的種子清洗、分類和處理技術的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 光學分選自動化提高了效率並降低了人事費用。

- 加工種子和加值種子的需求增加

- 政府補貼正加速推動收穫後作業的機械化進程。

- 商業種子繁殖中心的成長

- 向無微塑膠塗料的轉變正在推動預處理設備和乾燥機的改造。

- 數位化溯源和認證工作流程正在推動線上取樣和標籤技術的升級。

- 市場限制因素

- 智慧機器的初始成本很高

- 精密零件供應鏈的波動

- 操作員和服務技能瓶頸限制了運作。

- 圍繞聯網設備的資料所有權和網路安全問題引發的擔憂

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按機器類型

- 預清潔劑

- 清潔工

- 烘乾機

- 平土機

- 塗層和加工設備

- 分類機和除石機

- 磨床

- 光學分類機

- 種子包裝機

- 其他專用設備

- 透過運作模式

- 自動的

- 半自動

- 最終用戶

- 商業種子加工廠

- 種子生產商

- 研究機構

- 農場設施

- 糧食處理設施

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Buhler AG

- Cimbria A/S(Grain & Protein Technologies)

- PETKUS Technologie GmbH

- Satake Corporation

- Ag Growth International Inc.

- Westrup ApS(Fowler Westrup India Pvt. Ltd.)

- Alvan Blanch Development Company Limited

- Osaw Agro Industries Pvt. Ltd.

- Skiold A/S

- Oliver Manufacturing CO, Inc.

- Shijiazhuang Synmec International Trading, Ltd.(Hebei Ruixue Grain Selecting Machinery Co., Ltd.)

- Carter Day International, Inc.

- Lewis M. Carter Manufacturing, LLC

- Bratney Companies(KBC Group, Inc.)

- Spectrum Industries

第7章 市場機會與未來展望

According to Mordor Intelligence, the seed processing machinery market size was valued at USD 4.45 billion in 2025 and is projected to grow from USD 4.80 billion in 2026 to USD 6.87 billion by 2031, registering a 7.6% CAGR from 2026 to 2031.

This report is Segmented by Machinery Type (Pre-Cleaners, Cleaners, Dryers, Graders, Polishers, Optical Sorters, Seed Packagers, and More), by Operation Mode (Automatic and Semi-Automatic), by End-User (Commercial Seed Processing Plants, Seed Producers, On-Farm Facilities, and More), and by Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Seed Processing Machinery Market Trends and Insights

Automation of Optical Sorting Enhances Efficiency and Reduces Labor Costs

Automation is enhancing performance standards in the seed processing machinery market by minimizing manual intervention in sorting and defect removal processes. Artificial intelligence-enabled optical systems can identify variations in color, texture, and shape at the single-seed level, enabling processors to improve purity without compromising line speed. The launch of Buhler's SORTEX AI700 in 2025 exemplifies the transition toward deep-learning sorting systems aimed at improving inspection quality in seed and grain applications. As the market shifts from multiple mechanical stages to fewer intelligent sorting units, each line achieves higher productivity but also faces increased vulnerability to unplanned stoppages. This development underscores the growing importance of predictive maintenance, remote diagnostics, and robust service contracts in commercial procurement within the seed processing machinery market.

Increasing Demand for Treated and Value-Added Seeds

The seed processing machinery market is experiencing growth driven by advancements beyond basic fungicide treatments, including bioactive inoculants, micronutrient coatings, and specialized polymer films. These high-value seed products necessitate precise coating consistency, improved drying control, and enhanced lot segregation, as inconsistencies in application quality can compromise the performance of an entire certified batch. In October 2024, India's National Mission on Edible Oils and Oilseeds allocated INR 10,103 crore (USD 1.19 billion) and established 65 new seed hubs, generating direct downstream demand for equipment used in treating, coating, and packaging seeds. Additionally, the market is witnessing increased demand for ancillary equipment, such as cleaners, packagers, and labeling systems, to maintain lot integrity throughout the processing chain. The rise of biological treatments has further driven equipment demand, as processors require low-shear and temperature-controlled coating and drying systems to ensure the viability of microorganisms.

High Up-Front Cost of Smart Machinery

High initial costs remain a significant barrier to the adoption of advanced seed processing machinery. Buyers often compare the costs of advanced optical sorting systems with conventional mechanical equipment, finding optical sorters to be 40% to 60% more expensive. Additionally, expenses related to automation controls, connectivity infrastructure, and supervisory control and data acquisition systems further increase the overall project investment. These financial challenges are particularly pronounced in regions with limited access to agricultural financing and long equipment replacement cycles. Consequently, the high capital investment required continues to hinder the adoption of advanced seed processing machinery by cooperatives, farm-level processors, and small to medium-scale commercial operators.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies Boost Post-Harvest Mechanization Efforts

- Growth in Commercial Seed Multiplication Centers

- Supply Chain Volatility for Precision Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The seed processing machinery market share for the cleaners segment accounted for the largest 42.7% in 2025. Cleaners continue to dominate as primary seed cleaning is essential before subsequent operations, such as grading, treatment, drying, coating, and packaging, can commence. Air-screen cleaners are widely preferred due to their scalability, low maintenance requirements, and compatibility with various crop types and downstream equipment systems. Additionally, dryers and treatment systems are gaining significance in regions addressing post-harvest moisture management challenges and the increasing adoption of biological seed treatments. The cleaners segment benefits from sustained demand across commercial seed plants, grain handlers, and integrated seed-processing facilities managing large multi-crop processing workflows globally.

The seed processing machinery market for the optical sorters segment will advance to grow at the fastest CAGR of 7.6% from 2026 to 2031. This growth is driven by rising demand for export-grade seed purity, digital quality control, and automated defect detection technologies. Optical sorters are increasingly utilized as artificial intelligence-enabled imaging systems enhance processing precision and minimize contamination risks in high-value seed operations. Manufacturers are also incorporating compliance monitoring, traceability, and data-management features into sorting platforms to meet certification requirements. Despite the rapid growth of advanced sorting systems, cleaners remain the dominant equipment category, as primary seed-cleaning processes continue to serve as the operational foundation for commercial seed-processing workflows globally.

Geography Analysis

The sedd processing machinery market share for North America accounted for the largest 34.1% in 2025. The region benefits from a well-established commercial seed industry, widespread adoption of precision seed-treatment technologies, and extensive row-crop production systems. The large-scale cultivation of corn and soybeans drives strong demand for advanced seed-cleaning, grading, and optical-sorting systems. Commercial seed companies in the United States and Canada are increasingly investing in integrated processing infrastructure to enhance traceability, meet purity standards, and ensure export compliance. Factors such as strong replacement demand, digital process integration, and established seed-certification systems continue to reinforce North America's leading position in commercial seed-processing equipment and infrastructure development globally.

The sedd processing machinery market size for Asia-Pacific is projected to grow at the fastest 8.1% CAGR from 2026 to 2031. This growth is driven by the expansion of certified seeds, government-supported agricultural modernization initiatives, and increasing investments in commercial processing infrastructure across China, India, and Southeast Asia. Public funding for seed hubs, processing units, and grain-handling infrastructure is accelerating the adoption of modern cleaning, drying, and sorting systems throughout the region. Additionally, the rise of commercial agriculture and growing demand for high-quality certified seeds are fostering the modernization of processing operations. More developed agricultural economies, such as Japan, Australia, and South Korea, are focusing on optical sorting, digital compliance systems, and automated processing technologies within their commercial seed-production networks.

South America remains a significant growth region due to the extensive cereal and oilseed seed multiplication activities in Brazil and Argentina, which are closely tied to export-oriented agriculture. According to the Food and Agriculture Organization of the United Nations, Ethiopia's Postharvest Management Strategy 2024-2030 has allocated ETB 14.3 billion (USD 266 million) for post-harvest mechanization and processing technology deployment. This initiative supports the broader modernization of seed and grain infrastructure. In the Middle East and Africa, there is a growing focus on food security, controlled-environment agriculture, and improvements in post-harvest efficiency. These developments are gradually driving demand for modern seed-cleaning, sorting, and handling technologies in developing agricultural economies.

- Buhler AG

- Cimbria A/S (Grain & Protein Technologies)

- PETKUS Technologie GmbH

- Satake Corporation

- Ag Growth International Inc.

- Westrup ApS (Fowler Westrup India Pvt. Ltd.)

- Alvan Blanch Development Company Limited

- Osaw Agro Industries Pvt. Ltd.

- Skiold A/S

- Oliver Manufacturing CO, Inc.

- Shijiazhuang Synmec International Trading, Ltd. (Hebei Ruixue Grain Selecting Machinery Co., Ltd.)

- Carter Day International, Inc.

- Lewis M. Carter Manufacturing, LLC

- Bratney Companies (K.B.C. Group, Inc.)

- Spectrum Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automation of optical sorting enhances efficiency and reduces labor costs

- 4.2.2 Increasing demand for treated and value-added seeds

- 4.2.3 Government subsidies boost post-harvest mechanization efforts

- 4.2.4 Growth in commercial seed multiplication centers

- 4.2.5 Microplastic-free coating transition drives treater and dryer retrofits

- 4.2.6 Digital traceability and certification workflows drive inline sampling and labeling upgrades

- 4.3 Market Restraints

- 4.3.1 High up-front cost of smart machinery

- 4.3.2 Supply chain volatility for precision components

- 4.3.3 Operator and service-skill bottlenecks limit uptime

- 4.3.4 Data ownership and cyber security concerns around connected equipment

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Machinery Type

- 5.1.1 Pre-cleaners

- 5.1.2 Cleaners

- 5.1.3 Dryers

- 5.1.4 Graders

- 5.1.5 Coaters and Treaters

- 5.1.6 Separators and Destoners

- 5.1.7 Polishers

- 5.1.8 Optical Sorters

- 5.1.9 Seed Packagers

- 5.1.10 Other Specialized Equipment

- 5.2 By Operation Mode

- 5.2.1 Automatic

- 5.2.2 Semi-Automatic

- 5.3 By End-User

- 5.3.1 Commercial Seed Processing Plants

- 5.3.2 Seed Producers

- 5.3.3 Research Institutions

- 5.3.4 On-Farm Facilities

- 5.3.5 Grain Handling Facilities

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 Italy

- 5.4.2.4 Spain

- 5.4.2.5 United Kingdom

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Buhler AG

- 6.4.2 Cimbria A/S (Grain & Protein Technologies)

- 6.4.3 PETKUS Technologie GmbH

- 6.4.4 Satake Corporation

- 6.4.5 Ag Growth International Inc.

- 6.4.6 Westrup ApS (Fowler Westrup India Pvt. Ltd.)

- 6.4.7 Alvan Blanch Development Company Limited

- 6.4.8 Osaw Agro Industries Pvt. Ltd.

- 6.4.9 Skiold A/S

- 6.4.10 Oliver Manufacturing CO, Inc.

- 6.4.11 Shijiazhuang Synmec International Trading, Ltd. (Hebei Ruixue Grain Selecting Machinery Co., Ltd.)

- 6.4.12 Carter Day International, Inc.

- 6.4.13 Lewis M. Carter Manufacturing, LLC

- 6.4.14 Bratney Companies (K.B.C. Group, Inc.)

- 6.4.15 Spectrum Industries

7 Market Opportunities and Future Outlook

全球老虎機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球老虎機市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 粉末加工設備市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、最終用戶、地區和競爭格局分類,2021-2031年

粉末加工設備市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、最終用戶、地區和競爭格局分類,2021-2031年 2026年全球熔噴不織布機械市場報告

2026年全球熔噴不織布機械市場報告 精密加工市場分析與預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶、設備及解決方案分類

精密加工市場分析與預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶、設備及解決方案分類 鑽石單晶加工設備市場:依製程、設備類型、自動化程度和終端用戶產業分類-2026-2032年全球預測全球石材加工機械市場規模、佔有率、趨勢和成長分析報告:2026-2034年

鑽石單晶加工設備市場:依製程、設備類型、自動化程度和終端用戶產業分類-2026-2032年全球預測全球石材加工機械市場規模、佔有率、趨勢和成長分析報告:2026-2034年 精密加工市場規模、佔有率和趨勢分析報告:按營運方式、類型、最終用途、地區和細分市場預測,2026-2033年種子加工機械市場-2026-2031年預測

精密加工市場規模、佔有率和趨勢分析報告:按營運方式、類型、最終用途、地區和細分市場預測,2026-2033年種子加工機械市場-2026-2031年預測 石材加工機械市場規模、佔有率及成長分析(按機器類型、加工材料、應用、最終用戶、機器自動化程度及地區分類)-2026-2033年產業預測

石材加工機械市場規模、佔有率及成長分析(按機器類型、加工材料、應用、最終用戶、機器自動化程度及地區分類)-2026-2033年產業預測 全球精密加工市場

全球精密加工市場