|

市場調查報告書

商品編碼

2066510

寵物照護:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Pet Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

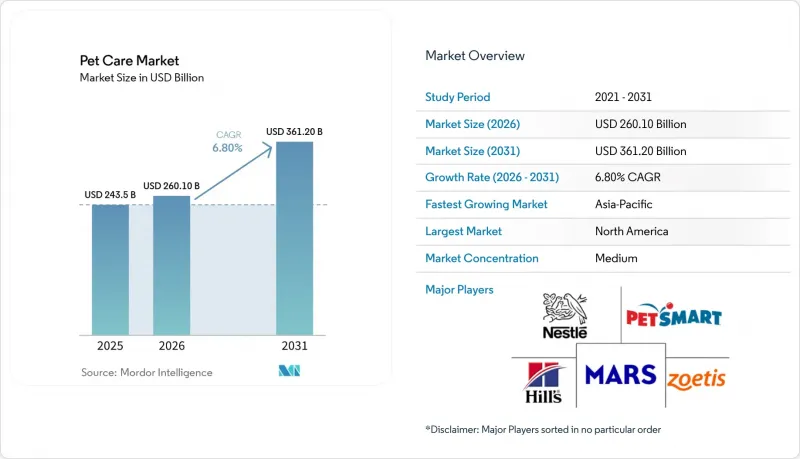

據 Mordor Intelligence 稱,2025 年寵物護理市場價值 2,435 億美元,預計將從 2026 年的 2,601 億美元成長到 2031 年的 3,612 億美元,2026 年至 2031 年的複合年成長率為 6.80%。

本報告按產品類型(寵物食品、寵物保健品、寵物美容產品、寵物用品、寵物服務)、動物種類(犬、貓、其他動物)、分銷管道(線下零售、線上零售)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元(USD)為單位。

全球寵物護理市場趨勢與洞察

寵物“擬人化”和“優質化”

寵物「人性化」和「優質化」正在推動寵物護理市場的長期成長。這是因為消費者越來越將伴侶動物視為家庭成員,並增加了在以提升寵物健康為重點的產品和服務上的支出。根據美國寵物用品協會預測,到2025年,美國養狗的比例將達到53%,高於前一年的51%,凸顯了消費者對優質營養、預防醫學、診斷、美容和豐富寵物生活等相關護理產品日益成長的需求。此外,人們對寵物的情感依附不斷加深,也促使他們在慢性病管理、專業治療和老齡化相關醫療服務方面的支出增加,推動了寵物照護市場的持續成長。

預防醫學與寵物保險的普及

預防性護理和寵物保險的日益普及正在推動寵物護理市場的成長。保險覆蓋範圍的擴大導致診斷、治療和常規獸醫服務的支出增加。根據北美寵物健康保險協會 (NAPHIA) 預測,北美地區的保費總收入預計將從 2023 年的 42 億美元增至 2024 年的 52 億美元。寵物保險投保人數的增加提高了寵物獲得預防性護理、慢性病管理和先進獸醫服務的便利性,同時也促使寵物飼主為他們心愛的寵物尋求更高品質的臨床護理和健康服務。

原料和包裝成本的波動

原料和包裝成本的波動仍然是寵物護理市場面臨的主要阻礙因素。蛋白質原料、包裝材料、運輸成本和能源價格的變化直接影響製造成本和消費者價格。根據碩騰公司(Zoetis Inc.)2025年年度報告,宏觀經濟壓力和家庭支出下降正在影響寵物就診趨勢和寵物保健品類別的購買行為。隨著寵物飼主越來越注重成本控制,各公司正優先加強供應鏈管理、最佳化籌資策略並提高營運效率,以維持寵物照護產業的獲利能力。

細分市場分析

預計到2025年,寵物食品將佔據寵物護理市場52.6%的最大佔有率。寵物食品之所以仍是主要品類,是因為其購買頻率高、供應充足,以及消費者對高級產品功能性營養產品的偏好日益成長。市場需求正轉向新鮮、冷藏、無穀物以及獸醫推薦的產品,這些產品能夠滿足消化健康、體重管理和特定年齡層的營養需求。製造商正透過採用永續原料和個人化餵食方案來拓展其高級產品線。超市、寵物店、獸醫診所和電商超級市場等零售通路的強勁滲透,持續支撐著全球已開發國家和新興市場伴侶動物照護市場的穩定消費。

在寵物護理市場中,寵物服務業預計將以最高速度成長,2026年至2031年的複合年成長率將達到10.0%。這一成長主要得益於獸醫護理、美容、日托、寵物酒店、保險和預防性醫療服務等方面的支出增加。消費者越來越傾向於將寵物健康管理和定期醫療保健視為必要的家庭開支,而非自由裁量權的支出。在都市區市場,訂閱式獸醫護理計劃、遠距醫療、診斷和行為支援服務也在迅速發展。此外,寵物老化和人們對預防性照護意識的提高,將繼續推動伴侶動物醫療保健生態系統中以定期體檢和健康維護為重點的寵物服務的長期需求。

區域分析

到2025年,北美將佔據寵物護理市場33.5%的最大佔有率。這一主導地位歸功於其較高的寵物擁有率、先進的獸醫基礎設施、廣泛的預防保健服務以及消費者在高階寵物營養和保健產品上的大量支出。該地區受益於獸醫醫院網路的擴張、對診斷和慢性病管理需求的成長以及訂閱式寵物醫療保健服務的日益普及。此外,伴侶動物保險投保率的上升以及對預防保健日益重視,也推動了美國和加拿大在獸醫服務、藥品、營養和保健方面的支出成長。

預計亞太市場將在2026年至2031年間以9.6%的複合年成長率(CAGR)實現最高成長。都市化、家庭規模縮小、母親年齡成長以及可支配收入增加等因素,推動了中國、印度、日本、韓國和東南亞國家寵物主人數量的成長。消費者越來越傾向於將資源投入高階寵物營養、預防保健、美容、診斷和健康服務。此外,數位商務和基於應用程式的寵物護理平台正在提升大都會圈寵物產品和獸醫諮詢服務的可及性。國內外企業正增加對高級產品組合和全通路分銷策略的投資,以鞏固其在快速發展的區域寵物護理市場的地位。

歐洲憑藉其成熟的寵物飼養趨勢、先進的獸醫服務以及不斷成長的預防保健和健康管理支出,仍然是至關重要的區域市場。根據英國保險協會預測,英國的寵物保險保單數量預計將從2023年的440萬份增至2024年的460萬份,這反映出人們對保險涵蓋的獸醫和預防保健服務的使用日益成長。對高階寵物食品、診斷產品、藥品和健康產品的強勁需求持續推動著該地區的成長。訂閱式獸醫服務和全通路零售的擴張進一步促進了歐洲主要市場對伴侶動物醫療保健的持續投入。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 寵物的人性化和優質化

- 千禧世代和Z世代的寵物擁有率不斷提高。

- 拓展線上零售訂閱配送業務

- 預防醫學和保險登記

- 整合獸醫醫院並交叉銷售護理計劃

- 新型蛋白質和功能成分的核准

- 市場限制因素

- 原料和包裝成本的波動

- 更嚴格遵守標籤和功效聲明方面的規定。

- 獸醫人手不足

- 低溫運輸和生鮮食品最後一公里運輸的經濟學

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 寵物食品

- 寵物保健

- 寵物美容產品

- 寵物用品

- 寵物服務

- 依動物類型

- 狗

- 貓

- 其他

- 透過分銷管道

- 線下零售

- 超級市場和大賣場

- 寵物專賣店

- 動物診所

- 線上零售

- 線下零售

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mars, Incorporated

- Nestle Purina PetCare Company(Nestle SA)

- Hill's Pet Nutrition, Inc.(Colgate-Palmolive Company)

- The JM Smucker Company

- Blue Buffalo Company, Ltd.(General Mills, Inc.)

- Spectrum Brands Holdings, Inc.

- Central Garden & Pet Company

- Freshpet, Inc.

- Unicharm Corporation

- Zoetis Inc.

- Elanco Animal Health Incorporated

- Virbac SA

- Dechra Pharmaceuticals PLC

- IDEXX Laboratories, Inc.

- PetSmart LLC(BC partners)

第7章 市場機會與未來展望

According to Mordor Intelligence, the pet care market size was valued at USD 243.50 billion in 2025 and is projected to grow from USD 260.10 billion in 2026 to USD 361.20 billion by 2031, registering a CAGR of 6.80% from 2026 to 2031.

This report is Segmented by Product Type (Pet Food, Pet Healthcare, Pet Grooming Products, Pet Accessories, and Pet Services), by Animal Type (Dogs, Cats, and Other Animals), by Distribution Channel (Offline Retail and Online Retail), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Pet Care Market Trends and Insights

Pet Humanization and Premiumization

Pet humanization and premiumization are driving long-term growth in the pet care market, as consumers increasingly view companion animals as family members and allocate more spending toward wellness-focused products and services. According to the American Pet Products Association, dog ownership reached 53% of United States households in 2025, up from 51% the previous year, highlighting the growing demand for premium nutrition, preventive healthcare, diagnostics, grooming, and enrichment-related pet care products. Additionally, the rising emotional attachment to pets is fostering increased expenditure on chronic care management, specialty treatments, and age-related healthcare services, contributing to sustained value growth in the pet care market.

Preventive Care and Insurance Adoption

Preventive care and the adoption of pet insurance are driving growth in the pet care market, as insurance coverage promotes increased spending on diagnostics, treatments, and routine veterinary services. According to the North American Pet Health Insurance Association (NAPHIA), the total written premium in North America reached USD 5.2 billion in 2024, up from USD 4.2 billion in 2023. The rising adoption of pet insurance is enhancing access to preventive healthcare, chronic disease management, and advanced veterinary procedures. It also motivates pet owners to seek higher-value clinical care and wellness services for their companion animals.

Raw Material and Packaging Cost Volatility

Volatility in raw material and packaging costs continues to be a significant restraint on the pet care market. Fluctuations in the prices of protein ingredients, packaging materials, freight, and energy directly impact manufacturing expenses and consumer pricing. According to Zoetis Inc.'s 2025 Annual Report, macroeconomic pressures and reduced household spending have influenced veterinary visit trends and purchasing behavior across companion animal healthcare categories. Increasing cost sensitivity among pet owners is prompting companies to enhance supply chain management, optimize sourcing strategies, and prioritize operational efficiency to sustain margins within the pet care industry.

Other drivers and restraints analyzed in the detailed report include:

- Veterinary Clinic Corporatization and Care-Plan Cross-Sell

- Novel Proteins and Functional Ingredient Approvals

- Veterinary Labor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The pet care market share for the pet food segment accounted for the largest 52.6% in 2025. Pet food remains the dominant category due to its recurring purchase frequency, wide product availability, and increasing consumer preference for premium and functional nutrition products. Demand is shifting toward fresh, refrigerated, grain-free, and veterinary-recommended formulations that address digestive health, weight management, and age-specific nutrition needs. Manufacturers are expanding premium offerings by incorporating sustainable ingredients and personalized feeding solutions. Strong retail penetration across supermarkets, pet specialty stores, veterinary clinics, and e-commerce platforms continues to support stable consumer spending in both developed and emerging companion animal care markets globally.

The pet care market size for the pet services segment is projected to grow at the fastest 10.0% CAGR from 2026 to 2031. This growth is driven by increasing expenditure on veterinary care, grooming, daycare, boarding, insurance, and preventive healthcare services. Consumers increasingly consider pet wellness and routine medical care as essential household expenses rather than discretionary spending. Subscription-based veterinary plans, telehealth consultations, diagnostics, and behavioral support services are also expanding rapidly in urban markets. Additionally, the aging pet population and rising awareness of preventive treatments continue to drive long-term demand for recurring clinical and wellness-focused pet service offerings within the companion animal healthcare ecosystem.

Geography Analysis

The pet care market share for North America held the largest 33.5% in 2025. This leading position is attributed to high pet ownership rates, advanced veterinary infrastructure, widespread adoption of preventive healthcare services, and substantial consumer spending on premium pet nutrition and wellness products. The region benefits from the expansion of veterinary clinic networks, growing demand for diagnostics and chronic disease management, and increased use of subscription-based pet healthcare services. Additionally, the rising adoption of companion animal insurance and a stronger emphasis on preventive care are driving spending across veterinary services, pharmaceuticals, nutrition, and wellness categories in the United States and Canada.

The Asia-Pacific market size is projected to grow at the fastest CAGR at 9.6% from 2026 to 2031. Urbanization, smaller household sizes, delayed parenthood, and rising disposable incomes are contributing to increased pet ownership in countries such as China, India, Japan, South Korea, and across Southeast Asia. Consumers are allocating more resources to premium nutrition, preventive healthcare, grooming, diagnostics, and wellness services for their pets. Additionally, digital commerce and app-based pet care platforms are enhancing access to products and veterinary consultation services in metropolitan areas. Both domestic and international companies are investing in premium product portfolios and omnichannel distribution strategies to strengthen their presence in the rapidly developing regional pet care markets.

Europe remains a key regional market because of established pet ownership trends, advanced veterinary services, and strong emphasis on preventive care and wellness spending. According to the Association of British Insurers, pet insurance coverage in the United Kingdom reached 4.6 million policies in 2024, compared with 4.4 million policies in 2023, reflecting rising adoption of insurance-backed veterinary care and preventive healthcare services. The region also continues benefiting from strong demand for premium pet nutrition, diagnostics, pharmaceuticals, and wellness products. Subscription-based veterinary services and omnichannel retail expansion are further supporting recurring companion animal healthcare spending across major European markets.

- Mars, Incorporated

- Nestle Purina PetCare Company (Nestle S.A.)

- Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- The J. M. Smucker Company

- Blue Buffalo Company, Ltd. (General Mills, Inc.)

- Spectrum Brands Holdings, Inc.

- Central Garden & Pet Company

- Freshpet, Inc.

- Unicharm Corporation

- Zoetis Inc.

- Elanco Animal Health Incorporated

- Virbac S.A.

- Dechra Pharmaceuticals PLC

- IDEXX Laboratories, Inc.

- PetSmart LLC (BC partners)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pet humanization and premiumization

- 4.2.2 Rising millennial and Generation Z pet ownership

- 4.2.3 Online retail and autoship expansion

- 4.2.4 Preventive care and insurance adoption

- 4.2.5 Veterinary clinic corporatization and care-plan cross-sell

- 4.2.6 Novel proteins and functional ingredient approvals

- 4.3 Market Restraints

- 4.3.1 Raw material and packaging cost volatility

- 4.3.2 Labeling and claims compliance tightening

- 4.3.3 Veterinary labor shortages

- 4.3.4 Cold-chain and last-mile economics for fresh diets

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Pet Food

- 5.1.2 Pet Healthcare

- 5.1.3 Pet Grooming Products

- 5.1.4 Pet Accessories

- 5.1.5 Pet Services

- 5.2 By Animal Type

- 5.2.1 Dogs

- 5.2.2 Cats

- 5.2.3 Others

- 5.3 By Distribution Channel

- 5.3.1 Offline Retail

- 5.3.1.1 Supermarkets and Hypermarkets

- 5.3.1.2 Pet Specialty Stores

- 5.3.1.3 Veterinary Clinics

- 5.3.2 Online Retail

- 5.3.1 Offline Retail

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Mars, Incorporated

- 6.4.2 Nestle Purina PetCare Company (Nestle S.A.)

- 6.4.3 Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- 6.4.4 The J. M. Smucker Company

- 6.4.5 Blue Buffalo Company, Ltd. (General Mills, Inc.)

- 6.4.6 Spectrum Brands Holdings, Inc.

- 6.4.7 Central Garden & Pet Company

- 6.4.8 Freshpet, Inc.

- 6.4.9 Unicharm Corporation

- 6.4.10 Zoetis Inc.

- 6.4.11 Elanco Animal Health Incorporated

- 6.4.12 Virbac S.A.

- 6.4.13 Dechra Pharmaceuticals PLC

- 6.4.14 IDEXX Laboratories, Inc.

- 6.4.15 PetSmart LLC (BC partners)

7 Market Opportunities and Future Outlook

寵物行為監測與分析平台市場預測至2034年-全球分析(依監測重點領域、技術整合、服務模式、經營模式、最終使用者和地區分類)

寵物行為監測與分析平台市場預測至2034年-全球分析(依監測重點領域、技術整合、服務模式、經營模式、最終使用者和地區分類) 行動寵物護理市場規模、佔有率和成長分析:按服務類型、寵物類型、經營模式、最終用戶和地區分類-2026-2033年產業預測2034年全球寵物倫理繁殖市場預測-按動物類型、繁殖方法、服務內容、認證類型、繁殖者類型、最終使用者、銷售管道和地區分類的全球分析寵物眼科護理市場預測至2034年-全球產品、設備、適應症、給藥途徑、動物種類、最終用戶、通路和區域分析寵物腫瘤市場預測至2034年-全球癌症類型、動物種類、治療方法、診斷方法、最終用戶、通路和區域分析寵物護膚市場預測至2034年-按產品類型、寵物品種、成分類型、通路和地區分類的全球分析

行動寵物護理市場規模、佔有率和成長分析:按服務類型、寵物類型、經營模式、最終用戶和地區分類-2026-2033年產業預測2034年全球寵物倫理繁殖市場預測-按動物類型、繁殖方法、服務內容、認證類型、繁殖者類型、最終使用者、銷售管道和地區分類的全球分析寵物眼科護理市場預測至2034年-全球產品、設備、適應症、給藥途徑、動物種類、最終用戶、通路和區域分析寵物腫瘤市場預測至2034年-全球癌症類型、動物種類、治療方法、診斷方法、最終用戶、通路和區域分析寵物護膚市場預測至2034年-按產品類型、寵物品種、成分類型、通路和地區分類的全球分析 寵物照護市場規模、佔有率和成長分析:寵物用品、寵物服務、寵物娛樂、寵物保健產品,按地區分類-2026-2033年產業預測2034年全球寵物在超當地語系化照護服務市場預測-按服務類型、平台類型、收入模式、預訂模式、最終用戶和地區分類的全球分析寵物行為監測市場預測至2034年-全球分析(按組件、產品類型、動物類型、訂閱模式、技術、應用、最終用戶和地區分類)

寵物照護市場規模、佔有率和成長分析:寵物用品、寵物服務、寵物娛樂、寵物保健產品,按地區分類-2026-2033年產業預測2034年全球寵物在超當地語系化照護服務市場預測-按服務類型、平台類型、收入模式、預訂模式、最終用戶和地區分類的全球分析寵物行為監測市場預測至2034年-全球分析(按組件、產品類型、動物類型、訂閱模式、技術、應用、最終用戶和地區分類) 行動寵物護理市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

行動寵物護理市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)