|

市場調查報告書

商品編碼

2066500

氣墊船:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Hovercraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

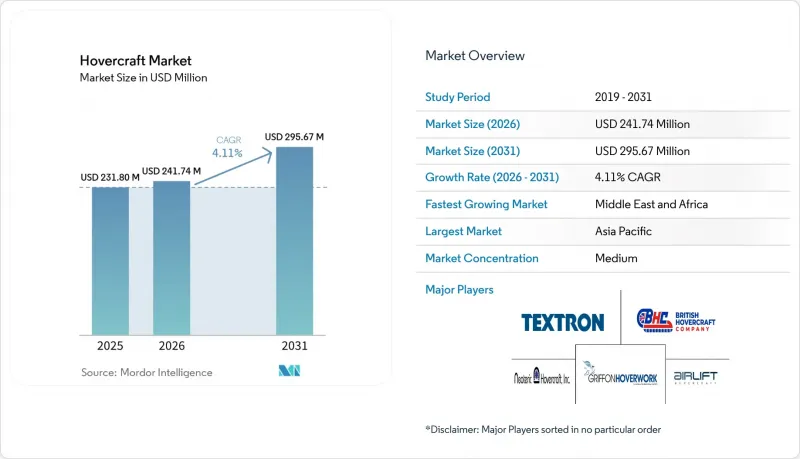

根據 Mordor Intelligence 預測,氣墊船市場規模將從 2025 年的 2.318 億美元成長到 2026 年的 2.4174 億美元,然後在 2031 年達到 2.9567 億美元,2026 年至 2031 年的複合年成長率為 4.11%。

本報告按尺寸(小型、中型、大型)、應用領域(國防安全、客運渡輪服務、海洋能源支援等)、推進系統(柴油引擎、燃氣渦輪機、混合動力、純電動、氫燃料電池)、最終用戶(軍用和民用)以及地區(北美、歐洲等)對氣墊船進行分類。市場預測以美元計價。

全球氣墊船市場趨勢及洞察

氣候變遷引發的洪水增加了對兩棲運輸的需求。

極端降雨推動了沿海城市對能夠穿越被洪水淹沒的道路、佈滿碎石的運河和被冰封的河流的全地形船舶的需求。印度的PROTECT災害應變計畫和美國運輸部90億美元的韌性基金都為市政氣墊船採購提供了津貼框架。在荷蘭以及英國的郡縣一級,氣墊救援艇正在試運行,以應對堤壩決口的情況,因為在這些情況下,船舶會因水深過深而無法航行,輪式車輛則會陷入泥潭。由於洪水俱有間歇性,租賃模式正日益普及,使城市能夠在無需永久性資本支出的情況下獲得所需的救援能力。需求激增主要集中在季風季節的南亞和東南亞以及颶風季節的美國墨西哥灣沿岸地區,導致部署週期雖然可預測但較短。提供模組化、可快速部署的小型船舶的製造商能夠很好地掌握這一週期性但永續的收入來源。

現代突擊和後勤氣墊船以及軍用艦艇的更新換代週期

美國海軍的艦岸連接器(SSC)專案是國防裝備現代化所需典型十年週期的典型例證。首艘試驗艦於2020年服役,根據後續價值3.943億美元的訂單,預計將持續交付至2030年。最新的SSC艦體能夠卸載74噸貨物,並且足以容納M1A2坦克。此外,由於齒輪箱數量減少了一半,它們在整個生命週期中降低了維護成本。中國的076型兩棲攻擊艦於2024年12月服役,其塢艙足夠大,可以容納登陸艇和氣墊船,這進一步加劇了太平洋地區的軍備競賽。北歐國家也紛紛效法;芬蘭於2025年向格里芬海事公司訂購了三艘12.7公尺長的北極氣墊船,用於冰區巡邏任務。與地方政府資金相比,國防預算更有可能吸收成本超支,而且由於美國「極地安全艦」等競爭項目正在分流資金,輔助氣墊船的採購速度正在放緩。

沿海地區交通噪音高、環境法規多

由燃氣渦輪機或高轉速柴油引擎驅動的風扇噪音通常超過 85 分貝(A),違反了美國國家公園管理局規定的航行噪音限制(75 分貝(A)),以及加州和斯堪地那維亞的類似規定。南安普敦、舊金山和大阪的港口當局已實施季節性營運限制,縮短了旅遊遊輪和渡輪的班次。為了遵守規定,營運商被迫降低引擎功率、加裝隔音罩或改用電力推進,但每種方案在續航里程和成本方面都存在劣勢。作為世界上歷史最悠久的客運服務公司,Hovertravel 在索倫特海峽繼續運營,受到當地社區的密切關注,目前正考慮將其船隊改造為動力來源電動技術,以維持其 60 年歷史的航線。除非到 2028 年實現零排放轉型在經濟上可行,否則營運商可能會將重點轉向投資水翼船,因為水翼船可以在更嚴格的噪音限制下運作。

細分市場分析

2025年,中型船舶佔總收入的46.27%,主要得益於國防和海上後勤任務的需求。同時,小型船舶市場預計將以5.23%的複合年成長率成長,進一步推動氣墊船市場的發展勢頭,這主要得益於都市區電動救援艇的引入以及休閒用戶向零排放車型的轉變。中型船舶,例如74噸級的SSC,將繼續在軍事部署戰略中發揮關鍵作用。此外,俄羅斯的Husky-10氣墊船表明,北極地區對負載容量的需求也支撐著對中型船舶的需求。

長度小於15公尺的小型氣墊船設計在芬蘭和加拿大預算緊張、需要快速回應巡邏任務的機構的競標中具有優勢。由於電池重量與船體體積成正比,即使是緊湊型船艇也能迅速達到100海浬的航程標準,進而刺激市政氣墊船市場的發展。對於大型氣墊船而言,由於兩棲航空母艦甲板空間持續有限,除中國和俄羅斯以外,基本客群正在萎縮。因此,已建立模組化小型船艇生產線的製造商預計將獲得越來越多的訂單,而無需擔心可能持續數年的國防採購延誤。

到2025年,國防領域將佔市場規模的37.44%。然而,海上能源支援領域預計到2031年將維持5.24%的複合年成長率,因為風電場營運商正從直升機轉向高速水面效應運輸船,這在履帶式運輸船應用中成長速度最快。以Hovertravel為代表的客運渡輪正面臨來自水翼船競爭對手的壓力,後者以更低的噪音和更低的燃料成本為賣點。

儘管搜救和勘測仍屬於小眾領域,但它們佔據著至關重要的戰略地位,尤其是在極地航線日益便捷的情況下。海上作業人員運輸的經濟效益促使人們採用定期契約,將資本成本分攤到每日輪調中,這與國防部門的間歇性採購模式截然不同。能夠同時獲得國際海事組織(IMO)和離岸風力發電船級社認證的營運商正在獲得高額利潤,這凸顯了氣墊船市場佔有率擺脫傳統軍事依賴、實現多元化發展的需求轉變。

區域分析

隨著中國、日本和印度不斷提升兩棲作戰和災害應變能力,預計2025年,亞太地區將佔全球交付的33.11%。該地區的海軍項目,包括中國076型護衛艦的下水,支撐了市場需求,而南亞各地地方政府訂單的增加也進一步推動了需求成長。然而,中東和非洲市場正逐漸威脅到亞太地區在氣墊船市場佔有率的主導。預計中東和非洲市場將以6.01%的複合年成長率成長,這主要得益於海上石油設施人員運輸和紅海安全巡邏等合約的推動。

沿岸地區的營運商,例如阿布達比國家石油公司(ADNOC)和沙烏地阿美公司,估計每年可節省數千萬美元的直升機營運成本,這推動了對混合動力電動載人運輸機的進一步投資。 AIRCAT 35在安哥拉的投入使用反映了西非石油開發地區類似的經濟狀況。歐洲雖然受到更嚴格的環境法規的限制,但透過採購北極巡邏機和長期營運的索倫特海峽客運服務,仍保持穩定的訂單。

北美正受惠於SSC的飛機更新換代週期和加拿大的零排放設計研究。然而,美國海岸警衛隊的市場滲透率仍然較低。總體而言,氣墊船市場日益反映出全球能源投資趨勢,預計與風力發電廠和油氣樞紐相關的地區將出現強勁成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 氣候變遷引發的洪水增加了對兩棲運輸的需求。

- 軍艦現代化改造週期,包括最新型突擊艇。

- 低噪音電力和氫動力推進技術的進步

- 放鬆管制以促進商業客運服務

- 海洋能源和極地物流的需求

- 加大對緊急應變的投入,主要集中在防洪方面。

- 市場限制因素

- 沿海地區運作期間噪音水平高,且有環境法規問題

- 合格飛行員和維修技術人員短缺

- 與陸基效應艦和水翼艦的競爭

- 燃料成本波動會影響軍事採購週期。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按尺寸分類的氣墊船

- 小型

- 中等的

- 大的

- 透過使用

- 國防與安全

- 客運渡輪服務

- 海上能源支持

- 搜救

- 測量和地圖繪製

- 農業/環境管理

- 透過推進系統

- 柴油引擎

- 燃氣渦輪機

- 混合動力/電動

- 純電動

- 氫燃料電池

- 最終用戶

- 軍隊

- 商業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Griffon Hoverwork Ltd.

- Textron Systems Corporation(Textron Inc.)

- The British Hovercraft Company Ltd.

- Neoteric Hovercraft Inc.

- AEROHOD Ltd.

- Airlift Hovercraft Pty Ltd.

- CHRISTY HOVERCRAFT

- Hovertechnics, LLC.

- Ivanoff Hovercraft AB

- Bill Baker Vehicles Ltd.

- Mad Hovercraft

- Vigor Industrial LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the hovercraft market size is expected to grow from USD 231.80 million in 2025 to USD 241.74 million in 2026 and is forecasted to reach USD 295.67 million by 2031 at a 4.11% CAGR over 2026-2031.

This report is Segmented by Hovercraft Size (Small, Medium, and Large), Application (Defense and Security, Passenger Ferry Services, Offshore Energy Support, and More), Propulsion System (Diesel Engine, Gas Turbine, Hybrid-Electric, Fully Electric, and Hydrogen Fuel-Cell), End User (Military and Commercial), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Hovercraft Market Trends and Insights

Rising Demand for Amphibious Transport Driven by Climate-Related Flooding

Extreme rainfall pushed coastal cities to seek all-terrain craft that can traverse submerged streets, debris-laden canals, and ice-choked rivers. India's PROTECT-funded disaster program and the US Department of Transportation's (DoT's) USD 9 billion resilience fund both create grant pathways for municipal hovercraft procurement. Provincial and county-level agencies in the Netherlands and the United Kingdom are trialing air-cushion rescue fleets for dike-breach scenarios where boats draw too much draft and wheeled vehicles stall in mud. Leasing models are emerging because flood events are episodic, allowing cities to secure capabilities without a permanent capital outlay. Demand spikes concentrate in South and Southeast Asia during monsoon seasons and along the US Gulf Coast during hurricane months, creating a predictable but short deployment window. Manufacturers that supply modular, quickly deployable small craft stand to capture this cyclical but resilient revenue stream.

Military Fleet Replacement Cycles for Modern Assault and Logistics Hovercraft

The US Navy's Ship-to-Shore Connector (SSC) program exemplifies the typical decade-long timeline of defense recapitalization. The first experimental unit sailed in 2020, and deliveries under the USD 394.3 million follow-on order are expected to run through 2030. Modern SSC hulls can lift 74 tons, enough to support an M1A2 tank, while halving the gearbox count, which reduces life-cycle maintenance costs. China's December 2024 launch of the Type 076 amphibious assault ship widens the Pacific arms race by adding a well deck sized for landing craft and hovercraft. Nordic states echo the trend; Finland ordered three 12.7 m Arctic-capable units from Griffon Marine in 2025 for ice patrol duties. Although defense budgets absorb cost overruns better than municipal coffers, competing programs such as the Polar Security Cutter in the United States siphon funds, slowing auxiliary hovercraft acquisitions.

High Operating Noise and Environmental Restrictions in Coastal Regions

Gas-turbine and high-RPM diesel fans routinely exceed 85 dB(A), breaching the US National Park Service's 75 dB(A) underway limit and comparable rules in California and Scandinavia. Port authorities at Southampton, San Francisco, and Osaka have imposed seasonal curfews that curtail tourist runs and ferry schedules. Operators pursuing compliance must derate engines, add acoustic shields, or switch to electric drives, each option imposing range or cost penalties. Hovertravel, the world's oldest passenger service, continues its Solent operations under community scrutiny and is now studying the repower of its fleet with battery-electric technology to preserve its 60-year route. Unless zero-emission retrofits reach economic parity by 2028, operators may divert investment toward hydrofoil alternatives that sail under stricter noise caps.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Low-Noise Electric and Hydrogen Propulsion Technologies

- Growing Offshore Energy and Polar Logistics Requirements

- Scarcity of Certified Pilots and Specialized Maintenance Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium units secured 46.27% of 2025 revenue due to defense and offshore logistics missions, while the small-craft cohort is forecast to grow at 5.23% CAGR as cities adopt electric rescue fleets and leisure users upgrade to zero-emission models, reinforcing momentum in the hovercraft market. Medium hulls, such as the 74-ton SSC, will remain integral to force-projection strategies, and Russia's Husky-10 demonstrates how Arctic payload needs sustain mid-size demand.

Small designs under 15 meters are winning budget-constrained tenders from Finnish and Canadian agencies keen on rapid-response patrols. Battery weights scale linearly with hull volume, allowing compact footprints to reach 100-nautical-mile range thresholds sooner, thereby fueling the expansion of the hovercraft market at the municipal level. Large craft face a contracting customer base outside China and Russia because amphibious mothership decks remain limited. As a result, producers that master modular small-craft production stand to capture rising orders without the multiyear defense procurement lag.

Defense retained 37.44% of the 2025 value. Still, offshore energy support is projected to deliver a 5.24% CAGR through 2031, the fastest among the tracked uses, as wind farm operators shift from helicopters to high-speed surface-effect shuttles. Passenger ferries, exemplified by Hovertravel, face pressure from hydrofoil rivals that promise lower noise and fuel costs.

Search-and-rescue (SAR) and surveying remain niche yet strategically vital, especially as polar routes become more accessible. Offshore crew transfer economics drive recurring contracts that spread capital cost over daily rotations, contrasting with episodic defense buys. Segment operators who can certify hulls to both the IMO and offshore wind classification societies will anchor premium margins, underlining a demand pivot that diversifies the hovercraft market share away from traditional military reliance.

Geography Analysis

The Asia-Pacific region accounted for 33.11% of 2025 deliveries, as China, Japan, and India bolstered their amphibious and disaster response capabilities. The region's naval programs, including China's Type 076 launch, anchor baseline demand, while emerging municipal orders across South Asia add incremental volume. However, the hovercraft market share leadership is gradually being challenged by the Middle East and Africa, which are projected to grow at a 6.01% CAGR, driven by offshore oil crew-transfer contracts and Red Sea security patrols.

Gulf operators, such as ADNOC and Saudi Aramco, quantify helicopter cost savings in the tens of millions of dollars annually, prompting further investment in hybrid-electric crew liners. Angola's AIRCAT 35 deployment reflects similar economic conditions in West African oil plays. Europe, although hampered by tighter environmental scrutiny, maintains a steady pipeline via Arctic patrol procurements and the long-running Solent passenger service.

North America benefits from the SSC fleet renewal cycle and Canadian zero-emission design studies. Yet, US Coast Guard budget reallocations toward icebreakers slow auxiliary hovercraft buys, moderating regional expansion. South America remains underpenetrated, where shallow-draft steel boats undercut the acquisition costs of air-cushion vessels. Overall, the hovercraft market is increasingly mirroring global energy investment patterns, with high-growth corridors tied to wind-farm and hydrocarbon hubs.

- Griffon Hoverwork Ltd.

- Textron Systems Corporation (Textron Inc.)

- The British Hovercraft Company Ltd.

- Neoteric Hovercraft Inc.

- AEROHOD Ltd.

- Airlift Hovercraft Pty Ltd.

- CHRISTY HOVERCRAFT

- Hovertechnics, LLC.

- Ivanoff Hovercraft AB

- Bill Baker Vehicles Ltd.

- Mad Hovercraft

- Vigor Industrial LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for amphibious transport amid climate-driven floods

- 4.2.2 Military fleet replacement cycles for modern assault craft

- 4.2.3 Advances in low-noise electric and hydrogen propulsion

- 4.2.4 Relaxed regulations supporting commercial passenger services

- 4.2.5 Offshore energy and polar logistics requirements

- 4.2.6 Increased investment in flood-oriented emergency response

- 4.3 Market Restraints

- 4.3.1 High operating noise and coastal environmental restrictions

- 4.3.2 Scarcity of certified pilots and maintenance technicians

- 4.3.3 Competition from ground-effect and hydrofoil vessels

- 4.3.4 Fuel-cost volatility affecting military procurement cycles

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Hovercraft Size

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

- 5.2 By Application

- 5.2.1 Defense and Security

- 5.2.2 Passenger Ferry Services

- 5.2.3 Offshore Energy Support

- 5.2.4 Search and Rescue

- 5.2.5 Surveying and Mapping

- 5.2.6 Agricultural and Environmental Management

- 5.3 By Propulsion System

- 5.3.1 Diesel Engine

- 5.3.2 Gas Turbine

- 5.3.3 Hybrid-Electric

- 5.3.4 Fully Electric

- 5.3.5 Hydrogen Fuel-Cell

- 5.4 By End User

- 5.4.1 Military

- 5.4.2 Commercial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Griffon Hoverwork Ltd.

- 6.4.2 Textron Systems Corporation (Textron Inc.)

- 6.4.3 The British Hovercraft Company Ltd.

- 6.4.4 Neoteric Hovercraft Inc.

- 6.4.5 AEROHOD Ltd.

- 6.4.6 Airlift Hovercraft Pty Ltd.

- 6.4.7 CHRISTY HOVERCRAFT

- 6.4.8 Hovertechnics, LLC.

- 6.4.9 Ivanoff Hovercraft AB

- 6.4.10 Bill Baker Vehicles Ltd.

- 6.4.11 Mad Hovercraft

- 6.4.12 Vigor Industrial LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment