|

市場調查報告書

商品編碼

2066463

歐洲牙科設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Dental Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

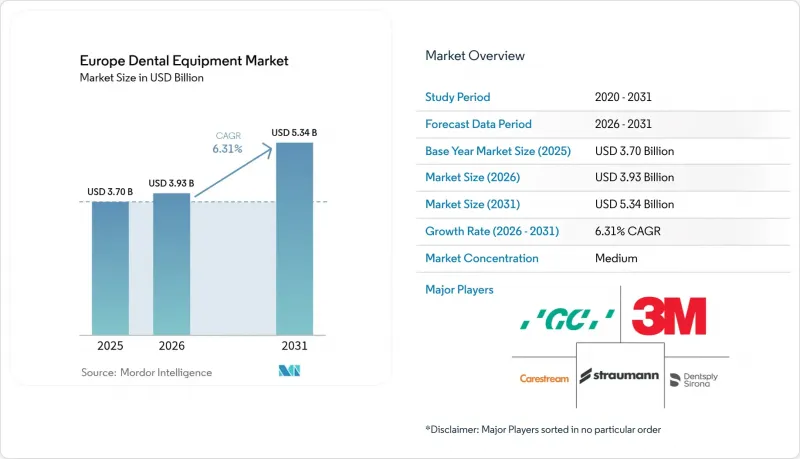

根據 Mordor Intelligence 預測,歐洲牙科設備市場規模將從 2025 年的 37 億美元成長到 2026 年的 39.3 億美元,然後在 2031 年達到 53.4 億美元,2026 年至 2031 年的複合年成長率為 6.31%。

本報告按產品(通用和診斷設備、牙科耗材等)、治療領域(正畸、牙髓病、牙周治療、修復)、最終用戶(牙科醫院、牙科診所等)和地區(德國、英國、法國、義大利、西班牙和其他歐洲國家)對產業進行細分。市場預測以美元計價。

歐洲牙科設備市場趨勢與洞察

牙科疾病發生率增加

歐洲牙科設備市場深受日益加重的疾病負擔影響,目前該地區超過一半的成年人口都受到疾病困擾。僅齲齒一項,就有33.6%的人口患有齲齒,25.2%的人口面臨嚴重的牙齒缺失,因此對修復設備和成像系統的需求持續旺盛。預計到2050年,重度牙周炎病例將會增加,這將促使牙科診所採用先進的牙周探針和攜帶式診斷設備。難民人口的湧入進一步加劇了牙科領域的需求缺口。在義大利接受檢查的烏克蘭兒童中,84%被發現患有齲齒,這凸顯了移動式X光設備和預防技術的必要性。這些流行病學因素預計將推動耗材、刮器和CAD/CAM相容型義齒的出貨量成長。

牙科產品創新

仿生玻璃離子黏固劑和奈米填料複合樹脂正在提高修復體的耐久性,降低再治療率,並縮短治療時間(materials-journal.com)。幾丁聚醣和膠原蛋白等天然聚合物正成為引導組織再生(GTR)薄膜的基礎材料,加速了相應分配裝置的臨床應用(materials-journal.com)。供應商正在將專用分配器和針對這些新型化學特性最佳化的固化燈整合到其產品中。二氧化鋯植入可作為光波導,實現動態生物膜去活化。這可減少高達85%的細菌數量,從而拓展了雷射相容型植入牙科手機的應用前景(microorganisms-journal.com)。隨著研發管線的擴展,銷售耗材和應用裝置套裝的供應商預計將在歐洲牙科器械市場中獲得持續的收入來源。

牙科治療保險報銷不足

各國的保險覆蓋模式各不相同,阻礙了技術的統一應用。在法國,只有60%的基本診療費由保險覆蓋,這降低了小規模牙科診所升級高性能影像設備的意願。在丹麥,成年人必須自付60%的費用,而瑞典的分級補貼制度則使自付費用存在不確定性,減緩了高成本雷射設備的早期普及(nhwstat.org)。英國的牙醫診所正面臨國民醫療服務體系(NHS)預算限制和資金儲備日益減少的困境,謝菲爾德的牙科診所難以償還近期擴張貸款就是一個例證。因此,租賃和付費使用制模式在歐洲牙科設備市場正變得越來越普遍。

細分市場分析

根據歐洲牙科設備市場規模數據,預計到2025年,牙科耗材將佔銷售額的58.05%,主要歸因於其規律性的採購週期以及在治療中不可或缺的地位。天然生物材料,例如藻酸鹽、纖維素和羥磷石灰,因其良好的生物相容性而備受臨床醫生青睞。供應商正致力於推出預裝式耗材盒,以簡化椅旁耗材的處理流程。同時,歐洲牙科設備產業也迎來了智慧耗材分配器的蓬勃發展,這些分配器能夠追蹤耗材使用情況並自動補貨,從而減少缺貨情況的發生。

雖然通用和診斷設備的銷量較小,但預計其成長率最高,到2031年複合年成長率將達到7.93%,這主要得益於人工智慧口腔內掃描儀和錐形束CT(CBCT)設備逐漸成為治療計劃中的標準配置。雷射設備是最具活力的細分領域,其中Er:YAG雷射系統可實現無瓣拔牙,而基於二極體雷射的牙周治療輔助設備則能顯著減少牙周組織深度。專注於耗材和診斷設備捆綁銷售的供應商,例如將感染控制試劑盒與成像感測器捆綁銷售的供應商,預計將進一步擴大其在歐洲牙科設備市場的佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 牙科疾病發生率增加

- 牙科產品創新

- 對美容牙科的需求日益成長

- 牙科解決方案的技術進步

- 在北歐國家,政府主導的口腔健康篩檢計畫正在推動影像診斷設備安裝數量的增加。

- 西班牙和匈牙利矯正旅遊業的蓬勃發展,帶動了對數位化口內掃描器的需求。

- 市場限制因素

- 牙科治療保險報銷不足

- 手術費用高昂

- 中東歐地區熟練的 CAD/CAM 技術人員短缺,減緩了牙體技術所自動化的普及。

- 亞洲OEM廠商的進入給入門級牙科手機。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品

- 通用診斷設備

- 牙科雷射

- 軟組織雷射

- 硬組織雷射治療

- 放射診斷設備

- 口外放射學設備

- 口內X光設備

- 牙科診療用椅和設備

- 其他通用和診斷設備

- 牙科雷射

- 牙科耗材

- 牙科生物材料

- 人工植牙

- 冠和橋

- 其他牙科耗材

- 其他牙科設備

- 通用診斷設備

- 按類型治療

- 正畸

- 根管治療

- 牙周病

- 修復學

- 最終用戶

- 牙科醫院

- 牙醫診所

- 學術研究機構

- 國家

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Dentsply Sirona

- Envista Holdings(KaVo Kerr)

- Planmeca Oy

- Straumann Group

- Align Technology, Inc.

- 3M Oral Care

- Ivoclar Vivadent

- GC Corporation

- Vatech Co., Ltd.

- Acteon Group

- Carestream Dental LLC

- A-dec Inc.

- Midmark Corporation

- Coltene Holding AG

- Ultradent Products Inc.

- DentalEZ Group

- Nobel Biocare Services AG

- Anthogyr SAS

- VOCO GmbH

- Osstem Implant Co.

- Eurodent Srl

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe dental equipment market size is expected to grow from USD 3.70 billion in 2025 to USD 3.93 billion in 2026 and is forecast to reach USD 5.34 billion by 2031 at 6.31% CAGR over 2026-2031.

This report Segments the Industry Into by Product (General and Diagnostics Equipment, Dental Consumables and More), by Treatment (Orthodontic, Endodontic, Peridontic, Prosthodontic), by End User (Dental Hospitals, Dental Clinics, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Dental Equipment Market Trends and Insights

Increasing Incidence of Dental Diseases

The Europe dental equipment market is heavily influenced by a rising disease burden that now affects more than half of the region's adults who.int. Dental caries alone afflict 33.6% of residents, while 25.2% experience significant tooth loss, generating steady demand for restorative devices and imaging systems. Severe periodontitis cases are projected to escalate through 2050, prompting practices to adopt advanced periodontal probes and portable diagnostic units. Refugee cohorts amplify unmet need: 84% of Ukrainian children examined in Italy showed caries, underscoring the requirement for mobile X-ray and preventive technologies . Collectively, these epidemiological pressures are set to lift unit shipments across consumables, scalers, and CAD/CAM-enabled prosthetics.

Innovation in Dental Products

Biomimetic glass ionomer cements and nanofilled composite resins are improving longevity of restorations, lowering retreatment rates, and reducing chair time materials-journal.com. Natural polymers such as chitosan and collagen now underpin guided tissue regeneration membranes, boosting clinical adoption of compatible delivery equipment materials-journal.com. Equipment vendors are integrating dedicated dispensers and curing lights optimized for these new chemistries. Zirconium dioxide implants act as optical waveguides that allow photodynamic biofilm inactivation, cutting bacterial counts by as much as 85% and opening opportunities for laser-ready implant handpieces microorganisms-journal.com. As R&D pipelines widen, suppliers that bundle consumables with application devices stand to capture recurring revenue streams across the Europe dental equipment market.

Lack of Proper Reimbursement of Dental Care

Fragmented national coverage models hinder uniform technology rollouts. France reimburses only 60% of basic consultations, dampening appetite for premium imaging upgrades among smaller practices. Denmark requires adults to pay 60% of fees, while Sweden's tiered subsidy introduces copay uncertainty, blunting early adoption of high-cost lasers nhwstat.org. UK clinics, grappling with constrained NHS budgets, face reduced capital reserves, as evidenced by practices in Sheffield struggling to service recent expansion loans. As a result, leasing and pay-per-use models are gaining ground within the Europe dental equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Cosmetic Dentistry

- Technological Advancements in Dental Solutions

- High Cost of Surgeries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Europe dental equipment market size data show dental consumables captured 58.05% revenue share in 2025 on the back of recurring purchase cycles and procedural indispensability. Natural biomaterials such as alginate, cellulose, and hydroxyapatite are winning clinician favor for their biocompatibility, pushing suppliers to introduce pre-dosed cartridges that simplify chairside handling materials. The Europe dental equipment industry is simultaneously witnessing a leap in smart dispensers that track usage and automate reordering, reducing stockouts.

General and diagnostics equipment, although smaller by revenue, is posting the fastest 7.93% CAGR through 2031 as AI-ready intraoral scanners and CBCT units become routine for treatment planning. Lasers represent the most dynamic subcategory because Er:YAG systems now enable flapless extractions, while diode-laser periodontal adjuncts deliver measurable reductions in probing depth. Suppliers focused on bundling consumables with diagnostics-such as infection-control kits packaged with imaging sensors-stand to deepen wallet share in the Europe dental equipment market.

List of Companies Covered in this Report:

- Dentsply Sirona

- Envista Holdings (KaVo Kerr)

- Planmeca

- Straumann Group

- Align Technology

- 3M Oral Care

- Ivoclar Vivadent

- GC Corporation

- Vatech Co., Ltd.

- Acteon Group

- Carestream Dental

- A-dec

- Midmark

- Coltene Holding

- Ultradent Products

- DentalEZ Group

- Nobel Biocare Services

- Anthogyr

- VOCO

- Osstem Implant Co.

- Eurodent Srl

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Dental Diseases

- 4.2.2 Innovation in Dental Products

- 4.2.3 Increasing Demand for Cosmetic Dentistry

- 4.2.4 Technological Advancements in Dental Solutions

- 4.2.5 Government-sponsored oral-health screening programs expanding imaging fleet in Nordics

- 4.2.6 Orthodontic tourism inflow to Spain & Hungary boosting demand for digital intra-oral scanners

- 4.3 Market Restraints

- 4.3.1 Lack of Proper Reimbursement of Dental Care

- 4.3.2 High Cost of Surgeries

- 4.3.3 Shortage of trained CAD/CAM technicians in CEE slows lab automation uptake

- 4.3.4 Price compression in entry-level handpieces due to Asian OEM influx

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 General and Diagnostics Equipment

- 5.1.1.1 Dental Laser

- 5.1.1.1.1 Soft Tissue Lasers

- 5.1.1.1.2 Hard Tissue Lasers

- 5.1.1.2 Radiology Equipment

- 5.1.1.2.1 Extra Oral Radiology Equipment

- 5.1.1.2.2 Intra-oral Radiology Equipment

- 5.1.1.3 Dental Chair and Equipment

- 5.1.1.4 Other General and Diagnostic equipment

- 5.1.1.1 Dental Laser

- 5.1.2 Dental Consumables

- 5.1.2.1 Dental Biomaterial

- 5.1.2.2 Dental Implants

- 5.1.2.3 Crowns and Bridges

- 5.1.2.4 Other Dental Consumables

- 5.1.3 Other Dental Devices

- 5.1.1 General and Diagnostics Equipment

- 5.2 By Treatment

- 5.2.1 Orthodontic

- 5.2.2 Endodontic

- 5.2.3 Peridontic

- 5.2.4 Prosthodontic

- 5.3 By End User

- 5.3.1 Dental Hospitals

- 5.3.2 Dental Clinics

- 5.3.3 Academic & Research Institutes

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Dentsply Sirona

- 6.3.2 Envista Holdings (KaVo Kerr)

- 6.3.3 Planmeca Oy

- 6.3.4 Straumann Group

- 6.3.5 Align Technology, Inc.

- 6.3.6 3M Oral Care

- 6.3.7 Ivoclar Vivadent

- 6.3.8 GC Corporation

- 6.3.9 Vatech Co., Ltd.

- 6.3.10 Acteon Group

- 6.3.11 Carestream Dental LLC

- 6.3.12 A-dec Inc.

- 6.3.13 Midmark Corporation

- 6.3.14 Coltene Holding AG

- 6.3.15 Ultradent Products Inc.

- 6.3.16 DentalEZ Group

- 6.3.17 Nobel Biocare Services AG

- 6.3.18 Anthogyr SAS

- 6.3.19 VOCO GmbH

- 6.3.20 Osstem Implant Co.

- 6.3.21 Eurodent Srl

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球牙科銼市場:機會與策略展望(至2035年)

全球牙科銼市場:機會與策略展望(至2035年) 2026-2030年全球牙科設備市場

2026-2030年全球牙科設備市場 牙科壓縮機市場規模、佔有率和成長分析:按產品類型、技術、移動性、容量、壓力範圍、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

牙科壓縮機市場規模、佔有率和成長分析:按產品類型、技術、移動性、容量、壓力範圍、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 全球牙科器械市場:按產品和最終用戶分類-預測(至2031年)

全球牙科器械市場:按產品和最終用戶分類-預測(至2031年) 牙科刺激器市場預測至2034年:按類型、應用、最終用戶和地區分類的全球分析

牙科刺激器市場預測至2034年:按類型、應用、最終用戶和地區分類的全球分析 牙科鉗市場規模、佔有率和趨勢分析報告:按類型、材質、應用、分銷管道、最終用途、地區和細分市場預測(2026-2033 年)

牙科鉗市場規模、佔有率和趨勢分析報告:按類型、材質、應用、分銷管道、最終用途、地區和細分市場預測(2026-2033 年) 牙科設備及耗材市場:2026-2032年全球市場預測(按產品類型、技術、材料類型、患者類型、分銷管道、最終用戶和應用分類)

牙科設備及耗材市場:2026-2032年全球市場預測(按產品類型、技術、材料類型、患者類型、分銷管道、最終用戶和應用分類) 牙科設備市場規模、佔有率和成長分析:按類型、產品類型、最終用戶和地區分類-2026-2033年產業預測

牙科設備市場規模、佔有率和成長分析:按類型、產品類型、最終用戶和地區分類-2026-2033年產業預測 牙科手用器材市場:依產品類型、材料、應用、最終用戶和地區分類牙科設備市場:按產品、治療方法、最終用戶和地區分類

牙科手用器材市場:依產品類型、材料、應用、最終用戶和地區分類牙科設備市場:按產品、治療方法、最終用戶和地區分類