|

市場調查報告書

商品編碼

2066460

農業接種劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Agricultural Inoculants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

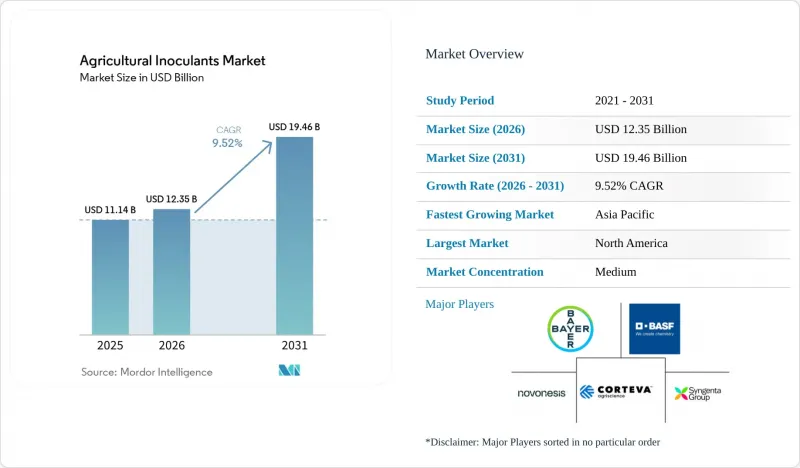

根據 Mordor Intelligence 預測,農業接種劑市場規模將從 2025 年的 111.4 億美元成長到 2026 年的 123.5 億美元,然後在 2031 年達到 194.6 億美元,2026 年至 2031 年的複合年成長率為 9.52%。

本報告按功能(作物營養和生物防治劑)、微生物(細菌、真菌、病毒)、施用方法(種子處理、土壤處理、葉面噴布)、作物類型(穀類、油籽、經濟作物等)、劑型(液體、固體)和地區(北美、亞太、南美等)進行分類。預測值以美元計價。

全球農業接種劑市場趨勢及洞察

有機農地的擴張和對無殘留食品的需求。

由於有機農業的擴張和全球食品價值鏈中更嚴格的殘留標準,農業接種劑市場正在成長。歐盟和北美的消費者越來越需要殘留量極低的農產品,這推動了生物來源作物投入品的普及。這一趨勢不僅限於高價值的水果和蔬菜,還擴展到了大規模的田間作物。歐盟委員會的《2025年生物經濟框架》將生物基肥料和生物植物保護產品列為戰略重點,並推動將其融入農業永續性舉措。對於生產商而言,將產品定位為「零殘留」可以擴大市場准入,並在以合規為導向的銷售管道中確保價格穩定,從而提升接種劑在永續性發展應用之外的商業性價值。

引入生物肥料以抵消合成材料的價格波動

此外,隨著農民採用微生物營養產品來降低對化肥價格波動的依賴並提高養分利用效率,農業接種劑市場正在不斷擴大。許多農場正在將接種劑納入現有的養分管理系統,以促進固氮和磷吸收,而不是完全取代合成肥料。這種方法在依賴化肥進口的農業經濟體中尤其重要,因為投入成本的波動會顯著影響農場的盈利。發表在《植物》(Plants)雜誌上的一項研究表明,在巴西的一些大豆種植區,接種慢生根瘤菌(Bradyrhizobium)和巴西固氮螺菌(Azospirillum brasilense)的混合物,通過替代尿素,顯著降低了成本並直接提高了盈利。這項發現凸顯了生產者為何將這些產品視為有效的經濟工具。該研究還表明,接種劑的應用不僅僅是作為傳統肥料的替代品,而是作為綜合營養管理方案的一部分。因此,農業接種劑市場正受益於投入成本的降低和盈利的提高。

土壤和氣候條件導致的性能差異

由於微生物活性高度依賴土壤溫度、濕度、pH值、種植歷史和本地微生物群落等因素,其性能的變異性仍然是農業接種劑市場面臨的主要挑戰。因此,與合成肥料相比,接種劑在田間表現往往缺乏穩定性,尤其是在大規模農業生產和環境條件波動的情況下。工業微生物學的研究表明,接種劑的有效性仍然顯著受到環境條件、載體設計和施用後存活條件的影響。這種變異性導致種植者缺乏信心,因為他們需要可預測的投入效果以進行可靠的規劃。除非提供更準確的田間施用建議,否則農業接種劑市場可能會繼續面臨推廣受阻的問題,尤其是在氣候和土壤容易產生變異性的地區。

細分市場分析

到2025年,生物防治劑將佔據最大的市場佔有率,達到58.1%,在所有功能類別中對農業接種劑市場做出最大貢獻。這一主導地位歸因於主要害蟲系統對合成農藥的抗藥性日益增強,以及主要作物市場對某些化學活性成分的監管日益嚴格。與其他生物防治劑類別相比,農業接種劑市場繼續依賴生物防治劑,並受益於其完善的商業基礎設施。巴斯夫公司(BASF SE)、Valent BioSciences LLC和Koppert Biological Systems BV等公司在該領域擁有強大的生物害蟲管理產品組合,確保了全球供給能力和經銷商的信心。

作物營養領域是成長最快的領域,預計到2031年將以5.1%的複合年成長率成長。這一成長反映了生產者在提高營養效率方面方法的廣泛轉變。在農業接種劑市場,生物促效劑的銷售方式正日益多元化,不再僅僅將其視為普通的植物保健補充劑,而是作為增強養分吸收和應對脅迫的實用工具。這項轉變意義重大,因為農藝師現在可以將生物促效劑納入低施肥方案,而無需農民完全取代傳統系統。 2026年3月,BASF公司完成了對AgBiTech集團的收購,顯示領先的農業材料公司越來越重視將生物技術融入其產品組合策略和長期成長計畫。因此,儘管成熟的生物防治平台仍然是收入的主要來源,但以營養為重點的農業接種劑產品正在加速成長。

預計到2025年,細菌將佔最大的市場佔有率,達到43.4%,成為農業接種劑市場中微生物種類最重要的細分市場。這一主導地位源自於根瘤菌屬(Bradyrhizobium)、巴西固氮螺旋菌(Azospirillum brasilense)和枯草芽孢桿菌(Bacillus subtilis)等菌株的長期商業性應用,這些菌株可用於固氮、養分活化和促進植物生長。在農業接種劑市場,細菌產品具有註冊流程完善、應用廣泛(適用於大豆、豆類和穀物種植系統)等優勢。南美洲在該領域扮演著至關重要的角色,因為根瘤菌產品與豆類作物生產和大豆種植的獲利能力密切相關。雖然真菌接種劑也發揮重要作用,尤其是在園藝和土壤傳播病害防治方面,但細菌產品仍是各地區商業性基礎最廣泛的產品。

病毒是微生物學領域成長最快的細分市場,預計到2031年將以8.0%的複合年成長率成長。這一成長主要得益於核多污泥病毒技術在防治難以控制的鱗翅目害蟲方面的應用日益廣泛。病毒防治害蟲的生產力提高、田間驗證以及規模化應用能力的增強,正推動農業接種劑市場對此細分市場給予更多關注。

區域分析

北美仍然是最大的區域貢獻者,在2025年佔據了農業接種劑市場佔有率的32.1%。這得益於強大的零售網路、先進的農業諮詢體係以及大豆和玉米生產中較高的採用率。隨著微生物產品被有效地整合到以種子處理、作物保護和永續性重點的農業計畫中,美國繼續引領區域需求。 2025年,Pivot Bio公司透過其N-OVATOR計畫進一步加速了產品應用,並擴大了在玉米帶的零售夥伴關係,進一步強化了生物投入在提高農業生產力和環境績效方面的作用。

亞太地區是成長最快的區域市場,預計到2031年將維持6.8%的複合年成長率。這一成長主要受化肥成本上漲、政府對生物來源材料的支持以及農業推廣計劃的擴展所驅動。由於監管政策的完善提高了生物來源產品的商業化標準,印度仍然是一個重要的成長市場。 2024年9月,Novonesis A/S與印度農民合作社有限公司(KRIBHCO)合作,在印度推出了針對主要作物的菌根生物肥料,從而加強了其在該地區的業務。澳洲也透過推廣精密農業,為該地區的成長提供支持。

歐洲仍然是農業接種劑的重要市場,但其成長在一定程度上受到歐盟現行微生物法規的限制。歐盟委員會正在對這些法規進行審查,審查結果可能會逐步擴大已通過核准微生物產品的清單。南美洲仍然是一個主要的成長區域,尤其是巴西,該國大規模的大豆種植和對化肥進口的依賴推動了對生物來源材料需求的成長。中東和非洲市場規模仍然小規模,但迄今為止其較低的採用率使其對業界具有吸引力,尤其是在豆科作物生產系統中,因為透過新的分銷和諮詢模式,這些地區仍有拓展空間。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 有機農地的擴張和對零農藥殘留食品的需求。

- 引入生物肥料以抵消合成材料的價格波動

- 為保護生技藥品和低殘留作物提供政策支援。

- 引入種子處理方法以提高噴灑精度

- 對綜合生物計劃在農場應用的需求

- 透過配方和封裝技術的創新延長保存期限。

- 市場限制因素

- 土壤和氣候條件導致的性能差異

- 農民更傾向於使用速效合成替代品

- 多菌株微生物產品報名手續的複雜性

- 微生物配送中的低溫運輸與污染風險

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按功能

- 作物營養

- 生物防治劑

- 微生物

- 細菌

- 芽孢桿菌屬

- 固氮菌

- 根瘤菌屬和慢生根瘤菌屬

- 磷酸鹽可溶性細菌

- 真菌

- 木黴

- 菌根

- 白殭菌

- 金屬二異質性

- 病毒

- 細菌

- 透過應用方法

- 種子處理

- 土壤處理

- 葉面噴布

- 按作物類型

- 穀物和穀類

- 豆類和油籽

- 經濟作物

- 水果和蔬菜

- 其他用途

- 配方

- 液體

- 乾燥

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- Bayer AG

- Novonesis A/S

- Corteva, Inc.

- Syngenta Group Co., Ltd.

- Valent BioSciences LLC

- Premier Tech Ltd.

- Lallemand Inc.

- Bioceres Crop Solutions Corp.

- Verdesian Life Sciences LLC

- Groundwork BioAg Ltd.

- Pivot Bio, Inc.

- Koppert Biological Systems BV

- XiteBio Technologies Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the agricultural inoculants market size is projected to grow from USD 11.14 billion in 2025 to USD 12.35 billion in 2026 and is forecast to reach USD 19.46 billion by 2031 at 9.52% CAGR over 2026-2031.

This report is Segmented by Function (Crop Nutrition and Biocontrol Agents), Microorganism (Bacteria, Fungi, and Viruses), Mode of Application (Seed Treatment, Soil Treatment, and Foliar Spray), Crop Type (Grains and Cereals, Oilseeds, Commercial Crops, and More), Formulation (Liquid and Dry), and Geography (North America, Asia-Pacific, South America, and More). Forecasts are in Terms of Value (USD).

Global Agricultural Inoculants Market Trends and Insights

Organic Acreage Expansion and Residue-Free Food Demand

The agricultural inoculants market is experiencing growth due to the expansion of organic farming and stricter residue standards in global food supply chains. Consumers in the European Union and North America are increasingly demanding agricultural products with minimal residues, driving the adoption of biological crop inputs. This trend is extending beyond high-value fruits and vegetables to include large-scale field crops. In 2025, the European Commission's bioeconomy framework identified bio-based fertilizers and biological plant-protection products as strategic priorities, promoting their integration into agricultural sustainability initiatives. For growers, positioning products as residue-free enhances market access and ensures pricing stability in compliance-driven sales channels, thereby strengthening the commercial importance of inoculants beyond sustainability-focused applications.

Biofertilizer Adoption to Offset Synthetic Input Cost Volatility

The agricultural inoculants market is also growing as farmers adopt microbial nutrition products to reduce dependence on volatile fertilizer prices and improve nutrient-use efficiency. Instead of completely replacing synthetic fertilizers, many farms are incorporating inoculants to enhance nitrogen fixation and phosphorus uptake within conventional nutrient-management systems. This approach is particularly significant in fertilizer-import-dependent agricultural economies, where input-cost fluctuations can heavily impact farm profitability. A study published in Plants demonstrated that co-inoculation with Bradyrhizobium species and Azospirillum brasilense in certain regions of Brazil's soybean cultivation resulted in significant savings in urea replacement and direct profitability gains. This finding highlights why growers consider these products as effective economic tools. The same study also shows that inoculants are being adopted as part of integrated nutrient programs rather than as simple substitutes for conventional fertilizers. As a result, the Agricultural inoculants market is benefiting from both input cost discipline and better return visibility.

Performance Variability Across Soil and Climate Conditions

Performance variability remains a significant challenge for the agricultural inoculants market, as microbial activity is highly dependent on factors such as soil temperature, moisture, pH, crop history, and native microbial populations. Consequently, inoculants often exhibit inconsistent field performance compared to synthetic inputs, particularly in large-scale farming operations and under varying environmental conditions. Industrial microbiology highlights that the efficacy of inoculants remains significantly influenced by environmental conditions, carrier design, and post-application survival conditions. This variability contributes to a trust gap, as growers seek predictable input responses for reliable planning. Without more precise field recommendations, the agricultural inoculants market is likely to continue to face hesitation in regions with climates and soils that yield inconsistent results.

Other drivers and restraints analyzed in the detailed report include:

- Policy Support for Biologicals and Lower-Residue Crop Protection

- Seed Treatment Adoption to Improve Application Precision

- Farmer Preference for Fast-Acting Synthetic Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Biocontrol agents accounted for the largest market share at 58.1% in 2025, making the most significant contribution to the agricultural inoculants market across functional categories. This dominance is attributed to increasing resistance to synthetic pesticides in key pest systems and stricter regulations on certain chemically active ingredients in major crop markets. The agricultural inoculants market continues to rely on biocontrol agents, as they benefit from a well-established commercial infrastructure compared to other biological categories. Companies such as BASF SE, Valent BioSciences LLC, and Koppert Biological Systems B.V. operate in this segment with robust biological pest management portfolios, ensuring global supply capabilities and distributor confidence.

Crop nutrition is the fastest-growing function, projected to expand at a CAGR of 5.1% through 2031. This growth reflects a broader shift in how growers approach nutrient efficiency. In the agricultural inoculants market, biostimulants are increasingly marketed as practical tools for enhancing nutrient uptake and managing stress, rather than as optional plant health supplements. This shift is significant as agronomists can now integrate biostimulants into reduced-rate fertilizer programs, rather than requiring farmers to completely replace conventional systems. In March 2026, BASF SE completed the acquisition of AgBiTech Group, emphasizing the growing focus of major crop input companies on integrating biological technologies into their portfolio strategies and long-term growth plans. Consequently, while mature biocontrol platforms continue to anchor revenue, nutrition-focused products are growing faster in the agricultural inoculants market.

Bacteria accounted for the largest market share in 2025, at 43.4%, representing the most significant segment of the agricultural inoculants market by microorganism. This dominance is attributed to the long-standing commercial use of strains such as Bradyrhizobium, Azospirillum brasilense, and Bacillus subtilis, which are utilized for nitrogen fixation, nutrient mobilization, and plant growth enhancement. In the agricultural inoculants market, bacterial products benefit from established registration processes and widespread application in soybean, pulse, and cereal systems. South America plays a critical role in this segment, as rhizobial products are closely linked to legume production and the economic viability of soybean cultivation. While fungal inoculants are also significant, particularly in horticulture and soil-borne disease management, bacteria continue to provide the broadest commercial base across regions.

Viruses represent the fastest-growing segment of microorganisms, with a projected CAGR of 8.0% through 2031. This growth is driven by the increasing adoption of nucleopolyhedrovirus technologies for managing challenging lepidopteran pests. The agricultural inoculants market is focusing more on this segment as advancements in production economics and field validation make virus-based pest control more scalable.

Geography Analysis

North America held 32.1% of the agricultural inoculants market share in 2025 and remained the largest regional contributor. Strong retailer networks, advanced agronomic advisory systems, and high adoption across soybean and corn production supported this. The United States continues to lead regional demand as microbial products integrate efficiently with seed treatment, crop protection, and sustainability-focused farming programs. In 2025, Pivot Bio, Inc. further expanded adoption through its N-OVATOR program and broader retail partnerships across the Corn Belt. This reinforced the role of biological inputs in improving both farm productivity and environmental performance.

Asia-Pacific is the fastest regional segment with a projected 6.8% CAGR through 2031. This growth is driven by fertilizer cost pressures, government support for biological inputs, and expanding agronomic extension programs. India remains a key growth market as regulatory formalization improves commercialization standards for biological products. In September 2024, Novonesis A/S strengthened its regional presence through its partnership with Krishak Bharati Cooperative Limited (KRIBHCO) to distribute mycorrhizal biofertilizers across major Indian crops. Australia also supports regional growth by increasing the adoption of precision agriculture.

Europe remains an important market for agricultural inoculants, although growth is partly constrained by current European Union regulations governing microorganisms. Ongoing regulatory reviews by the European Commission may gradually expand the list of approved microbial products. South America continues to be a major growth region, particularly in Brazil, where large-scale soybean cultivation and reliance on fertilizer imports are driving rising demand for biological inputs. The Middle East and Africa remain smaller markets but are attracting increasing industry attention because lower historical adoption leaves room for expansion through new distribution and advisory models, particularly in legume production systems.

- BASF SE

- Bayer AG

- Novonesis A/S

- Corteva, Inc.

- Syngenta Group Co., Ltd.

- Valent BioSciences LLC

- Premier Tech Ltd.

- Lallemand Inc.

- Bioceres Crop Solutions Corp.

- Verdesian Life Sciences LLC

- Groundwork BioAg Ltd.

- Pivot Bio, Inc.

- Koppert Biological Systems B.V.

- XiteBio Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Organic acreage expansion and residue-free food demand

- 4.2.2 Biofertilizer adoption to offset synthetic input cost volatility

- 4.2.3 Policy support for biologicals and lower-residue crop protection

- 4.2.4 Seed treatment adoption to improve application precision

- 4.2.5 On-farm compatibility demand for integrated biological programs

- 4.2.6 Shelf-life gains from formulation and encapsulation innovation

- 4.3 Market Restraints

- 4.3.1 Performance variability across soil and climate conditions

- 4.3.2 Farmer preference for fast-acting synthetic alternatives

- 4.3.3 Registration complexity for multi-strain microbial products

- 4.3.4 Cold-chain and contamination risk in microbe distribution

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Crop Nutrition

- 5.1.2 Biocontrol Agents

- 5.2 By Microorganism

- 5.2.1 Bacteria

- 5.2.1.1 Bacillus

- 5.2.1.2 Azotobacter

- 5.2.1.3 Rhizobium and Bradyrhizobium

- 5.2.1.4 Phosphate-solubilizing bacteria

- 5.2.2 Fungi

- 5.2.2.1 Trichoderma

- 5.2.2.2 Mycorrhiza

- 5.2.2.3 Beauveria bassiana

- 5.2.2.4 Metarhizium anisopliae

- 5.2.3 Viruses

- 5.2.1 Bacteria

- 5.3 By Mode of Application

- 5.3.1 Seed Treatment

- 5.3.2 Soil Treatment

- 5.3.3 Foliar Spray

- 5.4 By Crop Type

- 5.4.1 Grains and Cereals

- 5.4.2 Pulses and Oilseeds

- 5.4.3 Commercial Crops

- 5.4.4 Fruits and Vegetables

- 5.4.5 Other Applications

- 5.5 By Formulation

- 5.5.1 Liquid

- 5.5.2 Dry

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Italy

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Kenya

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Novonesis A/S

- 6.4.4 Corteva, Inc.

- 6.4.5 Syngenta Group Co., Ltd.

- 6.4.6 Valent BioSciences LLC

- 6.4.7 Premier Tech Ltd.

- 6.4.8 Lallemand Inc.

- 6.4.9 Bioceres Crop Solutions Corp.

- 6.4.10 Verdesian Life Sciences LLC

- 6.4.11 Groundwork BioAg Ltd.

- 6.4.12 Pivot Bio, Inc.

- 6.4.13 Koppert Biological Systems B.V.

- 6.4.14 XiteBio Technologies Inc.