|

市場調查報告書

商品編碼

2066440

無人海洋系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Unmanned Sea Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

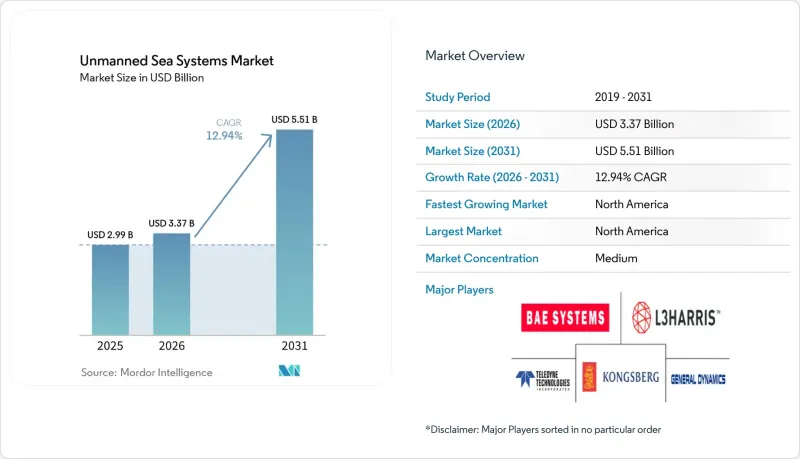

根據 Mordor Intelligence 預測,無人海洋系統市場規模將從 2025 年的 29.9 億美元成長到 2026 年的 33.7 億美元,到 2031 年將達到 55.1 億美元,2026 年至 2031 年的複合年成長率為 12.94%。

本報告按平台類型(無人水下航行器 (UUV) 和無人水面航行器 (USV))、航行器尺寸(小型、中型和大型)、推進系統(電動、混合動力等)、應用領域(軍事和商業)、組件類型(船體、自主導航系統、感測器系統等)以及地區(北美、歐洲等)進行細分。市場預測以美元 (USD) 計價。

全球無人海洋系統市場趨勢及洞察

全球擴大海軍現代化和部隊轉型計劃

在國防採購領域,自主平台的重要性日益凸顯,成為提升作戰能力、提高在競爭激烈的海上環境中作戰效率的重要手段。新推出的項目和原型表明,水雷戰、情報、監視與偵察(ISR)能力以及分佈式水下效應器正從實驗階段邁向艦隊作戰計劃的整合階段。 2026年2月,洛克希德·馬丁公司發布了「七鰓鰻」多用途自主水下航行器,這是一款模組化潛水器,配備可重建有效載荷艙,可支援情報、監視與偵察、電子戰和動能作戰任務。薩博公司正在根據國家合約開發一款大型水下航行器,專注於遠端阻礙力和海底防禦,並透過支援戰略防禦目標的官方歐洲計畫來實現這一目標。北約正在透過標準和框架正式建立互通性,以緩解多國特遣部隊內部的整合挑戰。這些措施將加快自主資產的部署進度,並實現模組化有效載荷現代化的標準化,從而提高盟軍艦隊的作戰效率。

離岸風力發電。

隨著離岸風力發電運營商業務的擴張,自主巡檢對於平衡有限的運營預算與嚴格的ESG合規要求至關重要。 2023年4月,Fugro公司利用其Blue Essence無人水面艇(USV)和Blue Volta電動遙控潛水器(eROV)完成了首次完全遠端操控的離岸風力發電電場巡檢。歐洲風電場相關人員正在採用自主技術來減少人員出行並延長巡檢窗口期,現場部署也已證明,這些技術在營運成本和持續監測的正常運作運作方面具有顯著優勢。這些努力透過減少天氣造成的停機時間、將勞動力從海上轉移到陸地以及縮短巡檢投資的回收期,進一步強化了「無人運作」的概念。這為無人平台建立了穩固的需求基礎,並得到了多個風電場區域穩健的運維合約的支持。

出口管制條例和國際武器貿易條例限制了全球銷售。

許可法規和國防物資分類延長了自動駕駛車輛和有效載荷的貿易週期,迫使供應商在通用的合規框架內優先考慮本地化生產、定製配置或本地化銷售。提供模組化架構的公司可以透過有效載荷升級來增強功能,從而避免平台重新認證,進而減輕後續批次的合規負擔。這些趨勢有利於擁有完善合規團隊和完善品質系統的成熟公司,並可能將市場佔有率轉移到監管路徑更為清晰的地區。

細分市場分析

2025年,無人水下航行器(UUV)的銷售額佔總銷售額的62.24%。這主要歸功於客戶在情報、監視與偵察(ISR)以及高風險區域的水雷戰中優先考慮隱蔽性、續航力和低可偵測性。在水下船隊中,儘管遙控潛水器(ROV)在作業和檢查任務中仍佔據主導地位,但自主水下航行器(AUV)憑藉其改進的路線規劃、分類和自主性,在廣域勘測方面正迅速崛起。市場上許多大型專案仍然依賴具有模組化艙室的深海船體,這種設計能夠快速更換有效載荷,從而縮短升級前置作業時間,而無需更換整個平台。在水面領域,遠端操作中心的普及以及支援持續無人檢查和巡邏任務的法規核准,正在推動無人水下航行器的應用日益廣泛。無人水面載具(USV)的成長率高達13.99%,在風電場巡檢等應用場景的推動下,其市場成長最為顯著。在風電場巡檢等應用場景中,無人水面載具作為電動遙控潛水器(ROV)的母船,即使在惡劣天氣條件下也能實現持續作業。平台製造商提供即插即用的有效載荷套件,無需對船體進行重大重新設計,即可柔軟性滿足國防和商業領域的各種應用需求。

法律規範也導致水面和水下系統市場准入途徑的差異。國際海事組織(IMO)正在製定《無人水面船舶安全規則》(MASS規則),該規則將成為無人水面船舶碰撞規避、遠端操作資格要求和網路彈性等方面的管治基礎。一些國家主管機關正在頒發具有里程碑意義的無人海上作業許可證,並建立陸基船長執照制度。這表明,商用無人水面載具(USV)的永續運作模式正在逐步建立。對於水下平台,分類規則仍然適用,重點是壓力安全、冗餘以及在特定任務剖面中對結構化自主性的檢驗。這兩個領域的成長都得益於模組化感測器和自主系統堆疊,這些堆疊可跨平台類型轉移,同時最大限度地減少整合負擔。

預計到2025年,小型船舶將佔據49.20%的市場佔有率,並有望以13.40%的複合年成長率實現最快成長,因為買家更傾向於可手動部署且可從陸地控制多台設備的系統。在訓練和探險應用場景中,無需大型船舶即可進行投放和回收的船舶具有優勢,從而降低租賃成本並提高部署頻率。在無人海洋系統市場,這些特性體現在更短的預算週期和更柔軟性的任務調度上,從而提高正常運轉率和整體生命週期價值。中型船舶在有效負載容量、航程以及運輸和甲板操作的實用性之間取得了平衡,使其成為測量公司和能源相關客戶的理想選擇,這些客戶需要在專案之間輪換使用設備。這類船舶通常包括作業用遙控潛水器(ROV)和中等深度自主水下航行器(AUV),它們需要強大的導航能力和動力來源來應對長時間的任務。資本投入最大的大型和超大型車輛用於戰略任務、深海任務或長期巡邏任務,因為這些任務的深度和持續時間足以證明其高昂的單位成本是合理的。

特定任務的採購趨勢影響國防和商業船隊中哪些尺寸範圍的船艇發展最為迅速。國防掃雷部隊和情報、監視與偵察 (ISR) 人員傾向於選擇中小型船艇,因為它們部署迅速、具備分散式感測能力,並且在短週期內可重複使用性高。另一方面,商業營運與維護 (O&M) 團隊既可以使用小型船艇進行渦輪機檢查,也可以使用中型船艇覆蓋勘測區域,這些船艇通常以水面/水下雙船配置運作。雖然從單位經濟性的角度來看,小型船艇在高頻任務中具有優勢,但深海作業能力強的高階船艇在海底測繪和戰略水下基礎設施監測等應用中佔據主導地位。在所有尺寸的船艇中,以軟體為中心的自主導航和集群控制技術進一步提升了感測器融合和指揮中間件的價值,使其能夠應用於整個船隊,而不僅僅是單一船艇。

區域分析

預計到2025年,北美將佔全球銷售額的38.36%,並將維持該地區最高的成長率,到2031年複合年成長率將達到14.09%。這主要得益於持續的採購以及在反人員、反大規模水雷戰和情報、監視與偵察(ISR)領域積極的原型開發項目。新型多用途自主水下航行器(AUV)的引入和測試取得了里程碑式的進展,凸顯了日益成熟的開發平臺,該體系將與潛艇相容的航行器與自主水面技術整合到一個更大的艦隊概念中。該地區的無人海上系統市場也持續交付反水雷設備,這些設備汲取了衝突地區的經驗教訓,提供可快速部署的模組化系統。美國和加拿大的供應商正透過垂直整合的有效載荷和與現有國防框架相連接的自主控制系統來鞏固其領先地位。隨著離岸風力發電和環境監測合約的簽訂,商業活動也在不斷擴大,相關核准和基礎設施建設也在穩步推進,以支援大規模無人作業。

在歐洲,這些技術的部署在國防和民用領域同步推進,尤其是在北海、波羅的海和大西洋航道沿線。斯堪地那維亞國家在無人操作許可、遠端操作和零排放法規方面持續處於領先地位,這些法規與自主式和電池驅動車輛的部署相契合,進而促進了這些技術在民用領域的應用,例如巡檢和後勤保障。歐洲國防項目包括大型水下航行器和集群項目,旨在進行海底測繪、水雷探測和深海基礎設施保護。民用業者持續檢驗使用無人水面航行器(USV)和遙控水下航行器(ROV)組合進行風力渦輪機全天候巡檢的工作流程,與載人勘測船相比,這種組合在燃油消耗和排放氣體方面具有優勢。該地區的政策環境和項目集中度正在持續推動對適用於高緯度地區和快速變化海況的平台和感測器的需求。

亞太地區的需求主要受國防能力現代化、離岸風力發電擴張以及複雜海岸線海域態勢感知需求的驅動。該地區的研究表明,超大型無人水下載具(UUV)在續航能力、潛水深度和導航穩定性方面均有所提升,這預示著一場激烈的技術研發競賽將推動採購總量的成長。韓國和新加坡正透過國內計畫和夥伴關係,持續將自主技術融入海上安全和商業活動。同時,在澳大利亞,採購活動與在印太地區持續進行的監視和阻礙力行動密切相關。預計在全部區域,如果各國法規與海上自主系統(MASS)類型的管治相符,且能源和港口管理部門允許在受管航道上進行無人作業,則無人技術的部署速度將會加快。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球擴大海軍現代化和部隊重組計劃

- 對離岸風力發電電場巡檢和海底勘測任務的需求日益成長。

- 與載人水面艦艇相比,每海浬成本更低

- 擴大採用具有群聚能力的無人水面載具(USV)進行水雷對抗。

- 無人船舶的ESG相關保險折扣

- 國防抵銷政策旨在促進美國海軍在國內的一體化。

- 市場限制因素

- 出口限制和國際武器貿易條例(ITAR)限制了全球銷售

- 衝突地區極易受到全球導航衛星系統(GNSS)阻塞的影響

- 獲得認證的海事人工智慧保障和測試設施數量有限。

- 鈦酸鋰電池供應中斷對注重耐用性的平台的影響。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依平台類型

- 無人水下航行器(UUV)

- 遙控潛水器(ROV)

- 自主水下航行器(AUV)

- 無人水面載具(USV)

- 遙控水面航行器(ROSV)

- 自主水面船舶(ASV)

- 無人水下航行器(UUV)

- 按車輛類型

- 小型

- 中等的

- 大的

- 透過推進力

- 電的

- 混合

- 柴油引擎和燃氣渦輪機

- 可再生能源(太陽能和波浪能)

- 透過使用

- 軍隊

- 情報、監視和偵察(ISR)

- 反水雷措施(MCM)

- 反潛戰(ASW)

- 物流和供應

- 商業

- 環境監測

- 基礎設施檢查

- 水文測量

- 其他

- 軍隊

- 依組件類型

- 船體

- Autonomy Suite

- 通訊與導航

- Sensors Suite

- 推進和動力系統

- 其他(有效載荷、發射和回收系統)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 其他南美國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- TKMS GmbH

- BAE Systems plc

- General Dynamics Corporation

- Lockheed Martin Corporation

- Unique Group

- Teledyne Technologies Incorporated

- Saab AB

- L3Harris Technologies, Inc.

- Maritime Robotics AS

- The Boeing Company

- Exail Technologies SA

- Elbit Systems Ltd.

- SAILDRONE, Inc.

- EDGE Group PJSC

- SeaRobotics Corporation

- Ocean Aero

- Textron Inc.

- Sea Machines Robotics, Inc.

- Thales Group

- Kongsberg Gruppen ASA

第7章 市場機會與未來展望

According to Mordor Intelligence, the unmanned sea systems market size is expected to grow from USD 2.99 billion in 2025 to USD 3.37 billion in 2026 and is forecast to reach USD 5.51 billion by 2031 at a 12.94% CAGR over 2026-2031.

This report is Segmented by Platform Type (Unmanned Underwater Vehicles (UUVs) and Unmanned Surface Vehicles (USVs)), Vehicle Size (Small, Medium, and Large), Propulsion (Electric, Hybrid, and More), Application (Military and Commercial), Component Type (Hull, Autonomy Suite, Sensors Suite, and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Unmanned Sea Systems Market Trends and Insights

Expansion of Global Naval Modernization and Force Transformation Programs

Defense procurement emphasizes autonomous platforms as force multipliers for operational efficiency in contested maritime environments. Newly introduced programs and prototypes highlight navies' progression from experimental phases to operational integration of mine warfare, ISR capabilities, and distributed undersea effectors in fleet planning. Lockheed Martin Corporation introduced the Lamprey Multi-Mission Autonomous Undersea Vehicle in February 2026 as a modular submersible with a reconfigurable payload bay to support ISR, electronic warfare, and kinetic missions. Saab AB advances large undersea vehicles under national contracts, focusing on long-range deterrence and seabed defense, through formal European programs supporting strategic defense objectives. NATO is formalizing interoperability through standards and frameworks, reducing integration challenges for multinational task groups. These measures accelerate deployment timelines for autonomous assets and standardize modular payload updates, enhancing operational efficiency across allied fleets.

Rising Demand for Offshore Wind Farm Inspection and Seabed Survey Missions

Autonomous inspection is critical as offshore wind operators expand operations, balancing limited O&M budgets with stringent ESG compliance requirements. In April 2023, Fugro conducted the first fully remote offshore wind farm inspection using its Blue Essence USV and Blue Volta eROV. European wind-farm stakeholders are introducing autonomy to reduce crew transfers and expand inspection windows, with field deployments that reveal strong operating cost and uptime benefits for persistent monitoring. These initiatives enhance zero-crew concepts by mitigating weather-related downtime, transitioning labor from sea to shore, and streamlining inspection payback. This establishes a dependable pipeline for unmanned platforms, underpinned by resilient O&M contracts across multiple wind basins.

Export Control Regulations and ITAR Restrictions Limiting Global Sales

Licensing regulations and defense article classifications extend transaction cycles for autonomous vehicles and payloads, prompting vendors to localize production, customize configurations, or prioritize sales within regions aligned with shared compliance frameworks. Companies that deliver modular architectures can advance capability through payload upgrades that avoid fresh platform certifications, a method that can reduce the compliance burden on subsequent tranches. These dynamics collectively favor incumbents with established compliance teams and documented quality systems and can nudge market share toward geographies with clearer regulatory pathways.

Other drivers and restraints analyzed in the detailed report include:

- Declining Cost per Sea Mile Compared to Crewed Surface Vessels

- Increased Adoption of Swarm-Capable USVs for MCM Operations

- High Vulnerability to GNSS Denial in Contested Maritime Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Unmanned Underwater Vehicles (UUVs) accounted for 62.24% of 2025 revenue, as customers prioritized stealth, endurance, and low-observable signatures for ISR and mine warfare in high-risk zones. Within subsurface fleets, ROVs hold a larger installed base for manipulation and inspection tasks, while AUVs are scaling faster as route planning, classification, and autonomy improve for wide-area survey. The market continues to anchor many of its premium programs on deep-rated hulls with modular bays that support rapid payload swaps, which compresses upgrade timelines versus full platform replacement. On the surface, rising adoption is being driven by remote operations centers and regulatory green lights that support persistent, uncrewed inspection and patrol missions. USVs grow fastest at 13.99%, reinforced by wind-farm inspection use cases, where uncrewed surface craft act as motherships for electric ROVs, enabling continuous operation through challenging weather. Platform makers that deliver plug-and-play payload suites gain flexibility to address both defense and commercial workflows without major hull redesigns.

Regulatory frameworks also differentiate the pathway to market for surface and subsurface systems. The International Maritime Organization is progressing the MASS Code, which provides the governance foundation for collision avoidance, remote operations qualifications, and cyber resilience for uncrewed surface vessels. Select national authorities have issued precedent-setting permits for uncrewed offshore operations and are building licensing regimes for shore-based masters, a move that signals durable operating models for commercial USVs. Subsurface platforms continue to follow classification rules that emphasize pressure safety, redundancy, and the validation of structured autonomy across specific mission profiles. Growth on both vectors is strengthened by modular sensors and autonomy stacks that can migrate across platform types with limited integration overhead.

Small-class vehicles captured 49.20% of the 2025 share and are set to deliver the fastest growth, 13.40% CAGR, as buyers favor hand-deployable systems and multi-asset control from shore. Training and expeditionary use cases benefit from vehicles that can be launched and recovered without the need for large ships, reducing charter costs and expanding deployment frequency. The unmanned sea systems market rewards these attributes with shorter budgeting cycles and mission-scheduling agility, thereby lifting utilization and total lifecycle value. Medium-class formats balance payload and endurance with transport and deck-handling practicalities, which make them well-suited for survey firms and energy customers that rotate assets across projects. This class is the typical home for work-class ROVs and mid-depth AUVs that require robust navigation and power for longer missions. The most capital-intensive large and extra-large vehicles serve strategic, deep-ocean, or long-patrol missions where mission depth and duration justify higher unit costs.

Procurement preferences by mission profile influence which size bands scale fastest across defense and commercial fleets. Defense mine warfare teams and ISR operators lean toward small and medium classes for rapid deployment, distributed sensing, and high reusability across short cycles. Commercial O&M teams can justify both small units for turbine inspections and medium units for survey coverage, often in paired surface-subsurface configurations. Unit economics favor small vehicles for high-frequency tasks, while deep-rated premium vehicles dominate applications such as seabed mapping and strategic undersea infrastructure monitoring. Across all sizes, software-centric autonomy and swarm control are pushing more value into sensor fusion and command middleware that span fleets rather than single hulls.

Geography Analysis

North America accounted for 38.36% of 2025 revenue and is projected to register the fastest regional CAGR of 14.09% through 2031, supported by ongoing procurement and active prototype programs across mine warfare and ISR. New multi-mission AUV introductions and test milestones underscore a maturing pipeline that blends submarine-compatible vehicles and surface autonomy within larger fleet concepts. The unmanned sea systems market in the region also reflects serial deliveries of mine countermeasures that leverage lessons from contested theaters to deliver modular systems ready for rapid deployment. The US and Canadian suppliers reinforce leadership with vertically integrated payloads and autonomy stacks linked to established defense frameworks. Commercial activity is growing from offshore wind and environmental monitoring contracts, with approvals and infrastructure emerging to support uncrewed operations at scale.

Europe shows synchronized defense and commercial adoption, especially in the North Sea, Baltic, and Atlantic corridors. Scandinavian countries continue to pioneer uncrewed permitting, remote operations, and zero-emission mandates that align with autonomous, battery-electric deployments, which, in turn, catalyze commercial inspection and logistics use cases. European defense programs include large undersea vehicles and swarm projects that target seabed mapping, mine hunting, and infrastructure protection at depth. Commercial operators continue to validate 24/7 inspection workflows for wind assets using USVs paired with ROVs, with fuel and emissions benefits relative to crewed survey ships. This region's policy environment and project density create durable demand for both platforms and sensors suited to high latitudes and variable sea states.

Asia-Pacific demand is driven by defense modernization, offshore wind build-out, and maritime domain awareness needs along complex coastlines. Regional research output highlights advancing capabilities in extra-large UUVs across endurance, depth, and navigation resilience, pointing to a competitive technology race that drives aggregate procurement. South Korea and Singapore continue to integrate autonomy into maritime security and commercial operations through domestic programs and partnerships. At the same time, Australia's ecosystem ties procurement to persistent Indo-Pacific monitoring and deterrence. Across the region, swifter adoption is likely where national rules align with MASS-style governance and where energy and port authorities enable zero-crew operations in controlled corridors.

- TKMS GmbH

- BAE Systems plc

- General Dynamics Corporation

- Lockheed Martin Corporation

- Unique Group

- Teledyne Technologies Incorporated

- Saab AB

- L3Harris Technologies, Inc.

- Maritime Robotics AS

- The Boeing Company

- Exail Technologies SA

- Elbit Systems Ltd.

- SAILDRONE, Inc.

- EDGE Group PJSC

- SeaRobotics Corporation

- Ocean Aero

- Textron Inc.

- Sea Machines Robotics, Inc.

- Thales Group

- Kongsberg Gruppen ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of global naval modernization and force transformation programs

- 4.2.2 Rising demand for offshore wind farm inspection and seabed survey missions

- 4.2.3 Declining cost per sea mile compared to crewed surface vessels

- 4.2.4 Increased adoption of swarm-capable USVs for MCM operations

- 4.2.5 ESG-linked Insurance Discounts for Zero-crew Craft

- 4.2.6 Defense offset policies promoting domestic integration of USS

- 4.3 Market Restraints

- 4.3.1 Export control regulations and ITAR restrictions limiting global sales

- 4.3.2 High vulnerability to GNSS denial in contested maritime environments

- 4.3.3 Limited availability of certified maritime AI-assurance and testing ranges

- 4.3.4 Disruptions in lithium-titanate battery supply impacting endurance-focused platforms

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 Unmanned Underwater Vehicles (UUVs)

- 5.1.1.1 Remotely Operated Vehicles (ROVs)

- 5.1.1.2 Autonomous Underwater Vehicles (AUVs)

- 5.1.2 Unmanned Surface Vehicles (USVs)

- 5.1.2.1 Remotely Operated Surface Vehicles (ROSVs)

- 5.1.2.2 Autonomous Surface Vehicles (ASVs)

- 5.1.1 Unmanned Underwater Vehicles (UUVs)

- 5.2 By Vehicle Size

- 5.2.1 Small

- 5.2.2 Medium

- 5.2.3 Large

- 5.3 By Propulsion

- 5.3.1 Electric

- 5.3.2 Hybrid

- 5.3.3 Diesel and Gas-Turbine

- 5.3.4 Renewable (Solar/Wave)

- 5.4 By Application

- 5.4.1 Military

- 5.4.1.1 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.4.1.2 Mine Counter-Measures (MCM)

- 5.4.1.3 Anti-Submarine Warfare (ASW)

- 5.4.1.4 Logistics and Resupply

- 5.4.2 Commercial

- 5.4.2.1 Environment Monitoring

- 5.4.2.2 Infrastructure Inspection

- 5.4.2.3 Hydrographic Survey

- 5.4.2.4 Others

- 5.4.1 Military

- 5.5 By Component Type

- 5.5.1 Hull

- 5.5.2 Autonomy Suite

- 5.5.3 Communications and Navigation

- 5.5.4 Sensors Suite

- 5.5.5 Propulsion and Power Systems

- 5.5.6 Others (Payload, Launch/Recovery systems)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 TKMS GmbH

- 6.4.2 BAE Systems plc

- 6.4.3 General Dynamics Corporation

- 6.4.4 Lockheed Martin Corporation

- 6.4.5 Unique Group

- 6.4.6 Teledyne Technologies Incorporated

- 6.4.7 Saab AB

- 6.4.8 L3Harris Technologies, Inc.

- 6.4.9 Maritime Robotics AS

- 6.4.10 The Boeing Company

- 6.4.11 Exail Technologies SA

- 6.4.12 Elbit Systems Ltd.

- 6.4.13 SAILDRONE, Inc.

- 6.4.14 EDGE Group PJSC

- 6.4.15 SeaRobotics Corporation

- 6.4.16 Ocean Aero

- 6.4.17 Textron Inc.

- 6.4.18 Sea Machines Robotics, Inc.

- 6.4.19 Thales Group

- 6.4.20 Kongsberg Gruppen ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment