|

市場調查報告書

商品編碼

2066439

無人機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Unmanned Aerial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

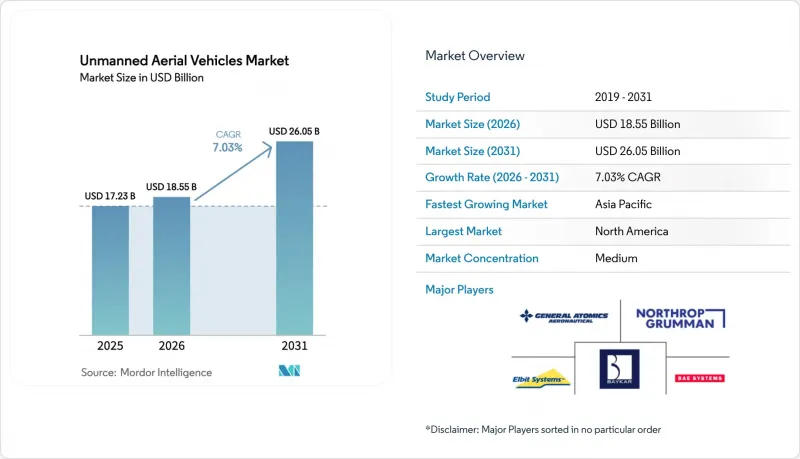

根據 Mordor Intelligence 預測,無人機 (UAV) 市場將從 2025 年的 172.3 億美元成長到 2026 年的 185.5 億美元,然後從 2026 年到 2031 年以 7.03% 的複合年成長率成長,到 2031 年達到 260.5 億美元。

本報告按無人機等級(I級(150公斤以下)、II級(150-600公斤)、III級(600公斤以上))、平台類型(固定翼、旋翼、混合動力)、操作模式(遙控、可選駕駛、全自主)、應用領域(作戰、情報、監視與偵察、物資投送、旋轉彈藥運輸)和地區(北美地區運輸)進行細分(北美旋轉彈藥運輸)。市場預測以美元計價。

全球無人機(UAV)市場趨勢與洞察

國防預算的增加正在推動無人機機隊的擴張。

戰場演示表明,即使是價格低廉的無人機也能取得以往只有有人駕駛裝備才能達到的效果,這促使世界各國國防部擴大無人機(UAV)的採購規模。印度已批准在2027年投入35億美元,用於研發國產無人機平台,以維持喜馬拉雅山脈的監視能力。此類預算撥款凸顯了無人機研發重點從卓越生存能力轉向數量,烏克蘭的例子便是例證,該國低成本無人機已大規模摧毀了敵方裝甲車輛。由於多域作戰需要持續偵察和快速攻擊,世界各國議會在其他預算項目削減的情況下,仍繼續保障與無人機相關的支出。因此,穩定的訂單基礎得以形成,供應商收入維持穩定,下一代系統的研發風險也得以降低。

對即時、全天候情報、監視與偵察(ISR)的實際需求。

指揮官們呼籲全天候監視,以將殺傷鏈從數小時縮短至數分鐘。到2024年底,美國空軍的MQ-9「死神」無人機機隊飛行時間將超過300萬小時,其中70%將用於情報、監視和偵察(ISR)任務,而非作戰任務。以色列的「赫爾墨斯900」行動展示了持續的晝夜監視能力,這構成了當前作戰理論的基礎,即無論天氣如何,都能從感測器獲取資訊。合成孔徑雷達和光電負荷提供的影像能夠穿透雲層,限制敵方隱藏行動的能力。隨著競爭對手分散兵力並利用偽裝,即時影像串流的價值日益凸顯,推動了多感測器飛機的採購,並加速了老舊飛機的有效載荷升級。

嚴格的出口管制和安全規定

飛彈及其技術管制制度(MTCR)禁止射程超過300公里、酬載超過500公斤的系統,導致市場需求分散,部分國家政府轉而依賴國內供應商。美國聯邦採購條例(FAR)40.2進一步限制使用中國製造的零件,增加了系統整合商的重新設計成本。以色列逐案核准的許可製度延緩了大規模海外銷售,為政治約束較少的土耳其供應商創造了機會。這些法規共同導致西方主要製造商可進入的無人機市場規模縮小,銷售週期延長,進而促使資金流入新興經濟體的國內項目。

細分市場分析

重量低於150公斤的I類平台將在2025年佔據44%的銷售額,凸顯了營級單位的有機情報、監視與偵察(ISR)目前佔據了市場需求的大部分。這些輕型無人機的成本低於10萬美元,採用現成組件,無需跑道即可起飛,使得預算有限的軍隊也能部署數百架。就以金額為準,I類平台在無人機市場中佔據最大佔有率,但隨著許多軍隊完成初始部署,其成長速度正在放緩。重量在150公斤至600公斤之間的II類平台預計將以7.55%的複合年成長率推動市場擴張,填補袖珍型四旋翼無人機和戰略性高空遠程(HALE)系統之間的空白。該系列無人機具備12小時飛行時間和多感測器能力等優勢,同時還可由C-130級運輸機運輸,這種機動性優勢符合遠徵部隊的需求。重量超過600公斤的III級平台在遠程情報、監視和偵察(ISR)以及攻擊任務中仍具有重要的戰略意義,但其超過3000萬美元的單價阻礙了其廣泛應用。

來自烏克蘭的快速作戰回饋表明,Bayraktar TB2 在 II 類無人機中表現出色,能夠在不增加大型無人機後勤負擔的情況下進行精確打擊。通用原子公司的 Mojave 短距起降型無人機也瞄準了這一類別,承諾可在公共道路上飛行,並且有效載荷與傳統的 Reaper 無人機通用。同時,旋翼式彈藥在 I 類無人機中仍然得到積極採購, 開關閘刀 600 和 Harop 的各種型號為最輕型無人機增加了反裝甲能力。最終,無人機市場在 I 類無人機的大批量訂單和 II 類無人機的成本績效合約之間保持著平衡,而 III 類無人機項目則擴大提供捆綁式服務契約,以減輕其高昂價格的影響。

預計到2025年,固定翼飛機將佔總銷售量的74.78%,這反映了其無與倫比的續航力和負載容量重量比。在戰略情報、監視和偵察(ISR)領域,20小時的續航時間和1500公里的航程足以證明跑道和起落架投資的合理性。旋翼無人機在都市區和山區等需要懸停的地區發揮特殊作用,但其續航時間通常僅4小時。混合動力垂直起降(VTOL)機型,即可在垂直起飛和飛行巡航之間切換的機型,預計將以9.25%的複合年成長率成長,這是所有平台類型中成長最快的。海軍之所以關注這類飛機,是因為多數艦艇甲板缺乏彈射器。貝爾公司的V-247「警戒者」傾轉傾斜式旋翼於2016年完成了甲板測試,證明了這個概念的可行性。

混合動力平台正憑藉更高的電池密度和輕量化複合材料旋翼,在無人機市場的新飛機製造支出中佔據越來越大的佔有率。諾斯羅普·格魯曼公司取消的「燕鷗」(Tern)計畫仍然展示了尾座式飛機的空氣動力學特性,一些新創公司正在將這些知識應用於小型補給飛機。固定翼飛機製造商則以可拆卸助推吊艙來應對,這種吊艙無需彈射器和自動著陸演算法,模糊了不同類型飛機之間的界限。旋翼飛機製造商則專注於整合用於近程偵察的感測器桅杆和近乎靜音的電動旋翼。儘管固定翼飛機仍然是收入的主要來源,但混合動力垂直起降(VTOL)機型的成長預示著未來將向靈活部署和海上作業方向發展。

區域分析

預計到2025年,北美將佔全球收入的40.12%,這得益於美國每年在無人系統上超過120億美元的支出。諸如協同作戰飛機(CCA)等項目旨在到本世紀末實現1000架自主護航飛機的交付,從而確保國內主要製造商擁有穩定的訂單儲備。加拿大訂購用於北極監視的「天空衛士」(SkyGuardian)無人機表明,其應用領域已多元化,涵蓋維護國家主權的任務;而墨西哥的「赫爾墨斯900」(Hermes 900)無人機機隊則用於應對打擊販毒集團的行動,這擴大了區域需求,使其不再局限於與類似對手發生戰爭的假設。強大的創業融資降低了智慧財產權壁壘,使得數十家軟體新創公司得以進入供應鏈。

亞太地區是成長最快的地區,年複合成長率達8.29%。中國正在大規模生產「翼潛鳥」(Wing Loon)和「CH」系列無人機,並出口到不受飛彈及其技術控制制度(MTCR)約束的中東買家。印度的「CATS Warrior」計畫計畫在2028年採購200架無人機,這將降低其對以色列進口的依賴。澳洲部署MQ-4C「海神」(Triton)無人機將增強其廣闊專屬經濟區(EEZ)的海上情境察覺,而日本部署「海上衛士」(SeaGuardian)無人機也顯示其在東海地區有著類似的優先事項。圍繞台灣和南海的地區緊張局勢正在推動採購,而韓國和印尼的主要國內企業正在競相爭取鄰近的東南亞市場佔有率。

歐洲、中東和非洲構成了剩餘的市場機會。在俄羅斯2022年入侵烏克蘭後,歐洲北約成員國加快了採購步伐。德國訂購了MQ-4C「海神」無人機,法國則延長了其「死神」無人機的服務壽命。土耳其透過放寬出口限制並出售TB2和「阿昆齊」無人機打破了僵局,在中亞和北非站穩了腳跟。在中東,以色列、阿拉伯聯合大公國和沙烏地阿拉伯正在為其機隊升級多感測器負荷,但預算和油價波動仍影響升級進度。非洲仍處於發展初期。南非的派拉蒙集團和肯亞的早期計畫都顯示出復甦跡象,但基礎設施和資金的匱乏阻礙了其廣泛應用。南美洲由於資金限制而落後,但巴西的巴西航空工業公司RQ-900無人機表明,當邊境監視成為戰略必需時,本土產業可以崛起。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 國防預算的增加推動了無人機數量的成長。

- 對即時、全天候情報、監視與偵察(ISR)的實際需求。

- 機載自主技術與人工智慧驅動的任務系統快速發展

- 有人和無人協作(「皇家僚機」)的概念正被納入採購週期。

- 「消耗型無人機」策略降低了大規模部署的成本門檻。

- 衛星網狀網路可在 GPS 無法覆蓋的戰區實現高彈性的超視距通訊。

- 市場限制因素

- 嚴格的出口管制和安全禁令(例如,飛彈及其技術管制制度、聯邦採購條例40.2)

- 高空長航時/中空長航時平台的購買成本與生命週期成本高昂

- 電子戰和無人機系統威脅環境日益加劇

- 供應鏈安全法規導致零件短缺和成本上升。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 無人機類型

- 一級(150公斤以下)

- 二級(150-600公斤)

- 三級(600公斤或以上)

- 依平台類型

- 固定翼飛機

- 旋翼飛機

- 混合

- 透過操作模式

- 遙控

- 可選控制類型

- 完全自主

- 透過使用

- 戰鬥

- 情報、監視和偵察(ISR)

- 送貨

- 輪值市政當局

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 其他南美國家

- 歐洲

- 英國

- 法國

- 德國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AeroVironment

- Airbus SE

- BAE Systems plc

- BAYKAR AS

- The Boeing Company

- Elbit Systems Ltd.

- General Atomics

- Israel Aerospace Industries Ltd.

- Kratos Defense & Security Solutions, Inc.

- Leonardo SpA

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Saab AB

- Textron Systems Corporation

- Turkish Aerospace Industries(TAI)

- QinetiQ Group

- Hindustan Aeronautics Limited

- Korean Aerospace Industries(KAI)

- Griffon Aerospace, Inc.

- Teledyne Technologies Incorporated

- Griffon Aerospace, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the unmanned aerial vehicles market is expected to grow from USD 17.23 billion in 2025 to USD 18.55 billion in 2026, and is forecasted to reach USD 26.05 billion by 2031 at a 7.03% CAGR over 2026-2031.

This report is Segmented by UAV Class (Class I (Below 150 Kg), Class II (150-600 Kg), Class III (Above 600 Kg)), Platform Type (Fixed-Wing, Rotary-Wing, Hybrid), Mode of Operation (Remotely Piloted, Optionally Piloted, Fully Autonomous), Application (Combat, ISR, Delivery, Loitering Munition), and Geography (North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Unmanned Aerial Vehicles Market Trends and Insights

Rising Defense Budgets Fueling UAV Fleet Expansion

Defense ministries have increased the procurement of unmanned aerial vehicles after battlefield evidence demonstrated that inexpensive drones can deliver results previously achievable only with manned assets. India approved USD 3.5 billion for indigenous platforms through 2027 to sustain Himalayan surveillance. These allocations underscore a shift from exquisite survivability to quantity, mirroring Ukraine's experience, where low-cost drones neutralized armor at scale. As multi-domain operations demand persistent sensing and rapid strike cycles, legislatures continue to ring-fence UAV spending even where other line items decline. The outcome is a steady baseline of orders that stabilizes supplier revenue and de-risks R&D for next-generation systems.

Operational Demand for Real-Time, All-Weather ISR

Commanders seek 24-hour coverage that compresses kill chains from hours to minutes. The US Air Force's MQ-9 Reaper fleet exceeded 3 million flight hours by late 2024, with 70% logged in ISR sorties rather than kinetic missions. Israeli Hermes 900 operations demonstrated actual day-night persistence, informing doctrine that now expects sensor feeds regardless of weather. Synthetic-aperture radar and electro-optical payloads deliver cloud-penetrating imaging, limiting adversaries' ability to mask movements. As peer competitors disperse assets and employ camouflage, real-time feeds become more valuable, reinforcing procurement of multi-sensor airframes and driving payload upgrades to legacy fleets.

Stringent Export-Control and Security-Prohibition Regimes

The Missile Technology Control Regime (MTCR) bars systems with a range beyond 300 km and a payload over 500 kg, fragmenting demand and steering some governments toward indigenous suppliers. US FAR 40.2 further restricts the use of components of Chinese origin, adding redesign costs for integrators. Case-by-case licensing in Israel delays large foreign sales, creating an opportunity for Turkish vendors that face fewer political constraints. Cumulatively, these rules shrink the accessible unmanned aerial vehicles market for Western primes and elongate sales cycles, diverting capital toward domestic programs in emerging economies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Advances in Onboard Autonomy and AI-Driven Mission Systems

- Manned-Unmanned Teaming Concepts Entering Procurement Cycles

- High Acquisition and Life-Cycle Cost of HALE/MALE Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class I platforms, which weigh under 150 kg, accounted for 44% of 2025 revenue, underscoring that organic ISR at the battalion level currently dominates demand. These lightweight airframes cost under USD 100,000, utilize commercial parts, and launch without runways, allowing budget-constrained forces to field hundreds of units. In dollar terms, Class I accounted for the largest share of the unmanned aerial vehicles market; however, growth moderates as many armies complete their initial rollouts. Class II platforms, weighing between 150 kg and 600 kg, are forecast to lead the expansion at a 7.55% CAGR, bridging the gap between pocket-sized quadcopters and strategic HALE systems. The segment benefits from 12-hour endurance and multi-sensor payloads yet still fits on C-130-class transports, a mobility advantage that resonates with expeditionary forces. Class III platforms weighing more than 600 kg maintain strategic relevance for long-range ISR and strike, but unit costs exceeding USD 30 million discourage widespread adoption.

Rapid operational feedback from Ukraine validated the Class II impact of the Bayraktar TB2, which delivered precision strikes without the logistics footprint of larger drones. General Atomics' Mojave STOL variant targets this category, promising highway operations and payload commonality with legacy Reapers. Meanwhile, loitering munitions keep Class I procurement lively, as Switchblade 600 and Harop variants add anti-armor punch to the lowest weight class. Ultimately, the UAV market balances high-volume Class I orders with value-dense Class II contracts, while Class III programs increasingly bundle service contracts to ease sticker shock.

Fixed-wing airframes accounted for 74.78% of 2025 revenue, reflecting their unmatched endurance and payload-to-weight ratios. For strategic ISR, 20-hour loiter times and 1,500 km range justify investments in runways and arresting gear. Rotary-wing drones serve specialized roles in urban or mountainous terrain, where hovering is essential, but their endurance typically lasts only four hours. Hybrid VTOL models that take off vertically then transition to wing-borne cruise are forecast to expand at a 9.25% CAGR, the fastest clip across the platform-type continuum. Navies prize such airframes because most ship decks lack catapults; Bell's V-247 Vigilant tilt-rotor completed deck trials in 2016, proving the concept viable.

Hybrid platforms now capture new-build spending in the UAV market, benefiting from improved battery density and lightweight composite rotors. Northrop Grumman's canceled Tern project nevertheless validated tail-sitting aerodynamics, and several startups apply those lessons to smaller resupply craft. Fixed-wing manufacturers respond with detachable booster pods and autoland algorithms to avoid catapults, blurring the lines between categories. Rotary-wing suppliers focus on sensor-mast integration and near-silent electric rotors for close-quarters reconnaissance. While fixed-wing models remain the revenue anchor, the growth of hybrid VTOL models signals a long-term pivot toward flexible basing and maritime operations.

Geography Analysis

North America generated 40.12% of 2025 revenue, sustained by US outlays exceeding USD 12 billion annually for unmanned systems. Programs such as the Collaborative Combat Aircraft aim to achieve 1,000 autonomous escorts by this decade, ensuring a steady backlog for domestic primes. Canada's Arctic-domain surveillance orders for SkyGuardian drones illustrate diversification into sovereignty missions, while Mexico's Hermes 900 fleet addresses cartel interdiction, broadening regional demand beyond peer-war contingencies. Intellectual-property barriers remain low due to strong venture financing, enabling dozens of software startups to enter the supply chain.

The Asia-Pacific region is the fastest-growing theater, with an 8.29% CAGR. China mass-produces Wing Loong and CH-series drones and exports them to Middle Eastern buyers unconstrained by MTCR. India's CATS Warrior project aims to procure 200 units by 2028, thereby reducing its reliance on Israeli imports. Australia's MQ-4C Triton deals strengthen maritime domain awareness across vast Exclusive Economic Zones, and Japan's SeaGuardian acquisition signals similar priorities in the East China Sea. Regional tensions over Taiwan and the South China Sea catalyze procurement, while domestic champions in South Korea and Indonesia vie to capture adjacent Southeast Asian markets.

Europe, the Middle East, and Africa form the remaining opportunity set. European NATO members accelerated purchases after Russia's 2022 invasion of Ukraine; Germany ordered MQ-4C Tritons and France lengthened Reaper operations. Turkey disrupted the status quo by selling TB2 and Akinci drones under fewer export constraints, gaining footholds in Central Asia and North Africa. In the Middle East, Israel, the UAE, and Saudi Arabia are upgrading their fleets with multi-sensor payloads, although budgetary and oil-price fluctuations still influence the timing. Africa remains nascent; South Africa's Paramount Group and Kenya's embryonic programs indicate green shoots, but infrastructure and funding gaps temper uptake. South America lags due to fiscal constraints, yet Brazil's Embraer RQ-900 demonstrates that an indigenous industry can emerge when border surveillance is a strategic imperative.

List of Companies Covered in this Report:

- AeroVironment

- Airbus SE

- BAE Systems plc

- BAYKAR A.S.

- The Boeing Company

- Elbit Systems Ltd.

- General Atomics

- Israel Aerospace Industries Ltd.

- Kratos Defense & Security Solutions, Inc.

- Leonardo S.p.A

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Saab AB

- Textron Systems Corporation

- Turkish Aerospace Industries (TAI)

- QinetiQ Group

- Hindustan Aeronautics Limited

- Korean Aerospace Industries (KAI)

- Griffon Aerospace, Inc.

- Teledyne Technologies Incorporated

- Griffon Aerospace, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising defense budgets fueling UAV fleet expansion

- 4.2.2 Operational demand for real-time, all-weather ISR

- 4.2.3 Rapid advances in onboard autonomy and AI-driven mission systems

- 4.2.4 Manned-unmanned teaming ("loyal wingman") concepts entering procurement cycles

- 4.2.5 Attritable-drone doctrine lowering cost threshold for mass deployment

- 4.2.6 Satellite-mesh networking enabling resilient BVLOS comms in GPS-contested theaters

- 4.3 Market Restraints

- 4.3.1 Stringent export-control and security-prohibition regimes (e.g., MTCR, FAR 40.2)

- 4.3.2 High acquisition and life-cycle cost of HALE/MALE platforms

- 4.3.3 Escalating electronic-warfare/counter-UAS threat environment

- 4.3.4 Supply-chain security restrictions driving component scarcity and cost inflation

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By UAV Class

- 5.1.1 Class I (Below 150 kg)

- 5.1.2 Class II (150-600 kg)

- 5.1.3 Class III (Above 600 kg)

- 5.2 By Platform Type

- 5.2.1 Fixed-wing

- 5.2.2 Rotary-wing

- 5.2.3 Hybrid

- 5.3 By Mode of Operation

- 5.3.1 Remotely Piloted

- 5.3.2 Optionally Piloted

- 5.3.3 Fully Autonomous

- 5.4 By Application

- 5.4.1 Combat

- 5.4.2 Intelligence, Surveillance & Reconnaissance (ISR)

- 5.4.3 Delivery

- 5.4.4 Loitering Munition

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 France

- 5.5.3.3 Germany

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AeroVironment

- 6.4.2 Airbus SE

- 6.4.3 BAE Systems plc

- 6.4.4 BAYKAR A.S.

- 6.4.5 The Boeing Company

- 6.4.6 Elbit Systems Ltd.

- 6.4.7 General Atomics

- 6.4.8 Israel Aerospace Industries Ltd.

- 6.4.9 Kratos Defense & Security Solutions, Inc.

- 6.4.10 Leonardo S.p.A

- 6.4.11 Lockheed Martin Corporation

- 6.4.12 Northrop Grumman Corporation

- 6.4.13 Saab AB

- 6.4.14 Textron Systems Corporation

- 6.4.15 Turkish Aerospace Industries (TAI)

- 6.4.16 QinetiQ Group

- 6.4.17 Hindustan Aeronautics Limited

- 6.4.18 Korean Aerospace Industries (KAI)

- 6.4.19 Griffon Aerospace, Inc.

- 6.4.20 Teledyne Technologies Incorporated

- 6.4.21 Griffon Aerospace, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

民用無人機市場:按類型、組件、推進系統、技術類型、應用和銷售管道分類-2026-2032年全球市場預測多旋翼無人機市場:按類型、組件、航程、推進系統、有效載荷能力、應用、終端用戶產業和銷售管道分類-2026-2032年全球市場預測

民用無人機市場:按類型、組件、推進系統、技術類型、應用和銷售管道分類-2026-2032年全球市場預測多旋翼無人機市場:按類型、組件、航程、推進系統、有效載荷能力、應用、終端用戶產業和銷售管道分類-2026-2032年全球市場預測 無人機降落傘回收系統市場規模、佔有率和成長分析:按類型、無人機類型、部署觸發方式、最終用戶、通路和地區分類-2026-2033年產業預測

無人機降落傘回收系統市場規模、佔有率和成長分析:按類型、無人機類型、部署觸發方式、最終用戶、通路和地區分類-2026-2033年產業預測 2026-2030年全球用於重大事件監測的無人機市場

2026-2030年全球用於重大事件監測的無人機市場 2026年全球無人機市場報告

2026年全球無人機市場報告 固定翼無人機系統市場報告:趨勢、預測與競爭分析(至2035年)無人機(UAV)市場報告:趨勢、預測和競爭分析(至2035年)無人機市場:2026-2032年全球市場預測(按平台、航程、推進技術、應用和最終用戶分類)懸浮摩托車市場:2026-2032年全球市場預測(依推進方式、價格範圍、飛行範圍、應用、最終用戶和銷售管道)2026年全球微型無人機(UAV)有機偵察套件市場報告

固定翼無人機系統市場報告:趨勢、預測與競爭分析(至2035年)無人機(UAV)市場報告:趨勢、預測和競爭分析(至2035年)無人機市場:2026-2032年全球市場預測(按平台、航程、推進技術、應用和最終用戶分類)懸浮摩托車市場:2026-2032年全球市場預測(依推進方式、價格範圍、飛行範圍、應用、最終用戶和銷售管道)2026年全球微型無人機(UAV)有機偵察套件市場報告