|

市場調查報告書

商品編碼

2066421

印度體外診斷市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India In-Vitro Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

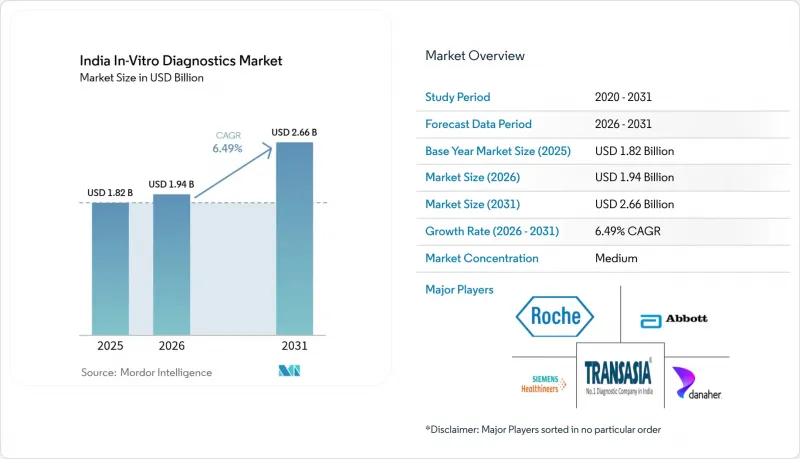

據 Mordor Intelligence 稱,印度體外診斷市場預計到 2026 年價值 19.4 億美元,高於 2025 年的 18.2 億美元,預計到 2031 年將達到 26.6 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.49%。

本報告按檢測類型(例如,臨床化學)、技術(例如,聚合酵素鏈鎖反應(PCR))、產品(例如,設備)、用途(例如,一次性體外診斷設備)、檢測地點(例如,中心檢查室)、檢體類型(例如,血液)、應用和最終用戶進行分類。市場預測以貨幣價值(美元)表示。

印度體外診斷市場趨勢及洞察。

傳染病和非傳染病的負擔日益加重,使得早期診斷至關重要。

結核病仍佔全球整體所有病例的27%,其中27%源自印度,促使人們從顯微鏡檢查轉向靈敏度更高、當天即可出結果的快速分子檢測。全國家庭健康調查數據顯示,女性貧血盛行率高達57%,五歲以下兒童貧血盛行率高達67%,推動了血液檢測的需求。同時,糖尿病盛行率的上升(目前影響著1.01億人)以及心血管疾病發生率的增加,也推動了臨床化學和免疫檢測分析檢測數量的成長。因此,實驗室正在擴展其檢測項目,在整合平台上提供血脂、糖化血紅蛋白(HbA1c)和心臟標記檢測,以及感染疾病檢測。在腫瘤學領域,無需進行侵入性切片檢查即可識別具有治療意義的突變的液態生物檢體的應用,正在加速精準診斷檢測的普及。這些情況清楚地表明,綜合診斷在印度體外診斷市場的發展中佔據核心地位。

醫療保險覆蓋範圍的擴大和可支配收入的增加正在減輕體檢的經濟負擔。

透過「總理人民健康計畫」(Pradhan Mantri Jan Arogya Yojana)等關鍵項目,印度的保險覆蓋率已從25%提升至51%。保險報銷檢測費用降低了患者的自付費用,並鼓勵他們選擇經認證的實驗室。檢測量的增加使實驗室能夠攤銷在高通量PCR、NGS和化學冷光平台上的投資,從而降低價格。這吸引了二線都市地區的中產階級。保險公司正在收緊品質標準,迫使小規模實驗室獲得NABL認證或與大型連鎖機構合作。因此,價格可承受性、品質和規模三者正在產生協同效應,進一步深化印度體外診斷市場的整體市場深度。

低溫運輸和物流基礎設施的缺乏限制了試劑向農村地區的配送。

五分之一的溫度敏感型醫療產品會因運輸和儲存場所無法維持2-8 度C的溫度劣化。像Phloton這樣的攜帶式電池驅動裝置可以將試劑在4-6 度C下保存10小時,但其應用仍處於早期階段。為了擴大農村地區的覆蓋範圍,目前正在廣泛部署太陽能製冷系統並測試隔熱被動包裝材料。低溫運輸的不足尤其阻礙了分子診斷和免疫檢測的應用,並減緩了農村地區對印度體外診斷市場的貢獻。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 感染疾病和非感染疾病的負擔日益加重,使得早期診斷至關重要。

- 醫療保險覆蓋範圍的擴大和可支配收入的增加,有助於減輕醫療檢查費用的負擔。

- 政府根據「國家衛生使命」對公共檢測設施基礎設施進行投資

- 高通量自動化和人工智慧在實驗室中的應用正在提高效率。

- 數位健康生態系統整合(實驗室資訊系統、遠端病理診斷)與擴大檢測機會

- 私營檢測機構的擴張推動了集中式檢測的發展。

- 市場限制因素

- 高昂的自付醫療費用導致人們對價格更加敏感。

- 依賴進口設備和原料而產生的外匯風險

- 低溫運輸和物流基礎設施的缺乏限制了試劑向農村地區的配送。

- 法規核准流程的碎片化延長了產品上市時間。

- 供應鏈分析

- 監理展望

- 波特五力模型

第5章 市場規模與成長預測

- 按測試類型

- 臨床化學

- 免疫診斷

- 血液學

- 分子診斷

- 凝血

- 微生物學

- 其他

- 透過技術

- 聚合酵素鏈鎖反應(PCR)

- 逆轉錄PCR(RT-PCR)

- 次世代定序

- 酵素免疫分析法(ELISA)

- 化學冷光

- 快速抗原檢測/側向層析法

- 依產品

- 設備/分析儀

- 試劑和試劑盒

- 軟體服務

- 透過可用性

- 免洗體外診斷設備

- 可重複使用的體外診斷設備

- 按測試地點

- 中心檢查室的檢測

- 即時檢測

- 檢體型

- 血

- 尿

- 唾液

- 其他體液

- 透過使用

- 感染疾病

- 糖尿病

- 癌症/腫瘤學

- 循環系統

- 自體免疫疾病

- 腎臟病學

- 其他

- 最終用戶

- 診斷檢查室

- 醫院和診所

- 居家照護和自我檢查

- 學術研究機構

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Abbott Laboratories

- F. Hoffmann-La Roche AG

- Siemens Healthineers

- Transasia Bio-Medicals Ltd

- Thermo Fisher Scientific

- Beckman Coulter, Inc.

- bioMerieux SA

- Danaher Corporation(Cepheid)

- Becton, Dickinson & Company

- Arkray, Inc.

- Bio-Rad Laboratories, Inc.

- Agappe Diagnostics

- Mylab Discovery Solutions

- J Mitra & Co. Pvt Ltd

- HLL Lifecare Ltd(Hindlabs)

- SRL Diagnostics(Fortis Healthcare)

- Dr. Lal PathLabs Ltd

- Metropolis Healthcare Ltd

- Molbio Diagnostics(Truenat)

- Seegene Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, india in-vitro diagnostics market size in 2026 is estimated at USD 1.94 billion, growing from 2025 value of USD 1.82 billion with 2031 projections showing USD 2.66 billion, growing at 6.49% CAGR over 2026-2031.

This report is Segmented by Test Type (Clinical Chemistry, and More), Technology (Polymerase Chain Reaction (PCR), and More), Product (Instruments, and More), Usability (Disposable IVD Devices, and More), Testing Site (Central Laboratory Testing, and More), Specimen Type (Blood, and More), Application, and End-User. The Market Forecasts are Provided in Terms of Value (USD).

India In-Vitro Diagnostics Market Trends and Insights

Rising Dual Burden of Communicable & Non-Communicable Diseases Necessitating Early Diagnostics

Tuberculosis still represents 27% of global cases traced to India, prompting a shift from microscopy to rapid molecular assays that offer higher sensitivity and same-day results. National Family Health Survey data show anemia prevalence of 57% among women and 67% among children under five, driving hematology test demand. Parallel growth of diabetes, now affecting 101 million citizens, and rising cardiovascular morbidity are pushing clinical chemistry and immunoassay volumes. Laboratories therefore broaden menus to run infectious disease panels alongside lipid, HbA1c, and cardiac marker testing on integrated platforms. Precision-oriented test adoption is accelerating in oncology as liquid biopsy assays identify actionable mutations without invasive biopsies, underlining why comprehensive diagnostics sit at the centre of India in-vitro diagnostics market development.

Expanding Health-Insurance Penetration & Disposable Incomes Enhancing Test Affordability

Insurance coverage has climbed from 25% to 51% of the population through flagship schemes such as Pradhan Mantri Jan Arogya Yojana. Reimbursement of laboratory procedures is lowering out-of-pocket spending and steering patients toward accredited sites. Growing volumes help labs amortise investments in high-throughput PCR, NGS, and chemiluminescence platforms, enabling price cuts that lure middle-income segments in tier-2 urban belts. Insurers are tightening quality criteria, compelling smaller centres to secure NABL accreditation or partner with organised chains. The resulting virtuous cycle of affordability, quality, and scale improves market depth across the India in-vitro diagnostics market.

Limited Cold-Chain & Logistics Infrastructure Restricting Rural Reagent Distribution

One-fifth of temperature-sensitive health products degrade because trucks and storage points cannot sustain 2-8°C. Portable battery-powered units like Phloton hold reagents at 4-6°C for 10 hours, but deployment is nascent. Widespread solar refrigeration roll-outs and passive insulated packaging are being tested to widen rural reach. Cold-chain gaps particularly hinder molecular and immunoassay expansion, slowing rural contribution to the India in-vitro diagnostics market.

Other drivers and restraints analyzed in the detailed report include:

- Government Investments in Public Laboratory Infrastructure under National Health Mission

- Adoption of High-Throughput Automation & AI in Laboratories Elevating Efficiency

- Fragmented Regulatory Approval Pathway Increasing Time-to-Market

For complete list of drivers and restraints, kindly check the Table Of Contents.

List of Companies Covered in this Report:

- Abbott Laboratories

- Roche

- Siemens Healthineers

- Transasia Bio-Medicals

- Thermo Fisher Scientific

- Beckton Dickinson

- bioMerieux

- Danaher

- Beckton Dickinson

- Arkray

- Bio-Rad Laboratories

- Agappe Diagnostics

- Mylab Discovery Solutions

- J Mitra & Co. Pvt Ltd

- HLL Lifecare Ltd (Hindlabs)

- SRL Diagnostics (Fortis Healthcare)

- Dr. Lal PathLabs Ltd

- Metropolis Healthcare Ltd

- Molbio Diagnostics (Truenat)

- Seegene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Dual Burden of Communicable & Non-Communicable Diseases Necessitating Early Diagnostics

- 4.2.2 Expanding Health-Insurance Penetration & Disposable Incomes Enhancing Test Affordability

- 4.2.3 Government Investments in Public Laboratory Infrastructure under National Health Mission

- 4.2.4 Adoption of High-Throughput Automation & AI in Laboratories Elevating Efficiency

- 4.2.5 Integration of Digital Health Ecosystems (LIS, Telepathology) Broadening Access to Testing

- 4.2.6 Expansion of Private Lab Chains Driving Centralized Testing

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Healthcare Spending Creating Price Sensitivity

- 4.3.2 Dependence on Imported Instruments & Raw Materials Exposing Currency Risk

- 4.3.3 Limited Cold-Chain & Logistics Infrastructure Restricting Rural Reagent Distribution

- 4.3.4 Fragmented Regulatory Approval Pathway Increasing Time-to-Market

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Immuno-Diagnostics

- 5.1.3 Haematology

- 5.1.4 Molecular Diagnostics

- 5.1.5 Coagulation

- 5.1.6 Microbiology

- 5.1.7 Others

- 5.2 By Technology

- 5.2.1 Polymerase Chain Reaction (PCR)

- 5.2.2 Reverse Transcription PCR (RT-PCR)

- 5.2.3 Next-Generation Sequencing

- 5.2.4 Enzyme-Linked Immunosorbent Assay (ELISA)

- 5.2.5 Chemiluminescence

- 5.2.6 Rapid Antigen / Lateral Flow

- 5.3 By Product

- 5.3.1 Instruments / Analysers

- 5.3.2 Reagents & Kits

- 5.3.3 Software & Services

- 5.4 By Usability

- 5.4.1 Disposable IVD Devices

- 5.4.2 Re-usable IVD Devices

- 5.5 By Testing Site

- 5.5.1 Central Laboratory Testing

- 5.5.2 Point-of-Care Testing

- 5.6 By Specimen Type

- 5.6.1 Blood

- 5.6.2 Urine

- 5.6.3 Saliva

- 5.6.4 Other Body Fluids

- 5.7 By Application

- 5.7.1 Infectious Disease

- 5.7.2 Diabetes

- 5.7.3 Cancer / Oncology

- 5.7.4 Cardiology

- 5.7.5 Auto-immune Disorders

- 5.7.6 Nephrology

- 5.7.7 Others

- 5.8 By End-user

- 5.8.1 Diagnostic Laboratories

- 5.8.2 Hospitals & Clinics

- 5.8.3 Home-care & Self-testing

- 5.8.4 Academic & Research Institutes

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche AG

- 6.3.3 Siemens Healthineers

- 6.3.4 Transasia Bio-Medicals Ltd

- 6.3.5 Thermo Fisher Scientific

- 6.3.6 Beckman Coulter, Inc.

- 6.3.7 bioMerieux SA

- 6.3.8 Danaher Corporation (Cepheid)

- 6.3.9 Becton, Dickinson & Company

- 6.3.10 Arkray, Inc.

- 6.3.11 Bio-Rad Laboratories, Inc.

- 6.3.12 Agappe Diagnostics

- 6.3.13 Mylab Discovery Solutions

- 6.3.14 J Mitra & Co. Pvt Ltd

- 6.3.15 HLL Lifecare Ltd (Hindlabs)

- 6.3.16 SRL Diagnostics (Fortis Healthcare)

- 6.3.17 Dr. Lal PathLabs Ltd

- 6.3.18 Metropolis Healthcare Ltd

- 6.3.19 Molbio Diagnostics (Truenat)

- 6.3.20 Seegene Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

電力線通訊和物聯網賦能的電網監測市場預測至2034年—按組件、技術、應用、最終用戶和區域分類的全球分析

電力線通訊和物聯網賦能的電網監測市場預測至2034年—按組件、技術、應用、最終用戶和區域分類的全球分析 全球照護現場測試市場(第13版)

全球照護現場測試市場(第13版) 2026-2030年全球體外診斷契約製造市場

2026-2030年全球體外診斷契約製造市場 體外診斷(IVD)膜材料市場:依產品類型、應用、最終用途、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

體外診斷(IVD)膜材料市場:依產品類型、應用、最終用途、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 2026年全球適體診斷試劑盒市場報告2026年全球體外診斷(IVD)實驗室耗材市場報告

2026年全球適體診斷試劑盒市場報告2026年全球體外診斷(IVD)實驗室耗材市場報告 體外診斷市場規模、佔有率和成長分析:按產品/服務、技術、應用、檢測地點、最終用戶、檢體和地區分類-2026-2033年產業預測高成長免疫學測量測試:趨勢、技術和市場機會(2026 年)

體外診斷市場規模、佔有率和成長分析:按產品/服務、技術、應用、檢測地點、最終用戶、檢體和地區分類-2026-2033年產業預測高成長免疫學測量測試:趨勢、技術和市場機會(2026 年) 智慧體外診斷市場:人工智慧在體外診斷中的應用—按應用、技術、產品和使用者分類—高階主管和顧問指南(2026-2030 年)體外診斷(IVD)品管市場:策略與趨勢,包括按檢測類型、施行地點、產品、製造商和國家/地區分類的預測 -經營團隊和諮詢顧問的市場分析(2026-2030 年)

智慧體外診斷市場:人工智慧在體外診斷中的應用—按應用、技術、產品和使用者分類—高階主管和顧問指南(2026-2030 年)體外診斷(IVD)品管市場:策略與趨勢,包括按檢測類型、施行地點、產品、製造商和國家/地區分類的預測 -經營團隊和諮詢顧問的市場分析(2026-2030 年)