|

市場調查報告書

商品編碼

2066420

遠端醫療:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Telemedicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

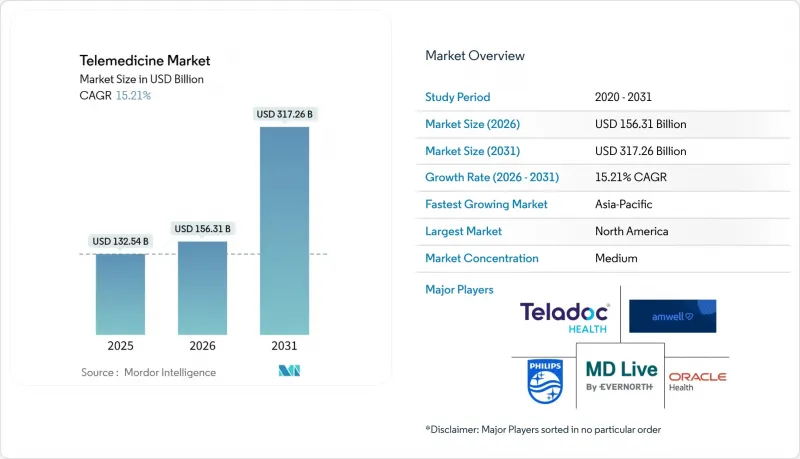

根據 Mordor Intelligence 預測,遠端醫療市場規模預計將在 2025 年達到 1,325.4 億美元,2026 年達到 1,563.1 億美元,2031 年達到 3,172.6 億美元,2026 年至 2031 年的複合年成長率為 15.21%。

本報告按交付方式(同步、非同步、遠端患者監護)、組件(軟體平台、硬體及周邊設備、服務)、最終用戶(醫療服務提供者、保險公司和雇主、患者/家庭用戶、政府機構和非政府組織)以及地區(北美、歐洲、亞太、中東和非洲、南美)進行細分。市場預測以美元計價。

全球遠端醫療市場趨勢及洞察

慢性病負擔迅速加重和人口老化。

根據世界衛生組織 (WHO) 的估計,到 2050 年,全球 65 歲及以上人口將超過 15 億,其中超過 60% 的人至少患有一種慢性疾病。遠端醫療透過實現遠距後續觀察和生命徵象的持續監測,減少了老年人的行動障礙。因此,早期介入成為可能,使美國聯邦醫療保險優勢計劃 (Medicare Advantage)用戶的再入院率降低了 22%。在高所得國家,約 75% 的醫療保健支出用於治療慢性疾病,保險公司高度重視這些成果。人口壓力和基於價值的資金模式正在推動遠端醫療市場解決方案成為標準的醫療保健工作流程。這些結構性因素將在未來幾十年持續發展,確保無論經濟週期如何波動,市場需求將保持強勁。

在經合組織和金磚國家地區,保險公司對遠距醫療報銷率的統一化正在擴大。

2025年底,美國已有43個州強制規定私人保險公司對遠距醫療提供同等報銷,另有24個州將同等報銷範圍擴大到醫療補助計劃(Medicaid)受益人。法國、德國、印度和巴西也已實施類似框架,有效消除了先前限制遠距醫療僅限於富裕患者的經濟障礙。與面對面諮詢同等收費系統的建立,增強了醫療服務提供者對其收入永續性的信心,同時,對價格敏感的患者也受益於自付費用的降低。這項監管轉變鞏固了遠端醫療作為健保服務的地位,並在多個用戶群體中建立了可預測的使用模式。

資料隱私和跨境許可法規仍然分散。

歐盟的《一般資料保護規則》(GDPR)限制了跨國資料流動,2024年至2025年的執法措施導致在歐盟境外儲存病患記錄的企業被處以1.2億歐元的罰款。在美國,截至2025年底,只有40個州加入了州際醫療執照互認協議(Interstate Medical Licensure Compact),迫使醫生獲得多個執照,每個執照在每個司法管轄區的費用都超過1000美元。印度目前正在審議的《數位個人資料保護法》強制要求資料儲存在國內,這增加了跨國平台的基礎設施成本。這些不一致之處加重了合規負擔,並阻礙了遠端醫療市場的跨區域擴充性。

細分市場分析

隨著美國FDA相繼批准可連接血糖值、心率和血壓感測器,並將連續數據傳輸至雲端分析引擎,遠端患者監護的需求正迅速成長,預計到2031年將以17.09%的複合年成長率成長。同步影片在2025年仍佔據最大的銷售佔有率,達到44.28%,尤其適用於需要即時互動的基層醫療、急診護理和行為醫學診療。同時,包括存轉成像和安全通訊在內的非同步工作流程約佔總支出的25%。到2025年底,Medicare Advantage的遠距病患監護計畫已涵蓋3,200萬用戶,並將30天內再入院率降低了22%,凸顯了保險公司對持續照護模式的高度關注。

同步服務的使用率已從疫情高峰迴落,並穩定在門診就診量的四分之一左右,但仍遠高於新冠疫情前的水平。非同步服務具有頻寬需求低、預約時間柔軟性等優勢,但與面對面諮詢相比,其報銷率往往較低。人工智慧分診技術的引入,例如優先處理皮膚影像或檢測心臟異常,有望加速頻寬受限地區非同步服務的普及。總體而言,遠距患者管理(RPM)的「始終在線」資料模型有望重塑慢性病診療的經濟模式,並可能在未來十年內為遠端醫療市場帶來最大的收入成長。

區域分析

北美地區憑藉著完善的報銷政策、較高的寬頻普及率以及企業積極採用數位醫療技術,預計到2025年將佔全球收入的38.06%。同時,亞太地區在政府主導的數位舉措的推動下,預計到2031年將以19.59%的複合年成長率成為該地區成長最快的地區。印度的「eSanjeevani」預計到2025年中期將完成第3億次諮詢,而中國的省級人工智慧平台將覆蓋超過4億農村居民。

在歐洲,法國對慢性病視訊後續觀察提供全額報銷,德國的DiGA計畫推薦符合保險報銷條件的健康應用程式,英國則將線上諮詢整合到整個NHS(英國國家醫療服務體系)基層醫療流程中。儘管有監管方面的結構性支持,但電子健康記錄(EHR)基礎設施的碎片化和語言差異阻礙了其在歐洲的擴充性,導致其普及速度慢於亞太地區。

儘管海灣國家的購物中心和公共設施正在安裝支援5G功能的自助服務終端,但南非的私人保險公司直到最近才開始為遠距精神病學提供資金。拉丁美洲約佔全球整體收入的4%,其中巴西的遠距心理健康服務範圍正在擴大,阿根廷正在實施一項針對農村地區的遠距監測試點計畫。該地區的成長軌跡與寬頻普及率和政府報銷意願密切相關,這證實了遠端醫療市場的發展取決於政策和基礎設施建設的相互作用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 慢性病盛行率快速上升和人口老化。

- 經合組織和金磚國家地區付款方擴大等額還款法律的適用範圍

- 5G 和邊緣運算的引入使得低延遲視訊會診成為可能。

- 雇主提供的虛擬初級保健計劃正在迅速擴展。

- 受疫情影響,消費者對線上醫療諮詢的偏好將在後疫情時代持續存在。

- 透過整合人工智慧驅動的決策支援來提高臨床接受度

- 市場限制因素

- 資料隱私和跨境許可法規仍然分散。

- 關於從 2026 年起削減聯邦醫療保險醫生薪酬的擬議規則。

- 數位鴻溝阻礙了低收入國家向農村地區引入患者。

- 由於電子病歷和遠端醫療。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按模式

- 同步

- 非同步

- 遠端患者監護

- 按組件

- 軟體平台

- 硬體和周邊設備

- 服務

- 遠距病理診斷

- 遠端心臟診斷

- 遠端放射診斷

- 遠距皮膚病學

- 遠距精神科護理

- 遠距中風醫療

- 其他服務

- 最終用戶

- 醫療服務提供方

- 付款人和雇主

- 患者/家庭用戶

- 政府機構和非政府組織

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Allscripts Healthcare Solutions Inc.

- Amwell(American Well)

- Babylon Health

- Cerner/Oracle Health

- Cisco Systems

- Doctor On Demand

- eClinicalWorks

- Epic Systems

- GE Healthcare

- Honeywell International Inc.

- Koninklijke Philips NV

- MDLive(Cigna)

- Medtronic

- PlushCare

- Practo Technologies Pvt. Ltd.

- Resideo Technologies Inc.

- SHL Telemedicine Ltd.

- Siemens Healthineers

- Teladoc Health Inc.

- Zoom Video Communications

第7章 市場機會與未來展望

According to Mordor Intelligence, the telemedicine market size is projected to be USD 132.54 billion in 2025, USD 156.31 billion in 2026, and reach USD 317.26 billion by 2031, growing at a CAGR of 15.21% from 2026 to 2031.

This report is Segmented by Modality (Synchronous, Asynchronous, Remote Patient Monitoring), Component (Software Platforms, Hardware & Peripherals, Services), End User (Healthcare Providers, Payers & Employers, Patients / Home Users, Government Agencies & NGOs), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Telemedicine Market Trends and Insights

Surging Chronic-Disease Burden And Aging Population

Estimates from the World Health Organization show that the global population aged 65 and older will surpass 1.5 billion by 2050, with more than 60% living with at least one chronic condition. Telehealth lowers mobility-related barriers for seniors by enabling remote follow-ups and continuous monitoring of vitals, resulting in earlier interventions that reduce hospital readmissions by 22% among Medicare Advantage enrollees in the United States. Payers favor these outcomes because chronic-disease care accounts for approximately 75% of health expenditures in high-income countries. The alignment of demographic pressure and value-based funding embeds telemedicine market solutions into baseline care workflows. Because these structural forces evolve over decades, demand remains resilient regardless of economic cycles.

Payer Reimbursement Parity Laws Expanding In OECD And BRICS Regions

By the end of 2025, 43 U.S. states mandated private-payer parity for virtual visits, and 24 states extended equivalent payments to Medicaid beneficiaries. Similar frameworks were introduced in France, Germany, India, and Brazil, effectively removing the financial barrier that had previously limited adoption to affluent patients. With tariffs aligned to in-person care, provider groups are confident about revenue continuity, while patients in price-sensitive segments enjoy lower out-of-pocket costs. This regulatory shift normalizes telehealth as a covered benefit, underpinning predictable utilization patterns across multiple insurance cohorts.

Data-Privacy And Cross-Border Licensure Regulations Remain Fragmented

The European Union's GDPR restricts cross-border data flows, and enforcement actions between 2024-2025 levied EUR 120 million in penalties on operators that stored patient records outside the bloc. In the United States, only 40 states had joined the Interstate Medical Licensure Compact by late 2025, leaving physicians to secure multiple licenses at fees surpassing USD 1,000 per jurisdiction. India's pending Digital Personal Data Protection Act requires domestic data residency, which increases infrastructure costs for multinational platforms. These inconsistencies elevate compliance overhead and compress the telemedicine market's cross-regional scalability.

Other drivers and restraints analyzed in the detailed report include:

- 5G And Edge-Computing Roll-Outs Enabling Low-Latency Video Consultations

- Employer-Sponsored Virtual Primary-Care Plans Scaling Rapidly

- Physician Reimbursement Cuts In Medicare Draft Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Remote patient monitoring captured accelerating interest, notching a 17.09% CAGR forecast through 2031 as the U.S. FDA cleared successive waves of connected glucose, cardiac, and blood-pressure sensors that stream continuous data to cloud analytics engines. Synchronous video maintained the largest 2025 revenue share at 44.28%, particularly suited for primary-care, urgent-care, and behavioral-health sessions that require real-time interaction. Asynchronous workflows, including store-and-forward imaging and secure messaging, accounted for approximately 25% of spending. Medicare Advantage enrolled 32 million members in RPM programs by the end of 2025, reducing 30-day readmissions by 22% and confirming payer appetite for continuous-care models.

Synchronous utilization is stabilizing at one-quarter of outpatient encounters, down from pandemic highs, yet remains far above pre-COVID levels. Asynchronous modalities benefit from lower bandwidth demands and flexible scheduling, although payment rates tend to lag behind those for live visits. The incorporation of AI triage that prioritizes dermatology images or flags cardiac anomalies is expected to lift asynchronous adoption in bandwidth-constrained regions. Overall, RPM's always-on data model positions it to redefine chronic-care economics, securing the largest incremental share of telemedicine market revenue over the next decade.

Geography Analysis

North America contributed 38.06% of global revenue in 2025, driven by well-established reimbursement policies, high broadband penetration, and robust employer adoption. The Asia-Pacific region, however, is projected to deliver the fastest regional CAGR of 19.59% through 2031, driven by government-backed digital health initiatives. India's eSanjeevani recorded its 300 millionth consultation by mid-2025, while China's AI-enhanced provincial platforms cover more than 400 million rural residents.

In Europe, France reimburses 100% of chronic-care video follow-ups, Germany's DiGA program prescribes reimbursable health apps, and the United Kingdom has embedded virtual consults across National Health Service primary-care pathways. Despite structural regulatory support, fragmented EHR infrastructures and language diversity temper pan-European scalability, slowing the uptake compared with the Asia-Pacific region.

Gulf states are installing 5G kiosks in malls and public offices, whereas South Africa's private payers only recently began funding telepsychiatry. Latin America accounted for approximately 4% of global revenue, with Brazil expanding virtual mental health coverage and Argentina running rural remote monitoring pilots. Regional growth trajectories correlate strongly with broadband availability and government willingness to reimburse, confirming the telemedicine market's dependence on synchronized policy and infrastructure advances.

- Allscripts

- Amwell (American Well)

- Babylon Health

- Cerner / Oracle Health

- Cisco Systems

- Doctor On Demand

- eClinicalWorks

- Epic Systems

- GE Healthcare

- Honeywell International

- Koninklijke Philips

- MDLive (Cigna)

- Medtronic

- PlushCare

- Practo Technologies Pvt. Ltd.

- Resideo Technologies

- SHL Telemedicine Ltd.

- Siemens Healthineers

- Teladoc Health

- Zoom Video Communications

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Chronic Disease Prevalence and Ageing Population

- 4.2.2 Payer Reimbursement Parity Laws Expanding in OECD & BRICS Regions

- 4.2.3 5G And Edge-Computing Roll-Outs Enabling Low-Latency Video Consultations

- 4.2.4 Employer-Sponsored Virtual Primary-Care Plans Scaling Rapidly

- 4.2.5 Pandemic-Driven Consumer Preference for Virtual Visits Sustaining Post-COVID

- 4.2.6 Integration of AI-Based Decision-Support Improving Clinical Acceptance

- 4.3 Market Restraints

- 4.3.1 Data-Privacy & Cross-Border Licensure Regulations Remain Fragmented

- 4.3.2 Physician Reimbursement Cuts in Medicare 2026+ Draft Rules

- 4.3.3 Digital-Divide Limiting Rural Patient Adoption in Low-Income Economies

- 4.3.4 Platform Fatigue Among Clinicians Due To EHR-Telehealth Integration Gaps

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Modality

- 5.1.1 Synchronous

- 5.1.2 Asynchronous

- 5.1.3 Remote Patient Monitoring

- 5.2 By Component

- 5.2.1 Software Platforms

- 5.2.2 Hardware & Peripherals

- 5.2.3 Services

- 5.2.3.1 Telepathology

- 5.2.3.2 Telecardiology

- 5.2.3.3 Teleradiology

- 5.2.3.4 Teledermatology

- 5.2.3.5 Telepsychiatry

- 5.2.3.6 Telestroke

- 5.2.3.7 Other Services

- 5.3 By End User

- 5.3.1 Healthcare Providers

- 5.3.2 Payers & Employers

- 5.3.3 Patients / Home Users

- 5.3.4 Government Agencies & NGOs

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Allscripts Healthcare Solutions Inc.

- 6.3.2 Amwell (American Well)

- 6.3.3 Babylon Health

- 6.3.4 Cerner / Oracle Health

- 6.3.5 Cisco Systems

- 6.3.6 Doctor On Demand

- 6.3.7 eClinicalWorks

- 6.3.8 Epic Systems

- 6.3.9 GE Healthcare

- 6.3.10 Honeywell International Inc.

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 MDLive (Cigna)

- 6.3.13 Medtronic

- 6.3.14 PlushCare

- 6.3.15 Practo Technologies Pvt. Ltd.

- 6.3.16 Resideo Technologies Inc.

- 6.3.17 SHL Telemedicine Ltd.

- 6.3.18 Siemens Healthineers

- 6.3.19 Teladoc Health Inc.

- 6.3.20 Zoom Video Communications

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

遠距照護市場-2026-2032年全球市場預測遠端醫療市場:按組件、技術、收入模式、應用、專科、最終用戶、部署模式和病患年齡分類-2026-2032年全球市場預測

遠距照護市場-2026-2032年全球市場預測遠端醫療市場:按組件、技術、收入模式、應用、專科、最終用戶、部署模式和病患年齡分類-2026-2032年全球市場預測 2026年全球庇護醫療保健服務市場報告

2026年全球庇護醫療保健服務市場報告 遠距照護市場規模、佔有率和成長分析:按技術、交付方式、部署方式、應用、最終用戶和地區分類-2026-2033年產業預測

遠距照護市場規模、佔有率和成長分析:按技術、交付方式、部署方式、應用、最終用戶和地區分類-2026-2033年產業預測 全球遠端醫療設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球虛擬睡眠診所市場報告

全球遠端醫療設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球虛擬睡眠診所市場報告 視訊遠端醫療市場預測—全球產品、組件、通訊方式、應用、最終用戶和地區分析—2034年

視訊遠端醫療市場預測—全球產品、組件、通訊方式、應用、最終用戶和地區分析—2034年 遠端醫療市場規模、佔有率和成長分析:按服務類型、最終用戶、技術、應用和地區分類-2026-2033年產業預測遠端醫療市場預測至2034年-全球分析(按組成部分、模式、交付方式、類型、應用、最終用戶和地區分類)

遠端醫療市場規模、佔有率和成長分析:按服務類型、最終用戶、技術、應用和地區分類-2026-2033年產業預測遠端醫療市場預測至2034年-全球分析(按組成部分、模式、交付方式、類型、應用、最終用戶和地區分類) 遠端醫療市場:按服務、應用、最終用戶和地區分類(2026-2034 年)

遠端醫療市場:按服務、應用、最終用戶和地區分類(2026-2034 年)