|

市場調查報告書

商品編碼

2066417

海上鑽井鑽機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Offshore Drilling Rigs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

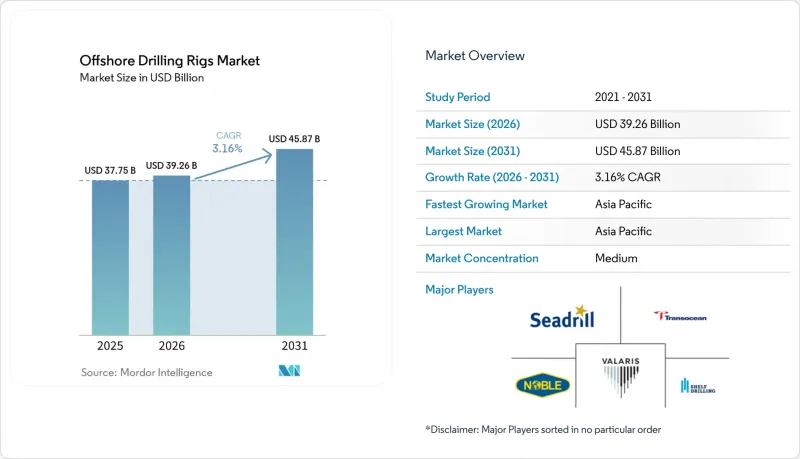

根據 Mordor Intelligence 預測,海上鑽井鑽機市場規模將從 2025 年的 377.5 億美元成長到 2026 年的 392.6 億美元,然後在 2031 年達到 458.7 億美元,2026 年至 2031 年的複合年成長率為 3.16%。

本報告按鑽機類型(自升式鑽井平台、半潛式鑽井平台、鑽井船及其他類型)、水深(淺海、深海和超深海)以及地區(北美、歐洲、亞太、南美以及中東和非洲)進行細分。市場規模和預測均以美元計價。

全球海上鑽井鑽機市場趨勢及洞察

全球能源需求成長

預計到2030年,石油和天然氣在全球能源結構中的總合將維持在52%,這將為海上鑽井作業創造永續的基本負載需求。阿布達比國家石油公司(ADNOC)鑽井部門計畫在2028年將其鑽機平台數量擴大到125座,以幫助阿拉伯聯合大公國實現日產500萬桶的產能,充分體現了這家國有石油公司在支撐需求方面所扮演的角色。印度石油天然氣公司(ONGC)已延長其在克里希納-戈達瓦里河谷的自升式鑽井鑽機的租約,以維持老舊油井的生產,這凸顯了淺水鑽探在能源需求旺盛的新興經濟體中的重要性。巴西石油公司(Petrobras)已為鹽鹽層下作業租用了12艘鑽井船,顯示這家國有企業能夠不受價格週期波動的影響,維持鑽井活動。這種兩極化,以經合組織國家效率提高和非經合組織國家擴張為特徵,造成了層級構造需求模式:自升式鑽機滿足了亞洲不斷成長的生產需求,而高階浮體式鑽機則追蹤著前沿深海油田的原油產量。

未開發海洋蘊藏量的探勘

奈米比亞的橘子盆地估計蘊藏量100億桶可採資源,道達爾能源和殼牌計劃在2024年至2025年間共部署四艘鑽井船。圭亞那的斯塔布布魯克區塊已探明蘊藏量超過110億桶,需要持續營運六艘鑽井船才能維持日產量超過64萬桶的成長。這些成功案例降低了人們對風險的認知,而更高的成功機率也使得超過1億美元的單井成本合理。安哥拉耗資60億美元的卡米尼奧計畫將在四年內部署兩艘鑽井船,這凸顯了即使盈虧平衡點約為每桶35美元,人們仍然願意投資於前沿深海開發。因此,能夠應對10000英尺水深和20000磅/平方英寸高壓高溫(HPHT)作業的先進鑽井船正在推動海上鑽井鑽機市場的成長。

加強環境問題和ESG監管

自2025年起,歐盟排放交易體系(ETS)將適用於海上船舶,這意味著未採用排放技術的鑽機每年將增加高達1,000萬美元的碳排放成本。美國環保署(EPA)也收緊了鑽井液的排放標準,導致資本投資增加15%至20%。這些法規迫使Transocean公司將三座老舊的半潛式鑽機運作,因為升級改造已不再具有經濟效益。隨著營運商將環境、社會和治理(ESG)指標納入採購流程,配備混合動力裝置和即時排放監測系統的承包商在競標中獲得了優勢。挪威石油安全局已引入連續甲烷監測要求,進一步提高了北海鑽井鑽機的合規要求。

細分市場分析

2025年,自升式鑽井鑽機佔據了海上鑽井鑽機43.9%的市場佔有率,這主要得益於波斯灣、東南亞和墨西哥灣的高運轉率。相較之下,鑽井船預計到2031年將以7.2%的複合年成長率成長,屆時該細分市場的規模預計將達到180億美元。能夠處理20,000 psi高壓高溫井的高階鑽機鑽機收入可達50萬美元。例如,Transocean公司的「深水阿特拉斯號」鑽井平台於2025年與Equinor公司簽訂了為期三年的合約。同樣在2025年,半潛式鑽井鑽機在中等深度水域的作業中主導地位,運轉率78%。其中許多平台被用於西非和北海遠海區域的評估工作。隨著舊舊鑽機不斷退役,需求集中在高規格資產上,這使得正在對其車隊進行現代化改造的承包商擁有更大的定價權。

海上鑽井鑽機市場的趨勢凸顯了船隊的標準化和數位化。三星重工在2024年至2025年間交付了兩艘新的鑽井船,並立即投入巴西石油公司(Petrobras)的鹽層下下層開發案。這顯示高階浮體式鑽井鑽機市場擴張空間有限。同時,東南亞自升式鑽井鑽機的供應過剩迫使博爾鑽井公司(Bol Drilling)在2025年將其四座鑽井平台重新部署到中東,並尋求比泰國高出25%的租金。 2025年底,全球自升式鑽井鑽機的運轉率為82%,而浮體式鑽井鑽機的利用率則高達91%,證實了淺水設施吸收新增需求的速度慢於深海域。

區域分析

亞太地區(主要得益於泰國、越南和印度)預計在2025年將佔全球銷售額的37.6%,並將繼續保持成長最快的地區地位,預計到2031年將以4.1%的複合年成長率成長。 2025年,泰國國家石油公司(PTTEP)簽署了三份自升式鑽機契約,以延長其在泰國灣的運作。同時,越南石油集團(PetroVietnam)繼續在北河(Bac Ho)和九龍(Khu Long)運作五座鑽機,以彌補海事限制導致前沿探勘緩慢的影響。印度石油天然氣公司(ONGC)延長了多座自升式鑽機的契約,以降低對進口的依賴,支持政府到2030年實現國內日產量100萬桶的目標。中國海洋天然氣田部署了六個浮體式鑽井平台,以滿足粵港澳大灣區的工業需求。同時,伍德賽德能源公司(Woodside)正在推進斯卡伯勒氣田的泰巴克(Tybak)項目,該項目預計將在2026年做出最終投資決定(FID)。

在北美,不同地區的趨勢各不相同。在美國墨西哥灣,重點是海底回接項目,鑽機需求保持平穩,而墨西哥國家石油公司(Pemex)則獲得了2024-2025年的三份自升式鑽機契約,以將日產量穩定在180萬桶。在南美,巴西和圭亞那繼續發揮主導作用。巴西石油公司(Petrobras)營運12艘鑽井船,以維持日產量超過300萬桶;而在圭亞那的斯塔布布魯克區塊,六座浮體式鑽井平台正在開發和探勘井上運作。特立尼達的淺海天然氣井為大西洋液化天然氣(LNG)加工提供支持,並維持了適中的自升式鑽井平台運轉率。

在歐洲,活動主要集中在挪威,Equinor公司在Johan Sverdrup油田實施了數位雙胞胎,將非生產時間減少了15%。在英國大陸棚,退役工作成為優先事項,四座自升式鑽機正在進行油井關閉作業。在中東,淺水區活動依然活躍。 ADNOC Drilling公司的125座鑽機計畫支持日產500萬桶的產量目標;卡達的North Field East天然氣田擴建計畫預計到2025年需要六座自升式鑽機;沙烏地阿美公司的鑽機數量則根據歐佩克+的產量上限而波動。在非洲超深水區,以奈米比亞和安哥拉為首,活動激增。道達爾能源公司的Kaminho油田開發案和奈及利亞的Bonga Southwest評估計畫鞏固了非洲大陸長期的鑽機需求前景。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球能源需求成長

- 未開發海洋蘊藏量的探勘

- 在南美洲和非洲的深海和超深海中,探勘發現不斷增加。

- 計劃退役的未完成項目推動了對鑽井鑽機再利用的需求。

- 海洋二氧化碳儲存和地熱鑽探的興起

- 利用浮式液化天然氣開發中的孤立氣體的潛力

- 市場限制因素

- 加強環境問題和ESG監管

- 原油價格波動會影響資本投資週期。

- 海底回接作業正在減少新探勘井的需求。

- 超深海設備供應鏈瓶頸

- 供應鏈分析

- 以往的日薪趨勢(浮體式和自升式平台)

- 大型海上上游專案管道

- 監管狀況(環境與安全)

- 技術趨勢(鑽機自動化、遠端控制、數位雙胞胎)

- 波特五力模型

第5章 市場規模與成長預測

- 按鑽機類型

- 自升式鑽井鑽機

- 半潛式平台

- 鑽井船

- 其他類型(輔助船、駁船、改裝型海上鑽井平台)

- 按水深

- 淺水區(小於400英尺)

- 深海(400-5000英尺)

- 超深海(超過5000英尺)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 挪威

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 泰國

- 越南

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 千里達及托巴哥

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 奈及利亞

- 安哥拉

- 奈米比亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Keppel Corp

- Seatrium Ltd(Sembcorp Marine)

- Samsung Heavy Industries

- Hyundai Heavy Industries

- DSME

- China Merchants HI

- CIMC Raffles

- Friede & Goldman

- Damen Shipyards

- Irving Shipbuilding

- Transocean

- Valaris

- Seadrill

- Noble

- Shelf Drilling

- Borr Drilling

- Diamond Offshore

- Stena Drilling

- COSL

- KCA Deutag

第7章 市場機會與未來展望

According to Mordor Intelligence, the offshore drilling rigs market size is expected to grow from USD 37.75 billion in 2025 to USD 39.26 billion in 2026 and is forecast to reach USD 45.87 billion by 2031 at 3.16% CAGR over 2026-2031.

This report is Segmented by Rig Type (Jack-Ups, Semi-Submersibles, Drillships, and Other Rig Types), Water Depth (Shallow Water, Deepwater, and Ultra-Deepwater), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Offshore Drilling Rigs Market Trends and Insights

Increasing Global Energy Demand

Oil and gas are expected to retain a combined 52% share of the global energy mix through 2030, creating a durable baseload for offshore drilling campaigns. ADNOC Drilling plans to grow its fleet to 125 rigs by 2028 to help the UAE hit 5 million bpd production capacity, illustrating how national oil companies backstop demand. India's ONGC is extending jack-up charters in the Krishna-Godavari basin to preserve output from aging wells, reinforcing the shallow-water importance in energy-hungry emerging economies. Petrobras secured 12 drillships for pre-salt operations, signaling that state-backed operators can sustain drilling through price cycles. This bifurcation, OECD efficiency versus non-OECD expansion, results in a two-tier demand pattern where jack-ups cater to incremental volumes in Asia while premium floaters chase frontier deepwater barrels.

Exploration of Untapped Offshore Reserves

Namibia's Orange Basin holds an estimated 10 billion barrels of recoverable resources, with TotalEnergies and Shell collectively deploying four drillships during 2024-2025. Guyana's Stabroek block surpassed 11 billion barrels discovered, requiring a continuous fleet of six drillships to sustain its ramp-up past 640,000 bpd. These successes are lowering perceived risk and supporting well costs above USD 100 million when success probabilities rise. Angola's USD 6 billion Kaminho project will use two drillships over four years, highlighting the willingness to fund frontier deepwater when breakevens sit near USD 35 per barrel. Modern drillships capable of 10,000-foot water depths and 20,000-psi HPHT ratings thus form the growth engine of the offshore drilling rigs market.

Environmental Concerns & Stricter ESG Regulation

From 2025, the EU's Emissions Trading System extends to offshore vessels, adding up to USD 10 million per year in carbon costs for rigs lacking abatement technology. The U.S. EPA also tightened drilling-fluid discharge norms, increasing equipment spend by 15-20%. These mandates prompted Transocean to cold-stack three legacy semi-subs that were uneconomical to upgrade. Contractors with hybrid power packs and real-time emissions monitoring now enjoy bidding advantages as operators integrate ESG metrics into sourcing. Norway's Petroleum Safety Authority has introduced continuous methane monitoring requirements, adding further compliance layers for North Sea rigs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Deep- & Ultra-Deepwater Discoveries in South America & Africa

- Decommissioning Backlog Driving Rig-Repurposing Demand

- Crude-Oil Price Volatility Impacting CAPEX Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Jack-ups controlled 43.9% of the offshore drilling rigs market share in 2025, supported by high utilization in the Persian Gulf, Southeast Asia, and the Gulf of Mexico. In contrast, drillships are forecast to post a 7.2% CAGR through 2031, pushing the offshore drilling rigs market size for this segment to an expected USD 18 billion by the end-year window. Premium units fetch USD 500,000 per day when equipped for 20,000-psi HPHT wells, such as Transocean's Deepwater Atlas, which began a three-year Equinor contract in 2025. Semi-submersibles filled mid-water campaigns with 78% utilization in 2025, largely for appraisal work in West Africa and the Far North Sea. The continuing retirement of vintage rigs concentrates demand on high-specification assets, promoting stronger pricing power for contractors that modernize their fleets.

The offshore drilling rigs market trajectory underscores a pivot toward fleet standardization and digital enablement. Samsung Heavy Industries delivered two newbuild drillships in 2024-2025 that immediately entered Petrobras' pre-salt pool, evidencing thin slack in the premium floater segment. Conversely, jack-up oversupply in Southeast Asia pressured Borr Drilling to redeploy four units to the Middle East in 2025, chasing rates 25% higher than in Thailand. Global jack-up utilization was 82% in late 2025 versus 91% for floaters, confirming that shallow-water capacity is absorbing the demand upswing more slowly than deepwater.

Geography Analysis

Asia-Pacific retained 37.6% revenue in 2025 thanks to Thailand, Vietnam, and India, and remains the fastest-growing region at 4.1% CAGR through 2031. PTTEP awarded three jack-up contracts in 2025 to extend life in the Gulf of Thailand, while PetroVietnam kept five rigs active on Bach Ho and Cuu Long, compensating for territorial constraints that slow frontier exploration. India's ONGC extended multiple jack-ups to guard against import dependence, backing the government's 1 million bpd domestic output goal by 2030. China's CNOOC deployed six floaters to South China Sea gas fields to feed the Greater Bay Area's industrial demand, while Woodside advances the Scarborough gas tieback that could enter final investment decision in 2026.

North America showed divergent trends. The U.S. Gulf of Mexico focused on subsea tieback projects, flattening rig demand, whereas Mexico's Pemex secured three jack-up contracts in 2024-2025 to stabilize 1.8 million bpd output. South America remained dominated by Brazil and Guyana. Petrobras operated twelve drillships to hold production above 3 million bpd, while Guyana's Stabroek block kept six floaters busy across development and exploration wells. Trinidad's shallow-water gas wells support Atlantic LNG throughput, sustaining moderate jack-up utilization.

Europe's activity centered on Norway, where Equinor deployed digital twins on Johan Sverdrup to shave 15% off non-productive time. The UK Continental Shelf prioritized decommissioning, letting four jack-ups work well-abandonment campaigns. The Middle East maintained high shallow-water intensity: ADNOC Drilling's 125-rig program underpins a 5 million bpd target, Qatar's North Field East gas expansion required six jack-ups in 2025, and Saudi Aramco's rig count fluctuated with OPEC+ output ceilings. Africa's ultra-deepwater frontier surged, led by Namibia and Angola. TotalEnergies' Kaminho development and Nigeria's Bonga Southwest appraisal reinforced the continent's longer-term rig demand profile.

- Keppel Corp

- Seatrium Ltd (Sembcorp Marine)

- Samsung Heavy Industries

- Hyundai Heavy Industries

- DSME

- China Merchants HI

- CIMC Raffles

- Friede & Goldman

- Damen Shipyards

- Irving Shipbuilding

- Transocean

- Valaris

- Seadrill

- Noble

- Shelf Drilling

- Borr Drilling

- Diamond Offshore

- Stena Drilling

- COSL

- KCA Deutag

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing global energy demand

- 4.2.2 Exploration of untapped offshore reserves

- 4.2.3 Rising deep- & ultra-deepwater discoveries in South America & Africa

- 4.2.4 Decommissioning backlog driving rig-repurposing demand

- 4.2.5 Emergence of offshore carbon-storage & geothermal drilling

- 4.2.6 Accessibility of stranded gas via FLNG developments

- 4.3 Market Restraints

- 4.3.1 Environmental concerns & stricter ESG regulation

- 4.3.2 Crude-oil price volatility impacting CAPEX cycles

- 4.3.3 Subsea tiebacks reducing demand for new exploration wells

- 4.3.4 Supply-chain bottlenecks for ultra-deepwater equipment

- 4.4 Supply-Chain Analysis

- 4.5 Historical Day-Rate Trends (Floaters & Jack-ups)

- 4.6 Major Offshore Upstream Projects Pipeline

- 4.7 Regulatory Landscape (environmental & safety)

- 4.8 Technological Outlook (rig automation, remote ops, digital twins)

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry Intensity

5 Market Size & Growth Forecasts

- 5.1 By Rig Type

- 5.1.1 Jack-ups

- 5.1.2 Semi-submersibles

- 5.1.3 Drillships

- 5.1.4 Other Rig Types (Tender, Barges, Modu conversions)

- 5.2 By Water Depth

- 5.2.1 Shallow Water (Below 400 ft)

- 5.2.2 Deepwater (400 to 5,000 ft)

- 5.2.3 Ultra-deepwater (Above 5,000 ft)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Norway

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Thailand

- 5.3.3.4 Vietnam

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Trinidad and Tobago

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 Angola

- 5.3.5.7 Namibia

- 5.3.5.8 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Keppel Corp

- 6.4.2 Seatrium Ltd (Sembcorp Marine)

- 6.4.3 Samsung Heavy Industries

- 6.4.4 Hyundai Heavy Industries

- 6.4.5 DSME

- 6.4.6 China Merchants HI

- 6.4.7 CIMC Raffles

- 6.4.8 Friede & Goldman

- 6.4.9 Damen Shipyards

- 6.4.10 Irving Shipbuilding

- 6.4.11 Transocean

- 6.4.12 Valaris

- 6.4.13 Seadrill

- 6.4.14 Noble

- 6.4.15 Shelf Drilling

- 6.4.16 Borr Drilling

- 6.4.17 Diamond Offshore

- 6.4.18 Stena Drilling

- 6.4.19 COSL

- 6.4.20 KCA Deutag

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

海上鑽井鑽機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、作業深度、地區和競爭格局分類,2021-2031年

海上鑽井鑽機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、作業深度、地區和競爭格局分類,2021-2031年 半潛式鑽機市場:依鑽井平台類型、深度、移動性、推進方式、定位方式、鑽機功能及最終用戶分類-2026-2032年全球預測

半潛式鑽機市場:依鑽井平台類型、深度、移動性、推進方式、定位方式、鑽機功能及最終用戶分類-2026-2032年全球預測 2026年全球海上開採鑽機市場報告半潛式鑽井鑽機市場(按移動性、合約類型、鑽井技術、類型、水深、鑽井深度、應用和最終用戶分類),全球預測,2026-2032年

2026年全球海上開採鑽機市場報告半潛式鑽井鑽機市場(按移動性、合約類型、鑽井技術、類型、水深、鑽井深度、應用和最終用戶分類),全球預測,2026-2032年 2025-2029年全球海上鑽油平臺市場

2025-2029年全球海上鑽油平臺市場 2026-2032 年海上鑽油平臺市場(按類型、水深和地區)

2026-2032 年海上鑽油平臺市場(按類型、水深和地區) 海上鑽油平臺市場規模、佔有率及成長分析(按服務、供應類型、應用、最終用戶和地區)-2025-2032 年產業預測

海上鑽油平臺市場規模、佔有率及成長分析(按服務、供應類型、應用、最終用戶和地區)-2025-2032 年產業預測