|

市場調查報告書

商品編碼

2066414

模組化建築:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Modular Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

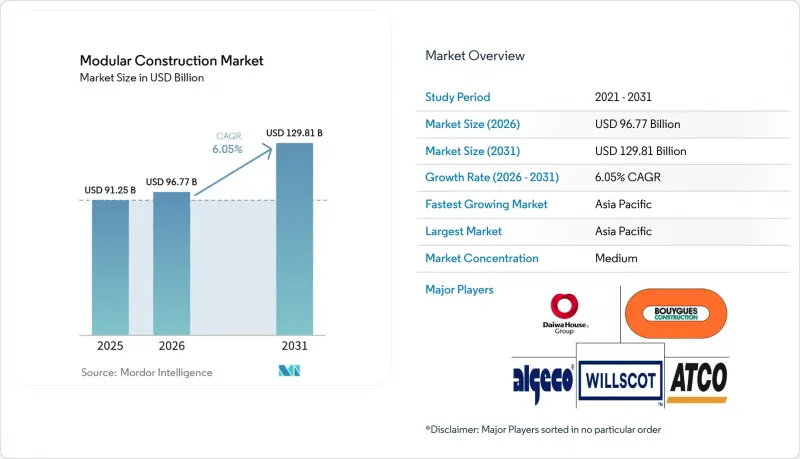

根據 Mordor Intelligence 預測,模組化建築市場預計將從 2025 年的 912.5 億美元成長到 2026 年的 967.7 億美元,到 2031 年達到 1,298.1 億美元,2026 年至 2031 年的複合年成長率為 6.05%。

本報告按材料(鋼材、混凝土、木材、塑膠)、建築類型(永久性模組化建築和移動式模組化建築)、服務階段(新建、售後服務/維護和維修)、最終用戶行業(工業和公共設施、住宅、商業)以及地區(亞太地區、北美、歐洲、南美以及中東和非洲)進行分類。

全球模組化建築市場趨勢與洞察

由於快速都市化導致的住宅短缺

亞太地區的都市化進程正不斷突破傳統建築能力的極限。預計2024年,中國的都市化將達到65%,2030年將達到70%。這項變更將新增3億人口,並增加對更快供應模式的需求。在深圳、北京和上海,公共工程中30%必須採用預製系統;在印度的「總理住房計畫」(Pradhan Mantri Awas Yojana)中,已批准建設1120萬套都市區住宅,其中886.2萬套將於2025年前竣工。在越南,預計2030年城鎮人口比例將達到40%,河內和胡志明市正在進行工業化建築試點計畫。即使是英國也面臨430萬套住宅的缺口,因此制定了每年建造1.5萬套模組化住宅的目標,但由於工廠產能的限制,目前的產量有限。這些因素共同推動了對模組化建築的基本需求。

政府支持措施和法規

監管機構正將政策從自願性指導方針轉向具有法律約束力的配額和直接補貼。加州的工廠化住宅計畫將2024年獲得1,200萬美元州政府技術援助的地區的建築許可核准流程從18個月縮短至6個月。聯邦法案HR 10171提案300億美元的津貼和30億美元的稅額扣抵,以加速模組化建築的推廣應用。同時,修訂後的歐盟建築能源性能指令要求所有新建建築到2030年必須實現零排放。沙烏地阿拉伯的「2030願景」計畫旨在每年建造30萬套住房,該計畫高度重視模組化建築,因為它能夠確保施工速度。這些措施正在提高專案的經濟可行性,使模組化建築市場相對於傳統建築方法更具優勢。

工廠和模組處理初期階段需要大量資本投資。

建立一家年產能500至1000套住宅的中型工廠,需要1500萬至2500萬美元的土地、起重機、自動化焊接設備、溫控工作間及其他相關設備。對於跨州運營的公司而言,還需要數百萬美元用於專用拖車和輔助車輛。工廠需維持60%至70%的運轉率才能達到收支平衡,但由於新興市場企劃案融資管道有限,借貸成本居高不下。這些經濟因素使得模組化建築市場集中在資金雄厚、垂直整合的營運商手中,阻礙了小規模承包商進入該市場。

細分市場分析

到2025年,鋼材將佔據模組化建築市場83.87%的佔有率,這主要得益於其卓越的強度重量比以及與自動化工廠設備的兼容性。隨著ASTM A992等高強度鋼材的出現,鋼材能夠在保證運輸重量限制的前提下實現更長的跨度,預計這一優勢將持續下去。自動化焊接技術透過減少工時和提高接頭質量,進一步鞏固了鋼材在工業和多層建築項目中的地位。

在歐洲和北美,木材(主要是交錯層壓木材:CLT)正逐漸成為一種低碳替代材料,在歐盟木材法規的指導下實現了兩位數的成長。 CLT 每立方公尺儲存約 0.8 噸二氧化碳,目前已符合高達 18 層建築的防火安全標準。由於混凝土模組板材重量大、物流成本高,因此仍屬於小眾產品。同時,塑膠複合材料在災害救援領域正發揮越來越重要的作用,其耐腐蝕性和空運便利性彌補了結構上的不足。儘管材料的不斷創新正在拓展供應商的選擇範圍,但預計到 2031 年,鋼材仍將在模組化建築市場保持絕對主導地位。

預計到2025年,永久性模組化系統將佔模組化建築市場的67.18%,並繼續保持其主導地位,因為機場、學校、資料中心、醫院和其他行業對長壽命資產的需求日益成長。整合式機械和電氣系統均交付預先測試,從而縮短了試運行時間,並最大限度地減少了修改的需要。

移動模組化建築以7.35%的複合年成長率成長,受到採礦、災害救援和臨時醫療設施運營商的青睞,這些運營商優先考慮快速部署和重複使用。 WillScot Mobile Mini公司管理超過20萬套租賃單元,這些單元均包含維護服務,充分展現了靈活資產模式為模組化建築市場帶來的深遠影響。長壽命和可移動設計並存,使供應商能夠應對不同的風險狀況和資金籌措週期。

區域分析

預計到2025年,亞太地區將佔全球銷售額的47.16%,並將以每年7.21%的速度持續成長至2031年。中國計劃在2030年將都市化提高到70%,印度的大規模住宅供應計劃,以及新加坡和馬來西亞強制使用預製建築,都在推動資本流向異地生產。日本大型企業如積水住宅和大型企業正在向澳洲和美國輸出其工廠技術,從而加強其區域價值鏈。

北美地區勞動力短缺,但政府提供大規模獎勵。提案的300億美元聯邦津貼計畫和各州層級的計畫正在縮短核准時間,而像達拉斯/沃斯堡機場F航站樓這樣的大型企劃也展現了規模經濟效益。然而,由於各州法規差異導致合規成本持續高企,以及跨州運輸延誤,模組化建築市場的成長速度正在放緩。

歐洲的發展趨勢以脫碳法規和木材的廣泛應用為特徵。 《建築能源性能指令》強制要求零排放目標,而工廠預製的外牆材料被視為實現合規的捷徑。德國和英國的勞動力短缺正在加速預製建築的轉型。儘管沙烏地阿拉伯和巴西等新興地區的需求強勁,但必須克服資金籌措限制和當地工廠產能不足等問題,才能最大限度地發揮其在模組化建築市場的作用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於快速都市化導致的住宅短缺

- 政府扶持性獎勵和法規

- 專案工期縮短,生命週期成本降低

- 透過異地生產緩解人手不足

- ESG相關金融與碳定價帶來的利多因素

- 市場限制因素

- 初期階段對工廠和模組處理設施進行了大量資本投資。

- 建築和美學設計限制

- 不同國家的建築規範和許可證制度有差異

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 材料

- 鋼

- 具體的

- 樹

- 塑膠

- 依建築類型

- 永久模組化

- 攜帶式模組化

- 服務階段

- 新建工程

- 售後服務、維護與翻新

- 按最終用戶行業分類

- 工業和公共部門

- 住宅

- 商業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ACS Group

- Algeco UK Limited(Modulaire Group)

- Alta-Fab Structures Ltd.

- ATCO Ltd.

- Balfour Beatty

- Bechtel Corporation

- Bouygues Construction

- CIMC Modular Building

- DAIWA HOUSE INDUSTRY CO., LTD.

- Fluor Corporation

- Guerdon, LLC.

- Laing O'Rourke

- Larsen & Toubro Limited

- Lendlease Corporation

- Modular System Sp. z oo

- NRB Modular Solutions

- Red Sea International

- Sekisui House Ltd

- Skanska

- Stack Modular

- Wernick Group

- WillScot

- Zekelman Industries

第7章 市場機會與未來展望

According to Mordor Intelligence, the modular construction market size is expected to increase from USD 91.25 billion in 2025 to USD 96.77 billion in 2026 and reach USD 129.81 billion by 2031, growing at a CAGR of 6.05% over 2026-2031.

This report is Segmented by Material (Steel, Concrete, Wood, and Plastic), Construction Type (Permanent Modular and Relocatable Modular), Service Stage (New Construction and After-Sales Maintenance and Refurbishment), End-User Sector (Industrial/Institutional, Residential, and Commercial), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Global Modular Construction Market Trends and Insights

Rapid Urbanisation-Driven Housing Gap

Asia-Pacific's pace of city growth is stretching conventional building capacity. China's urbanization rate reached 65% in 2024 and is guided to 70% by 2030, a shift that adds 300 million residents and intensifies demand for faster delivery models. Shenzhen, Beijing, and Shanghai require that 30% of public projects use prefab systems, and India's Pradhan Mantri Awas Yojana has cleared 1.12 crore urban units, of which 88.62 lakh were completed by 2025. Vietnam expects 40% urban population by 2030 and is piloting industrialized building in Hanoi and Ho Chi Minh City. Even the United Kingdom faces a 4.3 million-home shortfall, which prompted a target of 15,000 modular units each year, although factory capacity constrains current output. These conditions collectively lift baseline demand for the modular construction market.

Supportive Government Incentives and Mandates

Regulators have moved from voluntary guidelines to binding quotas and direct subsidies. California's Factory-Built Housing program cut permitting cycles from 18 months to 6 months in areas that accepted USD 12 million of state technical aid in 2024. A federal bill, H.R. 10171, proposes USD 30 billion in grants and USD 3 billion in tax credits to accelerate adoption, while Europe's revised Energy Performance of Buildings Directive requires all new structures to be zero-emission by 2030. Saudi Arabia's Vision 2030 program targets 300,000 units per year and ranks modular delivery high for speed assurance. These tools improve project economics, favoring the modular construction market over conventional methods.

High Upfront Factory and Module-Handling CAPEX

Establishing a mid-scale plant that delivers 500-1,000 housing units each year demands USD 15-25 million for land, cranes, automated welders, and climate-controlled bays. Specialized trailers and escort vehicles add several million more for firms that serve multi-state corridors. Factories must operate at 60-70% utilization to meet breakeven, yet limited access to project finance in emerging markets keeps borrowing costs high. These economics funnel activity toward well-capitalized, vertically integrated players and restrain smaller contractors from entering the modular construction market.

Other drivers and restraints analyzed in the detailed report include:

- Faster Project Timelines and Lifecycle Cost Savings

- Labour-Shortage Mitigation Via Off-Site Fabrication

- Architectural and Aesthetic Design Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Steel captured 83.87% of modular construction market share in 2025 thanks to its favorable strength-to-weight profile and compatibility with automated factory tools. That dominance is expected to persist as high-strength grades such as ASTM A992 allow longer spans while staying within transport weight limits. Automated welding drops labor hours and improves joint quality, further anchoring steel in industrial and multi-story projects.

Wood-mainly cross-laminated timber-has emerged as a low-carbon alternative in Europe and North America, enjoying double-digit growth under the EU Timber Regulation. CLT stores about 0.8 tons of CO2 per cubic meter and now meets fire-safety codes up to 18 stories. Concrete modules remain niche due to heavy panel weights that raise logistics costs, while plastic composites are carving out roles in disaster relief where corrosion resistance and airlift ability outweigh structural limits. Continuous material innovation broadens supplier options, yet steel is expected to hold a clear lead in the modular construction market through 2031.

Permanent modular accounted for 67.18% of modular construction market size in 2025 and will stay ahead as airports, schools, data centers, and hospitals seek long-life assets. Integrated mechanical and electrical systems arrive pre-tested, cutting commissioning time and minimizing punch-list items.

Relocatable modular, growing at a 7.35% CAGR, appeals to mining, disaster relief, and temporary healthcare operators that value rapid deployment and reuse. WillScot Mobile Mini manages a fleet of more than 200,000 units under lease contracts that wrap in maintenance, showing how flexible asset models add depth to the modular construction market. The coexistence of long-life and relocatable designs enables suppliers to serve divergent risk profiles and funding cycles.

Geography Analysis

Asia-Pacific contributed 47.16% of global revenue in 2025 and is expected to expand at 7.21% through 2031. China's plan to raise its urbanization ratio to 70% by 2030, India's sizable housing missions, and prefab mandates across Singapore and Malaysia all steer capital toward off-site production. Japanese leaders Sekisui House and Daiwa House export factory know-how into Australia and the United States, strengthening regional value chains.

North America is characterized by labor shortages and large-scale incentives. The proposed USD 30 billion federal grant package and state-level programs shorten approval windows, while mega-projects such as Terminal F at Dallas Fort Worth showcase scale efficiencies. Regulatory fragmentation between states, however, still inflates compliance costs and slows shipment across borders, tempering the pace of modular construction market growth.

Europe's path is defined by decarbonization rules and timber uptake. The Energy Performance of Buildings Directive enforces zero-emission targets, positioning factory-made envelopes as a compliance shortcut. Labor deficits in Germany and the United Kingdom amplify the shift toward prefab methods. Emerging regions, including Saudi Arabia and Brazil, register strong demand but must overcome financing constraints and limited local plant capacity to unlock full contributions to the modular construction market.

- ACS Group

- Algeco UK Limited (Modulaire Group)

- Alta-Fab Structures Ltd.

- ATCO Ltd.

- Balfour Beatty

- Bechtel Corporation

- Bouygues Construction

- CIMC Modular Building

- DAIWA HOUSE INDUSTRY CO., LTD.

- Fluor Corporation

- Guerdon, LLC.

- Laing O'Rourke

- Larsen & Toubro Limited

- Lendlease Corporation

- Modular System Sp. z o.o.

- NRB Modular Solutions

- Red Sea International

- Sekisui House Ltd

- Skanska

- Stack Modular

- Wernick Group

- WillScot

- Zekelman Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urbanisation-Driven Housing Gap

- 4.2.2 Supportive Government Incentives and Mandates

- 4.2.3 Faster Project Timelines and Lifecycle Cost Savings

- 4.2.4 Labour-Shortage Mitigation Via Off-Site Fabrication

- 4.2.5 ESG-Linked Financing and Carbon-Pricing Tailwinds

- 4.3 Market Restraints

- 4.3.1 High Upfront Factory and Module-Handling CAPEX

- 4.3.2 Architectural and Aesthetic Design Constraints

- 4.3.3 Fragmented Global Building Codes and Permits

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Steel

- 5.1.2 Concrete

- 5.1.3 Wood

- 5.1.4 Plastic

- 5.2 By Construction Type

- 5.2.1 Permanent Modular

- 5.2.2 Relocatable Modular

- 5.3 By Service Stage

- 5.3.1 New Construction

- 5.3.2 After-sales Maintenance and Refurbishment

- 5.4 By End-user Sector

- 5.4.1 Industrial/Institutional

- 5.4.2 Residential

- 5.4.3 Commercial

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 NORDIC Countries

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 ACS Group

- 6.4.2 Algeco UK Limited (Modulaire Group)

- 6.4.3 Alta-Fab Structures Ltd.

- 6.4.4 ATCO Ltd.

- 6.4.5 Balfour Beatty

- 6.4.6 Bechtel Corporation

- 6.4.7 Bouygues Construction

- 6.4.8 CIMC Modular Building

- 6.4.9 DAIWA HOUSE INDUSTRY CO., LTD.

- 6.4.10 Fluor Corporation

- 6.4.11 Guerdon, LLC.

- 6.4.12 Laing O'Rourke

- 6.4.13 Larsen & Toubro Limited

- 6.4.14 Lendlease Corporation

- 6.4.15 Modular System Sp. z o.o.

- 6.4.16 NRB Modular Solutions

- 6.4.17 Red Sea International

- 6.4.18 Sekisui House Ltd

- 6.4.19 Skanska

- 6.4.20 Stack Modular

- 6.4.21 Wernick Group

- 6.4.22 WillScot

- 6.4.23 Zekelman Industries

7 Market Opportunities and Future Outlook

- 7.1 Green and Sustainable Construction Demand

- 7.2 White-space and Unmet-Need Assessment

全球模組化建築市場(至2035年):產業趨勢與預測

全球模組化建築市場(至2035年):產業趨勢與預測 全球模組化建築市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球模組化建築市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 模組化建築市場規模、佔有率及成長分析(按類型、材料、模組、最終用途產業和地區分類)-2026-2033年產業預測

模組化建築市場規模、佔有率及成長分析(按類型、材料、模組、最終用途產業和地區分類)-2026-2033年產業預測 模組化建築市場規模、佔有率和趨勢分析報告:按類型、材料、應用、模組、地區和細分市場預測,2026-2033年

模組化建築市場規模、佔有率和趨勢分析報告:按類型、材料、應用、模組、地區和細分市場預測,2026-2033年 全球模組化與可攜式建築市場模組化建築市場:未來預測(2025-2030)

全球模組化與可攜式建築市場模組化建築市場:未來預測(2025-2030) 模組化建築市場評估:按產品(可移動和永久)、材料(木材、鋼材和混凝土)、應用(住宅和非住宅)和地區劃分的機會和預測(2017-2031)全球模組化建築市場規模:按類型、材料、最終用途領域、地區、範圍和預測

模組化建築市場評估:按產品(可移動和永久)、材料(木材、鋼材和混凝土)、應用(住宅和非住宅)和地區劃分的機會和預測(2017-2031)全球模組化建築市場規模:按類型、材料、最終用途領域、地區、範圍和預測 模組化建築市場:到 2033 年的市場分析和預測 - 按類型、按產品、按服務、按技術、按組件、按應用、按材料類型、按工藝、按最終用戶、按地區

模組化建築市場:到 2033 年的市場分析和預測 - 按類型、按產品、按服務、按技術、按組件、按應用、按材料類型、按工藝、按最終用戶、按地區