|

市場調查報告書

商品編碼

2066412

北美飼料氨基酸:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)North America Feed Amino Acids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

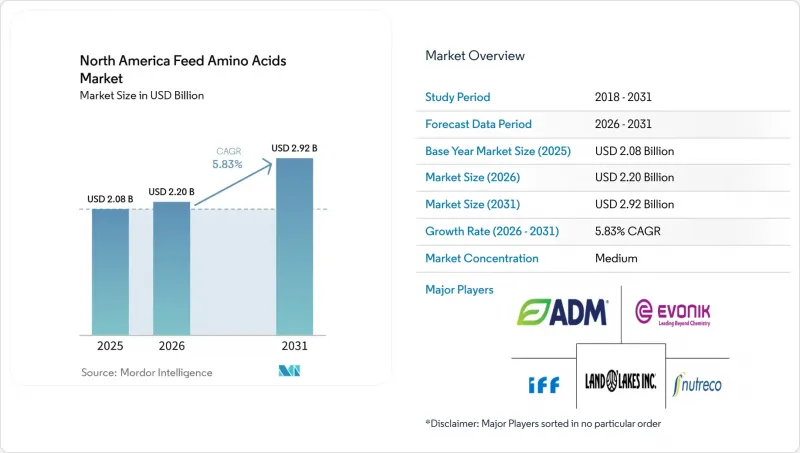

根據 Mordor Intelligence 預測,北美飼料氨基酸市場規模將從 2025 年的 20.8 億美元和 2026 年的 22 億美元成長到 2031 年的 29.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.83%。

本報告按輔助添加劑(離胺酸、甲硫胺酸等)、目標動物(水產養殖、家禽、反芻動物等)和地區(加拿大、墨西哥等)進行細分。市場預測以價值(美元)和數量(公噸)表示。

北美飼料氨基酸市場趨勢與洞察

家禽和生豬生產中對高效蛋白質轉換率的需求日益成長。

為了因應不斷上漲的飼料成本,畜牧養殖戶正優先考慮提高飼料轉換率。一家肉雞一體化生產商透過補充甲硫胺酸和離胺酸,通常能將飼料轉換率降低到1.5:1以下(而傳統方案的飼料轉換率通常為1.8:1),從而使每公斤活重的飼料成本降低0.15美元。在肥育豬飼料添加蘇氨酸,可以在保持增重的同時,將粗蛋白含量從16%降低到14%。胺基酸平衡的改善使氮排泄量減少了高達25%,符合多個州的營養管理法規。這些經濟效益有助於實現合規目標,同時也鞏固了北美市場對飼料氨基酸的需求。

墨西哥和美國工業化規模家禽養殖業務的擴張

墨西哥和美國各地正在進行的現代化項目引入了自動化配料系統,以確保氨基酸配方的精確性。在墨西哥,一項耗資5億美元的飼料廠維修計畫推動了雞肉產量在2024年逐步成長,該計畫實現了數千個雞舍營養成分的標準化。美國的肉雞生產也呈現類似的整合趨勢,前十大公司佔據了國內最大的市場。這些公司之間簽訂的多年採購合約確保了穩定的客戶群,並提高了胺基酸供應商的規模經濟效益。

玉米和大豆價格的波動會影響胺基酸生產的獲利能力。

2024年,玉米價格飆升導致離胺酸生產成本上漲25%,進而引發季度合約審查和毛利率下降。受天然氣價格波動的影響,甲硫胺酸成本每季在每噸200至400美元之間波動。這種不確定性限制了期貨合約的交易,並增加了北美飼料氨基酸市場對營運資金的需求。市場參與企業必須適應這些波動,同時保持營運效率和財務穩定性。

細分市場分析

離胺酸作為家禽和豬用玉米-大豆飼料中的第一限制性氨基酸,預計到2025年將佔據北美飼料氨基酸市場42.15%的佔有率。甲硫胺酸在2026年至2031年間的複合年成長率將達到6.05%,這主要得益於肉雞飼料用量的增加以及新型瘤胃保護乳牛飼料的出現。贏創位於阿拉巴馬州莫比爾的後向整合已使甲硫胺酸成本降低了15%,並提高了供應可靠性。蘇氨酸在蛋雞飼料中的市場佔有率穩步成長,而色氨酸則在旨在減少運輸壓力的細分應用領域中日益受到關注。

甲硫胺酸的成長得益於瘤胃保護配方領域的突破性技術創新,這些創新使酪農能夠在不增加粗蛋白的情況下提高乳蛋白質。纈氨酸、異亮氨酸和組氨酸等特種氨基酸目前在北美飼料氨基酸市場中所佔佔有率不到10%,但隨著精準營養技術的成熟,預計其市場佔有率將有所成長。供應商正在開發與包封和緩釋技術相關的智慧財產權,使其能夠獲得高於通用級產品的溢價。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 飼養的動物數量

- 家禽

- 反芻動物

- 豬

- 飼料生產

- 水產養殖

- 家禽

- 反芻動物

- 豬

- 法律規範

- 加拿大

- 墨西哥

- 美國

- 價值鍊和通路分析

- 市場促進因素

- 家禽和生豬生產中對高效蛋白質轉換率的需求日益成長。

- 墨西哥和美國工業化規模家禽養殖業務的擴張

- 飼料成本壓力正在推動胺基酸補充策略的最佳化。

- 精準發酵法製取的飼料胺基酸的興起降低了價格壁壘。

- 旨在推廣氨基酸均衡飲食的碳足跡展示計劃。

- 擴大胺基酸強化昆蟲粉在水產養殖飼料的應用。

- 市場限制因素

- 玉米和大豆價格的波動會影響胺基酸生產的經濟可行性。

- 進口關稅和貿易不確定性正在擾亂供應鏈。

- 中國過剩的溶素產能引發了人們對北美傾銷的擔憂。

- 消費者強烈抵制有機肉類供應鏈中的化學合成添加劑。

第5章 市場區隔

- 添加劑

- 離胺酸

- 甲硫胺酸

- 蘇胺酸

- 色氨酸

- 其他胺基酸

- 動物

- 水產養殖

- 按目標動物

- 魚

- 蝦

- 其他水產養殖

- 按目標動物

- 家禽

- 按目標動物

- 肉雞

- 產蛋母雞

- 其他家禽

- 按目標動物

- 反芻動物

- 按目標動物

- 牛

- 牛

- 其他反芻動物

- 按目標動物

- 豬

- 其他動物

- 水產養殖

- 地區

- 加拿大

- 墨西哥

- 美國

- 其他北美國家

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介。

- Evonik Industries AG

- Archer-Daniels-Midland Co.

- IFF(Danisco Animal Nutrition)

- SHV(Nutreco NV)

- Land O'Lakes

- Adisseo

- Ajinomoto Co., Inc.

- CJ CheilJedang(CJ BIO)

- BASF SE(Animal Nutrition)

- Novus International, Inc.

- Cargill, Inc.

- Kemin Industries

- Alltech, Inc.

- Balchem Corporation

- Phibro Animal Health Corporation

第7章:執行長面臨的關鍵策略問題

According to Mordor Intelligence, the north america feed amino acids market size is projected to expand from USD 2.08 billion in 2025 and USD 2.20 billion in 2026 to USD 2.92 billion by 2031, registering a CAGR of 5.83% between 2026 and 2031.

This report is Segmented by Sub Additive (Lysine, Methionine, and More), by Animal (Aquaculture, Poultry, Ruminants, and More), and Geography (Canada, Mexico, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Feed Amino Acids Market Trends and Insights

Growing demand for high-efficiency protein conversion in poultry and swine production

Livestock producers are prioritizing feed conversion efficiency to counter elevated feed costs. Broiler integrators routinely achieve feed conversion ratios below 1.5:1 after supplementing methionine and lysine, compared with 1.8:1 in conventional programs, reducing feed expense by USD 0.15 for each kilogram of live weight. Swine finisher diets fortified with threonine cut crude protein from 16% to 14% while sustaining gain rates. Improved amino acid balance trims nitrogen excretion by up to 25%, meeting nutrient management rules in several states. These economics solidify demand for the North America feed amino acids market while supporting compliance goals.

Expansion of industrial-scale poultry farming operations in Mexico and the United States

Modernization projects across Mexico and the United States are embedding automated dosing systems that guarantee precise amino acid inclusion. Mexico produced a modest amount of poultry meat in 2024, underpinned by USD 500 million in feed-mill upgrades that standardize nutrient profiles across thousands of houses. United States broiler production is similarly consolidated, with the top ten firms producing the maximum share of national output. Their multi-year procurement contracts create steady off-take, reinforcing economies of scale for amino acid suppliers.

Volatility in corn and soybean prices affecting amino-acid production economics

Surging corn prices lifted lysine production costs 25% in 2024, prompting quarterly contract resets and shrinking gross margins. Methionine costs fluctuate with natural gas swings, moving USD 200-400 per metric ton quarter to quarter. Such uncertainty limits forward contracting and raises working capital needs across the North America feed amino acids market. The market participants must adapt to these dynamic conditions while maintaining operational efficiency and financial stability.

Other drivers and restraints analyzed in the detailed report include:

- Feed-cost pressures driving optimized amino-acid supplementation strategies

- Carbon-footprint labeling programs incentivizing amino-acid balanced diets

- Import tariffs and trade uncertainties disrupting supply chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lysine held 42.15% of the North America feed amino acids market share in 2025, driven by its status as the first limiting amino acid in corn-soy formulas for poultry and swine. Methionine is progressing at a 6.05% CAGR between 2026 to 2031, buoyed by wider use in broilers and novel rumen-protected forms for dairy cows. Evonik's backward integration in Mobile, Alabama, trims methionine costs by 15%, advancing supply reliability. Threonine enjoys steady gains in layer diets, whereas tryptophan sees niche uptake for stress mitigation in transport settings.

Rumen-protected delivery breakthroughs underpin methionine's momentum, enabling dairy operators to elevate milk protein without increasing crude protein. Specialty amino acids such as valine, isoleucine, and histidine account for less than 10% of the North America feed amino acids market size but offer future upside as precision nutrition matures. Suppliers cultivate intellectual property around encapsulation and timed release, commanding premiums over commodity grades.

List of Companies Covered in this Report:

- Evonik Industries AG

- Archer-Daniels-Midland Co.

- IFF (Danisco Animal Nutrition)

- SHV (Nutreco NV)

- Land O' Lakes

- Adisseo

- Ajinomoto Co., Inc.

- CJ CheilJedang (CJ BIO)

- BASF SE (Animal Nutrition)

- Novus International, Inc.

- Cargill, Inc.

- Kemin Industries

- Alltech, Inc.

- Balchem Corporation

- Phibro Animal Health Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Growing demand for high-efficiency protein conversion in poultry and swine production

- 4.5.2 Expansion of industrial-scale poultry farming operations in Mexico and the United States

- 4.5.3 Feed-cost pressures driving optimized amino-acid supplementation strategies

- 4.5.4 Rise of precision-fermentation-derived feed-grade amino acids lowering price barriers

- 4.5.5 Carbon-footprint labeling programs incentivizing amino-acid balanced diets

- 4.5.6 Increasing adoption of amino-acid enriched insect meal in aquaculture diets

- 4.6 Market Restraints

- 4.6.1 Volatility in corn and soybean prices affecting amino-acid production economics

- 4.6.2 Import tariffs and trade uncertainties disrupting supply chains

- 4.6.3 Excess Chinese lysine capacity triggering dumping concerns in North America

- 4.6.4 Consumer pushback against chemically synthesized additives in organic meat supply chains

5 MARKET SEGMENTATION (VALUE AND VOLUME)

- 5.1 Sub Additive

- 5.1.1 Lysine

- 5.1.2 Methionine

- 5.1.3 Threonine

- 5.1.4 Tryptophan

- 5.1.5 Other Amino Acids

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.1.1 By Sub Animal

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.2.1 By Sub Animal

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Geography

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Evonik Industries AG

- 6.4.2 Archer-Daniels-Midland Co.

- 6.4.3 IFF (Danisco Animal Nutrition)

- 6.4.4 SHV (Nutreco NV)

- 6.4.5 Land O' Lakes

- 6.4.6 Adisseo

- 6.4.7 Ajinomoto Co., Inc.

- 6.4.8 CJ CheilJedang (CJ BIO)

- 6.4.9 BASF SE (Animal Nutrition)

- 6.4.10 Novus International, Inc.

- 6.4.11 Cargill, Inc.

- 6.4.12 Kemin Industries

- 6.4.13 Alltech, Inc.

- 6.4.14 Balchem Corporation

- 6.4.15 Phibro Animal Health Corporation