|

市場調查報告書

商品編碼

2066399

亞太地區人壽及產物保險:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Life And Non-Life Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

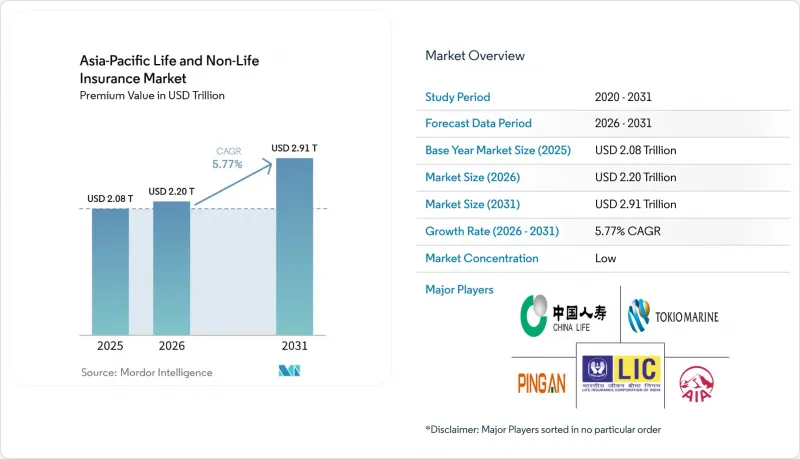

根據 Mordor Intelligence 預測,亞太地區人壽和產物保險市場規模預計將在 2025 年達到 2.08 兆美元,2026 年達到 2.2 兆美元,2031 年達到 2.91 兆美元,2026 年至 2031 年的複合年成長率為 5.7%。

本報告按保險類型(人壽保險、產物保險(汽車、健康、財產、責任等))、客戶群(個人、企業)、銷售管道(仲介、代理人、銀行、直銷、其他管道)和地區(印度、中國、日本、澳洲、韓國、東南亞等)進行細分。市場預測以美元計價。

亞太地區人壽、財產和產物保險市場的趨勢和洞察。

私人醫療保險的擴張是由醫療成本飆升和公共醫療保險體系的不足所驅動的。

2026年1月,印度健康保險保費較上年同期上漲27.17%。這主要得益於淨保費總額增加37.78%,而淨保費成長的促進因素是零售保險合約的商品及服務稅(GST)稅率從18%降至5%,以及「阿尤斯曼·巴拉特」(Ayushman Bharat)計畫使用率的提高。根據怡安集團(Aon)報告顯示,預計2026年印度醫療保健支出成長率將達到11.5%,高於全球平均。許多消費者正在轉向保額更高的保險產品,以支付慢性病和特殊治療的費用。在中國,預計2026年醫療保健支出成長率將達到11.1%。由於基準利率在2025年之前持續下降,保險公司正轉向推出保額較低但分紅型的健康保險產品。此舉旨在調整產品盈利,以適應低利率環境,同時應對不斷成長的保險賠償。新加坡、馬來西亞和菲律賓等國預計到2026年將經歷該地區醫療保健成本成長最快的時期,促使監管機構透過共同支付和免賠額等方式引入成本分擔措施,以遏制過度醫療和防止詐欺。瑞士再保險公司估計,到2024年,亞洲醫療保健覆蓋缺口將達到相當於2,580億美元的保費,這意味著透過私人保險、微額保險和團體保險擴大醫療服務覆蓋範圍的空間巨大。馬來西亞的「可負擔醫療保健藍圖」和印尼選擇性推遲強制性共同保險等政策框架表明,在可負擔性、永續性和更廣泛的覆蓋範圍之間,持續尋求平衡。

受有利的利率環境和退休金改革的推動,人壽保險和退休儲蓄金正處於復甦趨勢。

日本人壽險業預計到2030年將維持5.4%的年成長率,在2024年政策調整後,日圓儲蓄產品的收益率和利率提高,直接保費收入預計將達到3,377億美元。在中國,一項提供稅收優惠和優惠提款率的全國性自願個人退休金計畫於2024年12月推出,截至2024年11月,已開設帳戶7,280萬個。企業提前採用該計劃也表明,人們對補充性退休金計劃的興趣日益濃厚。韓國提議從2026年開始逐步提高國民退休金計畫的繳費率,從9%提高到13%,旨在維持基金的長期支付能力並提高收入替代率。印度的退休金改革提案了延長某些提款等待期和最低餘額要求等規定。同時,2025年9月生效的壽險和醫療保險保費商品及服務稅(GST)免稅政策,有助於減輕保費負擔,並促進長期複利效應。日本和韓國的人口老化,以及印度日益成長的老年人口,正推動亞太地區壽險和產物保險市場對年金、醫療附加險和儲蓄型保險的持續需求。

再保險承保能力和嚴格的合約條款推高了自然災害保險費率和免賠額,使得負擔得起的保險變得困難。

預計到2025年,亞太地區的災害損失將達730億美元,但保險賠償預計僅90億美元,留下巨大的未投保缺口。這抑制了再保險承保能力以能夠迅速填補缺口的價格水平投入的意願。 2024年4月台灣發生的7.2級地震造成13億美元的總損失,並嚴重擾亂了商業活動,導致後續續保的保費更高,合約條款也更加嚴格,與理賠記錄良好的市場相比,情況更是如此。儘管到2025年底全球再保險資本將達到創紀錄水平,但泰國在地震和颱風後也出現了保費上漲的情況。菲律賓的產物保險市場呈現強勁成長,但由於極端天氣事件頻發,索賠額不斷增加,迫使保險公司在保障範圍廣和保費可負擔性之間尋求平衡。儘管澳洲的颶風互助基金在2025年處理了大量保險索賠,但政府支持的承保能力使得高風險地區的保費較基金成立前有所下降。 2026年1月的續約合約顯示,許多無索賠記錄的保單保費有所降低,但免賠額和共同支付率有所上升。一些面臨特定天災風險的再保險投保人則面臨保費持平或兩位數的成長,凸顯了亞太地區人壽和產物保險市場結果的差異性。

細分市場分析

2025年,人壽保險在亞太地區人壽及產物保險市佔率中佔比達63.21%。這主要得益於中國和日本等大型市場對長期保障、年金和儲蓄產品的需求。預計到2031年,亞太地區人壽和產物保險市場中的健康保險市場將以9.10%的複合年成長率成長。這主要是由於醫療成本上漲、慢性病盛行率上升以及監管壓力促使雇主提供保險,導致保險索賠的頻率和嚴重性增加,從而推高了保費。汽車保險行業受益於中國和部分東協市場汽車銷量的成長以及電動汽車的普及,但電池和特殊部件相關的索賠成本仍然是盈利方面的一大挑戰。在面臨自然災害風險的市場,財產保險保費正在趨於整合,而承保規範和再保險結構正在影響續保費率和免賠額。隨著企業越來越傾向於轉移風險,責任險和特殊保險業從小規模的基數開始成長,仲介協助的合約安排和結構化解決方案推動了它們的普及。

在監管機構和雇主正在重新設計免賠額、提款和保險計劃以促進成本分擔和合理使用方面,健康保險的強勁表現尤為顯著。在稅收減免和改進的數位化參保流程的推動下,印度的微型健康保險市場在2026年之前加速成長。同時,團體健康保險的續保定價正變得更加精細化,反映出使用數據和福利上限。中國和印度的汽車保險公司正在採用行為模式的定價和遠端資訊處理技術來區分風險並降低損失趨勢,以應對電氣化和不斷變化的用車模式。在亞太地區人壽和產物保險市場,儲蓄和保障產品的創新持續進行,以應對不斷變化的收益環境,在保證收益降低的地區,分紅型和投資連結型產品的佔有率正在擴大。這些變化表明,到2031年,亞太地區人壽和產物保險市場將轉向更數據驅動和模組化的福利設計方法,涵蓋人壽和產物保險組合。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 私人醫療保險的擴張是由醫療成本飆升和公共保險體系的不足所驅動的(中國、印度、東南亞)。

- 受有利的利率環境和退休金制度改革的推動,人壽保險和退休儲蓄金正處於復甦趨勢。

- 擴大汽車保險承保規模,引入遠端資訊處理和基於里程的保費設置,其中電動車發揮主導作用。

- 對氣候變遷和災難性風險的重新評估正在推高財產和工程保險費。

- 利用超級應用程式和即時支付基礎設施,透過嵌入式保險擴大微額保險。

- 透過 IFRS 17 和 RBC 現代化改造,重新設計產品並實現數據驅動型銷售。

- 市場限制因素

- 供給能力和嚴格的合約條件正在推高自然災害保險費率和免賠額,給賠付帶來壓力。

- 銀行保險業務和產品法規限制在某些市場銷售投資相關產品。

- 醫療保險理賠的通貨膨脹加劇了雇主和個人客戶的賠付率和保費負擔。

- IFRS 17 和 RBC 準則下的資本、人才和資料管治的挑戰正在減緩中型保險公司推出新產品的速度。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 保險類型

- 人壽保險

- 產物保險

- 汽車保險

- 健康保險

- 財產保險

- 責任險

- 其他保險

- 按客戶細分

- 零售

- 公司

- 透過分銷管道

- 仲介

- 機構

- 銀行

- 直銷

- 其他頻道

- 按地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- China Life Insurance(Group)Company

- Ping An Insurance(Group)Company of China, Ltd.

- People's Insurance Company of China(PICC)

- Nippon Life Insurance Company

- Dai-ichi Life Holdings, Inc.

- China Pacific Insurance(Group)Co., Ltd.(CPIC)

- AIA Group Limited

- Tokio Marine Holdings, Inc.

- MS&AD Insurance Group Holdings, Inc.

- Sompo Holdings, Inc.

- QBE Insurance Group Limited

- Insurance Australia Group(IAG)

- Suncorp Group Limited

- Life Insurance Corporation of India(LIC)

- HDFC Life Insurance Company Limited

- SBI Life Insurance Company Limited

- ICICI Prudential Life Insurance Company Limited

- Samsung Life Insurance Co., Ltd.

- Hanwha Life Insurance Co., Ltd.

- Cathay Life Insurance Co., Ltd.

- Fubon Life Insurance Co., Ltd.

- Great Eastern Holdings Limited

- Prudential plc(Asia)

- Manulife Asia

- Sun Life Asia

- AXA Asia & Africa

- Chubb Asia Pacific

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific life and non-Life insurance market size is projected to be USD 2.08 trillion in 2025, USD 2.20 trillion in 2026, and reach USD 2.91 trillion by 2031, growing at a CAGR of 5.77% from 2026 to 2031.

This report is Segmented by Insurance Type (Life Insurance, Non-Life Insurance (Motor, Health, Property, Liability and More)), Customer Segment (Retail, and Corporate), Distribution Channel (Broker, Agents, Banks, Direct Sales, and Other Channels), and Geography (India, China, Japan, Australia, South Korea, Southeast Asia and More). The Market Forecasts are Provided in Value (USD).

Asia-Pacific Life And Non-Life Insurance Market Trends and Insights

Private Health Insurance Expansion Amid Medical Inflation And Public Scheme Gaps

India's health insurance premiums rose 27.17% year over year in January 2026, supported by a reduction of GST on retail policies from 18% to 5% and stronger Ayushman Bharat uptake that lifted gross written premiums by 37.78%. Aon reported India's 2026 medical trend at 11.5%, higher than the global average, and noted that most consumers are moving to higher coverage limits to manage the costs of chronic conditions and specialty treatments. In China, medical trend rates are projected at 11.1% for 2026, and insurers are pivoting to participating health products with lower guarantees as benchmark rates fell through 2025, aligning product economics with a lower-yield environment while addressing claims inflation. Singapore, Malaysia, and the Philippines face some of the steepest 2026 medical trend rates in the region, with regulators adding cost-sharing through co-payments and deductibles to temper utilization and fraud. Swiss Re estimated Asia's health protection gap at USD 258 billion in premium-equivalent terms as of 2024, signaling significant headroom for private cover, micro-policies, and group schemes to expand access. Policy frameworks like Malaysia's affordable health roadmap and selective delays to co-insurance mandates in Indonesia indicate an ongoing balance between affordability, sustainability, and wider coverage.

Life Protection And Retirement Savings Rebound Under Favorable Rates And Pension Reforms

Japan's life sector is on a 5.4% growth path through 2030, reaching USD 337.7 billion in direct written premiums as yields improved after the 2024 policy shift, lifting credited rates on yen-denominated savings products. China's nationwide voluntary personal pensions, implemented in December 2024 with tax incentives and a favorable withdrawal structure, drew 72.8 million account openings by November 2024, and early corporate adoption signals rising interest in supplemental retirement plans. South Korea proposed raising National Pension Scheme contributions from 9% to 13% starting in 2026 with phased increases, targeting longer fund solvency and an improved income replacement rate. India's pension reforms introduced longer waiting periods for certain withdrawals and a minimum balance rule, while the GST exemption on life and health premiums set in September 2025 supports better affordability and long-term compounding. Demographic aging across Japan and South Korea, together with India's expanding senior cohort, is reinforcing persistent demand for annuities, health riders, and protection-backed savings policies in the Asia-Pacific life and non-life insurance market.

Reinsurance Capacity And Tight Terms Raising NatCat Rates And Deductibles, Pressuring Affordability

Asia-Pacific's USD 73 billion in 2025 disaster losses carried only USD 9 billion in insured payouts, leaving a large uninsured gap that constrains appetite to deploy capacity at price levels that would close the gap quickly. Taiwan's 7.2 magnitude earthquake in April 2024 caused USD 1.3 billion in overall losses with significant business interruption, which drove higher pricing and stricter terms at subsequent renewals relative to markets with benign loss experience. Thailand also saw rate increases after seismic and typhoon activity, even as global reinsurer capital reached record levels by late 2025. The Philippines' property segment is experiencing stronger growth but faces rising claims tied to recurring severe weather, with insurers balancing coverage breadth against affordability pressures. Australia's cyclone pool saw large claim volumes in 2025, yet government-backed capacity helped lower premiums in higher-risk areas compared with the period before the pool's establishment. At January 2026 renewals, softening was evident for many loss-free accounts, but deductibles and co-participations rose, and certain catastrophe-exposed cedants faced flat to double-digit increases, underscoring heterogeneous outcomes within the Asia-Pacific life and non-life insurance market.

Other drivers and restraints analyzed in the detailed report include:

- Motor Exposure Growth And EV-Led Telematics And Usage-Based Pricing Adoption

- Climate And Catastrophe Risk Repricing Lifting Property And Engineering Premiums

- Bancassurance Conduct And Product Rules Curbing Investment-Linked Sales In Select Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Life insurance held 63.21% of the Asia-Pacific life and non-life insurance market share in 2025, supported by demand for long-term protection, annuities, and savings products in large markets such as China and Japan. The Asia-Pacific life and non-life insurance market size for health insurance is set to grow at a 9.10% CAGR through 2031, as medical inflation, chronic disease prevalence, and regulatory nudges for employer coverage increase both frequency and severity of claims and drive premium expansion. Motor lines are benefitting from higher vehicle sales and EV penetration in China and select ASEAN markets, although claim costs linked to batteries and specialized parts remain a profitability challenge. Property premiums are adjusting in catastrophe-exposed markets, where underwriting discipline and reinsurance structures are steering rate and deductible decisions at renewal. Liability and specialty lines are growing from smaller bases as corporate risk transfer preferences broaden, with adoption aided by broker placement and structured solutions.

Health's outperformance is visible where regulators and employers introduce co-payments, deductibles, and plan redesign to share costs and encourage responsible utilization. India's retail health segment accelerated into 2026 on the back of a tax-cut tailwind and better digital onboarding, while group health renewal pricing has become more granular, incorporating utilization data and benefit caps. Motor insurers across China and India are deploying behavior-based pricing and telematics to differentiate risk and mitigate loss trends as electrification and usage patterns evolve. The Asia-Pacific life and non-life insurance market continues to see product innovation in savings and protection policies as yield environments change, with participating and unit-linked structures gaining share where guaranteed returns were lowered. These shifts point to a more data-driven and modular approach to benefit design through 2031 in both life and non-life portfolios in the Asia-Pacific life and non-life insurance market.

List of Companies Covered in this Report:

- China Life Insurance (Group) Company

- Ping An Insurance (Group) Company of China, Ltd.

- People's Insurance Company of China (PICC)

- Nippon Life Insurance Company

- Dai-ichi Life Holdings, Inc.

- China Pacific Insurance (Group) Co., Ltd. (CPIC)

- AIA Group Limited

- Tokio Marine Holdings, Inc.

- MS&AD Insurance Group Holdings, Inc.

- Sompo Holdings, Inc.

- QBE Insurance Group Limited

- Insurance Australia Group (IAG)

- Suncorp Group Limited

- Life Insurance Corporation of India (LIC)

- HDFC Life Insurance Company Limited

- SBI Life Insurance Company Limited

- ICICI Prudential Life Insurance Company Limited

- Samsung Life Insurance Co., Ltd.

- Hanwha Life Insurance Co., Ltd.

- Cathay Life Insurance Co., Ltd.

- Fubon Life Insurance Co., Ltd.

- Great Eastern Holdings Limited

- Prudential plc (Asia)

- Manulife Asia

- Sun Life Asia

- AXA Asia & Africa

- Chubb Asia Pacific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Private health insurance expansion amid medical inflation and public scheme gaps (China, India, SEA)

- 4.2.2 Life protection and retirement savings rebound under favorable rates and pension reforms

- 4.2.3 Motor exposure growth and EV-led telematics/usage-based pricing adoption

- 4.2.4 Climate and catastrophe risk repricing lifting property and engineering premiums

- 4.2.5 Embedded insurance via super-apps and real-time payments rails scaling micro coverage

- 4.2.6 IFRS 17 and RBC modernization enabling product redesign and data-driven distribution

- 4.3 Market Restraints

- 4.3.1 Reinsurance capacity/tight terms raising NatCat rates and deductibles, pressuring affordability

- 4.3.2 Bancassurance conduct and product rules curbing investment-linked sales in select markets

- 4.3.3 Health claims inflation elevating loss ratios and premium burdens for employers/retail

- 4.3.4 Capital, talent and data-governance frictions under IFRS17/RBC slowing launches at mid-tier carriers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (value)

- 5.1 By Insurance Type

- 5.1.1 Life Insurance

- 5.1.2 Non-Life Insurance

- 5.1.2.1 Motor Insurance

- 5.1.2.2 Health Insurance

- 5.1.2.3 Property Insurance

- 5.1.2.4 Liability Insurance

- 5.1.2.5 Other Insurance

- 5.2 By Customer Segment

- 5.2.1 Retail

- 5.2.2 Corporate

- 5.3 By Distribution Channel

- 5.3.1 Brokers

- 5.3.2 Agents

- 5.3.3 Banks

- 5.3.4 Direct Sales

- 5.3.5 Other Channels

- 5.4 By Geography

- 5.4.1 India

- 5.4.2 China

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 China Life Insurance (Group) Company

- 6.4.2 Ping An Insurance (Group) Company of China, Ltd.

- 6.4.3 People's Insurance Company of China (PICC)

- 6.4.4 Nippon Life Insurance Company

- 6.4.5 Dai-ichi Life Holdings, Inc.

- 6.4.6 China Pacific Insurance (Group) Co., Ltd. (CPIC)

- 6.4.7 AIA Group Limited

- 6.4.8 Tokio Marine Holdings, Inc.

- 6.4.9 MS&AD Insurance Group Holdings, Inc.

- 6.4.10 Sompo Holdings, Inc.

- 6.4.11 QBE Insurance Group Limited

- 6.4.12 Insurance Australia Group (IAG)

- 6.4.13 Suncorp Group Limited

- 6.4.14 Life Insurance Corporation of India (LIC)

- 6.4.15 HDFC Life Insurance Company Limited

- 6.4.16 SBI Life Insurance Company Limited

- 6.4.17 ICICI Prudential Life Insurance Company Limited

- 6.4.18 Samsung Life Insurance Co., Ltd.

- 6.4.19 Hanwha Life Insurance Co., Ltd.

- 6.4.20 Cathay Life Insurance Co., Ltd.

- 6.4.21 Fubon Life Insurance Co., Ltd.

- 6.4.22 Great Eastern Holdings Limited

- 6.4.23 Prudential plc (Asia)

- 6.4.24 Manulife Asia

- 6.4.25 Sun Life Asia

- 6.4.26 AXA Asia & Africa

- 6.4.27 Chubb Asia Pacific

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment