|

市場調查報告書

商品編碼

2066391

雙碳電池:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Dual Carbon Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

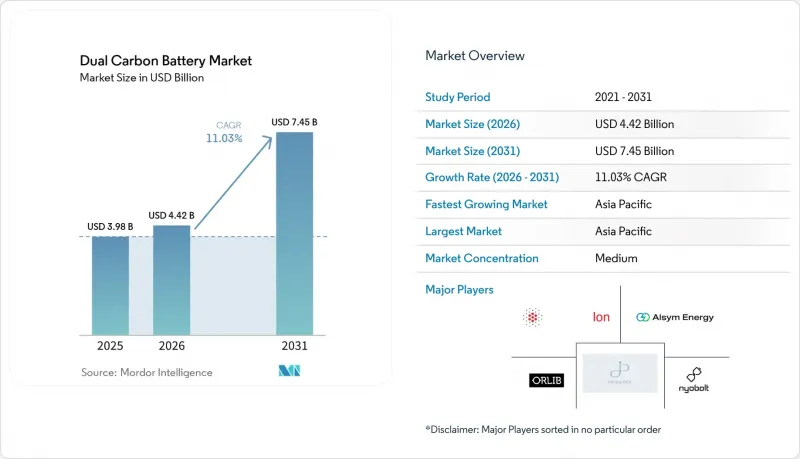

根據 Mordor Intelligence 預測,雙碳電池市場規模將從 2025 年的 39.8 億美元成長到 2026 年的 44.2 億美元,然後在 2031 年達到 74.5 億美元,2026 年至 2031 年的複合年成長率為 11.03%。

本報告按電池類型(一次性雙碳電池和可充電雙碳電池)、容量(小於 10 kWh、10–100 kWh、100–500 kWh 和大於 500 kWh)、應用(汽車電池、工業固定式儲能、可攜式/消費性電子產品、航太和國防等)以及地區(北美、歐洲、亞太地區分類和以及中東、歐洲和非洲地區進行分類。

全球雙碳電池市場趨勢與洞察

電動車快速電氣化的相關法規

歐盟和美國多個州計劃在2035年後禁止銷售新的內燃機汽車,這顯著提升了對可在5分鐘內充電至10-80%且無需高成本冷卻迴路的電池的潛在需求。雙碳電極能夠承受高電流,同時保持比同類鋰離子電池組低18 度C的核心溫度,從而簡化了溫度控管硬體。中國力爭2030年實現新能源汽車40%的市場佔有率,進一步刺激了市場需求。為規避鎳鈷價格波動風險,國內汽車製造商正轉向使用除NMC基化學成分以外的其他材料。監管合規的分階段期限與超級工廠產能擴張的預期相吻合,使得專業研發公司能夠在傳統供應商完成合規之前鎖定供應合約。

獎勵建立碳中和供應鏈

歐盟的電池護照將於2027年2月起強制執行,要求製造商揭露從生產開始到工廠出貨的整個過程中的二氧化碳排放強度和回收材料含量。全碳電極無需高溫金屬提煉,從而減少了隱含排放,其化學成分也使其符合相關法規的高評級標準。在美國,如果國內採購比例超過60%,根據《通膨削減法案》,稅額扣抵將提高至每度45美元。在美國,使用天然石墨或碳纖維的「雙碳」電池製造商可以達到這項標準。旨在減少範圍3排放的企業買家擴大在報價階段要求提供生命週期評估(LCA)數據,低碳化學成分正逐漸成為採購的必要條件,而不僅僅是行銷附加價值。

從單體電池到電池封裝的熱失控測試已暫停。

大多數型式認證協議仍專注於鋰離子電池的濫用模式,對於雙碳等化學成分,尚無明確的合格/不合格標準。監管機構要求提供單獨的測試矩陣,而缺乏成文標準導致每個車輛項目的認證週期延長6-9個月。目前,ISO和IEC正在製定臨時指南草案,但預計要到2026年下半年才能最終定稿,這將限制車輛短期內進入市場。對於缺乏資源在多個地區並行進行檢驗專案的中型供應商而言,這種延誤將造成尤其嚴重的打擊。

細分市場分析

至2025年,可充電產品將佔雙碳電池市場86.35%的佔有率。這反映了該化學體系適用於需要反覆充放電的應用,例如搭乘用電動車和電動巴士車隊。長期道路測試證實,即使經過3000次完全深度循環,其容量維持率仍高達80%,與金屬基電池相比,總擁有成本(TCO)更低。金屬基電池需要過度設計的電池組才能滿足保固要求。一次性雙碳電池仍屬於小眾產品,主要用於航太領域的緊急電源,在這些領域,安全故障模式比經濟效益更為重要。

2025年,一家大型研發公司獲得3,000萬美元C輪資金籌措,並宣布汽車業已採用八項設計,可充電電池的商業性應用由此加速。標準化的21700和46xx外形規格目前已開始在試點生產線上進行量產,使得電池組製造商只需對模具進行少量改動即可完成整合。隨著應用範圍的擴大,規模經濟預計將在2025年至2028年間使每千瓦時成本降低約22%,從而縮小與磷酸鋰鐵鋰電池的價格差距。

區域分析

預計到2025年,亞太地區的市佔率將達到49.02%,凸顯了其從針狀焦原料到成品電極的深度垂直整合。中國合成石墨生產商正利用水力發電和太陽能等自發電方式,將隱含排放控制在每千瓦時4公斤二氧化碳當量以下,遠低於歐洲平均。區域各國政府為試點生產線提供20%的資本津貼,加速在地化生產並維持出口成本優勢。在各國政策強制規定電動車電池組使用國產零件的最低標準的推動下,預計到2031年,亞太「雙碳」電池市場將以12.1%的複合年成長率成長。

北美是該地區成長最快的市場。由於《通貨膨脹削減法案》中每塊汽車電池模組最高可達3,750美元的稅額扣抵,預計到2025年,至少有四家原始設備製造商(OEM)將與美國雙碳新創公司簽署有條件啟動協議。美國能源部提供的2,500萬美元資金籌措正在支持11個項目,以擴大國內電極塗層和離子液體電解質的合成。加拿大礦業公司正透過兩個計畫於2027年運作的大型片狀石墨項目,確保穩定的原料供應,這也有助於降低物流成本。

歐洲未來的發展取決於與碳基化學品完全一致的永續性法規。 「電池護照」鼓勵可追溯性和低排放材料的使用。芬蘭和瑞典的木質素衍生碳先導工廠的目標是到2028年實現年總合1.5萬噸的產能。歐洲汽車製造商目前從日本生產線進口原型電池,但計劃在前驅體供應鏈建立後開始本地生產模組。儘管中東和非洲市場規模仍然小規模,但沿岸地區的電力公司對沙漠氣候下的儲能系統表現出濃厚的興趣,因為沙漠地區的高溫會對傳統的鋰離子電池系統產生不利影響。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車快速電氣化的相關法規

- 獎勵建立碳中和供應鏈

- 關於廢舊產品可回收性的規定

- 電動巴士充電速度提升20倍的試點項目

- 透過 OEM 過渡到不需要負極的化學系統。

- 競標電網邊緣超高速儲能系統

- 市場限制因素

- 目前正在等待電池到封裝的熱失控測試結果。

- 缺乏 ISO/IEC 性能標準

- 大規模碳前驅物的供應有限。

- 創業投資正轉向固態能源領域。

- 比較分析:雙碳電池與其他電池技術

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依電池類型

- 免洗雙碳電池

- 可充電雙碳電池

- 按產能

- 小於10千瓦時

- 10~100 kWh

- 100~500 kWh

- 500度或以上

- 透過使用

- 汽車電池

- 工業固定式儲能系統

- 可攜式設備和家用電子設備

- 航太/國防

- 其他小眾應用

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 東南亞國協

- 其他亞太國家

- 南美洲

- 阿根廷

- 巴西

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和市場佔有率)

- 公司簡介

- PJP Eye Ltd(Power Japan Plus)

- Nyobolt

- Alsym Energy

- Carbon-Ion

- ORLIB Ltd

- Farad Power

- Panasonic Energy

- LG Energy Solution

- BYD Co. Ltd

- CATL

- Samsung SDI

- Hitachi Energy

- Toshiba

- Envision AESC

- Sion Power

- StoreDot

- Enevate

- QuantumScape

- Skeleton Technologies

- Northvolt

第7章 市場機會與未來展望

According to Mordor Intelligence, the dual carbon battery market size is expected to grow from USD 3.98 billion in 2025 to USD 4.42 billion in 2026 and is forecast to reach USD 7.45 billion by 2031 at 11.03% CAGR over 2026-2031.

This report is Segmented by Battery Type (Disposable Dual-Carbon Cells and Rechargeable Dual-Carbon Cells), Capacity (Below 10 KWh, 10 To 100 KWh, 100 To 500 KWh, and Above 500 KWh), Application (Automotive Batteries, Industrial Stationary Storage, Portable/Consumer Electronics, Aerospace and Defense, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Dual Carbon Battery Market Trends and Insights

Rapid EV Electrification Mandates

Policies banning new internal-combustion models from 2035 in the EU and several U.S. states significantly expand the addressable demand for batteries that can charge from 10-80% in five minutes without high-cost cooling loops. Dual carbon electrodes withstand elevated currents while maintaining core temperatures 18 °C lower than those of comparable lithium-ion packs, enabling simpler thermal management hardware. China's New Energy Vehicle target of 40% sales penetration by 2030 further cements volume pull, as domestic OEMs diversify beyond NMC chemistries to hedge against nickel and cobalt volatility. Staggered compliance deadlines align with expected gigafactory ramp-ups, allowing specialist developers to lock in offtake agreements before legacy suppliers adapt.

Carbon-Neutral Supply-Chain Incentives

The EU Battery Passport, which becomes compulsory from February 2027, requires manufacturers to disclose cradle-to-gate CO2 intensities and recycled-content percentages. Full-carbon electrodes reduce embodied emissions by eliminating high-temperature metal smelting, positioning the chemistry for premium scoring under the regulation. In the United States, the Inflation Reduction Act tax credits increase to USD 45 per kWh when domestic content exceeds 60%, a threshold that is attainable for dual carbon producers using U.S. natural graphite or carbon fiber. Corporate buyers seeking Scope 3 emission reductions increasingly request life-cycle assessment data at the request-for-quotation stage, turning low-carbon chemistries into a procurement prerequisite rather than a marketing plus.

Cell-to-Pack Thermal-Runaway Tests Pending

Most homologation protocols still revolve around lithium-ion abuse modes, leaving chemistries like dual carbon without explicit pass-fail criteria. Regulatory agencies require bespoke test matrices, and the absence of codified standards prolongs qualification by six to nine months per vehicle program. Interim guidelines are currently under draft at the ISO and IEC, but are not expected until late 2026, which will constrain near-term automotive launches. The delay particularly hurts mid-tier suppliers that lack the resources to run parallel validation programs across multiple regions.

Other drivers and restraints analyzed in the detailed report include:

- End-of-Life Recyclability Regulations

- 20x-Faster Charge Pilots in E-buses

- Limited Large-Scale Carbon Precursor Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rechargeable products accounted for 86.35% of the dual carbon battery market in 2025, reflecting the chemistry's suitability for repeated-cycle applications, such as passenger EVs and fleet e-buses. Long-term road tests demonstrate 3,000 full-depth cycles with 80% capacity retention, resulting in a lower total cost of ownership compared to metal-based cells that require pack oversizing to meet warranty obligations. Disposable dual-carbon formats remain niche, chiefly in aerospace emergency power, where benign failure modes trump unit economics.

Commercial traction for rechargeables accelerated after a leading developer secured USD 30 million Series C funding and disclosed eight automotive design wins in 2025. Standardized 21700 and 46xx form factors now roll off pilot lines, enabling pack-maker integration with minimal tooling change. As deployment widens, economies of scale are expected to reduce the cost per kWh by an estimated 22% between 2025 and 2028, thereby narrowing the pricing gap with lithium-iron-phosphate.

Geography Analysis

Asia-Pacific's 49.02% share in 2025 underscores deep vertical integration from needle coke feedstock to finished electrodes. Chinese synthetic-graphite producers leverage captive power sourced from hydroelectric and solar sources, keeping embodied emissions under 4 kg CO2-eq per kWh, which is well below European averages. Regional governments offer 20% capital-grant ratios for pilot lines, accelerating local output and maintaining export cost leadership. The dual carbon battery market size in Asia-Pacific is forecast to advance at a 12.1% CAGR to 2031, supported by national policies mandating minimum domestic content in EV packs.

North America is the fastest-growing market in the region. Inflation Reduction Act credits worth up to USD 3,750 per vehicle battery module drove at least four OEMs to sign conditional offtake agreements with U.S. dual carbon start-ups in 2025. The Department of Energy's USD 25 million funding round supports eleven projects that scale electrode coating and ionic-liquid electrolyte synthesis onshore. Canadian mining ventures enhance feedstock security with two large flake-graphite projects scheduled for commissioning in 2027, which helps lower logistics costs.

Europe's trajectory hinges on sustainability regulations that align squarely with carbon-based chemistries. The Battery Passport favors traceable, low-emission materials. Lignin-derived carbon pilot plants in Finland and Sweden target a combined annual capacity of 15,000 tons by 2028. European automakers currently import prototype cells from Japanese lines but intend to localize modules once the precursor supply matures. Middle East and African markets remain small, although Gulf utilities have expressed interest in desert-climate storage, where high ambient temperatures penalize traditional lithium-ion systems.

- PJP Eye Ltd (Power Japan Plus)

- Nyobolt

- Alsym Energy

- Carbon-Ion

- ORLIB Ltd

- Farad Power

- Panasonic Energy

- LG Energy Solution

- BYD Co. Ltd

- CATL

- Samsung SDI

- Hitachi Energy

- Toshiba

- Envision AESC

- Sion Power

- StoreDot

- Enevate

- QuantumScape

- Skeleton Technologies

- Northvolt

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid EV electrification mandates

- 4.2.2 Carbon-neutral supply-chain incentives

- 4.2.3 End-of-life recyclability regulations

- 4.2.4 20x-faster charge pilots in e-buses

- 4.2.5 OEM shift to anode-free chemistries

- 4.2.6 Grid-edge ultra-fast storage tenders

- 4.3 Market Restraints

- 4.3.1 Cell-to-pack thermal-runaway tests pending

- 4.3.2 Absence of ISO/IEC performance standard

- 4.3.3 Limited large-scale carbon precursor supply

- 4.3.4 VC funding tilt towards solid-state

- 4.4 Comparative Analysis: Dual-Carbon vs Other Battery Technologies

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Disposable Dual-Carbon Cells

- 5.1.2 Rechargeable Dual-Carbon Cells

- 5.2 By Capacity

- 5.2.1 Below 10 kWh

- 5.2.2 10 to 100 kWh

- 5.2.3 100 to 500 kWh

- 5.2.4 Above 500 kWh

- 5.3 By Application

- 5.3.1 Automotive Batteries

- 5.3.2 Industrial Stationary Storage

- 5.3.3 Portable/Consumer Electronics

- 5.3.4 Aerospace and Defense

- 5.3.5 Other Niche Uses

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 ASEAN Countries

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Argentina

- 5.4.4.2 Brazil

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PJP Eye Ltd (Power Japan Plus)

- 6.4.2 Nyobolt

- 6.4.3 Alsym Energy

- 6.4.4 Carbon-Ion

- 6.4.5 ORLIB Ltd

- 6.4.6 Farad Power

- 6.4.7 Panasonic Energy

- 6.4.8 LG Energy Solution

- 6.4.9 BYD Co. Ltd

- 6.4.10 CATL

- 6.4.11 Samsung SDI

- 6.4.12 Hitachi Energy

- 6.4.13 Toshiba

- 6.4.14 Envision AESC

- 6.4.15 Sion Power

- 6.4.16 StoreDot

- 6.4.17 Enevate

- 6.4.18 QuantumScape

- 6.4.19 Skeleton Technologies

- 6.4.20 Northvolt

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

雙碳電池市場:依電解液類型、電芯結構、電池類型、容量、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

雙碳電池市場:依電解液類型、電芯結構、電池類型、容量、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 雙碳電池市場:產品類型、電池容量、應用、最終用途 - 2026-2032年全球市場預測

雙碳電池市場:產品類型、電池容量、應用、最終用途 - 2026-2032年全球市場預測 雙碳電池市場 - 全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)

雙碳電池市場 - 全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年) 雙碳電池市場規模、佔有率和成長分析(按類型、電池結構、電解液類型、應用和地區分類)—2026-2033年產業預測雙碳電池市場報告:趨勢、預測和競爭分析(至 2031 年)

雙碳電池市場規模、佔有率和成長分析(按類型、電池結構、電解液類型、應用和地區分類)—2026-2033年產業預測雙碳電池市場報告:趨勢、預測和競爭分析(至 2031 年) 至 2030 年雙碳電池市場預測:按組件、電池類型、應用和地區分類的全球分析

至 2030 年雙碳電池市場預測:按組件、電池類型、應用和地區分類的全球分析