|

市場調查報告書

商品編碼

2066373

咖啡:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Coffee - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

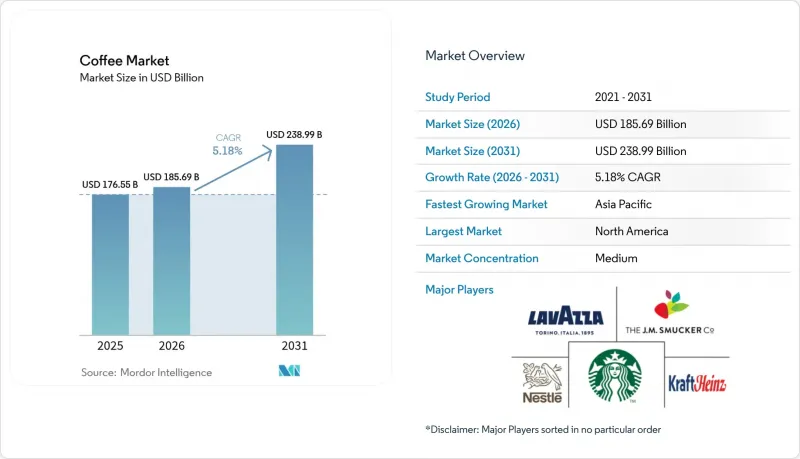

據 Mordor Intelligence 稱,2025 年全球咖啡市場價值 1765.5 億美元,預計到 2031 年將達到 2389.9 億美元,而 2026 年為 1856.9 億美元,預測期(2026-2031 年)複合年成長率為 5.18%。

本報告按產品類型(生咖啡豆、咖啡粉等)、分銷管道(On-Trade和Off-Trade)、咖啡品種(阿拉比卡、羅布斯塔等)、產地(單一產地/專門食品和拼配咖啡)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以價值(美元)和銷售量(噸)為單位呈現。

全球咖啡市場趨勢及洞察

專門食品和優質咖啡的需求不斷成長

隨著消費者偏好不斷演變,尤其是在年輕一代中,對專門食品和高階咖啡日益成長的需求正在推動全球咖啡市場的發展。在美國,專門食品咖啡正成為零售消費的重要組成部分。根據美國國家咖啡協會(NCA)預測,到2024年,46%的美國成年人將飲用專門食品咖啡。這一趨勢在美國咖啡市場也十分明顯,反映出消費者對單一產地咖啡豆、符合道德標準的採購方式以及咖啡館式體驗的興趣日益濃厚。在全球範圍內,由於強勁的外出用餐需求以及專門食品咖啡對經濟挑戰的抵禦能力,其消費成長速度超過了傳統咖啡。在印度,儘管國內咖啡消費量穩定成長,但根據印度外交部截至2025年6月的數據,該國的咖啡出口量預計將在過去十年加倍,到2024會計年度達到18億美元。隨著消費者將焦點從單純的價格轉向品質、獨特風味和符合道德標準的採購方式,專門食品咖啡的市場佔有率持續擴大。

千禧世代與Z世代中日益興起的咖啡文化

千禧世代和Z世代在全球咖啡市場成長中扮演著重要角色。這些年輕消費者追求高品質、符合道德標準的咖啡,並偏好獨特的風味和高階體驗。他們中的許多人更喜歡專門食品咖啡館和手工咖啡,而不是主流咖啡。根據Convenience Org報告,Z世代咖啡愛好者選擇冰咖啡的頻率與熱咖啡一樣高,約85%的人會添加奶精,而所有咖啡愛好者中只有70%的人會這樣做。這顯示他們更偏愛風味獨特、口感豐富的咖啡。他們也更傾向於在戶外飲用咖啡,從而推動了咖啡文化的流行。在印度,根據印度咖啡委員會的一份報告,都市化、收入成長以及連鎖咖啡館的興起正在推動咖啡在年輕人中的流行。這些偏好的轉變正在重塑全球咖啡市場,推動創新和穩定成長。

監管壓力和進出口限制

監管壓力和不斷變化的貿易限制正給全球咖啡市場帶來重大挑戰。例如,2025年8月,美國對巴西咖啡徵收50%的關稅,擾亂了既有的供應鏈。這迫使出口商將出貨地轉向中國和歐盟等其他市場,為世界領先的咖啡供應國之一巴西帶來了不確定性。同樣,印度推出了新的進口法規,要求咖啡豆必須提供燻蒸證明以防止蟲害。這些法規進一步加重了出口商的合規負擔。結果,營運成本上升,出貨延遲,小規模生產商難以適應新的標準和文件要求。這些挑戰正在重塑市場動態,尤其對那些缺乏資源有效應對這些監管變化的生產者和出口商而言更是如此。

細分市場分析

到2025年,研磨咖啡將佔全球咖啡市場佔有率的33.02%,並繼續保持其作為咖啡產品中最大收入來源的地位。其受歡迎程度主要源自於消費者對濃郁香氣、醇厚口感及沖泡體驗的重視。隨著越來越多的人購買家用咖啡沖泡設備,例如法式濾壓壺、摩卡壺和濃縮咖啡咖啡機,人們對在家享用咖啡館品質咖啡的需求也日益成長。這一趨勢表明,人們越來越注重咖啡的高品質,尤其是在歐洲和北美等成熟市場。

同時,即飲咖啡(RTD)市場預計將在2026年至2031年間以7.52%的複合年成長率成長,成為咖啡市場中成長最快的細分市場。速溶咖啡曾經僅被視為便捷的提神飲品,但如今卻變得優質化。精緻口味、冷萃和專門食品調配方以及先進萃取技術的引入,顯著提升了即溶咖啡的口感和風味。忙碌的都市區年輕人越來越青睞單份罐裝和瓶裝咖啡,尤其是那些功能更強大、更注重健康的產品。他們也更傾向於在便利商店購買,這表明他們對能夠輕鬆融入忙碌生活的攜帶式咖啡有著很高的需求。這種轉變凸顯了人們對能夠以便捷方式享用的咖啡師品質咖啡的需求日益成長,鞏固了即飲咖啡在新興和成熟飲料市場中的重要驅動力。

在2025年的全球咖啡市場預測中,阿拉比卡咖啡豆仍將佔據主導地位,市佔率高達56.74%。其順滑的口感和低咖啡因含量使其深受注重品質的消費者喜愛。阿拉比卡咖啡豆生長於涼爽的高海拔地區,廣泛用於專門食品咖啡和高級拼配咖啡,尤其是在北美、歐洲和日本等已開發市場。家庭咖啡沖泡的日益普及以及消費者對單一產地和可追溯咖啡產品(其中風味和品質是關鍵因素)需求的成長,進一步推動了阿拉比卡咖啡豆的流行。

儘管阿拉比卡咖啡目前在市場規模上佔據主導地位,但羅布斯塔咖啡預計將成為成長最快的咖啡品種,到2031年複合年成長率將達到5.98%。羅布斯塔咖啡以其更濃郁、更苦澀的風味和更高的咖啡因含量而聞名,由於其價格實惠且風味濃郁,擴大被用於濃縮咖啡濃縮咖啡、即飲咖啡和速溶咖啡中。其對氣候變遷和病蟲害的高抵抗力也使其成為越南、巴西和非洲部分地區等國家咖啡生產商的首選。隨著加工技術和風味的不斷改進,羅布斯塔咖啡在經濟和創新咖啡市場都獲得了認可,市場佔有率不斷擴大。

區域分析

到2025年,北美將佔全球咖啡市場銷售額的23.64%。這主要得益於其濃厚的咖啡文化、冷萃咖啡的流行以及專門食品咖啡的廣泛普及。該地區擁有全球最高的人均咖啡消費量之一,這也支撐了高級產品的高價。北美咖啡烘焙商也在永續發展方面主導作用,例如透過與墨西哥農民合作進行再生農業,以及為哥倫比亞生產商提供適應性融資。這些舉措正在為永續咖啡生產和供應鏈實踐樹立全球標準。該地區對創新和永續發展的重視將繼續塑造全球咖啡市場的格局。

中東和非洲是咖啡市場成長最快的地區,預計到2031年複合年成長率將達到8.16%。中產階級收入的成長和年輕都市區的增加正在加速中東和非洲地區對咖啡的需求,消費者正從傳統咖啡消費模式轉向更高階的咖啡館和居家咖啡體驗。在沿岸地區,杜拜、利雅德和杜哈等城市湧現大量專門食品咖啡館和國際連鎖店。這些咖啡館融合了悠久的咖啡傳統和第三波咖啡浪潮的概念,使該地區成為體驗式、設計感十足的咖啡空間的典範。在埃塞俄比亞、奈及利亞和南非等非洲市場,國內咖啡消費更加活躍,人們越來越關注本地種植的阿拉比卡咖啡豆、專門食品烘焙商以及面向富裕消費者和資深咖啡愛好者的膠囊咖啡系統。從人流量大的購物中心提供的專屬飲品,到酒店和辦公室提供的優質膠囊咖啡,該地區日益成熟的咖啡文化和不斷變化的偏好正在推動餐飲服務和零售咖啡領域的強勁成長。

歐洲在重塑全球咖啡市場方面發揮關鍵作用,尤其體現在其嚴格的永續發展法規上。這些法規推動了咖啡採購可追溯性的提升,而這正逐漸成為全球標準。斯堪地那維亞國家在推廣公平貿易咖啡方面處於領先地位,而義大利和法國等傳統市場則在對經典咖啡的熱愛與對單一產地濃縮咖啡日益成長的興趣之間尋求平衡。拉丁美洲既是主要的咖啡生產地,也是新興的消費市場,其國內咖啡消費量正持續成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 專門食品和優質咖啡的需求不斷成長

- 千禧世代與Z世代中日益興起的咖啡文化

- 即飲/冷萃咖啡的消費量正在激增。

- 對永續性和道德採購的意識

- 面向企業和職場的咖啡解決方案

- 社群媒體與網紅行銷的影響

- 市場限制因素

- 咖啡豆價格波動

- 關稅壁壘和歐盟關於森林砍伐的法規。

- 監管壓力和進出口限制

- 消費者對咖啡因及其健康風險的擔憂

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 整豆

- 研磨咖啡

- 即溶咖啡

- 即飲型(RTD)

- 咖啡膠囊和咖啡包

- 透過分銷管道

- On-Trade

- Off-Trade

- 超級市場和大賣場

- 便利商店

- 專業零售商

- 線上零售

- 其他Off-Trade通路

- 咖啡品種

- 阿拉比卡

- 羅布斯塔

- 利比里卡

- 其他

- 按原產地

- 單一產地/專門食品

- 混合物

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 哥倫比亞

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 印尼

- 越南

- 馬來西亞

- 新加坡

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 南非

- 埃及

- 科威特

- 衣索比亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nestle SA

- UCC Ueshima Coffee Co.

- Starbucks Corporation

- The Kraft Heinz Company

- Luigi Lavazza SpA

- Massimo Zanetti Beverage Group SpA

- The JM Smucker Company

- Tata Consumer Products

- Coava Coffee Roasters

- Tchibo GmbH

- Louis Dreyfus Company Coffee

- TGL Company

- Trung Nguyen Legend Group

- Mayora Group(Kopiko)

- The Coca-Cola Company

- Unilever PLC

- Zino Davidoff Group

- Sleepy Owl Coffee

- Bewley's Limited

- Strauss Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the global coffee market size was valued at USD 176.55 billion in 2025 and estimated to grow from USD 185.69 billion in 2026 to reach USD 238.99 billion by 2031, at a CAGR of 5.18% during the forecast period (2026-2031).

This report is Segmented by Product Type (Whole-Bean, Ground Coffee, and More), Distribution Channel (On-Trade and Off-Trade), Coffee Species (Arabica, Robusta and More), Origin (Single Origin/Specialty and Mixed), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Coffee Market Trends and Insights

Rising demand for specialty and premium coffee

Growing demand for specialty and premium coffee is driving the global coffee market, as consumer preferences continue to evolve, particularly among younger generations. In the United States, specialty coffee has become a significant part of retail consumption. According to the National Coffee Association of the USA, 46% of American adults consumed specialty coffee in 2024.This trend is also evident in the U.S. coffee market, reflecting rising interest in single-origin beans, ethically sourced products, and cafe-style experiences. Globally, specialty coffee consumption is increasing at a faster pace compared to traditional coffee, supported by strong demand for out-of-home consumption and its ability to withstand economic challenges. In India, domestic coffee consumption has been steadily rising, while the country's coffee exports have doubled over the past decade, reaching USD 1.8 billion in FY24, according to the Ministry of External Affairs as of June 2025. As consumers place greater importance on quality, unique flavors, and ethical sourcing rather than focusing solely on price, specialty coffee continues to expand its market share.

Growing coffee culture among millennials and gen Z

Millennials and Gen Z are playing a major role in the growth of the global coffee market. These younger consumers are looking for high-quality, ethically sourced coffee and prefer unique flavors and premium experiences. Many of them enjoy specialty cafes and artisanal coffee over regular options. According to Convenience Org, Gen Z coffee drinkers are just as likely to start with iced coffee as hot coffee, and about 85% of them add creamer, compared to 70% of coffee drinkers overall. This shows their preference for personalized and flavorful coffee. They also tend to drink more coffee outside the home, boosting the popularity of cafe culture. In India, urbanization, higher incomes, and the rise of cafe chains have made coffee more popular among young adults, as reported by the Coffee Board of India. These changing preferences are reshaping the coffee market worldwide, driving innovation and steady growth.

Regulatory pressure and import/export restrictions

Regulatory pressure and changing trade restrictions are creating significant challenges for the global coffee market. For instance, in August 2025, the U.S. introduced a 50% tariff on Brazilian coffee, disrupting established supply chains. This forced exporters to redirect shipments to alternative markets like China and the European Union, creating uncertainty for Brazil, one of the largest coffee suppliers globally. Similarly, India has implemented new import rules requiring fumigation certificates for coffee beans to prevent pest infestations. These regulations have added extra compliance burdens for exporters. As a result, operational costs are rising, shipments are facing delays, and smaller producers are struggling to adapt to the new standards and documentation requirements. These challenges are reshaping the market dynamics, particularly for producers and exporters who lack the resources to navigate these regulatory changes effectively.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability and ethical sourcing awareness

- Corporate and workplace coffee solutions

- Consumer concerns over caffeine and health risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ground coffee made up 33.02% of the global coffee market share in 2025, maintaining its position as the top revenue generator among coffee products. Its popularity is driven by consumers valuing the rich aroma, flavor, and brewing experience it offers. With more people buying home brewing equipment like French presses, moka pots, and espresso machines, there is a growing demand for cafe-style coffee at home. This trend highlights the focus on premium quality, especially in established markets like Europe and North America.

On the other hand, ready-to-drink(RTD) is expected to grow at a CAGR of 7.52% from 2026 to 2031, making it the fastest-growing segment in the coffee market. Ready-to-drink coffee, once seen merely as a quick caffeine fix, is now undergoing a premium transformation. With the introduction of sophisticated flavor profiles, cold brews, specialty-style recipes, and advanced brewing technologies, the taste and texture of RTD coffee have been significantly elevated. Urban youth, always on the move, are increasingly drawn to single-serve cans and bottles, especially those that are functional and health-oriented. They also favor offerings from convenience stores, underscoring a demand for portable coffee that seamlessly fits into their fast-paced lives. This shift underscores a growing appetite for barista-quality coffee in convenient formats, solidifying RTD coffee's position as a key growth driver in both emerging and established beverage markets.

Arabica remained the top choice in the global coffee market in 2025, holding 56.74% of the total share. Its smooth flavor and lower caffeine content make it popular among consumers who value quality. Grown in cooler, high-altitude regions, Arabica is widely used in specialty coffee and premium blends, especially in developed markets like North America, Europe, and Japan. Its popularity is further boosted by the rise in at-home brewing and the demand for single-origin and traceable coffee products, where flavor and quality are key.

While Arabica leads in value, Robusta is expected to grow the fastest among coffee types, with a CAGR of 5.98% through 2031. Known for its stronger, more bitter taste and higher caffeine content, Robusta is increasingly used in espresso blends, ready-to-drink coffee, and instant coffee due to its affordability and bold flavor. It is also more resistant to climate change and diseases, making it a preferred choice for producers in countries like Vietnam, Brazil, and parts of Africa. With improvements in processing and flavor, Robusta is gaining acceptance and expanding in both budget-friendly and innovative market segments.

Geography Analysis

North America accounted for 23.64% of the global coffee market revenue in 2025, driven by a strong cafe culture, the popularity of cold-brew coffee, and the widespread adoption of specialty coffee. The region has one of the highest per-capita coffee consumption rates globally, which supports higher pricing for premium products. Roasters in North America are also leading sustainability initiatives, such as partnering with farmers in Mexico for regenerative agriculture and providing adaptation loans to Colombian growers. These efforts are setting global standards for sustainable coffee production and supply chain practices. The region's focus on innovation and sustainability continues to shape the global coffee market landscape.

The Middle East and Africa are the fastest-growing regions in the coffee market, with a projected CAGR of 8.16% through 2031. Rising middle-class incomes and a young, urban population are accelerating coffee demand across the Middle East and Africa, where consumers are increasingly trading up from traditional formats to more premium cafe and at-home experiences. In the Gulf, cities such as Dubai, Riyadh, and Doha are seeing a proliferation of specialty cafes and international chains, blending long-standing coffee traditions with third-wave concepts and positioning the region as a showcase for experiential, design-led coffee spaces. African markets like Ethiopia, Nigeria, and South Africa are witnessing stronger domestic consumption, with a growing focus on locally sourced arabica, specialty roasteries, and capsule or pod systems that target affluent and aspirational drinkers. From limited-edition drinks in high-traffic malls to premium capsules in hospitality and office channels, the region's increasingly sophisticated coffee culture and evolving taste preferences are underpinning robust growth in both out-of-home and retail coffee segments.

Europe is playing a significant role in reshaping the global coffee market, particularly through its strict sustainability regulations. These regulations are pushing for greater traceability in coffee sourcing, which is becoming a standard expectation worldwide. Scandinavian countries are leading the way in adopting fair-trade coffee, while traditional markets like Italy and France are balancing their love for classic coffee with a growing interest in single-origin espressos. Latin America, as both a major producer and an emerging consumer market, is experiencing growth in domestic coffee consumption.

- Nestle SA

- UCC Ueshima Coffee Co.

- Starbucks Corporation

- The Kraft Heinz Company

- Luigi Lavazza S.p.A.

- Massimo Zanetti Beverage Group SpA

- The J. M. Smucker Company

- Tata Consumer Products

- Coava Coffee Roasters

- Tchibo GmbH

- Louis Dreyfus Company Coffee

- TGL Company

- Trung Nguyen Legend Group

- Mayora Group (Kopiko)

- The Coca-Cola Company

- Unilever PLC

- Zino Davidoff Group

- Sleepy Owl Coffee

- Bewley's Limited

- Strauss Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for specialty and premium coffee

- 4.2.2 Growing coffee culture among millennials and Gen Z

- 4.2.3 Booming RTD/cold-brew consumption

- 4.2.4 Sustainability and ethical sourcing awareness

- 4.2.5 Corporate and workplace coffee solutions

- 4.2.6 Influence of social media and influencer marketing

- 4.3 Market Restraints

- 4.3.1 Volatility in coffee bean prices

- 4.3.2 Tariffs and European union deforestation regulation barriers

- 4.3.3 Regulatory pressure and import/export restrictions

- 4.3.4 Consumer concerns over caffeine and health risks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Whole-bean

- 5.1.2 Ground Coffee

- 5.1.3 Instant Coffee

- 5.1.4 Ready-to-Drink (RTD)

- 5.1.5 Coffee Pod and Capsules

- 5.2 By Distribution Channel

- 5.2.1 On-trade

- 5.2.2 Off-trade

- 5.2.2.1 Supermarkets/Hypermarkets

- 5.2.2.2 Convenience Stores

- 5.2.2.3 Specialist Retailers

- 5.2.2.4 Online Retail

- 5.2.2.5 Other Off-trade Channels

- 5.3 By Coffee Species

- 5.3.1 Arabica

- 5.3.2 Robusta

- 5.3.3 Liberica

- 5.3.4 Others

- 5.4 By Origin

- 5.4.1 Single Origin/Specialty

- 5.4.2 Mixed

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Colombia

- 5.5.2.3 Argentina

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Indonesia

- 5.5.4.7 Vietnam

- 5.5.4.8 Malaysia

- 5.5.4.9 Singapore

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Egypt

- 5.5.5.6 Kuwait

- 5.5.5.7 Ethiopia

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nestle SA

- 6.4.2 UCC Ueshima Coffee Co.

- 6.4.3 Starbucks Corporation

- 6.4.4 The Kraft Heinz Company

- 6.4.5 Luigi Lavazza S.p.A.

- 6.4.6 Massimo Zanetti Beverage Group SpA

- 6.4.7 The J. M. Smucker Company

- 6.4.8 Tata Consumer Products

- 6.4.9 Coava Coffee Roasters

- 6.4.10 Tchibo GmbH

- 6.4.11 Louis Dreyfus Company Coffee

- 6.4.12 TGL Company

- 6.4.13 Trung Nguyen Legend Group

- 6.4.14 Mayora Group (Kopiko)

- 6.4.15 The Coca-Cola Company

- 6.4.16 Unilever PLC

- 6.4.17 Zino Davidoff Group

- 6.4.18 Sleepy Owl Coffee

- 6.4.19 Bewley's Limited

- 6.4.20 Strauss Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

2026-2034年全球餐飲服務業咖啡市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球餐飲服務業咖啡市場規模、佔有率、趨勢和成長分析報告 咖啡市場規模、佔有率和成長分析:按產品類型、咖啡品種、性質、烘焙程度、分銷管道、最終用戶和地區分類-2026-2033年產業預測

咖啡市場規模、佔有率和成長分析:按產品類型、咖啡品種、性質、烘焙程度、分銷管道、最終用戶和地區分類-2026-2033年產業預測 商用咖啡機市場規模、佔有率和成長分析:按容量、材質、應用、通路和地區分類-2026-2033年產業預測2026-2034年餐飲服務業咖啡市場規模、佔有率、成長、全球產業分析、區域趨勢及預測

商用咖啡機市場規模、佔有率和成長分析:按容量、材質、應用、通路和地區分類-2026-2033年產業預測2026-2034年餐飲服務業咖啡市場規模、佔有率、成長、全球產業分析、區域趨勢及預測 咖啡市場報告:趨勢、預測和競爭分析(至2035年)菊苣咖啡市場報告:趨勢、預測及競爭分析(至2035年)

咖啡市場報告:趨勢、預測和競爭分析(至2035年)菊苣咖啡市場報告:趨勢、預測及競爭分析(至2035年) 咖啡市場:依產品類型、通路和地區分類

咖啡市場:依產品類型、通路和地區分類 咖啡基個人護理市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、最終用途、通路、地區及競爭格局分類,2021-2031年)無菊苣咖啡市場-2026-2031年預測

咖啡基個人護理市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、最終用途、通路、地區及競爭格局分類,2021-2031年)無菊苣咖啡市場-2026-2031年預測 全球烘焙研磨市場

全球烘焙研磨市場