|

市場調查報告書

商品編碼

2065792

害蟲防治:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Insect Pest Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

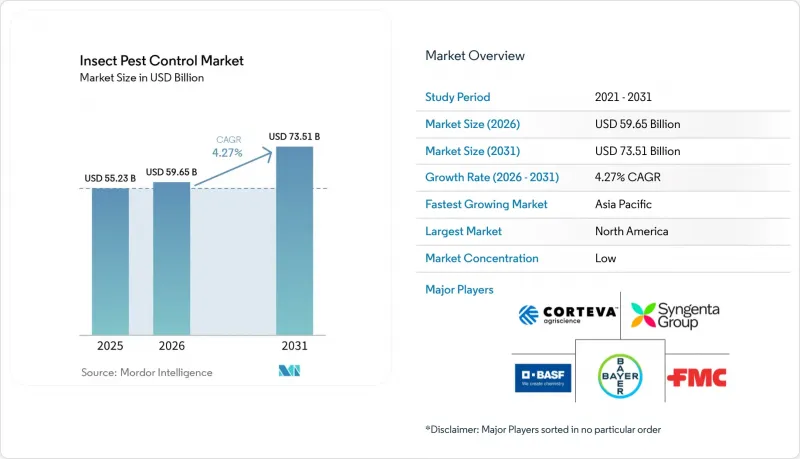

根據 Mordor Intelligence 預測,害蟲防治市場規模將從 2025 年的 552.3 億美元成長到 2026 年的 596.5 億美元,到 2031 年達到 735.1 億美元,2026 年至 2031 年的複合年成長率為 4.27%。

本報告按防治方法(化學、生物、物理)、作物類型(穀物、水果和蔬菜、油籽和豆類等)、施用方法(葉面噴布、種子處理、土壤處理等)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測(價值,美元)。

全球害蟲防治市場趨勢及洞察

病蟲害威脅加劇,作物減產風險增加

全球作物生產持續面臨病蟲害造成的產量損失的嚴峻壓力,這仍然是農業盈利面臨的最持久威脅之一。作物保護網預測,到2025年,無脊椎動物害蟲將在2024年使美國29個州的玉米產量下降4.0%,造成超過6.1億蒲式耳的損失。這顯示病蟲害對現代農業造成的經濟負擔依然沉重。由於產量管理仍是生產者盈利的關鍵,即使農場利潤微薄,也很難延後病蟲害防治的支出。此外,病蟲害防治市場正受惠於同一季節內防治多種害蟲的需求不斷成長,尤其是在病蟲害週期重複出現的作物中。這一趨勢推動了對各種病蟲害防治方案的需求成長,並有利於那些能夠在同一病蟲害防治市場中提供多種作用機制的供應商。

監管機構和零售商推廣低殘留物計劃

環境規制の強化や小売業者の基準の厳格化により、より選択性が高く残留量の少ない害虫防除プログラムへの移行が加速しています。米国環境保護庁(EPA)は2025年4月29日、「殺虫剤戦略」を最終決定しました。これは約8,300万エーカーの処理対象面積をカバーし、散布ドリフト防止のための緩衝地帯や流出水資源管理などの緩和措置を義務付けています。欧州では、農薬の使用や記録管理に対する監視が厳格化されており、農業実務におけるデジタル記録やトレーサビリティへの広範な移行を含め、コンプライアンスへの圧力は依然として高い水準にあります。これにより、総合的害虫管理(IPM)プログラムに適した製品の価値が高まり、生物農薬、フェロモン製剤、および選択性のある化学農薬の活躍の場が広がっています。したがって、害虫駆除市場では、コンプライアンスを軸としたプレミアムプログラムと、代替圧力がより強まっている汎用プログラムとの間に明確な二極化が見られます。

對傳統化學農藥的抗藥性

由於多種主要害蟲對傳統化學農藥的抗藥性日益增強,害蟲防治市場正面臨明顯的限制。巴登-符騰堡州發布的2026年官方綜合蟲害管理指南指出,德國萊茵平原和克賴希高地區的油菜甲蟲種群中出現了“超級KDR抗性”,建議種植者在這些高發地區使用替代活性成分。這增加了害蟲防治項目的成本,迫使種植者採用輪作、混合噴灑和新型活性成分,而不是低成本的重複噴灑。此外,現有產品的商業性有效期正在縮短,因此具有新型作用機制的產品(例如先正達集團IRAC 30類殺蟲劑)的重要性日益凸顯。因此,儘管害蟲防治市場持續成長,但傳統產品越來越難以維持穩定的銷售量和價格。

細分市場分析

2025年、化学的害虫駆除は害虫駆除市場シェアの67.5%を占め、依然として圧倒的な差で最大のセグメントとしての地位を維持しました。この地位は、広範囲の農地における長い実績、強力な流通網、そして穀物、綿花、油糧種子、種植作物にまたがる多くの複合害虫問題に対処できる能力を反映しています。また、害虫駆除業界における化学的害虫駆除は、新しい合成分子が依然として古い非專利系よりも高い価格を維持しているため、商業性的にも重要な位置を占め続けています。生物的防除は最も急成長しているセグメントであり、2026年から2031年にかけてCAGR6.3%を記録しています。これは、成長の軸が残留物管理や耐性ローテーションを中核とするプログラムへと移行していることを示しています。中国の2025年および2026年の技術計画は、生物的ローテーションに対する追加的な政策支援を提供し、それによって世界最大級の作物保護システムの一つにおける導入を強化しました。

拜耳公司透過與Ginkgo Bioworks公司建立新的多年合作關係,拓展了其生物農藥平台,並加速了用於害蟲防治和永續農業應用的微生物產品的開發。因此,害蟲防治市場不再簡單地區分化學農藥和生物農藥,許多種植者現在在同一季節的種植計畫中同時使用化學農藥和生物農藥。這種混合模式將使生物農藥在害蟲防治市場中成長最快的細分領域獲得更大的佔有率,同時維持化學農藥的使用規模。

區域分析

到2025年,北美將佔據害蟲防治市場37.6%的佔有率,成為最大的區域市場。該地區憑藉其成熟的綜合蟲害管理(IPM)體系、高品質化學農藥的高滲透率以及強大的生物農藥和種子處理劑開發平臺,佔據了有利地位。美國環保署(EPA)於2025年最終確定的農藥策略將推動精準噴灑和殘留減量計畫在約8,300萬英畝的已處理面積內實施。歐洲仍然是一個至關重要的高價值地區,該地區日益嚴格的法規和更嚴格的文件標準正在以超過總處理面積擴張速度的速度改變產品結構,並持續向選擇性化學農藥和生物防治方法轉型。

亞太地區是成長最快的區域市場,預計2026年至2031年複合年成長率將達到5.6%,並將繼續在未來的害蟲防治市場需求成長中發揮核心作用。中國是主要驅動力,其2025年和2026年主要作物病蟲害防治計畫正式納入了生物防治和輪作方案,預計水稻和玉米種植系統將出現大規模病蟲害爆發。此外,不斷成長的需求、政策支持的生物防治推廣以及種植密度的提高,共同為該地區創造了強勁的成長基礎。南美洲仍然是害蟲防治領域的潛在成長區域,巴西和阿根廷大豆和玉米種植面積的擴大導致每個種植季節的病蟲害防治週期增加。巴西國家糧食供應公司(CONAB)預測,2025/26年度大豆產量將達到創紀錄的1.801億噸,這將推動大規模種植系統中對毛蟲、椿象和吸汁昆蟲等害蟲防治方案的需求。此外,隨著害蟲抗藥性的增強,種植者擴大採用殺蟲劑輪換、種子處理和生物防治等方法。

儘管中東和非洲的害蟲防治市場規模仍然相對較小,但這兩個地區都蘊藏著巨大的成長潛力。海灣國家和土耳其保護性耕作的擴張,正在擴大生物防治和低殘留害蟲管理在蔬菜、觀賞植物和幼苗作物的應用範圍。在非洲,由於入侵害蟲持續肆虐,特別是對玉米和其他主糧作物的侵害,長期需求仍然強勁。安德瑪特非洲公司宣佈於2025年與Provivi公司建立合作夥伴關係,共同開發和推廣東非地區的新一代害蟲防治解決方案,這反映出小規模農戶對基於信息素的害蟲防治系統的商業性興趣日益濃厚。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 病蟲害威脅加劇,作物減產風險增加

- 監管機構和零售商推廣低殘留物計劃

- 生物防治和生物來源殺蟲劑的迅速推廣

- 精準勘測、無人機和人工智慧最佳化了害蟲防治的時機。

- 保護性栽培和育苗設施的擴張正在推高對生物防治的需求。

- 種子處理和抗蟲性狀的疊加

- 市場限制因素

- 對傳統化學品的抗性

- 活性成分登記及最大殘留限量壓力

- 暢銷殺蟲劑的一般化

- 生物製藥的保存期限和現場性能差異

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過害蟲防治方法

- 化學防治

- 生物防治

- 物理控制

- 按作物類型

- 穀物和穀類

- 水果和蔬菜

- 油籽/豆類

- 種植作物

- 草坪和觀賞植物

- 透過應用方法

- 葉面噴布

- 種子處理

- 土壤處理

- 化學

- 燻蒸和空間處理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Syngenta Group Co., Ltd.

- Bayer AG

- BASF SE

- Corteva, Inc.

- FMC Corporation

- UPL Limited

- Sumitomo Chemical Co., Ltd.

- Nufarm Limited

- Gowan Company, LLC

- AMVAC Chemical Corporation(American Vanguard Corporation(AVD))

- Pro Farm Group Inc

- Certis USA LLC

- Environmental Science US LLC

- Koppert Biological Systems BV

- Biobest Group NV

第7章 市場機會與未來展望

According to Mordor Intelligence, the insect pest control market size is anticipated to increase from USD 55.23 billion in 2025 to USD 59.65 billion in 2026 and reach USD 73.51 billion by 2031, growing at a CAGR of 4.27% over 2026-2031.

This report is Segmented by Control Method (Chemical, Biological, and Physical), by Crop Type (Grains and Cereals, Fruits and Vegetables, Oilseeds and Pulses, and More), by Mode of Application (Foliar Spray, Seed Treatment, Soil Treatment, and More), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). Market Forecasts in Value (USD).

Global Insect Pest Control Market Trends and Insights

Rising Insect Pressure and Crop-Loss Risk

Global crop production continues to face severe pressure from insect-driven yield losses, which remain one of the most persistent threats to farm profitability. In 2025, the Crop Protection Network anticipated that invertebrate pests reduced corn yields by 4.0% across 29 United States states during the 2024 season, resulting in losses exceeding 610 million bushels, demonstrating the continuing economic burden of insect infestations on modern agriculture. This keeps insect control spending hard to defer even when farm margins tighten, because yield protection remains central to grower economics. The insect pest control market also gains from the rising need to manage multiple pest species within the same season, especially in crops with repeated infestation cycles. That pattern supports a stronger demand for broad programs and favors suppliers that can offer several modes of action within the same insect pest control market.

Regulatory and Retailer Push for Lower-Residue Programs

Tighter environmental oversight and stricter retailer standards are accelerating the shift toward more selective and lower-residue insect control programs. The United States Environmental Protection Agency (EPA) finalized its Insecticide Strategy on April 29, 2025, covering nearly 83 million treated acres and requiring mitigation measures such as spray-drift buffers and runoff controls. In Europe, compliance pressure remains high as pesticide use and documentation receive closer scrutiny, including the broader shift toward digital recording and traceability in farm practices. This raises the value of products that fit integrated pest management (IPM) programs and creates more room for biologicals, pheromone tools, and selective chemistry. The insect pest control market, therefore, shows a clear split between premium programs built around compliance and commodity programs that face greater substitution pressure.

Resistance to Legacy Chemistries

The insect pest control market faces a clear limit due to rising resistance to older chemistries across several key pest complexes. The official 2026 integrated pest management guidance in Baden-Wurttemberg reported super-kdr resistance in oilseed rape flea beetle populations in the Rhine Plain and Kraichgau regions of Germany and advised growers to use alternative active ingredients in those hotspots. This raises program costs because growers need rotations, mixtures, and newer active ingredients instead of lower-cost repeat applications. It also shortens the commercially useful life of established products and increases the importance of novel modes of action, such as Syngenta Group's IRAC group 30 insecticides . The result is that the insect pest control market keeps growing, but legacy products within it face a harder path to stable volume and pricing.

Other drivers and restraints analyzed in the detailed report include:

- Fast Adoption of Biological Control and Bioinsecticides

- Precision Scouting, Drones, and AI Improve Treatment Timing

- Registration and MRL Pressure on Active Ingredients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical control accounted for 67.5% of the insect pest control market share in 2025, maintaining its position as the largest segment by a wide margin. This position reflects its long record in broad-acre crops, strong distribution coverage, and the ability to address many pest complexes across grains, cotton, oilseeds, and plantation crops. The chemical side of the insect pest control industry also remains commercially important because newer synthetic molecules still command higher pricing than older generic classes. Biological control is the fastest-growing segment, with a 6.3% CAGR during 2026-2031, indicating that growth is shifting toward programs built around residue management and resistance rotation. China's 2025 and 2026 technical plans provided additional policy support for biological rotations, thereby strengthening adoption in one of the world's largest crop protection systems.

Bayer AG expanded its biological crop protection platform through a new multi-year partnership with Ginkgo Bioworks to accelerate the development of microbial products for pest management and sustainable agriculture applications. The practical outcome is that the insect pest control market is no longer simply separating chemical and biological programs, because many growers now use both within the same seasonal plan. That mixed model should maintain the chemical scale while enabling biological products to capture a larger share of the fastest-growing segment of the insect pest control market.

Geography Analysis

North America accounted for 37.6% of the insect pest control market share in 2025, making it the largest regional segment. The region benefits from established integrated pest management systems, high adoption of premium chemistry, and a strong pipeline of biological and seed-applied products. The United States Environmental Protection Agency (EPA) final Insecticide Strategy in 2025 strengthened the case for precision-applied and lower-residue programs across nearly 83 million treated acres. Europe remains an important high-value region where regulatory attrition and more stringent documentation standards are changing the product mix faster than the total treated area, supporting continued substitution toward selective chemistry and biological tools.

Asia-Pacific is the fastest-growing regional segment, with a 5.6% CAGR during 2026-2031, and remains central to future demand expansion in the insect pest control market. China is a major driver because its 2025 and 2026 major crop pest plans formalized biological control plus rotation programs, and projected very large pest incidence across rice and corn systems. This gives the region a strong mix of volume demand, policy-backed biological adoption, and rising crop intensity. South America remains a potential growth region for insect pest control due to the expansion of soybean and corn acreage in Brazil and Argentina, which has increased the number of insect treatment cycles required per season. Brazil's National Supply Company (CONAB) has projected a record soybean harvest for the 2025/26 season of 180.1 million metric tons, driving demand for caterpillar, stink bug, and sucking-pest control programs in large-scale row-crop systems. Additionally, pest resistance is prompting growers to adopt rotational insecticide programs, seed treatments, and biological insect-control solutions.

The Middle East and Africa remain smaller in absolute terms, but both offer significant growth opportunities in the insect pest control market. Protected cultivation in Gulf countries and Turkey is widening the addressable base for biological and low-residue insect management in vegetables, ornamentals, and nursery crops. Africa has strong long-term demand because invasive pest pressure remains high, particularly in maize and other staple crops. Andermatt Africa announced a 2025 partnership with Provivi to develop and distribute next-generation pest control solutions in East Africa, which signals rising commercial interest in pheromone-based systems for smallholder agriculture.

- Syngenta Group Co., Ltd.

- Bayer AG

- BASF SE

- Corteva, Inc.

- FMC Corporation

- UPL Limited

- Sumitomo Chemical Co., Ltd.

- Nufarm Limited

- Gowan Company, L.L.C.

- AMVAC Chemical Corporation (American Vanguard Corporation (AVD))

- Pro Farm Group Inc

- Certis USA L.L.C.

- Environmental Science U.S. LLC

- Koppert Biological Systems B.V.

- Biobest Group NV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising insect pressure and crop-loss risk

- 4.2.2 Regulatory and retailer push for lower-residue programs

- 4.2.3 Fast adoption of biological control and bioinsecticides

- 4.2.4 Precision scouting, drones, and AI improve treatment timing

- 4.2.5 Protected-crop and nursery expansion lifts biocontrol demand

- 4.2.6 Seed-treatment and insect-protection trait stacking

- 4.3 Market Restraints

- 4.3.1 Resistance to legacy chemistries

- 4.3.2 Registration and MRL pressure on active ingredients

- 4.3.3 Generic erosion of blockbuster insecticides

- 4.3.4 Shelf-life and field-performance variability in biologicals

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of new entrants

- 4.6.2 Bargaining power of buyers

- 4.6.3 Bargaining power of suppliers

- 4.6.4 Threat of substitutes

- 4.6.5 Intensity of competitive rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Control Method

- 5.1.1 Chemical Control

- 5.1.2 Biological Control

- 5.1.3 Physical Control

- 5.2 By Crop Type

- 5.2.1 Grains and Cereals

- 5.2.2 Fruits and Vegetables

- 5.2.3 Oilseeds and Pulses

- 5.2.4 Plantation Crops

- 5.2.5 Turf and Ornamentals

- 5.3 By Mode of Application

- 5.3.1 Foliar Spray

- 5.3.2 Seed Treatment

- 5.3.3 Soil Treatment

- 5.3.4 Chemigation

- 5.3.5 Fumigation and Space Treatment

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta Group Co., Ltd.

- 6.4.2 Bayer AG

- 6.4.3 BASF SE

- 6.4.4 Corteva, Inc.

- 6.4.5 FMC Corporation

- 6.4.6 UPL Limited

- 6.4.7 Sumitomo Chemical Co., Ltd.

- 6.4.8 Nufarm Limited

- 6.4.9 Gowan Company, L.L.C.

- 6.4.10 AMVAC Chemical Corporation (American Vanguard Corporation (AVD))

- 6.4.11 Pro Farm Group Inc

- 6.4.12 Certis USA L.L.C.

- 6.4.13 Environmental Science U.S. LLC

- 6.4.14 Koppert Biological Systems B.V.

- 6.4.15 Biobest Group NV

7 Market Opportunities and Future Outlook

害蟲防治服務市場-全球市場預測(2026-2032年)害蟲防治市場-全球市場預測(2026-2032年)害蟲防治市場:2026-2032年全球市場預測(依害蟲類型、處理方法、服務類型、產品類型、應用方法、製劑形式、最終用途和分銷管道分類)

害蟲防治服務市場-全球市場預測(2026-2032年)害蟲防治市場-全球市場預測(2026-2032年)害蟲防治市場:2026-2032年全球市場預測(依害蟲類型、處理方法、服務類型、產品類型、應用方法、製劑形式、最終用途和分銷管道分類) 害蟲防治市場報告:按類型、害蟲種類、應用和地區分類(2026-2034 年)

害蟲防治市場報告:按類型、害蟲種類、應用和地區分類(2026-2034 年) 害蟲防治產品和服務市場:依產品類型、應用、最終用戶、服務類型和地區分類。

害蟲防治產品和服務市場:依產品類型、應用、最終用戶、服務類型和地區分類。 人工智慧害蟲檢測市場預測至2034年—按作物類型、組件、部署模式、技術、應用、最終用戶和地區分類的全球分析

人工智慧害蟲檢測市場預測至2034年—按作物類型、組件、部署模式、技術、應用、最終用戶和地區分類的全球分析 Acephate全球市場規模、佔有率、趨勢和成長分析報告,2026-2034年

Acephate全球市場規模、佔有率、趨勢和成長分析報告,2026-2034年 2026年全球害蟲防治及滅鼠服務市場報告2026年全球建築害蟲防治服務市場報告Acephate市場:依作物類型、劑型、應用方法和銷售管道分類-2026-2032年全球市場預測

2026年全球害蟲防治及滅鼠服務市場報告2026年全球建築害蟲防治服務市場報告Acephate市場:依作物類型、劑型、應用方法和銷售管道分類-2026-2032年全球市場預測