|

市場調查報告書

商品編碼

2065774

合法攔截:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Lawful Interception - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

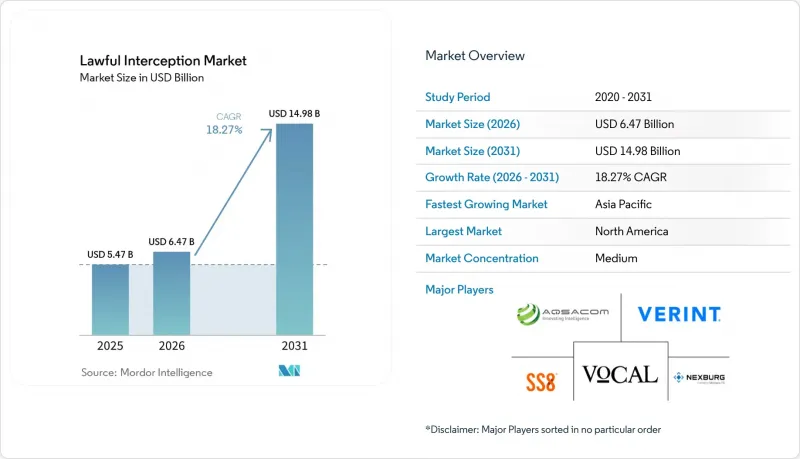

根據 Mordor Intelligence 預測,合法攔截市場規模將從 2025 年的 54.7 億美元成長到 2026 年的 64.7 億美元,然後在 2031 年達到 149.8 億美元,2026 年至 2031 年的複合年成長率為 18.27%。

本報告按組件(解決方案和服務)、網路(固定網路、行動網路、IP網路)、通訊管道(語音通訊、資料通訊等)、最終用戶(政府和執法機關等)、部署模式(本地部署、雲端/託管LI即服務)和地區細分。市場預測以美元計價。

全球合法攔截市場的趨勢與洞察

網路威脅日益加劇,國家安全問題也日益突出。

地緣政治緊張局勢和國家主導的網路行動正在推動全部區域攔截預算的增加。美國國防部2024年對中國網路戰態勢的評估強調了對能夠同時進行多通路監控的先進攔截基地的迫切需求。 MITRE公司2024年12月發布的一份關於無所不在的技術監控的評估報告指出,人工智慧驅動的分析可以將原始攔截數據轉化為可操作的洞察,迫使各機構升級其攔截能力,超越語音攔截的範疇。如今,快速偵測有組織的威脅模式依賴於跨5G網路、衛星鏈路和加密通訊的即時關聯分析。因此,提供整合分析套件而非孤立探測器的供應商正在獲得競爭優勢。國家級採購項目,尤其是在美國、英國、澳洲和日本,持續推動這項根本需求。

監理義務和合規要求

世界各國政府正在加強法律體制,要求通訊業者和數位平台提供合法的存取能力。歐盟擬議的2024年兩用物項出口管制修正案要求對監控工具進行更嚴格的實質審查,這使得擁有完善合規流程文件的供應商更具優勢。印度的《電訊法》草案和國家網路協調中心(NCCC)2024年發布的5G攔截規範提供了詳細的技術藍圖,指導本地通訊業者採用經過驗證的符合3GPP標準的解決方案。金融機構現在被要求將攔截記錄與FinCEN的跨境資金追蹤義務保持一致,這導致企業在合規監控方面的支出增加。由於監管機構將3GPP TS 33.106/107作為架構指南,參與標準化委員會的供應商的解決方案正在加速普及。

隱私權和資料保護法引發強烈反彈

對公民自由的訴求和嚴格的資料保護法律正在阻礙監控工具的廣泛應用,尤其是在歐洲和北美。歐洲資料保護委員會於2025年2月發布的關於人工智慧隱私風險的指南呼籲演算法透明化和資料最小化,提高了人工智慧驅動的攔截中全面資料收集的標準。各成員國之間法規的差異迫使通訊業者維護不同的合規流程,增加了成本。倡導團體持續就演算法偏見和大規模監控提起訴訟,敦促供應商實施選擇性目標定位和強大的監控儀錶板。同時,OTT平台預設的端對端加密設定限制了攔截範圍,加劇了關於特殊存取義務的政策辯論。

細分市場分析

到2025年,解決方案將佔合法攔截市場的67.20%,這主要得益於對中間設備、攔截網路基地台和分析平台的需求成長。然而,隨著通訊業者和企業將整合、合規性和生命週期支援外包,服務領域預計將以18.62%的複合年成長率成長。將3GPP規格轉化為可執行部署計畫的諮詢服務仍然需求旺盛,尤其是在5G切片帶來的架構複雜性日益增加的情況下。對於缺乏全天候保全人員的小規模通訊業者而言,託管攔截服務極具吸引力。在眾多解決方案領域中,攔截管理軟體的成長速度最快。這主要歸功於分析加密有效載荷的AI模組日益成長的分析價值。解密引擎和行為附加元件插件與核心偵測器相輔相成,能夠實現主動異常警報。中間設備面臨來自軟體定義替代方案的商品化壓力,但在傳統的電路交換領域仍發揮重要作用。因此,合法攔截市場正在向整合硬體抽象化和雲端編配的平台轉變。

法規的快速變化進一步提升了服務的價值。諮詢團隊透過出口管制評估和隱私影響審計通訊業者提供支持,以最大限度地降低合規風險。持續整合支援確保探針韌體符合每季發布的 3GPP 標準。培訓服務使負責人能夠有效利用 AI 儀表板,從而縮短獲得洞察的平均時間。隨著多租戶雲端的普及,供應商正在擴展其 DevSecOps 解決方案,以實現補丁和檢驗的自動化。因此,儘管解決方案仍是主流,但來自專業服務和託管服務的持續收入正日益穩定合法攔截市場中供應商的收入結構。

到2025年,行動基礎設施將佔合法攔截市場規模的50.60%,反映了GSM、UMTS和LTE等成熟監控基礎設施的現狀。然而,隨著VoIP、VoLTE和OTT流量的出現,通訊正向分組域轉移,IP網路的複合年成長率(CAGR)也高達19.05%。分組域能夠釋放豐富的元資料,使執法部門能夠繪製出窄頻語音無法取得的社交關係圖和行為模式。 5G獨立組網環境中的網路切片技術正在創建繞過傳統核心探測的虛擬子網,從而刺激了對邊緣部署攔截能力的需求。能夠將用戶平面探測與高吞吐量資料包仲介整合的供應商正在獲得一級營運商的廣泛認可。

固定網路領域保持穩定,但隨著銅纜線路的加速退役,其規模正在緩慢萎縮。混合 VoLTE 的引入模糊了行動網路和 IP 網路之間的界限,需要跨 RAN、核心網路和 IMS 域進行整合攔截編配。 NEC 基於 SS8 的跨太平洋合法攔截合規認證清楚地展示了透過海底線路進行跨洋資料包攔截的要求。在行動領域,3G/4G 網路仍然佔據探測流量的大部分,但 5G 流量呈指數級成長,迫使供應商在不封包遺失下實現 100 Gbps 的捕獲速率。因此,投資正轉向可擴展的虛擬化 IP 攔截框架,以應對未來快速成長的加密流量。

區域分析

2025年,北美將繼續佔據合法監聽市場38.85%的佔有率,這得益於聯邦政府的資金支持、成熟的通訊基礎設施以及塑造全球標準的供應商生態系統。美國政府機構不斷完善《執法機關通訊援助法案》(CALEA)的條款,這推動了國內對升級版監聽設備的需求。在地緣政治審查日益嚴格的情況下,加拿大對5G供應鏈的安全審計使得通訊業者獲得監聽合規認證的迫切性日益凸顯。人工智慧研究領域的區域領先地位正在加速高階分析模組的部署,從而形成創新和採購的良性循環。勒索軟體和國家支持的駭客攻擊事件的增加,促使預算撥款持續投入,並確保平台的穩定更新。

預計到2031年,亞太地區的複合年成長率將達到19.36%,成為所有地區中成長最快的地區。 5G的快速部署需要針對網路切片和邊緣雲端的攔截機制,而這些要求已由印度的國家通訊業者正在採用雲端託管探測技術以避免巨額資本投資,這與該地區的數位轉型策略相契合。中國不斷擴大的網路戰戰略迫使鄰國加強國內監控能力,從而增加了對人工智慧驅動的分析技術的需求。然而,該地區法律體系的多樣性要求供應商為每個司法管轄區量身訂做合規方案。

在歐洲,隱私和安全要求錯綜複雜地交織在一起。歐盟委員會高層小組建議對不合作的OTT服務提供者實施制裁,這凸顯了監管方向強調通訊可追溯性。然而,GDPR要求將資料最小化並限制合法用途,這增加了實施的複雜性。由於各成員國的法規各不相同,通訊業者通常需要並行維護多個中間閘道器,以適應不同的本地介面切換格式。因此,擁有豐富法律庫的成熟供應商具有競爭優勢。同時,在拉丁美洲、中東和非洲,市場仍在發展中,但前景看好。這些地區的通訊業者通常使用雲端服務來平衡攔截方面的投資與持續的基礎設施建設,並避免大規模的本地硬體投資。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 網路威脅日益加劇,國家安全問題也日益突出。

- 監理義務和合規要求

- 基於網際網路協定 (IP) 和 5G 通訊的普及

- 遷移到基於雲端的攔截平台

- 利用人工智慧 (AI) 進行即時元資料分析的投資報酬率 (ROI)

- 數位證據可採納性框架

- 市場限制因素

- 隱私權和資料保護法引發強烈反彈

- 建置多網路高成本且複雜

- 廠商鎖定限制了互通性。

- 針對Over-The-Top應用的「預設加密」策略

- 價值鏈分析

- 監管情勢與政府應對措施

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 調解裝置

- 攔截網路基地台

- 攔截管理軟體

- 解密和分析模組

- 服務

- 諮詢

- 整合與部署

- 支援與維護

- 解決方案

- 網路

- 固定通訊網路

- 公共交換電話網路(PSTN)

- 寬頻

- 行動網路

- 世界行動通訊系統(GSM)

- 通用封包無線服務 (GPRS)

- 3G/4G/LTE

- 5G 和未來無線接取網路(RAN)

- IP網路

- 網際網路協定語音通訊(VoIP)

- 監控數據流量

- 固定通訊網路

- 透過通訊管道

- 語音通訊

- 資料通訊

- 社群媒體和OTT通訊

- 最終用戶

- 政府和執法機關

- 情報機構

- 公司

- 部署模式

- 現場

- 基於雲端/主機的 LI 即服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Verint Systems Inc.

- SS8 Networks, Inc.

- Nexburg GmbH

- Trovicor GmbH

- BAE Systems plc

- Gamma Group

- Elbit Systems Ltd.

- IPS SpA

- Aqsacom Inc.

- Vocal Technologies Ltd.

- Ericsson AB

- Nokia Corp.

- Huawei Technologies Co. Ltd.

- Cisco Systems, Inc.

- Rohde and Schwarz GmbH

- Group 2000

- NetQuest Corp.

- NICE Ltd.

- Thales Group

- Palantir Technologies Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the lawful interception market size is expected to grow from USD 5.47 billion in 2025 to USD 6.47 billion in 2026 and is forecast to reach USD 14.98 billion by 2031 at 18.27% CAGR over 2026-2031.

This report is Segmented by Component (Solution and Services), Network (Fixed Networks, Mobile Networks, and IP Networks), Communication Channel (Voice Communication, Data Communication, and More), End-User (Government and Law-Enforcement Agencies, and More), Deployment Mode (On-Premise, and Cloud/Hosted LI-As-A-Service), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Lawful Interception Market Trends and Insights

Rising Cyber-Threats and National Security Concerns

Geopolitical tensions and state-sponsored cyber operations are elevating interception budgets across North America, Europe, and Asia-Pacific. The U.S. Department of Defense's 2024 assessment of China's cyber-warfare posture underscores the urgency for advanced listening posts capable of simultaneous multi-channel surveillance. MITRE's December 2024 review of ubiquitous technical surveillance argues that AI-enabled analytics convert raw intercepts into actionable intelligence, driving agencies to upgrade beyond voice taps. Rapid detection of coordinated threat patterns now hinges on real-time correlation across 5G slices, satellite links, and encrypted messaging. Vendors offering integrated analytics suites rather than siloed probes therefore gain competitive traction. National-level procurement programs, particularly in the United States, United Kingdom, Australia, and Japan, continue to drive baseline demand.

Regulatory Mandates and Compliance Requirements

Governments worldwide are tightening legal frameworks that oblige telecom operators and digital platforms to furnish lawful-access capabilities. The EU's 2024 dual-use export-control update demands enhanced due diligence for surveillance tools, favoring vendors with mature compliance documentation. India's draft Telecommunication Bill and its 2024 National Cyber Coordination Centre (NCCC) specifications for 5G interception codify detailed technical blueprints, steering local carriers toward tested 3GPP-conformant solutions. Financial institutions must now align interception records with FinCEN's cross-border funds tracing obligations, expanding enterprise spending on compliance monitoring. As regulators reference 3GPP TS 33.106/107 for architectural guidance, vendors embedded in standards committees enjoy accelerated adoption.

Privacy-Rights Backlash and Data-Protection Laws

Civil-liberties pressure and stringent data-protection statutes temper the adoption of expansive surveillance tools, particularly in Europe and North America. The European Data Protection Board's February 2025 guidance on AI privacy risks calls for algorithmic transparency and data minimisation, raising hurdles for blanket data collection in AI-enhanced interception. Fragmented Member-State rules compel carriers to maintain disparate compliance workflows, adding cost. Advocacy groups continue to litigate algorithmic bias and mass-surveillance claims, forcing vendors to introduce selective targeting and robust oversight dashboards. In parallel, end-to-end encryption defaults on OTT platforms limit interception scope, intensifying the policy debate on exceptional-access mandates.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of IP-Based and 5G Communications

- Shift Toward Cloud-Hosted Interception Platforms

- High Cost and Complexity of Multi-Network Build-Out

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 67.20% of the lawful interception market share in 2025, underpinned by demand for mediation devices, interception access points, and analytics platforms. However, the services segment is projected to rise at a 18.62% CAGR as carriers and enterprises outsource integration, regulatory mapping, and lifecycle support. Consulting engagements that translate 3GPP specifications into actionable deployment blueprints remain in high demand, especially as 5G slicing adds architectural nuance. Managed interception services appeal to smaller operators lacking round-the-clock security staff. Within solutions, interception-management software enjoys the highest velocity because AI modules that parse encrypted payloads drive analytic value. Decryption engines and behavioural-analysis add-ons complement core probes, enabling proactive anomaly alerts. Mediation devices face commoditisation pressure from software-defined alternatives, yet they retain importance for legacy circuit-switched domains. The lawful interception market thus tilts toward platforms that bundle hardware abstraction with cloud-ready orchestration.

Rapid regulatory churn further elevates service value. Advisory teams guide carriers through export-control assessments and privacy-impact audits, minimising compliance risk. Continuous-integration support ensures that probe firmware aligns with quarterly 3GPP releases. Training services equip investigators to exploit AI dashboards, shortening mean-time-to-insight. As multi-tenant cloud deployments proliferate, vendors expand DevSecOps offerings to automate patching and verification. Consequently, although solutions remain dominant, recurring-revenue streams from professional and managed services increasingly stabilise vendor revenue profiles in the lawful interception market.

Mobile infrastructure held 50.60% of the lawful interception market size in 2025, reflecting entrenched GSM, UMTS, and LTE monitoring foundations. Yet IP networks are advancing at a 19.05% CAGR because VoIP, VoLTE, and OTT traffic shift communications toward packet domains. Packet orientation unlocks metadata richness, allowing agencies to map social graphs and behavioural patterns unavailable in narrowband voice. Network slicing under 5G standalone creates virtual sub-nets that bypass legacy core probes, prompting demand for edge-resident intercept functions. Vendors able to merge user-plane probes with high-throughput packet brokers capture mindshare among tier-one carriers.

The fixed-network segment remains stable but slides slowly as copper retirements accelerate. Hybrid VoLTE deployments blur mobile and IP boundaries, forcing unified interception orchestration across RAN, core, and IMS domains. NEC's certification of trans-Pacific lawful-intercept compliance with SS8 illustrates cross-ocean packet-intercept requirements for submarine routes. Within the mobile category, 3G/4G networks still generate majority probe volumes, but 5G traffic grows exponentially, pushing vendors to engineer 100 Gbps capture rates without packet loss. Consequently, investment tilts toward scalable, virtualised IP-intercept frameworks that future-proof carriers against surging encrypted traffic.

Geography Analysis

North America retained 38.85% of the lawful interception market size in 2025, supported by federal funding, mature telecom infrastructure, and vendor ecosystems that shape global standards. U.S. agencies continue to refine Communications Assistance for Law Enforcement Act provisions, bolstering domestic demand for upgraded probes. Canada's 5G supply-chain security reviews add urgency for carriers to certify interception compliance amid geopolitical scrutiny. Regional leadership in AI research accelerates the adoption of advanced analytics modules, feeding virtuous cycles of innovation and procurement. Heightened ransomware and state-sponsored hacking incidents sustain budget allocations, ensuring steady platform refreshes.

Asia-Pacific is projected to post the fastest regional CAGR at 19.36% through 2031. Rapid 5G roll-outs require intercept mechanisms for network slices and edge clouds, tasks codified by India's NCCC technical framework. Australia, Japan, and South Korea apply stringent critical-infrastructure rules, spurring proactive system upgrades. Meanwhile, Southeast Asian operators embrace cloud-hosted probes to avoid heavy capex, aligning with regional digital-transformation agendas. China's expanding cyber-warfare doctrine is prompting neighbouring states to harden domestic surveillance capabilities, reinforcing demand for AI-driven analytics. The region, however, presents heterogeneous legal regimes, compelling vendors to tailor compliance packs per jurisdiction.

Europe exhibits a complex interplay of privacy safeguards and security imperatives. The European Commission's High-Level Group recommendation to sanction non-cooperative OTT providers spotlights a regulatory tilt toward traceable communications. Yet GDPR obligations mandate data minimisation and lawful-purpose constraints, increasing deployment complexity. Fragmented member-state regulations mean that carriers often must maintain parallel mediation gateways to accommodate differing LI handover formats. Established vendors with extensive legal libraries, therefore, gain a competitive advantage. Elsewhere, Latin America, the Middle East, and Africa remain nascent yet promising; operators there balance interception investments against ongoing infrastructure build-outs, often turning to cloud services that circumvent heavy local hardware outlays.

- Verint Systems Inc.

- SS8 Networks, Inc.

- Nexburg GmbH

- Trovicor GmbH

- BAE Systems plc

- Gamma Group

- Elbit Systems Ltd.

- IPS S.p.A.

- Aqsacom Inc.

- Vocal Technologies Ltd.

- Ericsson AB

- Nokia Corp.

- Huawei Technologies Co. Ltd.

- Cisco Systems, Inc.

- Rohde and Schwarz GmbH

- Group 2000

- NetQuest Corp.

- NICE Ltd.

- Thales Group

- Palantir Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising cyber-threats and national security concerns

- 4.2.2 Regulatory mandates and compliance requirements

- 4.2.3 Proliferation of Internet Protocol (IP)-based and 5G communications

- 4.2.4 Shift toward cloud-hosted interception platforms

- 4.2.5 Artificial Intelligence (AI)-driven real-time metadata analytics Return on Investment (ROI)

- 4.2.6 Digital-evidence admissibility frameworks

- 4.3 Market Restraints

- 4.3.1 Privacy-rights backlash and data-protection laws

- 4.3.2 High cost and complexity of multi-network build-out

- 4.3.3 Vendor lock-in limits interoperability

- 4.3.4 "Encryption-by-default" policies in Over-The-Top (OTT) apps

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape and Government Initiatives

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.1.1 Mediation devices

- 5.1.1.2 Interception access points

- 5.1.1.3 Interception management software

- 5.1.1.4 Decryption and analytics modules

- 5.1.2 Services

- 5.1.2.1 Consulting

- 5.1.2.2 Integration and deployment

- 5.1.2.3 Support and maintenance

- 5.1.1 Solution

- 5.2 By Network

- 5.2.1 Fixed networks

- 5.2.1.1 Public Switched Telephone Network (PSTN)

- 5.2.1.2 Broadband

- 5.2.2 Mobile networks

- 5.2.2.1 Global System for Mobile Communications (GSM)

- 5.2.2.2 General Packet Radio Service (GPRS)

- 5.2.2.3 3G/4G/LTE

- 5.2.2.4 5G and future Radio Access Network (RAN)

- 5.2.3 IP networks

- 5.2.3.1 Voice over Internet Protocol (VoIP)

- 5.2.3.2 Data-traffic monitoring

- 5.2.1 Fixed networks

- 5.3 By Communication Channel

- 5.3.1 Voice communication

- 5.3.2 Data communication

- 5.3.3 Social media and OTT messaging

- 5.4 By End-User

- 5.4.1 Government and Law-Enforcement Agencies

- 5.4.2 Intelligence agencies

- 5.4.3 Enterprises

- 5.5 By Deployment Mode

- 5.5.1 On-premise

- 5.5.2 Cloud/Hosted LI-as-a-Service

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verint Systems Inc.

- 6.4.2 SS8 Networks, Inc.

- 6.4.3 Nexburg GmbH

- 6.4.4 Trovicor GmbH

- 6.4.5 BAE Systems plc

- 6.4.6 Gamma Group

- 6.4.7 Elbit Systems Ltd.

- 6.4.8 IPS S.p.A.

- 6.4.9 Aqsacom Inc.

- 6.4.10 Vocal Technologies Ltd.

- 6.4.11 Ericsson AB

- 6.4.12 Nokia Corp.

- 6.4.13 Huawei Technologies Co. Ltd.

- 6.4.14 Cisco Systems, Inc.

- 6.4.15 Rohde and Schwarz GmbH

- 6.4.16 Group 2000

- 6.4.17 NetQuest Corp.

- 6.4.18 NICE Ltd.

- 6.4.19 Thales Group

- 6.4.20 Palantir Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

合法監聽市場:按組件、通訊類型、網路類型、最終用途、國家和地區分類-全球產業分析、市場規模及佔有率和未來預測(2026-2033 年)

合法監聽市場:按組件、通訊類型、網路類型、最終用途、國家和地區分類-全球產業分析、市場規模及佔有率和未來預測(2026-2033 年) 合法攔截市場規模、佔有率、趨勢和預測:按網路技術、設備、通訊內容、服務、最終用戶和地區分類,2026-2034 年

合法攔截市場規模、佔有率、趨勢和預測:按網路技術、設備、通訊內容、服務、最終用戶和地區分類,2026-2034 年 2026年全球合法攔截市場報告

2026年全球合法攔截市場報告 合法攔截市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案、模式

合法攔截市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案、模式 全球合法攔截市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本合法攔截市場報告(按網路技術、設備、通訊內容、服務、最終用戶和地區分類,2026-2034年)

全球合法攔截市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本合法攔截市場報告(按網路技術、設備、通訊內容、服務、最終用戶和地區分類,2026-2034年) 合法攔截市場規模、佔有率和成長分析(按組件、網路、網路技術、通訊內容和地區分類)-2026-2033年產業預測

合法攔截市場規模、佔有率和成長分析(按組件、網路、網路技術、通訊內容和地區分類)-2026-2033年產業預測 合法攔截市場按組件、技術、最終用戶、部署類型、應用程式和組織規模分類 - 全球預測,2025 年至 2032 年

合法攔截市場按組件、技術、最終用戶、部署類型、應用程式和組織規模分類 - 全球預測,2025 年至 2032 年 合法攔截市場-全球產業規模、佔有率、趨勢、機會和預測(按網路、按中介設備、按最終用戶、按地區和競爭細分,2020-2030 年預測)

合法攔截市場-全球產業規模、佔有率、趨勢、機會和預測(按網路、按中介設備、按最終用戶、按地區和競爭細分,2020-2030 年預測) 合法攔截市場規模、佔有率、趨勢分析報告:按解決方案、網路技術、通訊技術、最終用途、地區、細分預測,2025-2030 年

合法攔截市場規模、佔有率、趨勢分析報告:按解決方案、網路技術、通訊技術、最終用途、地區、細分預測,2025-2030 年