|

市場調查報告書

商品編碼

2065759

硬體安全模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Hardware Security Modules - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

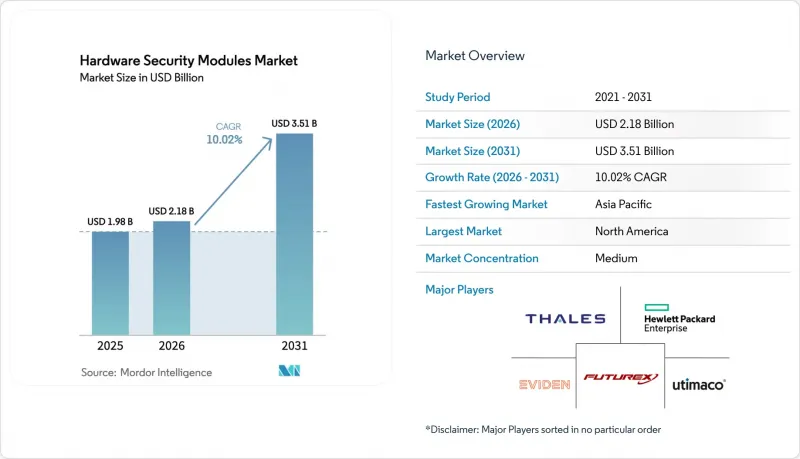

根據 Mordor Intelligence 預測,硬體安全模組 (HSM) 市場預計將從 2025 年的 19.8 億美元成長到 2026 年的 21.8 億美元,到 2031 年達到 35.1 億美元,2026 年至 2031 年的複合年成長率預計為 10.02%。

本報告按部署類型(本地部署、雲端 HSM、混合 HSM)、類型(通用型、支付型、雲端/託管型等)、應用領域(支付處理、金鑰管理等)、最終用戶(銀行、金融服務和保險 (BFSI)、政府機構、醫療保健等)和地區進行細分。市場預測以美元 (USD) 為單位。

全球硬體安全模組市場趨勢及洞察

遵守後量子密碼技術的最後期限正在加速硬體安全模組 (HSM) 的更新換代。

美國國家標準與技術研究院 (NIST) 於 2024 年最終確定了三種後量子演算法,這觸發了聯邦機構和受監管行業的強制過渡。目前,各公司正在維護雙重加密協定堆疊,以在過渡期間支援 ML-KEM、ML-DSA 和 SLH-DSA,這導致處理負載翻倍,並加快了設備更新週期。美國國家安全局 (NSA) 的「商業國家安全演算法套件 2.0」強制要求在 2035 年前為關鍵任務系統採用抗量子攻擊的原語,進一步縮短了規劃時間。 2024 年 4 月,泰雷茲 Luna 成為首款獲得 FIPS 140-3 3 級認證的硬體安全模組 (HSM),讓早期採用者在採購上具有優勢。 「先收集後解密」的威脅模式使情況更加緊迫,尤其對於那些必須保證數十年機密性的組織而言更是如此。

超超大規模資料中心業者推動了雲端原生金鑰管理的蓬勃發展

Google雲端、微軟Azure和AWS現已將FIPS認證的硬體整合到其多租戶環境中,使客戶能夠在滿足國內資料居住需求的同時,使用自有金鑰。 Marvell的LiquidSecurity闆卡每秒可實現100萬次操作,滿足超大規模資料中心業者資料中心的吞吐量目標。新加坡的《個人資料保護法》(PDPA)和日本的網路安全指南等國家框架要求部署在地化實例,從而推動了區域容量的擴張。印尼Krom銀行等金融服務業的新興企業正在利用託管式雲端HSM加速推出數位銀行服務,同時保持其在加密管理領域的主導。這些應用正在顯著擴大亞太地區的HSM市場。

符合 FIPS 140-3 標準的晶片供不應求

由於只有少數晶圓代工廠能夠生產符合 FIPS 140-3 測試向量的安全處理器,半導體產能依然緊張。 SK 海力士和美光已售罄 2025 年大部分時間的高頻寬記憶體 (HSM) 配額,迫使 HSM 製造商限制供應並提高價格。認證流程包括冗長的清零和防篡改檢驗,這導致新晶片的流片延遲,並增加了對現有供應商的依賴。因此,小規模的新參與企業面臨更長的前置作業時間,HSM 市場的經濟格局也向那些預先獲得晶圓安全認證的供應商傾斜。

細分市場分析

到2025年,本地部署設備仍將佔據硬體安全模組 (HSM) 市場71.85%的佔有率,這主要得益於國防、銀行和關鍵基礎設施營運商對直接金鑰管理的需求。許多公司為了滿足有關主權資料的監管要求,將「信任根」維護在自己的資料中心內。然而,隨著超大規模資料中心業者大規模資料中心供應商保證FIPS認證、可用性SLA和API優先訪問,雲端HSM訂閱量正以10.62%的複合年成長率成長。這種混合模式正在擴大HSM市場規模,因為企業在轉型期通常會採用雙重部署模式。

託管服務正吸引先前依賴軟體金鑰庫的新創公司和中型銀行,因為它們可以降低資本投資和續約風險。邊緣運算新增了一層,有助於建立分散式叢集,集中同步策略,並在 5G 邊界強制執行本地加密。供應商正透過提供基於容器的連接器來回應這項需求,使 DevSecOps 團隊能夠從 Kubernetes Pod 呼叫硬體服務。在整個預測期內,支出將轉向訂閱模式,儘管大規模受監管工作負載仍將保留在私有機架中。第二代部署策略正在將 HSM 功能整合到微型資料中心,以支援智慧工廠用例、聯網汽車更新簽章和城市公共安全網路。

預計到2025年,能夠在單一底盤內處理PKI根保護、代碼簽署、令牌化和資料庫加密的通用單元將佔總收入的59.45%。其演算法的柔軟性使其成為向後量子密碼學過渡的關鍵,而後量子密碼學在漫長的過渡期內需要RSA/ECC和基於格的原語。同時,雲端託管產品正以10.74%的複合年成長率成長,這得益於超大規模資料中心業者的付費使用制模式和統一的區域部署。儘管支付終端在PCI DSS標準下仍然必不可少,但供應商正在將支付和通用韌體整合到共用電路板上,以在晶片供應受限的情況下最佳化庫存。

容器化插件將 PKCS#11 呼叫轉換為 REST 介面,使開發人員無需學習底層驅動程式即可從微服務請求安全金鑰操作。專用於密封 AI 模型的晶片正在湧現,Fortanix 將敏感運算區域和 HSM編配整合在一起,以保護靜態和推理狀態下的機器學習資產。

區域分析

預計到2025年,北美將佔據全球硬體安全模組(HSM)市場佔有率的37.10%,這主要得益於FIPS 140-3標準的早期採用、聯邦機構層面的量子安全防護指南,以及支付處理商每三年更新一次設備的高密度集中度。持續的公共部門現代化津貼和總統關於零信任的法令維持了穩定的採購管道。加拿大正透過財政部的現代化和開放銀行監管的製定來效仿北美的做法,而在墨西哥,隨著金融科技公司接入CoDi和SPEI等高速支付網路,市場正在加速發展,從而推動了對低成本雲HSM閘道器的需求成長。

預計到2031年,亞太地區將維持12.17%的最高年複合成長率(CAGR),這主要得益於超大規模資料中心業者資料中心的建設以及需要主權金鑰系統的數位銀行牌照的發放。中國的MLPS 2.0強制要求使用國產演算法,這就要求部署能夠並行運行SM2和NIST曲線的雙棧設備。日本汽車製造商正在整合嵌入式IP以符合聯網汽車的網路安全法規,而印度的資料本地化政策正促使銀行使用託管在AWS孟買和GCP德里區域的特定區域金鑰庫。東協市場正在引入可互通的即時結算,這促使區域銀行採用共用HSM工具,從而在不影響合規性的前提下降低單筆交易成本。

歐洲仍是受MiCA、GDPR和PSD2等法規影響的戰略階段。隨著工廠採用基於5G的OPC-UA技術,德國的中型企業(Mittelstands)正在投資建造本地叢集以保護智慧財產權。英國脫歐後,重點關注關鍵數據分類方面的差異,這導致客製化設備認證的需求增加。在法國,以「SecNumCloud」為標籤的雲端優先政策正在擴展,該政策仍然要求在經過認證的硬體中使用根密鑰。包括立陶宛在內的東歐金融科技中心正在部署多租戶HSM網路,以吸引使用通行證計畫的加密資產服務供應商。儘管名義GDP成長放緩,但所有這些措施共同推動了整個歐洲大陸硬體安全模組(HSM)市場的擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 後量子密碼技術合規的最後期限正在加速硬體安全模組(HSM)的更新。

- 亞太地區超大規模資料中心業者雲端原生金鑰管理蓬勃發展

- 即時支付網路正在推動 HSM 在支付領域的應用。

- MiCA 對加密貨幣託管的監管正在推動歐盟對 FIPS HSM 的需求。

- UNECE R155 汽車應用法規正在推動嵌入式HSM IP 的採用。

- 多租戶 HSM 即服務的商業化

- 市場限制因素

- 符合 FIPS 140-3 標準的晶片供不應求

- 從傳統PKI遷移到雲端的複雜性

- 安全儲存設備價格飆升,給中小企業造成了沉重打擊。

- 跨國加密貨幣法律的零碎化(例如,中國的《貨幣監管與保護法》2.0版)

- 價值供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- 投資分析

第5章 市場規模與成長預測

- 依部署類型

- 現場

- Cloud HSM

- 混合 HSM

- 按類型

- 通用高速同步模組

- HSM支付

- 基於雲端/主機的HSM(HSM-aaS)

- USB/可攜式HSM

- 基於 PCIe 的 HSM

- 網路連線型 HSM

- 透過使用

- 支付處理

- 金鑰管理和KMS

- SSL/TLS 和程式碼簽名

- PKI 和憑證授權單位

- 區塊鏈和加密貨幣託管

- 資料庫和文檔加密

- 物聯網/邊緣設備 ID

- 後量子密碼加速

- 按最終用戶行業分類

- BFSI

- 政府/國防

- 醫療保健和生命科學

- 零售與電子商務

- 通訊/IT

- 工業和製造業

- 能源公用事業

- 雲端服務供應商

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 澳洲

- 紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- GCC

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Thales Group

- Utimaco Management Services GmbH

- Entrust Corporation

- IBM Corporation

- Hewlett Packard Enterprise(HPE)

- Eviden SAD(Atos Group)

- Futurex

- Amazon Web Services(AWS)

- Microsoft Azure Dedicated HSM

- Yubico

- Securosys SA

- Swissbit AG

- Secunet Security Networks AG

- Infineon Technologies AG

- Marvell Technology Inc.

- Fortanix Inc.

- Microchip Technology Inc.

- Broadcom Inc.

- Crypto4A Technologies

- Nitrokey GmbH

- nCipher(nShield)

- Rambus

第7章 市場機會與未來展望

According to Mordor Intelligence, the hardware security modules market size is expected to increase from USD 1.98 billion in 2025 to USD 2.18 billion in 2026 and reach USD 3.51 billion by 2031, growing at a CAGR of 10.02% over 2026-2031.

This report is Segmented by Deployment Type (On-Premise, Cloud HSM, Hybrid HSM), Type (General Purpose, Payment, Cloud/Hosted, and More), Application (Payment Processing, Key Management, and More), End-User (BFSI, Government, Healthcare, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Hardware Security Modules Market Trends and Insights

Post-quantum compliance deadlines accelerating HSM refresh

NIST finalized three post-quantum algorithms in 2024, triggering mandatory migrations across federal agencies and regulated industries. Enterprises now maintain dual cryptographic stacks to support ML-KEM, ML-DSA and SLH-DSA during transition periods, which doubles processing loads and precipitates accelerated appliance refresh cycles. The NSA's Commercial National Security Algorithm Suite 2.0 obliges mission-critical systems to adopt quantum-resistant primitives well before 2035, compressing planning horizons. Thales Luna became the first FIPS 140-3 Level 3 certified HSM in April 2024, giving early adopters a procurement advantage. "Harvest now, decrypt later" threat models further reinforce urgency, particularly for entities that must guarantee multi-decade confidentiality.

Hyperscaler cloud-native key-management boom

Google Cloud, Microsoft Azure and AWS now embed FIPS-validated hardware in multitenant locations, enabling customers to bring their own keys while satisfying domestic data-residency rules. Marvell's LiquidSecurity boards deliver 1 million operations per second to meet hyperscaler throughput targets. National frameworks such as Singapore's PDPA and Japan's cybersecurity guidelines require localized instances, stimulating region-specific capacity roll-outs. Financial-services newcomers like Indonesia's Krom Bank leverage managed CloudHSM to accelerate digital-banking launches while retaining cryptographic control. These deployments substantially expand the HSM market in APAC.

Scarcity of FIPS 140-3 chips

Semiconductor capacity remains constrained because only a handful of foundries can fabricate secure processors that meet FIPS 140-3 test vectors. SK Hynix and Micron have sold out high bandwidth memory allocations through most of 2025, forcing HSM makers to ration supply and raise prices. Certification introduces lengthy zeroization and tamper-response validations, slowing new tape-outs and reinforcing dependence on incumbent suppliers. Smaller entrants therefore face extended lead times, tipping HSM market economics toward vendors with pre-reserved wafers.

Other drivers and restraints analyzed in the detailed report include:

- Instant-payment rails fuelling payment HSM uptake

- Crypto-custody MiCA rules driving EU demand for FIPS HSMs

- Legacy PKI-to-cloud migration complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise appliances retained 71.85% of Hardware Security Modules market share in 2025 due to direct control over keys required by defense, banking and critical-infrastructure operators. Many firms keep root-of-trust inside data centers to satisfy sovereign data mandates. Nevertheless, cloud HSM subscriptions are scaling at a 10.62% CAGR as hyperscalers guarantee FIPS validations, availability SLAs and API-first consumption. This hybrid approach enlarges the HSM market size because organizations often run dual footprints during transitional years.

Managed offerings reduce capital outlay and refresh risk, attracting startups and mid-tier banks that previously relied on software keystores. Edge computing adds another layer, prompting distributed clusters that enforce local encryption at the 5G boundary while synchronizing policies centrally. Vendors address this by shipping container-based connectors so DevSecOps teams can call hardware services from Kubernetes pods. Over the forecast period, spending tilts toward subscription models even as sizeable regulated workloads remain locked inside private racks. Second-generation deployment strategies now bundle HSM functionality into micro-data-centers that support smart-factory use cases, connected-vehicle update signing and city-wide public-safety networks.

General-purpose units captured 59.45% of revenue in 2025 because they handle PKI root protection, code signing, tokenization and database encryption in a single chassis. Their algorithm agility makes them indispensable for post-quantum migrations that demand both RSA/ECC and lattice-based primitives during a prolonged overlap period. Meanwhile, cloud-hosted variants demonstrate an 10.74% CAGR, supported by hyperscaler pay-per-use economics and uniform regional roll-outs. Payment-class boxes remain essential for PCI DSS, yet vendors are embedding payment and general-purpose firmware on shared boards to optimize inventory under chip constraints.

Containerized plugins translate PKCS#11 calls into REST interfaces, letting builders request secure key operations from micro-services without learning low-level drivers. Specialized silicon for AI model sealing has emerged, as Fortanix integrates confidential-computing enclaves with HSM orchestration to protect machine learning assets at rest and in inference.

Geography Analysis

North America held 37.10% of global Hardware Security Modules market share in 2025 thanks to early FIPS 140-3 adoption, quantum-safe directives across federal agencies and a dense cluster of payment processors that refresh devices on three-year cycles. Ongoing public-sector modernization grants and zero-trust executive orders sustain steady procurement pipelines. Canada follows suit with treasury modernization and open-banking rulemaking, while Mexico shows emerging acceleration as fintechs connect to CoDi and SPEI fast-payment rails, demanding lower-cost cloud HSM gateways.

Asia Pacific exhibits the highest 12.17% CAGR through 2031, buoyed by hyperscaler data-center construction and digital-banking licenses that require sovereign key regimes. China's MLPS 2.0 imposes domestic algorithm usage, compelling dual-stack appliances capable of operating SM2 alongside NIST curves. Japan's automakers integrate embedded IP to comply with connected-vehicle cybersecurity provisions, and India's data-localization policies steer banks toward region-specific key vaults hosted on AWS Mumbai and GCP Delhi zones. ASEAN markets implement interoperable real-time payments, prompting regional banks to adopt shared-service HSM utilities that cut per-transaction costs without sacrificing compliance.

Europe remains a strategic arena shaped by MiCA, GDPR and PSD2. Germany's industrial Mittelstand invests in on-premise clusters to secure IP as factories adopt OPC-UA over 5G. The United Kingdom focuses on post-Brexit divergence in critical-data classifications, driving bespoke appliance certifications. France expands cloud-first mandates under the SecNumCloud label, which still requires root keys inside qualified hardware. Eastern European fintech hubs, notably Lithuania, deploy multi-tenant HSM grids to attract passporting crypto-service providers. Collectively these measures lift the Hardware Security Modules market size across the continent despite slower headline GDP growth.

- Thales Group

- Utimaco Management Services GmbH

- Entrust Corporation

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Eviden SAD (Atos Group)

- Futurex

- Amazon Web Services (AWS)

- Microsoft Azure Dedicated HSM

- Yubico

- Securosys SA

- Swissbit AG

- Secunet Security Networks AG

- Infineon Technologies AG

- Marvell Technology Inc.

- Fortanix Inc.

- Microchip Technology Inc.

- Broadcom Inc.

- Crypto4A Technologies

- Nitrokey GmbH

- nCipher (nShield)

- Rambus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-quantum compliance deadlines accelerating HSM refresh

- 4.2.2 Hyperscaler cloud-native key-management boom in APAC

- 4.2.3 Instant-payment rails fuelling payment HSM uptake

- 4.2.4 Crypto-custody MiCA rules driving EU demand for FIPS HSMs

- 4.2.5 Automotive UNECE R155 mandate pushing embedded HSM IP

- 4.2.6 Multi-tenant HSM-as-a-Service monetisation

- 4.3 Market Restraints

- 4.3.1 Scarcity of FIPS 140-3 chips

- 4.3.2 Legacy PKI-to-cloud migration complexity

- 4.3.3 Secure-memory price spikes hitting SMBs

- 4.3.4 Cross-border crypto-law fragmentation (e.g., China MLPS 2.0)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-Premise

- 5.1.2 Cloud HSM

- 5.1.3 Hybrid HSM

- 5.2 By Type

- 5.2.1 General Purpose HSM

- 5.2.2 Payment HSM

- 5.2.3 Cloud/Hosted HSM (HSM-aaS)

- 5.2.4 USB/Portable HSM

- 5.2.5 PCIe-based HSM

- 5.2.6 Network-attached HSM

- 5.3 By Application

- 5.3.1 Payment Processing

- 5.3.2 Key Management and KMS

- 5.3.3 SSL/TLS and Code-Signing

- 5.3.4 PKI and Certificate Authorities

- 5.3.5 Blockchain and Cryptocurrency Custody

- 5.3.6 Database and Document Encryption

- 5.3.7 IoT/Edge Device Identity

- 5.3.8 Post-Quantum Crypto Acceleration

- 5.4 By End-User Vertical

- 5.4.1 BFSI

- 5.4.2 Government and Defense

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Telecommunications and IT

- 5.4.6 Industrial and Manufacturing

- 5.4.7 Energy and Utilities

- 5.4.8 Cloud Service Providers

- 5.4.9 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia

- 5.5.4.7 New Zealand

- 5.5.4.8 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Thales Group

- 6.4.2 Utimaco Management Services GmbH

- 6.4.3 Entrust Corporation

- 6.4.4 IBM Corporation

- 6.4.5 Hewlett Packard Enterprise (HPE)

- 6.4.6 Eviden SAD (Atos Group)

- 6.4.7 Futurex

- 6.4.8 Amazon Web Services (AWS)

- 6.4.9 Microsoft Azure Dedicated HSM

- 6.4.10 Yubico

- 6.4.11 Securosys SA

- 6.4.12 Swissbit AG

- 6.4.13 Secunet Security Networks AG

- 6.4.14 Infineon Technologies AG

- 6.4.15 Marvell Technology Inc.

- 6.4.16 Fortanix Inc.

- 6.4.17 Microchip Technology Inc.

- 6.4.18 Broadcom Inc.

- 6.4.19 Crypto4A Technologies

- 6.4.20 Nitrokey GmbH

- 6.4.21 nCipher (nShield)

- 6.4.22 Rambus

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球硬體安全模組市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球硬體安全模組市場:市場規模、佔有率、趨勢和成長分析(2026-2034) HSM供應商:認證狀態與PQC合規狀態硬體安全模組硬體安全模組市場數據概覽:2026年第二季度

HSM供應商:認證狀態與PQC合規狀態硬體安全模組硬體安全模組市場數據概覽:2026年第二季度 硬體安全模組市場規模、佔有率和趨勢分析報告:按類型、部署模式、應用、最終用途、地區和細分市場預測(2026-2033 年)

硬體安全模組市場規模、佔有率和趨勢分析報告:按類型、部署模式、應用、最終用途、地區和細分市場預測(2026-2033 年) 硬體安全模組市場:依組織規模、部署類型、組件和應用分類-2026-2032年全球市場預測

硬體安全模組市場:依組織規模、部署類型、組件和應用分類-2026-2032年全球市場預測 2026年量子安全硬體安全模組全球市場報告2026年全球硬體安全模組市場報告

2026年量子安全硬體安全模組全球市場報告2026年全球硬體安全模組市場報告 硬體安全模組市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、外形、部署類型、最終用戶及功能分類

硬體安全模組市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、外形、部署類型、最終用戶及功能分類 汽車硬體安全模組 (HSM) 市場規模、佔有率及預測(依 HSM 類型(專用晶片、整合)、安全等級、加密演算法和 OEM 採用情況劃分)—全球預測至 2036 年

汽車硬體安全模組 (HSM) 市場規模、佔有率及預測(依 HSM 類型(專用晶片、整合)、安全等級、加密演算法和 OEM 採用情況劃分)—全球預測至 2036 年