|

市場調查報告書

商品編碼

2065739

汽車雷達:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Radar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

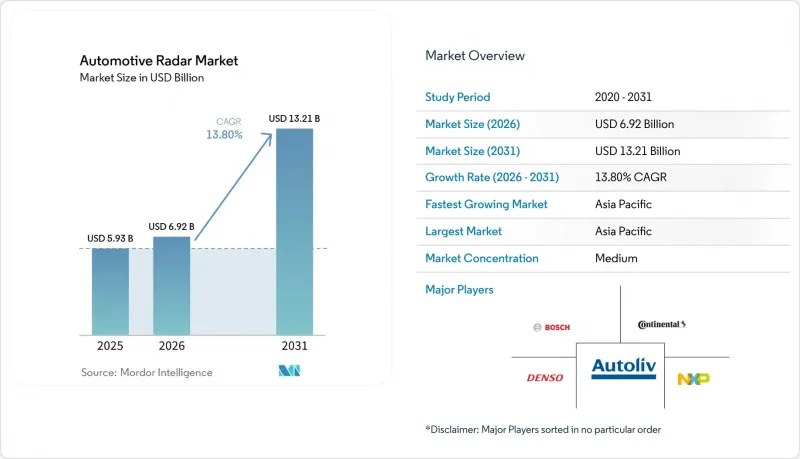

根據 Mordor Intelligence 預測,汽車雷達市場規模將從 2025 年的 59.3 億美元成長到 2026 年的 69.2 億美元,然後在 2031 年達到 132.1 億美元,2026 年至 2031 年的複合年成長率為 13.8%。

本報告依偵測範圍(短、中、長)、頻段(24 GHz、77 GHz 及其他)、應用(主動式車距維持定速系統、自動駕駛等)、車輛類型(乘用車、輕型商用車等)、驅動系統(內燃機車輛等)、銷售管道(OEM 原廠配套等)及地區進行細分。市場預測以美元計價。

全球汽車雷達市場趨勢與洞察

嚴格的NCAP和UNECE安全標準

歐洲新車安全評估協會 (Euro NCAP) 2025 年協議強制要求車輛配備兒童碰撞偵測和前向碰撞緩解系統,因此安裝雷達是獲得五星評級的必要條件。歐盟法規 2019/2206 將此要求擴展至所有新車,自 2024 年 9 月起生效,這將直接影響車輛採購決策和保險費計算。中國工業和資訊化部已宣佈到 2028 年強制實施自動緊急煞車系統 (AEB),隨著國內品牌開始領先安裝感測器,預計 77 GHz 頻段的訂單量將大幅成長。由於歐洲、北美和亞太地區的部署進度不同,需求呈分階段發展,這有望幫助汽車雷達市場避免週期性低迷。因此,一級供應商正在提前建立庫存,以應對監管要求的實施,而不是等待整車製造商 (OEM) 的直接交付。

77 GHz頻段成本主導小型化浪潮

從 24 GHz 到 77 GHz 的升級使模組尺寸縮小了約 60%,並將探測範圍擴大了一倍,達到 250 公尺。這使得感測器可以隱藏在保險桿飾板後面,而無需對設計做出任何妥協。德克薩斯(TI) 計畫於 2025 年發布的 AWR2944P 整合了硬體加速器和擴展內存,將分離式 DSP 和微控制器整合到單一晶片上。恩智浦 (NXP) 的 S32R47 支援 192 單元虛擬陣列,能夠以量產成本實現 4D 點雲。晶圓級整合、矽鍺製程和晶片分割技術預計將使平均售價從 2024 年的 85 美元降至 2025 年的 72 美元,並隨著中國晶圓廠產能的提升,到 2028 年達到 55 美元。價格的下降將使入門級產品也能配備高階雷達功能,加速感測器數量的成長,並提振汽車雷達市場的整體需求。

高成本多感測器融合系統

一套擁有超過100 TOPS人工智慧處理能力的集中式感知系統,將使每輛車的成本增加800至1200美元,這對於大眾市場汽車品牌來說難以承受。支撐這些系統的核心是英偉達Thor液冷計算模組,這需要重新設計封裝和散熱路徑,從而增加了物料清單(BOM)的成本壓力,尤其是在價格敏感的亞太地區。雖然中國供應商生產的計算模組價格比西方同行低40%至50%,但短期成本負擔限制了入門車型可選配雷達功能,並暫時限制了車輛的銷售數量。一級供應商被迫在銷售單一模組和進行完整的感測器融合整合之間做出選擇,這種權衡正在影響其盈利能力以及盈利。到本世紀末,由於 5nm 製程節點和晶片加速器,計算成本預計將減半,但 2026 年至 2028 年仍將是大規模普及的瓶頸時期。

細分市場分析

預計到 2025 年,短程雷達的銷售額將佔總銷售額的 44.64%,到 2031 年將以 13.92% 的複合年成長率成長。中程設備支援橫向交通偵測和交叉路口監控,而遠端設備仍然是主動式車距維持定速系統的基礎,但由於中國產能的擴大,正面臨價格壓力。

目前,角落安裝的感測器兼具廣角覆蓋和90米的探測範圍,單一感測器即可完成泊車、盲點檢測和車道變換等任務。 60 GHz乘員偵測模組正在形成一個全新的超短距離雷達細分市場,隨著歐洲新車安全評鑑協會(Euro NCAP)車載安全標準的日益普及,預計該市場將迅速成長。矽鍺前端成本的降低使得汽車製造商能夠在不超出其配置等級價格目標的情況下,整合4到6個短距離雷達單元。泊車、盲點偵測和後方交叉路口警示等功能的需求整合,確保了短距離雷達在2031年之前將保持穩定的成長動能。

2025年,77 GHz頻段的銷售額佔總銷售額的62.77%,但隨著79 GHz成像解決方案的出現,其成長速度將會放緩,預計到2031年,79 GHz成像解決方案的複合年成長率將達到13.86%。監管機構已凍結24 GHz頻段的新核准,這將導致舊設備過時,並收緊供應商在77 GHz和79 GHz頻段的藍圖。

一級供應商已宣布推出77-81 GHz頻段的系統晶片(SoC),這些晶片整合了深度學習加速技術,可從現有天線設計中挖掘更高的角度解析度。雖然高階車型和純電動車 (BEV) 平台採用79 GHz頻段,利用4 GHz掃描頻寬獲取高解析度點雲數據,但大眾市場車型仍使用77 GHz頻段以降低成本。在擁擠區域共用頻率的挑戰增加了工程難度,但專有的干擾抑制協議堆疊可確保性能符合歐洲新車安全評估協會 (Euro NCAP) 的限值。雙頻段藍圖使汽車製造商能夠分階段進行投資,並保留其77 GHz生產線的剩餘模具價值。

區域分析

亞太地區是成長最快的需求中心,預計到2025年將佔汽車雷達市場收入的38.48%,並在2031年之前以14.53%的複合年成長率成長。中國是推動這一成長的主要力量。為滿足2028年強制自動緊急煞車(AEB)的要求,中國國內供應商如程泰和華為正在提高77GHz和79GHz模組的產量;同時,汽車製造商(OEM)正在中端車型中標準化6感測器套件,以保持與歐美競爭對手的功能競爭力。在日本和韓國,雷達在豪華車中的應用率很高,電裝、日立Astemo和Nidec Elesys等公司大量出口雷達模組,但隨著國內市場接近飽和,成長速度正在放緩。儘管到2025年,印度的雷達普及率仍將低於10%,但印度公路運輸和高速公路部正在考慮在2027年至2028年間引入自動緊急煞車系統,這為預測期後半段區域出貨量的成長創造了潛在空間。雖然東南亞市場的監管執法力度不足,但加裝盲點監測系統的保險費折扣正在刺激泰國、印尼和越南的售後市場需求。在澳洲和紐西蘭,雷達的搭載率與西歐持平,因為長途高速公路的安全要求優先考慮遠端主動式車距維持定速系統模組。在全部區域,規模經濟正在降低平均售價,使得汽車雷達市場即使在出貨量增加的情況下也能保持獲利。

到2025年,歐洲將佔全球銷售量的約28%。這得歸功於歐洲新車安全評估協會(Euro NCAP)嚴格的評級標準,該標準強制要求所有力爭獲得五星評級的車輛必須安裝前向碰撞預警雷達、盲點監測雷達和車載兒童探測雷達。雖然高階品牌正在採用79 GHz 4D成像解決方案以提升辨識精度,從而脫穎而出,但大眾製造商仍依賴成本最佳化的77 GHz角部感測器來滿足法規要求。大陸集團2025年雷達累積產量達2億台,訂單額達15億歐元(17億美元),顯示歐洲正發揮設計檢驗中心和一級供應商大規模生產基地的雙重作用。東歐的代工組裝正在提高模組產量,以滿足德國、法國和義大利原始設備製造商(OEM)的需求,這些製造商正在採用近岸外包策略來降低物流風險。儘管27個成員國之間的監管協調確保了需求的一致性,但在法蘭克福和巴黎等交通繁忙的走廊,79 GHz頻寬的堵塞狀況需要加大干擾抑制方面的投入,從而推高了系統總成本。預計到2026年,電池式電動車(BEV)的註冊量將超過新車銷量的30%,而歐洲純電動車平台平均配備5-6個感測器,即使內燃機汽車銷量下降,其成長預計仍將持續。因此,歐洲仍然是軟體定義雷達升級和無線性能增強的關鍵市場。

預計到2025年,北美將佔全球銷量的約24%,其成長動能得益於美國國家公路交通安全管理局(NHTSA)強制實施的自動緊急煞車(AEB)法規,以及通用汽車的UltraCruise和福特的BlueCruise等免手持高速公路駕駛輔助系統的商業化應用。皮卡和全尺寸SUV配備了3-4個遠端感測器,用於拖車輔助和車道居中保持。儘管其出貨量低於緊湊型乘用車,但這推高了每輛車零件的價值。加拿大遵循美國的相關法規,而墨西哥則專注於為美國市場組裝出口導向的雷達車輛。預計到2025年,南美洲和中東及非洲地區的總銷量將不足10%。雷達技術的應用主要集中在車隊和商業領域,因為這些領域可以透過減少工作週期和降低保險費用來抵消初始硬體成本。巴西和沙烏地阿拉伯的政府安全計畫可能會從2027年起加速汽車雷達技術的普及,但標準不統一和供應商分佈有限限制了短期銷售成長。整體而言,地域多元化正在減輕區域政策變化對汽車雷達市場規模的影響,從而維持成熟市場和新興市場之間的成長平衡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 嚴格的NCAP和UNECE安全標準

- 77 GHz頻段成本主導小型化浪潮

- 2級以上自動駕駛技術在大眾市場的廣泛應用。

- 電動車架構,預留了安裝額外感測器的空間

- 新興的4D成像雷達可確保視覺系統的冗餘性

- 基於晶片組的雷達SoC帶來的改裝市場

- 市場限制因素

- 多感測器融合系統高成本

- 主要區域79 GHz頻寬壅塞狀況

- 傳統千兆乙太網路骨幹網路的熱瓶頸

- SiGe/GaAs晶圓供應受限

- 價值鏈分析

- 監理情勢

- 技術展望(傳統技術 vs. 4D 技術 vs. 影像技術)

- 波特五力模型

第5章 市場規模與成長預測

- 按範圍

- 短程雷達(SRR)

- 中程雷達(MRR)

- 遠程雷達(LRR)

- 按頻段

- 24 GHz

- 77 GHz

- 79 GHz 或更高

- 透過使用

- 主動式車距維持定速系統(ACC)

- 自動緊急煞車(AEB)

- 盲點/後方交叉路口

- 乘客狀況和司機監控

- 自動駕駛(L3+)

- 停車輔助和自動停車

- 車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 無人計程車及自動駕駛班車

- 透過推進力

- 內燃機車

- 電池式電動車

- 油電混合車

- 按銷售管道

- OEM 原廠設備

- 改裝

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Continental AG

- DENSO Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Texas Instruments Inc.

- HELLA GmbH and Co. KGaA

- NXP Semiconductors NV

- Infineon Technologies AG

- Analog Devices Inc.

- Magna International Inc.

- Autoliv Inc.

- Veoneer Safety Systems

- Renesas Electronics Corp.

- STMicroelectronics NV

- Valeo SA

- Arbe Robotics Ltd.

- Vayyar Imaging Ltd.

- Indie Semiconductor

- Uhnder Inc.

- Smartmicro GmbH

- Smart Radar System Inc.

- Hitachi Astemo Ltd.

- Nidec Elesys Corp.

- Lunewave Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the automotive radar market size is expected to grow from USD 5.93 billion in 2025 to USD 6.92 billion in 2026 and is forecast to reach USD 13.21 billion by 2031 at a 13.8% CAGR over 2026-2031.

This report is Segmented by Range (Short-Range, Mid-Range, and Long-Range), Frequency Band (24 GHz, 77 GHz, and More), Application (Adaptive Cruise Control, Autonomous Driving, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Propulsion (Internal Combustion Vehicles, and More), Sales Channel (OEM-Fitted, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Radar Market Trends and Insights

Stringent NCAP and UNECE Safety Mandates

Euro NCAP's 2025 protocol forces in-cabin child-presence detection and forward-collision mitigation, making radar mandatory for five-star ratings. The European Union Regulation 2019/2206 extends the requirement across all new vehicle types from September 2024, directly influencing fleet-procurement decisions and insurance pricing. China's Ministry of Industry and Information Technology has announced automatic emergency braking mandates for 2028, creating a pipeline of high-volume 77 GHz orders as domestic brands pre-load sensors. Differences in rollout cadence between Europe, North America and Asia-Pacific stage demand in sequential waves, helping the automotive radar market avoid cyclical slumps. Tier-1 suppliers are therefore stockpiling front-end inventory in anticipation of mandate triggers, rather than awaiting direct pull from original equipment manufacturers.

77 GHz Cost-Driven Miniaturisation Wave

Migrating from 24 GHz to 77 GHz has cut module footprints by around 60% and doubled detection range to 250 m, allowing sensors to hide behind bumper fascias without stylistic compromise. Texas Instruments' 2025 AWR2944P integrates a hardware accelerator and expanded memory, collapsing discrete DSPs and microcontrollers into one die. NXP's S32R47 adds support for 192-element virtual arrays that enable 4D point clouds at mass-market cost. Wafer-scale integration, silicon-germanium processes, and chiplet partitioning drive the average selling price from USD 85 in 2024 to USD 72 in 2025, with forecasts at USD 55 by 2028 as Chinese fabs ramp volume. Lower prices open premium radar functions to entry-level trims, accelerating sensor count and fueling overall automotive radar market demand.

High Multi-Sensor Fusion System Cost

Centralized perception stacks capable of 100+ TOPS artificial intelligence add USD 800-1,200 per vehicle, a premium mass-market brands cannot easily absorb. Liquid-cooled Nvidia Thor compute modules underpin these systems and force design changes in packaging and thermal paths, raising bill-of-material pressure, especially on price-sensitive Asia-Pacific trims. While Chinese suppliers produce compute at a 40-50% discount to Western peers, the near-term burden limits optional radar functions on entry-models and caps immediate addressable volume. Tier-1s must choose between selling standalone modules or taking on full sensor-fusion integration, a trade-off that impacts margin retention and automotive radar market profitability. By the decade's end, 5 nm nodes and chiplet accelerators promise to halve compute costs, but the 2026-2028 window remains a drag on mass uptake.

Other drivers and restraints analyzed in the detailed report include:

- Mass-Market Level-2+ Autonomy Adoption

- EV Architecture Headroom for Additional Sensors

- Spectrum Congestion at 79 GHz in Key Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Short-range radar captured 44.64% of 2025 revenue and is projected to advance at a 13.92% CAGR through 2031. Medium-range devices support cross-traffic detection and intersection monitoring, while long-range units remain the baseline for adaptive cruise control but face price pressure from expanding Chinese capacity.

Corner installations now combine wide-angle coverage with 90 m reach, enabling a single sensor to handle parking, blind-spot and lane-change tasks. Occupancy-monitoring modules at 60 GHz form a nascent ultra-short-range slice that will scale quickly as Euro NCAP in-cabin rules spread. Cost erosion in silicon-germanium front ends lets automakers deploy four to six short-range units without breaching trim-level price targets. Consolidated demand across parking, blind-spot and rear-cross-traffic functions secures a stable growth runway for short-range radar through 2031.

The 77 GHz band held 62.77% of 2025 revenue but its growth moderates as 79 GHz imaging solutions rise at a 13.86% CAGR through 2031. Regulators have frozen new 24 GHz approvals, pushing legacy units toward obsolescence and tightening supplier roadmaps around 77 GHz and 79 GHz.

Tier-1 suppliers unveiled 77-81 GHz system-on-chips that embed deep-learning acceleration, squeezing more angular resolution from established antenna designs. Premium and battery-electric platforms adopt 79 GHz to unlock 4 GHz sweep bandwidth for high-definition point clouds, yet mass-market models remain on 77 GHz for cost control. Spectrum-sharing challenges in dense corridors add engineering overhead, but proprietary interference-rejection stacks keep performance within Euro NCAP tolerance bands. The dual-band roadmap allows carmakers to stagger investment and protect residual tooling value in 77 GHz production lines.

Geography Analysis

Asia-Pacific generated 38.48% of 2025 revenue for the automotive radar market, and its 14.53% CAGR through 2031 positions the region as the fastest-growing demand center. China anchors this expansion: domestic suppliers such as Cheng-Tech and Huawei are scaling 77 GHz and 79 GHz module production to meet the 2028 automatic emergency-braking mandate, while original equipment manufacturers (OEMs) bundle six-sensor suites on mid-tier trims to hold feature parity with European and North American rivals. Japan and South Korea display high radar adoption in premium cars and export large volumes of modules through DENSO, Hitachi Astemo and Nidec Elesys, yet growth moderates as their domestic markets approach saturation. India's radar penetration remains below 10% in 2025, but the Ministry of Road Transport and Highways is evaluating a 2027-2028 automatic emergency-braking timeline, creating a latent runway that could lift regional shipments late in the forecast window. Southeast Asian markets lag in regulatory enforcement, although insurance rebates for blind-spot detection retrofits are stimulating aftermarket demand in Thailand, Indonesia and Vietnam. Australia and New Zealand maintain radar attach rates on par with Western Europe, driven by long-distance highway safety requirements that favor long-range adaptive-cruise modules. Collectively, Asia-Pacific's scale advantage reduces average selling prices, helping the automotive radar market defend margins even as unit counts accelerate.

Europe contributed roughly 28% of global revenue in 2025, underpinned by stringent Euro NCAP ratings that compel five-star contenders to fit forward-collision, blind-spot and in-cabin child-presence radar. Premium brands deploy 4D imaging solutions at 79 GHz to differentiate on perception accuracy, while volume manufacturers still rely on cost-optimized 77 GHz corner sensors for compliance. Continental's cumulative 200 million-unit production milestone and EUR 1.5 billion (USD 1.70 billion) in 2025 radar orders illustrate Europe's role as both design-validation hub and volume anchor for Tier-1 suppliers. Eastern European contract assemblers expand module output to serve German, French and Italian OEMs that embrace near-shoring strategies to contain logistics risk. Regulatory convergence across 27 member states guarantees homogeneous demand, yet spectrum congestion around 79 GHz in dense corridors such as Frankfurt and Paris requires interference-mitigation spending that raises total system cost. As battery-electric vehicle (BEV) registrations rise past 30% of new sales in 2026, European BEV platforms average five to six sensors, prolonging growth even as combustion volumes decline. Europe therefore remains the lead market for software-defined radar updates and over-the-air performance enhancements.

North America held approximately 24% of 2025 revenue, with momentum tied to National Highway Traffic Safety Administration automatic emergency-braking mandates and the commercialization of hands-free highway suites like General Motors Ultra Cruise and Ford BlueCruise. Pickup trucks and full-size SUVs integrate three to four long-range sensors for trailer-tow assistance and lane-centering, lifting per-vehicle dollar content despite lower unit shipments than compact passenger cars. Canada mirrors U.S. regulations, while Mexico focuses on export-oriented assembly of radar-equipped vehicles destined for the United States. South America, the Middle East and Africa together generated less than 10% of 2025 revenue; radar adoption concentrates in fleet and commercial segments where duty-cycle savings and lower insurance premiums offset initial hardware cost. Government safety programs in Brazil and Saudi Arabia may accelerate take-up after 2027, but fragmented standards and limited supplier footprints restrain near-term volumes. Overall, geographic diversification cushions the automotive radar market size from regional policy shocks and balances growth across mature and emerging economies.

- Robert Bosch GmbH

- Continental AG

- DENSO Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Texas Instruments Inc.

- HELLA GmbH and Co. KGaA

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Analog Devices Inc.

- Magna International Inc.

- Autoliv Inc.

- Veoneer Safety Systems

- Renesas Electronics Corp.

- STMicroelectronics N.V.

- Valeo SA

- Arbe Robotics Ltd.

- Vayyar Imaging Ltd.

- Indie Semiconductor

- Uhnder Inc.

- Smartmicro GmbH

- Smart Radar System Inc.

- Hitachi Astemo Ltd.

- Nidec Elesys Corp.

- Lunewave Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent NCAP And UNECE Safety Mandates

- 4.2.2 77 GHz Cost-Driven Miniaturisation Wave

- 4.2.3 Mass-Market Level-2+ Autonomy Adoption

- 4.2.4 EV Architecture Headroom For Additional Sensors

- 4.2.5 Emerging 4D Imaging Radar For Vision-Redundancy

- 4.2.6 Chiplet-Based Radar SOCs Enabling Retrofit Market

- 4.3 Market Restraints

- 4.3.1 High Multi-Sensor Fusion System Cost

- 4.3.2 Spectrum Congestion At 79 GHz In Key Regions

- 4.3.3 Thermal Bottlenecks In Legacy GigE Backbones

- 4.3.4 SiGe / GaAs Wafer Supply Constraints

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Conventional vs 4D vs Imaging)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Range

- 5.1.1 Short-Range Radar (SRR)

- 5.1.2 Medium-Range Radar (MRR)

- 5.1.3 Long-Range Radar (LRR)

- 5.2 By Frequency Band

- 5.2.1 24 GHz

- 5.2.2 77 GHz

- 5.2.3 79 GHz and above

- 5.3 By Application

- 5.3.1 Adaptive Cruise Control (ACC)

- 5.3.2 Automatic Emergency Braking (AEB)

- 5.3.3 Blind-Spot / Rear Cross-Traffic

- 5.3.4 Occupancy and Driver Monitoring

- 5.3.5 Autonomous Driving (L3+)

- 5.3.6 Parking Assistance and Automated Parking

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial Vehicles

- 5.4.4 Robotaxis and AV Shuttles

- 5.5 By Propulsion

- 5.5.1 Internal-Combustion Vehicles

- 5.5.2 Battery-Electric Vehicles

- 5.5.3 Hybrid-Electric Vehicles

- 5.6 By Sales Channel

- 5.6.1 OEM-Fitted

- 5.6.2 Aftermarket Retrofits

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Australia and New Zealand

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 DENSO Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Aptiv PLC

- 6.4.6 Texas Instruments Inc.

- 6.4.7 HELLA GmbH and Co. KGaA

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 Infineon Technologies AG

- 6.4.10 Analog Devices Inc.

- 6.4.11 Magna International Inc.

- 6.4.12 Autoliv Inc.

- 6.4.13 Veoneer Safety Systems

- 6.4.14 Renesas Electronics Corp.

- 6.4.15 STMicroelectronics N.V.

- 6.4.16 Valeo SA

- 6.4.17 Arbe Robotics Ltd.

- 6.4.18 Vayyar Imaging Ltd.

- 6.4.19 Indie Semiconductor

- 6.4.20 Uhnder Inc.

- 6.4.21 Smartmicro GmbH

- 6.4.22 Smart Radar System Inc.

- 6.4.23 Hitachi Astemo Ltd.

- 6.4.24 Nidec Elesys Corp.

- 6.4.25 Lunewave Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

汽車雷達市場預測至2034年-全球分析(依雷達偵測範圍、頻段、自動化程度、雷達類型、應用、銷售管道和地區分類)

汽車雷達市場預測至2034年-全球分析(依雷達偵測範圍、頻段、自動化程度、雷達類型、應用、銷售管道和地區分類) 汽車雷達市場:按類型、組件、偵測範圍、頻段、應用、車輛類型和銷售管道分類-2026-2032年全球市場預測

汽車雷達市場:按類型、組件、偵測範圍、頻段、應用、車輛類型和銷售管道分類-2026-2032年全球市場預測 汽車雷達市場分析及預測(至2035年):類型、產品、技術、組件、應用、功能、安裝方式、解決方案、模式

汽車雷達市場分析及預測(至2035年):類型、產品、技術、組件、應用、功能、安裝方式、解決方案、模式 全球汽車雷達市場(至2033年):依探測範圍(短、中、長)、車輛類型(乘用車、輕型商用車、重型商用車)、頻率(2GHz、7GHz)、電動車類型(純電動車、插電式混合動力車、燃料電池電動車、混合動力車)、安裝位置(車載、車外)、應用車外)、應用車外)

全球汽車雷達市場(至2033年):依探測範圍(短、中、長)、車輛類型(乘用車、輕型商用車、重型商用車)、頻率(2GHz、7GHz)、電動車類型(純電動車、插電式混合動力車、燃料電池電動車、混合動力車)、安裝位置(車載、車外)、應用車外)、應用車外) 汽車雷達市場規模、佔有率、趨勢和預測:按探測範圍、車輛類型、應用和地區分類,2026-2034年

汽車雷達市場規模、佔有率、趨勢和預測:按探測範圍、車輛類型、應用和地區分類,2026-2034年 2026年全球車輛雷達測試系統市場報告2026年全球汽車雷達市場報告汽車雷達感測器市場:按安裝類型、技術、車輛類型、最終用戶和應用分類-2026-2032年全球市場預測

2026年全球車輛雷達測試系統市場報告2026年全球汽車雷達市場報告汽車雷達感測器市場:按安裝類型、技術、車輛類型、最終用戶和應用分類-2026-2032年全球市場預測 汽車雷達市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

汽車雷達市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 汽車雷達市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

汽車雷達市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)