|

市場調查報告書

商品編碼

2065571

通訊業ERP:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Telecom Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

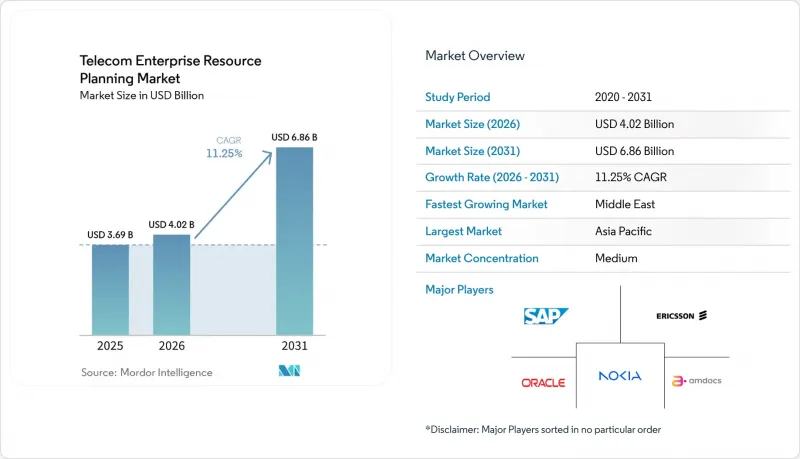

據 Mordor Intelligence 稱,通訊業的 ERP 市場預計將從 2025 年的 36.9 億美元成長到 2026 年的 40.2 億美元,到 2031 年的複合年成長率為 11.25%。

本報告按部署模式(本地部署、雲端部署、混合部署)、組件(軟體和服務)、組織規模(中小型通訊業者、大型通訊業者)、職能部門(財務會計、人力資源、供應鏈和採購、客戶關係管理、網路管理等)以及地區進行細分。市場預測以美元計價。

全球通訊業ERP市場趨勢與洞察

電信服務供應商(CSP) 的 5G 網路部署

獨立組網的 5G 核心網路需要即時收費、動態成本分配以及跨合作夥伴雲端的編配——這些功能是傳統 ERP 系統無法處理的。 MTN 南非公司 2025 年的部署凸顯了這些挑戰,促使該公司實施了一套雲端原生套件,整合了財務、庫存和網路分析功能。阿曼和印尼的通訊業者也紛紛效仿,透過基於 API 的 ERP 工作流程,將服務交付時間從數週縮短至數小時。此外,5G 的低延遲和網路切片功能支援垂直整合的企業服務,這些服務需要精細化的 SLA 定價,從而加速了向模組化 ERP 的轉型,模組化 ERP 整合了目錄和收入保障引擎。混合部署的擴張速度目前已超過市場成長速度,它允許利用基於雲端的分析來最佳化網路切片貨幣化,同時保持本地收費管治。

透過自動化降低營運成本的努力

由於平均每用戶收入 (ARPU) 成長停滯不前,而鐵塔租賃成本卻飆升,通訊業者幾乎沒有餘力維持人工流程。 Reliance Jio 透過在整合 ERP 平台內實現採購、庫存匹配和供應商付款的自動化,在 2024 年將營運成本降低了 30%。愛立信在遷移到 SAP S/4HANA 後,專案預算減少了 30%,這表明雲端 ERP 可以縮短實施時間和降低諮詢費用。諸如 GDPR 之類的法規結構進一步要求實現審計追蹤的自動化,合規性正從成本中心轉變為董事會層面的促進因素。因此,曾經受制於資金限制的中小型營運商,如今採用基於 SaaS 的 ERP 的速度約為整體市場複合年成長率的 1.5 倍。

三級通訊業者初始授權費用高昂

對於中型通訊業者,企業級ERP授權費用可能超過500萬美元,這筆費用與建造通訊塔或續訂頻段的成本相當。 SaaS定價模式減輕了這一負擔,但也引發了人們對供應商鎖定和外匯波動的擔憂。這一財務障礙導致預計複合年成長率下降約1.4個百分點,且供應商的銷售管道也傾向於大型成熟業者。

細分市場分析

預計到2025年,混合部署將在通訊業ERP市場佔據顯著佔有率,並在2031年之前以15.2%的複合年成長率成長。通訊業者正在利用雲端的擴充性進行分析、採購和人力資源管理,同時將用戶資料和關鍵收費流程保留在本地。這種方法還使他們能夠繞過數據主權障礙。雖然雲端模式仍然具有吸引力,預計到2025年將佔據通訊業ERP市場46%的佔有率,但純雲端模式的成長落後於混合模式,因為關鍵任務工作負載仍需要本地控制。隨著對延遲敏感的邊緣應用日益普及,通訊業ERP市場中混合解決方案的市場規模預計將進一步擴大。

Freedom Mobile 的雲端遷移案例研究表明,混合雲設計可實現 99.99% 的可用性,並降低 35% 的 IT 營運成本 (OPEX)。沃達豐、Orange 以及海灣國家的通訊業者目前也正在採用類似的模式。儘管嚴格的資料居住要求阻礙了中國和俄羅斯對公共雲端的採用,但監管機構已表示未來有意放寬監管,預計這將推動預測期內對混合雲解決方案的需求成長。

儘管預計到2025年軟體授權收入將佔總收入的55%,但從諮詢到託管營運等各類服務的成長速度更快,複合年成長率高達17.8%。隨著通訊業者將資料遷移、AI模型調優和API管治等專業技能外包,通訊業的ERP市場正在蓬勃發展。愛立信的SAP專案透過自動化遷移而非支付授權費,實現了30%的成本降低,從而顯著提升了價值。

IBM、Accenture和Amdocs等系統整合商提供固定價格的捆綁套餐,並保證過渡進度,這項提案引起了那些因IT預算難以預測而疲憊不堪的財務長們的共鳴。隨著人工智慧模組滲透到網路管理中,「資料科學家即服務」的需求不斷成長,進一步擴大了服務支出佔比。因此,儘管軟體仍將發揮基礎性作用,通訊業ERP市場中服務的佔有率預計將穩定成長。

區域分析

預計到2025年,亞太地區將佔全球收入的34%,這主要得益於印度5G的快速商業化以及中國數十億美元的虛擬化項目。繼Reliance Jio透過使用ERP系統將營運成本(OpEx)降低了30%之後,Bharti Airtel和Vodafone Idea也啟動了類似的專案。日本和韓國在4G時代完成了現代化改造,目前正專注於最佳化頻段的AI疊加模組,其業務重心也正悄悄從核心財務分析轉向網路分析。隨著各地監管機構逐步放寬跨境資料流動的限制,混合ERP的普及將與日益成長的邊緣運算流量保持同步。

中東是成長最快的地區,年複合成長率高達13.6%。沙烏地阿拉伯的「2030願景」和阿拉伯聯合大公國的智慧城市計畫都對即時收費、物聯網整合和彈性資源配置提出了要求。為了確保這些能力,STC和Etisalat正在向雲端原生ERP轉型,而波灣合作理事會(GCC)為協調資料法律所做的努力也進一步加速了這一進程。土耳其和以色列也緊隨其後,利用ERP現代化來提升其企業服務組合在競爭激烈的行動市場中的差異化優勢。

北美和歐洲市場規模依然龐大,但已趨於成熟。 AT&T 斥資 140 億美元的網路計畫和 Verizon 的頻段投資正將大量資金投入 ERP 系統中,以實現採購和庫存管理的自動化。在歐洲,GDPR(一般資料保護規則)強制要求即時收入保障,促使通訊業者採用整合合規工作流程的 ERP 套件。因此,成長更集中在模組級升級而非待開發區系統替換。南美和非洲的發展速度較為緩慢,但提供「按需收費」定價的 SaaS 模式正開始挖掘那些融資不佳的通訊業者的潛在需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設與市場定義* 研究範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電信服務供應商(CSP) 的 5G 網路部署

- 透過自動化降低營運成本的努力

- 擴大一級通訊業者對雲端原生BSS/OSS堆疊的採用

- 將人工智慧驅動的預測分析整合到ERP套件中

- 即時收入保障和可審計性的監管要求

- 對跨多廠商環境的端到端網路可視性的需求日益成長。

- 市場限制因素

- 三級企業的初始授權費用較高

- 從傳統 OSS/BSS 遷移資料所帶來的複雜性

- 通訊業ERP實施專業人員短缺

- 跨境雲端採用中的資料主權問題

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 現場

- 雲

- 混合

- 按組件

- 軟體

- 服務

- 按組織規模

- 中小型通訊業者

- 主要通訊業者

- 按功能

- 財會

- 人力資源

- 供應鏈與採購

- 客戶關係管理

- 網管

- 庫存管理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- International Business Machines Corporation

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- TEOCO Corporation

- Amdocs Limited

- CSG Systems International Inc.

- The Sage Group plc

- Infor Inc.

- Comarch SA

- Tecnotree Corporation

- Oracle NetSuite LLC

- SYSPRO(Pty)Ltd.

- Epicor Software Corporation

- IFS AB

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- FPT Software Company Limited

第7章 市場機會與未來展望

目錄

第1章:引言

- 研究假設與市場定義* 研究範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電信服務供應商(CSP) 的 5G 網路部署

- 透過自動化降低營運成本的努力

- 擴大一級通訊業者對雲端原生BSS/OSS堆疊的採用

- 將人工智慧驅動的預測分析整合到ERP套件中

- 即時收入保障和可審計性的監管要求

- 對跨多廠商環境的端到端網路可視性的需求日益成長。

- 市場限制因素

- 三級企業的初始授權費用較高

- 從傳統 OSS/BSS 遷移資料所帶來的複雜性

- 通訊業ERP實施專業人員短缺

- 跨境雲端採用中的資料主權問題

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 現場

- 雲

- 混合

- 按組件

- 軟體

- 服務

- 按組織規模

- 中小型通訊業者

- 主要通訊業者

- 按功能

- 財會

- 人力資源

- 供應鏈與採購

- 客戶關係管理

- 網管

- 庫存管理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- International Business Machines Corporation

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- TEOCO Corporation

- Amdocs Limited

- CSG Systems International Inc.

- The Sage Group plc

- Infor Inc.

- Comarch SA

- Tecnotree Corporation

- Oracle NetSuite LLC

- SYSPRO(Pty)Ltd.

- Epicor Software Corporation

- IFS AB

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- FPT Software Company Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the telecom ERP market size is expected to increase from USD 3.69 billion in 2025 to USD 4.02 billion in 2026 and reach USD 6.86 billion by 2031, growing at a CAGR of 11.25% over 2026-2031.

This report is Segmented by Deployment Model (On-Premise, Cloud, and Hybrid), Component (Software and Services), Organization Size (Small and Medium Telecom Operators and Large Telecom Operators), Function (Finance and Accounting, Human Resources, Supply Chain and Procurement, Customer Relationship Management, Network Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Telecom Enterprise Resource Planning Market Trends and Insights

Proliferation Of 5G Networks Among CSPs

Standalone 5G cores require real-time billing, dynamic cost allocation, and orchestration across partner clouds, functions that legacy ERP stacks cannot handle. MTN South Africa's 2025 rollout exposed these gaps, prompting the carrier to adopt a cloud-native suite that integrates finance, inventory, and network analytics. Operators in Oman and Indonesia echoed this pivot, reducing activation windows from weeks to hours through API-based ERP workflows. 5G's latency and slicing capabilities also unlock vertical enterprise services that demand granular SLA pricing, intensifying the shift toward modular ERP with embedded catalog and revenue-assurance engines. Hybrid deployments now outpace market growth because they retain on-premise billing governance while cloudifying analytics that optimize slice monetization.

Push Toward Operational Expenditure Reduction Via Automation

Stagnant ARPU and tower-lease inflation leave operators little room for manual processes. Reliance Jio cut operating costs by 30% in 2024 by automating procurement, inventory reconciliation, and vendor payments within a unified ERP fabric. Ericsson shaved 30% off project budgets after moving to SAP S/4HANA, confirming that cloud ERP compresses both implementation time and consultant fees. Regulatory frameworks like GDPR further demand automated audit trails, turning compliance from a cost center into a board-level driver. Small and medium carriers, once hampered by capital constraints, are therefore adopting SaaS ERP at almost 1.5 times the overall market CAGR.

High Upfront Licensing Costs For Tier-3 Operators

For a mid-size carrier, enterprise-grade ERP licenses can exceed USD 5 million, a figure that rivals tower builds and spectrum renewals. ARPU below USD 2 restricts credit headroom, delaying modernization projects in Africa and parts of Southeast Asia. SaaS pricing eases the pain but triggers concerns about vendor lock-in and exchange-rate volatility. This financial barrier reduces the projected CAGR by roughly 1.4 percentage points and skews vendor pipelines toward larger incumbents.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption Of Cloud-Native BSS/OSS Stacks In Tier-1 Operators

- Integration Of AI-Driven Predictive Analytics Within ERP Suites

- Data Migration Complexities From Legacy OSS/BSS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments captured a meaningful share of the telecom ERP market in 2025 and are poised to grow at a 15.2% CAGR through 2031. Operators keep subscriber data and critical billing on-premise while leveraging cloud elasticity for analytics, procurement, and HR. The approach also sidesteps sovereign data hurdles. Cloud models remain attractive, holding 46% telecom ERP market share in 2025, but pure-play cloud growth trails hybrid because mission-critical workloads still demand local control. The telecom ERP market size for hybrid solutions is expected to widen further as latency-sensitive edge applications proliferate.

Freedom Mobile's cloud migration proved that a hybrid design can deliver 99.99% availability and 35% IT Opex savings. Similar blueprints are now deployed by Vodafone, Orange, and operators across the Gulf states. In China and Russia, strict data-residency clauses hold back public-cloud adoption, yet regulators signal eventual relaxation, which will funnel pent-up demand toward hybrid over the forecast window.

Software licenses generated 55% revenue in 2025, but services, from consulting to managed operations, are scaling faster at 17.8% CAGR. The telecom ERP market for services is expanding as carriers outsource scarce skills in data migration, AI model tuning, and API governance. Ericsson's SAP program saved 30% not on licensing but on automated migration, underscoring where value accrues.

System integrators such as IBM, Accenture, and Amdocs are packaging fixed-price bundles that guarantee cut-over timelines, a proposition resonating with CFOs fatigued by open-ended IT budgets. As AI modules permeate network management, demand for data-scientist-as-a-service further tilts wallet share toward services. Consequently, the telecom ERP market share of services is projected to expand steadily, even as software retains its foundational role.

Geography Analysis

Asia-Pacific held 34% revenue in 2025, fueled by India's rapid 5G monetization and China's multi-billion-dollar virtualization programs. Reliance Jio's ERP-driven 30% OpEx drop spurred Bharti Airtel and Vodafone Idea to initiate similar projects. Japan and South Korea, having modernized during 4G cycles, now focus on AI overlay modules that optimize spectrum, subtly shifting wallet share from core finance to network analytics. As local regulators ease cross-border data hurdles, hybrid ERP adoption will keep pace with rising edge-compute traffic.

The Middle East is the fastest-growing region, with a 13.6% CAGR. Saudi Arabia's Vision 2030 mandates and the United Arab Emirates' smart-city agendas require real-time billing, IoT integration, and elastic provisioning. STC and Etisalat pivoted to cloud-native ERP to secure those capabilities, and the Gulf Cooperation Council's efforts to harmonize data laws further accelerate momentum. Turkey and Israel follow suit, leveraging ERP modernization to differentiate enterprise service portfolios in a crowded mobile landscape.

North America and Europe remain sizable but mature. AT&T's USD 14 billion network plan and Verizon's spectrum investments allocate meaningful funds to ERP for procurement and inventory automation. In Europe, GDPR compels real-time revenue assurance, nudging operators toward ERP suites with embedded compliance workflows. Growth therefore tilts toward module-level upgrades rather than greenfield replacements. South America and Africa progress more slowly, yet SaaS models that offer pay-as-you-grow pricing begin to unlock latent demand among cash-strapped carriers.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- International Business Machines Corporation

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- TEOCO Corporation

- Amdocs Limited

- CSG Systems International Inc.

- The Sage Group plc

- Infor Inc.

- Comarch S.A.

- Tecnotree Corporation

- Oracle NetSuite LLC

- SYSPRO (Pty) Ltd.

- Epicor Software Corporation

- IFS AB

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- FPT Software Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition * Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of 5G Networks Among CSPs

- 4.2.2 Push Toward Operational Expenditure Reduction Via Automation

- 4.2.3 Rising Adoption of Cloud-Native BSS/OSS Stacks in Tier-1 Operators

- 4.2.4 Integration of AI-Driven Predictive Analytics Within ERP Suites

- 4.2.5 Regulatory Mandates for Real-Time Revenue Assurance and Auditability

- 4.2.6 Growing Demand for End-to-End Network Visibility Across Multi-Vendor Environments

- 4.3 Market Restraints

- 4.3.1 High Upfront Licensing Costs for Tier-3 Operators

- 4.3.2 Data Migration Complexities From Legacy OSS/BSS

- 4.3.3 Scarcity of Telecom-Specific ERP Implementation Talent

- 4.3.4 Concerns Over Data Sovereignty in Cross-Border Cloud Deployments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Small and Medium Telecom Operators

- 5.3.2 Large Telecom Operators

- 5.4 By Function

- 5.4.1 Finance and Accounting

- 5.4.2 Human Resources

- 5.4.3 Supply Chain and Procurement

- 5.4.4 Customer Relationship Management

- 5.4.5 Network Management

- 5.4.6 Inventory Management

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 International Business Machines Corporation

- 6.4.5 Telefonaktiebolaget LM Ericsson

- 6.4.6 Nokia Corporation

- 6.4.7 TEOCO Corporation

- 6.4.8 Amdocs Limited

- 6.4.9 CSG Systems International Inc.

- 6.4.10 The Sage Group plc

- 6.4.11 Infor Inc.

- 6.4.12 Comarch S.A.

- 6.4.13 Tecnotree Corporation

- 6.4.14 Oracle NetSuite LLC

- 6.4.15 SYSPRO (Pty) Ltd.

- 6.4.16 Epicor Software Corporation

- 6.4.17 IFS AB

- 6.4.18 Huawei Technologies Co., Ltd.

- 6.4.19 ZTE Corporation

- 6.4.20 FPT Software Company Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment