|

市場調查報告書

商品編碼

2065564

AI偏向性審計與人力資源演算法公平性:市場佔有率分析、產業趨勢與統計數據以及成長預測(2026-2031年)AI Bias Audit And Algorithmic Fairness In HR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

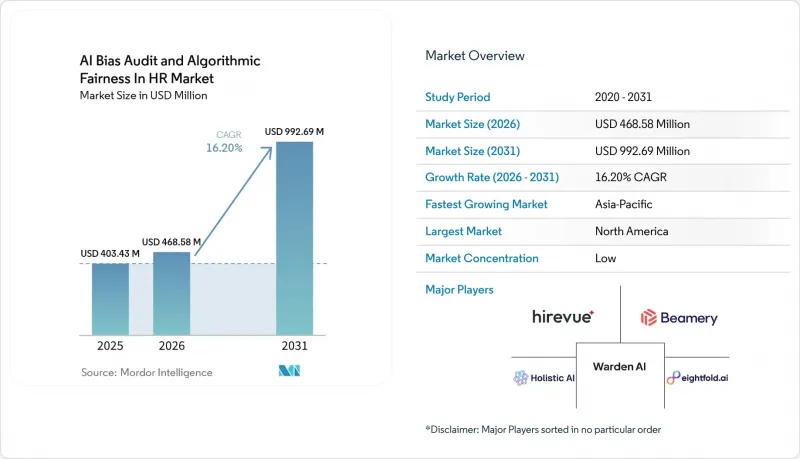

據 Mordor Intelligence 稱,2025 年人工智慧偏見審計和人力資源演算法公平性市場價值 4.0343 億美元,預計到 2031 年將達到 9.9269 億美元,2026 年至 2031 年的複合年成長率為 16.20%。

本報告按組件(軟體和服務)、人力資源工作流程(候選人篩檢和排名等)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、最終用戶行業(零售、電子商務等)以及地區進行細分。市場預測以美元計價。

全球市場趨勢及對人工智慧偏見審計和人力資源演算法公平性的洞察。

監管力度加大,導致自動化招募決策工具的偏見審計範圍擴大。

繼紐約市強制要求對自動化招聘決策工具進行獨立偏見審計後,人力資源領域的AI偏見審計和演算法公平性市場已進入更嚴格的合規階段。該規定要求受影響的雇主在實施後的12個月內接受審計,公佈審計結果,並在評估候選人之前使用相關工具。該框架還規定,每次違規每天將處以500至1500美元的罰款,將審計成本從可自由支配的預算項目轉變為法律風險管理措施。在伊利諾州,第103-0804號公共法案修訂了《伊利諾伊州人權法》,將AI在招聘中的歧視性影響列為雇主必須直接關注的問題,該修訂將於2026年1月1日生效,進一步加大了合規壓力。這項轉變意義重大,因為當AI工具影響招募、甄選或相關決策時,雇主就不能再只依賴供應商的說法。隨著越來越多的司法管轄區效仿這種模式,人工智慧偏向的人力資源審計和演算法公平市場越來越受到法律期限的驅動,而不是長期的內部管治計畫的驅動。

根據歐盟人工智慧法,人工智慧在就業領域被歸類為「高風險」技術。

歐盟人工智慧立法也推動了人工智慧偏見審計和人力資源演算法公平性市場的發展,因為用於招聘、甄選、晉升、職位分配和績效考核的僱用系統被歸類為高風險系統。歐盟第2024/1689號法規強制要求高風險人工智慧系統必須具備技術文件、資料管治、人工監督、上市後監控和正式的合規控制。該法規第4條也規定,員工使用這些系統的組織必須具備人工智慧素養。這意味著,即使在未來的實施里程碑完全實現之前,合規活動也已在進行中。第99條對組織施加了巨大的財務壓力,因為違規可能導致高達1500萬歐元(1620萬美元)或全球營業額3%的罰款。對於跨國公司而言,這並非取代美國偏見審計法規,而是一項平行實施的新業務流程。因此,人工智慧偏見審計和人力資源演算法公平性的市場正受益於全球人力資源營運中對合規準備、文件支援和工作流程層級管理的需求。

不同工具和司法管轄區之間缺乏標準化的公平性基準

在人工智慧主導的人力資源審計和演算法公平性市場中,目前仍缺乏適用於所有法律和營運環境的統一公平性標準。 Warden AI 的研究發現,即使是名義上相似的系統,其公平性評分也可能相差高達 40%,而且 15% 的受審計工具雖然滿足了某些人口統計閾值,卻未能滿足其他閾值。這對雇主來說是一個問題,因為審計結果會受到指標閾值、測試設計以及審查過程中適用的法律體制的嚴重影響。關於人工智慧和倫理的學術研究也得出了類似的結論,認為如果沒有更強大、更多樣化的監督機制,人工智慧人力資源系統無法在不同的法律環境下可靠地滿足公平性要求。對於供應商而言,無法跨地區直接複用單一的審計方法增加了服務跨國買家的成本。對於買家而言,每個供應商用於定義公平性的不同測試邏輯使得競爭供應商之間的比較變得困難,並延緩了採購流程。

細分市場分析

到2025年,軟體將佔據人力資源人工智慧審計和演算法公平性市場67.31%的佔有率。這反映出企業更傾向於擴充性的管治工具,而非一次性的專案執行。在投資初期,買家更青睞能夠集中管理審計儀錶板、測試環境、工作流程控制和文件的平台。隨著大規模企業通常同時管理多個招募流程,並需要跨流程進行可重現的監控,這一趨勢依然強勁。因此,在人力資源人工智慧審計和演算法公平性市場中,軟體已被視為政策執行、證據收集和跨轄區報告的營運基礎設施層。該領域的驅動力並非來自一次性的審計事件,而是來自對日誌維護、模型行為文件記錄以及跨團隊合規活動協調的需求。

預計到2031年,面向人力資源的AI審計和演算法公平性服務市場將以19.84%的複合年成長率成長,這表明買家正迅速意識到「僅部署工具」的局限性。那些最初採用軟體部署模式的公司逐漸意識到,獨立審查、糾正計劃、政策設計和技術諮詢服務仍然需要專家參與。審計和監控服務也受益於將開發人員聲明與第三方檢驗分開來的法律規範,尤其是在涉及公開披露和候選人通知的情況下。因此,面向人力資源的AI審計和演算法公平性市場正在出現混合合約的興起,這些合約除了軟體訂閱外,還結合了託管審計和合規支援。這種重疊雖然會對個體顧問的利潤率帶來壓力,但也推動了持續的服務需求,因為企業會在部署後重新檢視管治控制措施。

到2025年,候選人篩檢和排名將佔市場佔有率的36.49%,成為人工智慧偏見審計和人力資源演算法公平性市場中最大的工作流程。這個市場定位反映了監管和訴訟風險最為顯著的領域,因為自動化篩檢通常是招募的第一步,直接影響候選人的錄用機會。 2026年5月,史丹佛大學人力資源與創新研究所(Stanford HAI)發布了一項研究,分析了來自150家雇主的400萬份申請資料。研究發現,26%的黑人申請者和15%的亞裔申請者申請的職位,其人工智慧工具的篩選結果可能會受到聯邦歧視調查。這一事實解釋了為什麼在早期階段的篩檢審計會獲得最大的預算,尤其是在處理大量候選人的雇主中。篩檢仍然是人工智慧偏見審計和人力資源演算法公平性市場中最突出的工作流程,因為排名模型、候選人篩選工具和自動化建議直接決定了哪些候選人能夠進入下一階段。

預計到2031年,人力資源管治、監控和報告市場將以18.23%的複合年成長率成長,這表明買家正在擴大審查範圍,不再局限於篩檢階段。雇主們開始意識到,如果招募、升遷、績效監控或留任模式在其他方面有偏見,那麼僅靠合規的篩檢工具無法消除風險。歐盟人工智慧立法支持這種更廣泛的觀點,規定與就業相關的人工智慧的應用範圍不僅限於招聘,還包括晉升、職位分配和績效監督。因此,人力資源領域的人工智慧偏見審計和演算法公平性市場正在轉向支援持續報告、異常處理和審計合規性的整體管理結構。人工智慧偏見審計和演算法公平性在人力資源領域也受益於新興的應用場景,例如入職培訓、學習路徑分配和薪資校準。在這些領域,實施可能領先正式監督結構的建立,這可能需要在未來進行審查。

區域分析

2025年,北美繼續保持領先地位,在人工智慧偏見審計和人力資源演算法公平性領域佔據38.21%的市場佔有率。該地區擁有最嚴格的執法環境,紐約市強制要求對符合條件的自動化招募決策工具進行獨立審計並通知候選人。伊利諾伊州於2026年1月1日修訂了《伊利諾伊州人權法》,進一步加強了相關工作,以解決人工智慧在招募中應用所造成的歧視性影響。這些措施迫使雇主將審計準備視為持續的營運要求,而非未來的規劃挑戰。此外,北美地區集中了許多主要的人力資源技術買家和供應商,這意味著該地區的合規支出可能會迅速影響其他地區人工智慧偏見審計和人力資源演算法公平性市場的產品設計和商業重點。

歐洲仍然是主要的需求中心,因為歐盟人工智慧法案將招聘、晉升、職位分配和績效監控系統列為就業環境中的高風險領域。鑑於第四條中概述的人工智慧素養義務已經生效,各組織正在建立管治流程,無需等待未來的里程碑。由於GDPR對敏感資料使用的限制,可獲得的直接人口統計數據有限,因此對受控實驗和其他支持公平性審查的方法的需求仍然很高。德國、法國和荷蘭仍然是重要的市場,因為這些國家擁有眾多跨國公司,這些公司必須使當地的勞動實踐與更廣泛的人工智慧合規義務保持一致。

預計到2031年,亞太地區人工智慧審計和人力資源演算法公平性市場規模將以18.79%的複合年成長率成長,成為各區域市場中成長最快的細分市場。這一成長主要得益於主要經濟體加速從普遍採用人工智慧轉向對更正式的職場管治的期望。據美國人力資源管理協會(SHRM)稱,全部區域人力資源領域的人工智慧採用率已經很高,但在人工智慧被更深入地應用於招聘決策之前,需要建立相應的監管框架。南美洲和中東及非洲地區雖然目前的收入規模仍然較小,但隨著大型跨國企業將隱私、非歧視和人工智慧管治原則應用於招聘實踐,這些地區的需求正在迅速成長。儘管這些地區目前的市場佔有率有限,但監管的成熟以及跨境合規的需求預計將推動其在人工智慧審計和人力資源演算法公平性領域的成長高於全球平均水平,這一成長預計將持續到2031年。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 執法主導推動擴大對自動化招募決策工具的偏見審計

- 根據歐盟人工智慧法,人工智慧在就業領域被歸類為「高風險」技術。

- 企業向可解釋、可進行偏見審計的人才智慧平台轉型。

- 實施基於雲端的持續監控和管治工具。

- 合成履歷和受控實驗:在人口統計有限的情況下進行審計工作。

- 從採購中的“信任供應商”過渡到“採購前演算法保證和公開審計儀表板”

- 市場限制因素

- 缺乏工具和跨司法管轄區的標準化公平標準

- 隱私問題、黑箱的複雜性以及資料存取障礙正在減緩獨立審計的進展。

- 營運商主導的合規性會減慢採購週期。

- 審計範圍的不足會造成交叉關聯風險和減損風險等剩餘風險。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 審計和監控服務

- 諮詢和合規服務

- 按人力資源工作流程

- 候選人遴選和排名

- 人才發掘與匹配

- 內部調動與晉升分析

- 員工績效與留任率分析

- 人力資源管治監督與彙報

- 其他

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 銀行業、金融服務業及保險業

- 醫療保健和生命科學

- IT/通訊

- 製造業

- 零售與電子商務

- 政府/公共部門

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- HireVue, Inc.

- Eightfold AI Inc.

- Beamery Inc.

- Holistic AI Limited

- Warden AI, Inc.

- Harver BV

- Sapia.ai Pty Ltd

- Findem, Inc.

- Credo AI, Inc.

- FairNow, Inc.

- BABL AI, Inc.

- O'Neil Risk Consulting & Algorithmic Auditing, Inc.

- Fairly AI Inc.

- Affirmity, Inc.

- Talview, Inc.

- X0PA AI Pte. Ltd.

- Textio, Inc.

- SeekOut, Inc.

- HumanlyHR Inc.

- Equalture BV

第7章 市場機會與未來展望

According to Mordor Intelligence, the aI bias audit and algorithmic fairness in HR market size was valued at USD 403.43 million in 2025 and is forecast to reach USD 992.69 million by 2031, advancing at a CAGR of 16.20% during 2026-2031.

This report is Segmented by Component (Software, and Services), HR Workflow (Candidate Screening and Ranking, and More), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI Bias Audit And Algorithmic Fairness In HR Market Trends and Insights

Enforcement-Led Expansion of Bias Audits for Automated Employment Decision Tools

The AI bias audit and algorithmic fairness in HR market moved into a stricter compliance phase after New York City required independent bias audits for automated employment decision tools. The rule requires covered employers to obtain an audit within 12 months of deployment, publish a summary, and notify candidates before the tool is used in evaluation. The same framework also introduced penalties of USD 500 to USD 1,500 per violation per day, which changed audit spending from a discretionary budget item into a legal risk-control measure. Illinois extended this compliance pressure when Public Act 103-0804 amended the Illinois Human Rights Act and made discriminatory effects from AI use in employment a direct employer concern from January 1, 2026. That shift matters because employers can no longer rely on vendor claims alone when AI tools affect hiring, screening, or related decisions. As more jurisdictions follow this pattern, the AI bias audit and algorithmic fairness in HR market is being pulled forward by legal deadlines rather than long-cycle internal governance programs.

EU AI Act Classification of Employment AI as High-Risk

The AI bias audit and algorithmic fairness in HR market is also being supported by the EU AI Act because employment systems used in recruitment, selection, promotion, task allocation, and performance monitoring fall within the high-risk category. Regulation EU 2024/1689 requires technical documentation, data governance, human oversight, post-market monitoring, and formal compliance controls for high-risk AI systems. Article 4 also brought AI literacy obligations into force for organizations whose staff interact with these systems, meaning compliance activity is already underway before later enforcement milestones fully arrive. Article 99 imposes significant financial pressure, as non-compliance can lead to fines of up to EUR 15 million (USD 16.2 million) or 3% of global turnover. For multinational employers, this creates a parallel workstream that sits alongside U.S. bias audit rules rather than replacing them. As a result, the AI bias audit and algorithmic fairness in HR market is benefiting from demand for conformity preparation, documentation support, and workflow-level controls across global HR operations.

Lack of Standardized Fairness Benchmarks Across Tools and Jurisdictions

The AI bias audit and algorithmic fairness in HR market still lacks a single fairness standard that works across every legal and operational setting. Warden AI found that fairness scores can vary by up to 40% across nominally similar systems and that 15% of audited tools fail at least one demographic threshold while passing others. That creates a problem for employers because the audit result can depend heavily on the choice of metrics, test design, and the legal framework applied during the review. Academic research in AI and Ethics reached a similar conclusion, arguing that AI-HR systems cannot reliably satisfy fairness requirements across different legal settings without stronger and more plural oversight structures. For vendors, this increases the cost of serving multinational buyers because a single audit approach cannot be cleanly reused across regions. For buyers, it slows procurement because comparing competing vendors becomes harder when each supplier frames fairness through a different testing logic.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Shift to Explainable, Bias-Audited Talent Intelligence Platforms

- Cloud-Based Continuous Monitoring and Governance Tooling Adoption

- Privacy, Black-Box Complexity, and Data Access Barriers Slow Independent Audits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 67.31% of AI bias audit and algorithmic fairness in HR market share in 2025, which reflected enterprise preference for scalable governance tooling over one-off project delivery. In the first wave of spending, buyers favored platforms that could centralize audit dashboards, testing environments, workflow controls, and documentation. That logic remains strong because large employers often manage multiple hiring workflows simultaneously and need repeatable oversight across them. The AI bias audit and algorithmic fairness in HR market has therefore treated software as the operational base layer for policy enforcement, evidence capture, and cross-jurisdiction reporting. This part of the AI bias audit and algorithmic fairness in HR industry is supported by the need to maintain logs, document model behavior, and coordinate compliance activity across teams rather than around one isolated audit event.

The AI bias audit and algorithmic fairness in HR market size for services is projected to expand at a 19.84% CAGR through 2031, which shows how quickly buyers are discovering the limits of tool-only adoption. Enterprises that started with software are finding that independent reviews, remediation plans, policy design, and technical advisory work still require specialist input. Audit and monitoring services are also benefiting from regulatory structures that separate developer claims from third-party validation, especially when public disclosures or candidate notifications are involved. As a result, the AI bias audit and algorithmic fairness in HR market is seeing more blended contracts where software subscriptions sit beside managed audits and compliance support. That overlap creates margin pressure for stand-alone advisers, but it also expands recurring service demand as organizations revisit governance controls after deployment.

Candidate screening and ranking accounted for 36.49% of the market in 2025, making it the largest workflow in the AI bias audit and algorithmic fairness in HR market. This position reflects where regulation and litigation risk have been most visible, since automated screening is often the first hiring step that directly affects candidate access. Stanford HAI reported in May 2026 that its study of 4 million applications across 150 employers found that 26% of Black applicants and 15% of Asian applicants applied to positions where an AI tool produced outcomes triggering federal discrimination scrutiny. That evidence explains why screening audits have drawn the largest early budgets, especially among employers that process large candidate pools. In the AI bias audit and algorithmic fairness in HR market, screening remains the most exposed workflow because ranking models, shortlisting tools, and automated recommendations directly shape who moves forward.

HR governance, monitoring, and reporting is projected to expand at a 18.23% CAGR through 2031, indicating that buyers are widening the scope of review beyond the screening stage. Employers are realizing that a compliant screening tool does not eliminate risk if sourcing, promotion, performance monitoring, or retention models create bias elsewhere. The EU AI Act reinforces this broader view, as employment-related AI is not limited to recruitment and extends to promotion, task allocation, and performance oversight. That is shifting the AI bias audit and algorithmic fairness in HR market toward workflow-spanning controls that support continuous reporting, exception handling, and audit readiness. The AI bias audit and algorithmic fairness in HR market also gains from emerging use cases in onboarding, learning-path assignment, and compensation calibration, where adoption can move faster than formal oversight and create future review needs.

Geography Analysis

North America held 38.21% of AI bias audit and algorithmic fairness in HR market share in 2025, which kept the region in the lead. The region is defined by the strongest enforcement backdrop, with New York City requiring independent audits and candidate notice for covered automated employment decision tools. Illinois added further weight from January 1, 2026, by amending the Illinois Human Rights Act to address discriminatory effects arising from AI use in employment. These actions have pushed employers to treat audit readiness as a live operating requirement rather than a future planning task. North America also benefits from the concentration of major HR technology buyers and vendors, which means compliance spending in the region can quickly influence product design and commercial priorities elsewhere in the AI bias audit and algorithmic fairness in HR market.

Europe remains a major demand center because the EU AI Act classifies recruitment, promotion, task allocation, and performance monitoring systems as high-risk in employment contexts. Article 4 AI literacy obligations are already in effect, meaning organizations are not waiting for later milestones before building governance processes. GDPR-related limits on sensitive data use continue to raise the need for counterfactual testing and other methods that can support fairness reviews where direct demographic data is limited. Germany, France, and the Netherlands remain important because they host many multinational employers that must align local labor practices with broader AI compliance duties.

The AI bias audit and algorithmic fairness in HR market size in Asia-Pacific is projected to expand at an 18.79% CAGR through 2031, making it the fastest-growing regional segment. Growth is being supported by a faster move from general AI adoption toward more formal workplace governance expectations across key economies. SHRM reported that HR AI adoption is already high across Asia-Pacific, which increases the need for control layers before use becomes more deeply embedded in employment decisions. South America, the Middle East, and Africa remain smaller in terms of current revenue, but they are beginning to build demand as large enterprises and multinational employers apply privacy, anti-discrimination, and AI governance principles to hiring practices. These regions still contribute a limited share today, yet their regulatory maturation and cross-border compliance needs support above-average expansion through 2031 relative to the global baseline of the AI bias audit and algorithmic fairness in HR market.

- HireVue, Inc.

- Eightfold AI Inc.

- Beamery Inc.

- Holistic AI Limited

- Warden AI, Inc.

- Harver B.V.

- Sapia.ai Pty Ltd

- Findem, Inc.

- Credo AI, Inc.

- FairNow, Inc.

- BABL AI, Inc.

- O'Neil Risk Consulting & Algorithmic Auditing, Inc.

- Fairly AI Inc.

- Affirmity, Inc.

- Talview, Inc.

- X0PA AI Pte. Ltd.

- Textio, Inc.

- SeekOut, Inc.

- HumanlyHR Inc.

- Equalture B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enforcement-Led Expansion of Bias Audits for Automated Employment Decision Tools

- 4.2.2 EU AI Act Classification of Employment AI as High-Risk

- 4.2.3 Enterprise Shift to Explainable, Bias-Audited Talent Intelligence Platforms

- 4.2.4 Cloud-Based Continuous Monitoring and Governance Tooling Adoption

- 4.2.5 Synthetic Resume and Counterfactual Testing Unlocking Audits Where Demographic Data Is Sparse

- 4.2.6 Procurement Shift From Vendor Trust to Pre-Purchase Algorithm Assurance and Public Audit Dashboards

- 4.3 Market Restraints

- 4.3.1 Lack of Standardized Fairness Benchmarks Across Tools and Jurisdictions

- 4.3.2 Privacy, Black-Box Complexity, and Data Access Barriers Slow Independent Audits

- 4.3.3 Deployer-Led Compliance Slows Procurement Cycles

- 4.3.4 Audit Scope Gaps Create Residual Exposure for Intersectional and Disability Risk

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Audit and Monitoring Services

- 5.1.2.2 Advisory and Compliance Services

- 5.2 By HR Workflow

- 5.2.1 Candidate Screening and Ranking

- 5.2.2 Talent Sourcing and Matching

- 5.2.3 Internal Mobility and Promotion Analytics

- 5.2.4 Workforce Performance and Retention Analytics

- 5.2.5 HR Governance, Monitoring and Reporting

- 5.2.6 Other HR Workflows

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services and Insurance

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecommunications

- 5.5.4 Manufacturing

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 HireVue, Inc.

- 6.4.2 Eightfold AI Inc.

- 6.4.3 Beamery Inc.

- 6.4.4 Holistic AI Limited

- 6.4.5 Warden AI, Inc.

- 6.4.6 Harver B.V.

- 6.4.7 Sapia.ai Pty Ltd

- 6.4.8 Findem, Inc.

- 6.4.9 Credo AI, Inc.

- 6.4.10 FairNow, Inc.

- 6.4.11 BABL AI, Inc.

- 6.4.12 O'Neil Risk Consulting & Algorithmic Auditing, Inc.

- 6.4.13 Fairly AI Inc.

- 6.4.14 Affirmity, Inc.

- 6.4.15 Talview, Inc.

- 6.4.16 X0PA AI Pte. Ltd.

- 6.4.17 Textio, Inc.

- 6.4.18 SeekOut, Inc.

- 6.4.19 HumanlyHR Inc.

- 6.4.20 Equalture B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球可信賴人工智慧市場報告2026年全球資訊科技(IT)管治與策略市場報告

2026年全球可信賴人工智慧市場報告2026年全球資訊科技(IT)管治與策略市場報告 人工智慧合規市場預測至2034年—按平台組件、部署模式、合規類型、合規功能、應用、最終用戶和地區分類的全球分析2026年全球差分隱私市場報告2026年全球資訊科技(IT)管治、風險與合規(GRC)市場報告2026年全球負責任人工智慧偏見審計平台市場報告2026年全球人工智慧(AI)回應安全評分市場報告2026年全球人工智慧信任、風險與安全管理市場報告

人工智慧合規市場預測至2034年—按平台組件、部署模式、合規類型、合規功能、應用、最終用戶和地區分類的全球分析2026年全球差分隱私市場報告2026年全球資訊科技(IT)管治、風險與合規(GRC)市場報告2026年全球負責任人工智慧偏見審計平台市場報告2026年全球人工智慧(AI)回應安全評分市場報告2026年全球人工智慧信任、風險與安全管理市場報告 全球人工智慧信任、風險和安全管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球人工智慧信任、風險和安全管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2025-2029年全球人工智慧信任、風險與安全管理市場

2025-2029年全球人工智慧信任、風險與安全管理市場