|

市場調查報告書

商品編碼

2065560

建築業ERP:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Construction Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

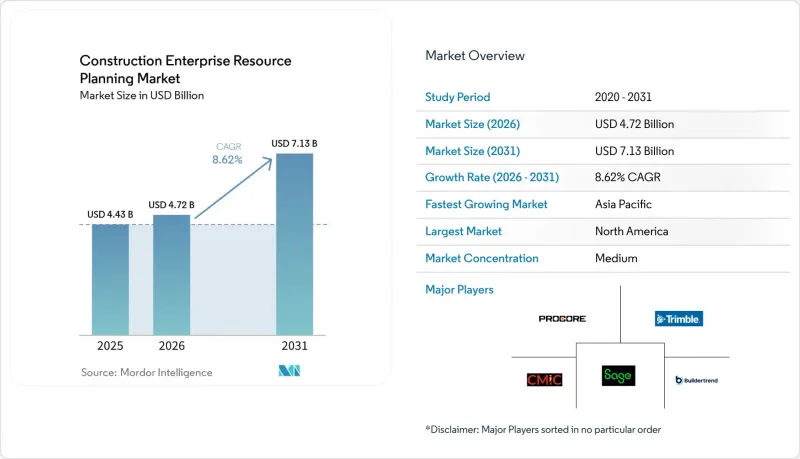

根據 Mordor Intelligence 預測,建築 ERP 市場規模將從 2025 年的 44.3 億美元和 2026 年的 47.2 億美元成長到 2031 年的 71.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 8.62%。

本報告按部署模式(雲端、本地部署、混合部署)、企業規模(中小企業、大型企業)、解決方案(軟體和服務)、最終用途(住宅建築、商業建築、基礎設施和土木工程、工業建築)以及地區進行細分。市場預測以美元計價。

全球建築ERP市場趨勢與洞察

擴大雲端ERP解決方案的採用

到2025年,雲端採用將佔營收的61.10%,複合年成長率(CAGR)為11.20%,比整體建築ERP市場成長率高出近300個基點。訂閱式定價將資本支出轉化為營運費用,從而釋放資金用於設備和人事費用。公共部門機構也認知到雲端的可靠性,例如美國退伍軍人事務部計劃在2025年將其171家醫療中心遷移到統一的雲端平台。供應商現在將多租戶功能和基於角色的入口網站打包在一起,使分包商的入駐流程能夠在幾分鐘內完成,並減少電子郵件溝通。 Procore的聯邦風險和授權管理計畫(FedRAMP)認證將於2025年獲得,這是美國聯邦計畫的強制性要求。歐洲的中小型企業也加入了這個趨勢。根據歐盟統計局的數據,中小企業 (SME) 和大型企業 (LBB) 的採用率相差 48 個百分點,但供應商正在透過引入基於專案的付費使用制來縮小這一差距。

政府增加對建築業的基礎建設支出

支出勢頭強勁。美國《基礎建設投資與就業法案》將在五年內撥款1.2兆美元,而英國2025年的預算也為主要交通走廊項目額外撥款17億英鎊(約21.5億美元)。在中東和北非地區,2025年前三個季度共授予了價值1570億美元的契約,其中沙烏地阿拉伯就佔了31%。印度的國家基礎設施管道和智慧城市計畫預計將使投資額從2025年的1,907億美元增加到2030年的2,806億美元。這些大型企劃需要合資企業會計、掙值分析和多幣種合併模組,而這些功能是普通軟體套件無法提供的。

高昂的初始設定和定製成本

根據基準研究,一家擁有 50 名員工的公司在 2025 年實施該專案的第一年,不計機會成本,預計支出在 14 萬至 21 萬美元之間。由於淨利率為 2% 至 4%,如此巨額的支出令許多競標望而卻步。雖然 Buildertrend 和 Projul 提供的入門訂閱計劃可以減輕前期成本負擔,但它們通常缺乏高級整合和 API 功能,迫使用戶在三年內轉換成本更高的平台。

細分市場分析

預計到2025年,雲端解決方案將佔總營收的61.10%,複合年成長率(CAGR)為11.20%。訂閱模式將伺服器和備份責任轉移給供應商,從而降低了資本支出,這支撐了雲端解決方案的強勁成長。隨著公共部門機構為聯邦公路和醫療設施採用FedRAMP認證的工具,預計建築ERP市場在雲端採用方面的規模將迅速擴大。在頻寬有限的地區,混合配置正在迅速發展,承包商將核心財務管理功能保留在本地,同時將現場協作遷移到雲端。隨著供應商逐步取消永久許可證,本地部署的使用率正在下降,但在受嚴格資料主權法規約束的國防承包商中,本地部署仍然佔據主導地位。

在建築ERP市場,具備整合快速配置功能的供應商目前佔優勢。 Procore的FedRAMP認證為其開闢了盈利的聯邦銷售管道,迫使競爭對手花費12至18個月的時間才能獲得類似認證。其多租戶架構使總承包商能夠立即啟動分包商門戶,無需再透過電子郵件發送資訊請求(RFI)。低程式碼工作流程引擎進一步縮短了標準成本加成和單價專案的部署時間。

預計到2025年,大型企業將佔據58.20%的收入佔有率,這主要得益於涵蓋數百個在建項目的多年期合約。然而,預計到2031年,中小企業(SME)的複合年成長率將達到10.40%,從而縮小市場普及率差距。隨著各國政府推出數位津貼,中小企業在建築ERP市場的市佔率預計將會上升。在馬來西亞,目前50%的軟體成本都得到了津貼。然而,資金籌措限制依然存在,預計到2025年,44%的歐洲中小企業將面臨信貸困難。雖然Buildertrend和Projul的分級定價模式將入門級年費控制在1萬美元以下,但如果缺少整合功能或車輛管理模組,則可能產生隱性升級成本。

實施過程中的負擔仍然是一項真正的挑戰。對於一家擁有 50 名員工的公司而言,六個月的實施期可能需要佔用關鍵員工 10% 到 20% 的工作時間,從而擾亂創收營運。為了解決這個問題,供應商正在提供預先配置的模板,用於住宅裝修、租戶室內裝修和大型土木工程項目,使中小企業能夠在八週內完成系統運作,從而保障現金流並加快價值實現。

區域分析

2025年,北美佔全球銷售額的43.70%。這主要得益於美國運輸部2026年預算中高達1,471億美元的巨額撥款,以及《戴維斯-培根法案》下嚴格的認證薪酬規定。加拿大透過其“加拿大投資計劃”,在12年內累計投資1800億加元(約1330億美元),約佔區域銷售額的8%至10%。在墨西哥,近岸外包推動的工廠建設熱潮促使大型承包商試行實施ERP系統,但中小企業仍更傾向於使用電子表格。儘管美國利率上升導致住宅開工量放緩,但建築ERP市場仍依賴合約續約和模組新增帶來的穩定維護收入。

亞太地區是成長最快的地區,預計到2031年複合年成長率將達到9.60%。印度已設定目標,到2030年建築支出達到2806億美元;沙烏地阿拉伯的建築項目儲備預計到2030年將達到1744億美元,複合年成長率為8.7%,這將推動對阿拉伯語和符合增值稅規定的系統的需求。在中國,由於「黃金稅」和資料居住法等障礙,ERP的普及程度仍不均衡。五家日本大型建設公司已將其企業套件標準化,目前正在試行數位雙胞胎以促進預測性維護。在東南亞,政府正在利用中小企業的津貼,隨著通訊基礎設施的改善,建築ERP市場正在蓬勃發展。

2025年,歐洲在全球銷售額中佔有重要佔有率。在英國,諸如泰晤士河下游通道等項目新增了17億英鎊(21.5億美元)的收入,刺激了分包商對自動化合規的需求。在德國和法國,發票自動化正根據國家商業法穩步推進,而從BIM到ERP的資料交換則由ISO 19650-4標準強制執行。在中東,沙烏地阿拉伯和阿拉伯聯合大公國合計佔據了2025年全球建築ERP市場收入的相當大一部分,目前正在進行的大型企劃更傾向於使用整合阿拉伯語語言包和多幣種帳簿的平台。南美和非洲仍處於起步階段,但EVOP和SYNEco等本地供應商正透過將電子帳單與區域稅務入口網站整合,開發利基市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大雲端ERP解決方案的採用

- 政府增加對建築業的基礎建設支出

- 對行動優先遠端協作功能的需求日益成長

- 更嚴格遵守有關建築會計和報告的法規。

- 人工智慧預測模組的出現減少了人工返工。

- BIM數位雙胞胎資料與ERP工作流程的整合

- 市場限制因素

- 初始實施和定製成本高昂

- 網路安全和資料隱私問題

- 遺留資料遷移的複雜性

- 建設產業ERP專業人才短缺

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 小型企業

- 大公司

- 透過解決方案

- 軟體

- 服務

- 按最終用途

- 住宅

- 商業建築

- 基礎設施和土木工程

- 工業建築

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Procore Technologies, Inc.

- Trimble Inc.(Viewpoint Division)

- CMiC Global Inc.

- Sage Group plc

- Jonas Construction Software Inc.

- Foundation Software, LLC

- Buildertrend Solutions, Inc.

- RedTeam Software, LLC

- Penta Technologies, Inc.

- Deltek, Inc.

- B2W Software, Inc.

- Explorer Software Group

- Eque2 Limited

- e-Builder, Inc.

- Projectmates(Systemates, Inc.)

- RIB Software GmbH

- UDA Technologies, Inc.

- Premier Construction Software

- COINS Global Limited

- Acumatica, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the construction eRP market size is projected to expand from USD 4.43 billion in 2025 and USD 4.72 billion in 2026 to USD 7.13 billion by 2031, registering an 8.62% CAGR between 2026 and 2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Solution (Software and Services), End Use (Residential Construction, Commercial Construction, Infrastructure and Civil Engineering, and Industrial Construction), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Construction Enterprise Resource Planning Market Trends and Insights

Growing Adoption of Cloud-Based ERP Solutions

Cloud deployment accounted for 61.10% of revenue in 2025 and is growing at a 11.20% CAGR, nearly 300 basis points above the Construction ERP market. Subscription pricing converts capital expenditures into operating expenses, freeing cash for equipment and labor. Public agencies validate cloud reliability, as seen when the United States Department of Veterans Affairs migrated 171 medical centers to a unified cloud platform in 2025. Vendors now package multi-tenancy and role-based portals so subcontractors can be onboarded in minutes, reducing email back-and-forth. The Federal Risk and Authorization Management Program (FedRAMP) certification, secured by Procore in 2025, has become mandatory for U.S. federal projects. European small firms are also entering the fold: Eurostat shows a 48-percentage-point adoption gap between small and large companies, which vendors are narrowing through pay-per-project tiers.

Increasing Government Infrastructure Spending on Construction

Spending momentum is pronounced. The United States Infrastructure Investment and Jobs Act channels USD 1.2 trillion over five years, while the United Kingdom's 2025 Budget added GBP 1.7 billion (USD 2.15 billion) for major transport corridors. In the Middle East and North Africa, USD 157 billion in contracts were let during the first three quarters of 2025, with Saudi Arabia alone accounting for 31%. India's National Infrastructure Pipeline and Smart Cities Mission underpin a rise from USD 190.7 billion in 2025 to USD 280.6 billion by 2030. These mega-projects demand joint-venture accounting, earned-value analysis, and multicurrency consolidation modules that generic suites cannot supply.

High Upfront Implementation and Customization Costs

Benchmarking shows a 50-person firm spent USD 140,000-210,000 on first-year deployment in 2025, excluding opportunity cost. With net margins at 2%-4%, six-figure outlays deter many bidders. Entry-level subscriptions from Buildertrend and Projul lower sticker shock but omit advanced consolidation and API features, often forcing a costly re-platform within three years.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Mobile-First and Remote Collaboration Capabilities

- Stricter Regulatory Compliance for Construction Accounting and Reporting

- Cybersecurity and Data-Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions accounted for 61.10% of revenue in 2025 and are growing at a 11.20% CAGR. This strength is anchored in subscription models that shift servers and backups to the vendor's responsibility, thereby reducing capital outlays. The Construction ERP market size for cloud deployments is forecast to climb sharply as public bodies adopt FedRAMP-authorized tools for federal highways and healthcare facilities. Hybrid configurations are growing rapidly because contractors in low-bandwidth regions keep financial cores on-premises while shifting field collaboration to the cloud. On-premise is contracting as vendors phase out perpetual licenses, yet it persists among defense contractors bound by strict data-sovereignty rules.

The Construction ERP market now rewards suppliers that embed rapid provisioning. Procore's FedRAMP authority has opened lucrative federal channels, forcing rivals to invest 12-18 months to earn similar clearance. Multi-tenant architectures allow general contractors to spin up subcontractor portals immediately, eliminating email-based RFIs. Low-code workflow engines further compress implementation timelines for standard cost-plus or unit-price projects.

Large enterprises held 58.20% of revenue share in 2025, buoyed by multi-year enterprise agreements covering hundreds of active projects. However, SMEs are advancing at a 10.40% CAGR to 2031, narrowing historical adoption gaps. The Construction ERP market share commanded by SMEs is expected to climb as governments launch digitalization grants. Malaysia now subsidizes 50% of software costs. Yet financing constraints linger: 44% of European SMEs reported credit difficulties in 2025. Tiered pricing from Buildertrend and Projul brings entry-level annual fees below USD 10,000, although missing consolidation and fleet modules can create hidden upgrade costs.

Implementation fatigue remains real. A 50-person company allocates 10%-20% of key staff hours during a six-month rollout, disrupting billable work. To compete, vendors are bundling pre-configured templates for residential remodeling, tenant improvement, or heavy civil so SMEs can go live in under eight weeks, thus protecting cash flow and improving time-to-value.

Geography Analysis

North America generated 43.70% of global revenue in 2025, energized by USD 147.1 billion in the United States Department of Transportation's 2026 budget and stringent Davis-Bacon certified payroll rules. Canada contributes roughly 8%-10% of regional sales through its Investing in Canada Plan, totaling CAD 180 billion (USD 133 billion) over 12 years. Mexico's nearshoring-driven factory boom is sparking ERP pilots among tier-one contractors, although smaller firms still favor spreadsheets. U.S. interest-rate hikes temper residential starts, but the Construction ERP market continues to bank on steady maintenance income from renewals and module add-ons.

Asia-Pacific is the fastest-growing region, with a 9.60% CAGR through 2031. India targets USD 280.6 billion in construction outlay by 2030, and Saudi Arabia's pipeline is slated to reach USD 174.4 billion at 8.7% CAGR by 2030, catalyzing demand for Arabic-language, VAT-ready systems. China's ERP adoption remains fragmented due to integration hurdles with Golden Tax and data-residency laws. Japan's Big Five contractors have standardized on enterprise suites and now pilot digital twins to drive predictive maintenance. Southeast Asia enjoys SME-friendly grants and is seeing Construction ERP market penetration grow as connectivity improves.

Europe captured significant percentage of global sales in 2025. The United Kingdom added GBP 1.7 billion (USD 2.15 billion) for projects such as the Lower Thames Crossing, spurring demand for subcontractor compliance automation. Germany and France automate invoicing under national commercial codes, while ISO 19650-4 drives BIM-to-ERP data exchange mandates. In the Middle East, Saudi Arabia and the United Arab Emirates together represented a notable percentage of global Construction ERP market revenue in 2025, with mega-projects that favor platforms embedding Arabic language packs and multicurrency ledgers. South America and Africa remain early-stage, but localized vendors such as EVOP and SYNEco are carving niches with e-invoicing connectors to regional tax portals.

- Procore Technologies, Inc.

- Trimble Inc. (Viewpoint Division)

- CMiC Global Inc.

- Sage Group plc

- Jonas Construction Software Inc.

- Foundation Software, LLC

- Buildertrend Solutions, Inc.

- RedTeam Software, LLC

- Penta Technologies, Inc.

- Deltek, Inc.

- B2W Software, Inc.

- Explorer Software Group

- Eque2 Limited

- e-Builder, Inc.

- Projectmates (Systemates, Inc.)

- RIB Software GmbH

- UDA Technologies, Inc.

- Premier Construction Software

- COINS Global Limited

- Acumatica, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Cloud-Based ERP Solutions

- 4.2.2 Increasing Government Infrastructure Spending on Construction

- 4.2.3 Rising Demand for Mobile-First and Remote Collaboration Capabilities

- 4.2.4 Stricter Regulatory Compliance for Construction Accounting and Reporting

- 4.2.5 Emergence of AI-Powered Predictive Modules Reducing Rework

- 4.2.6 Integration of BIM Digital Twin Data with ERP Workflows

- 4.3 Market Restraints

- 4.3.1 High Upfront Implementation and Customization Costs

- 4.3.2 Cybersecurity and Data-Privacy Concerns

- 4.3.3 Legacy Data Migration Complexity

- 4.3.4 Shortage of Skilled Construction-Specific ERP Talent

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Solution

- 5.3.1 Software

- 5.3.2 Services

- 5.4 By End Use

- 5.4.1 Residential Construction

- 5.4.2 Commercial Construction

- 5.4.3 Infrastructure and Civil Engineering

- 5.4.4 Industrial Construction

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Procore Technologies, Inc.

- 6.4.2 Trimble Inc. (Viewpoint Division)

- 6.4.3 CMiC Global Inc.

- 6.4.4 Sage Group plc

- 6.4.5 Jonas Construction Software Inc.

- 6.4.6 Foundation Software, LLC

- 6.4.7 Buildertrend Solutions, Inc.

- 6.4.8 RedTeam Software, LLC

- 6.4.9 Penta Technologies, Inc.

- 6.4.10 Deltek, Inc.

- 6.4.11 B2W Software, Inc.

- 6.4.12 Explorer Software Group

- 6.4.13 Eque2 Limited

- 6.4.14 e-Builder, Inc.

- 6.4.15 Projectmates (Systemates, Inc.)

- 6.4.16 RIB Software GmbH

- 6.4.17 UDA Technologies, Inc.

- 6.4.18 Premier Construction Software

- 6.4.19 COINS Global Limited

- 6.4.20 Acumatica, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment