|

市場調查報告書

商品編碼

2065531

人工智慧驅動的企業培訓:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)AI-Powered Corporate Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

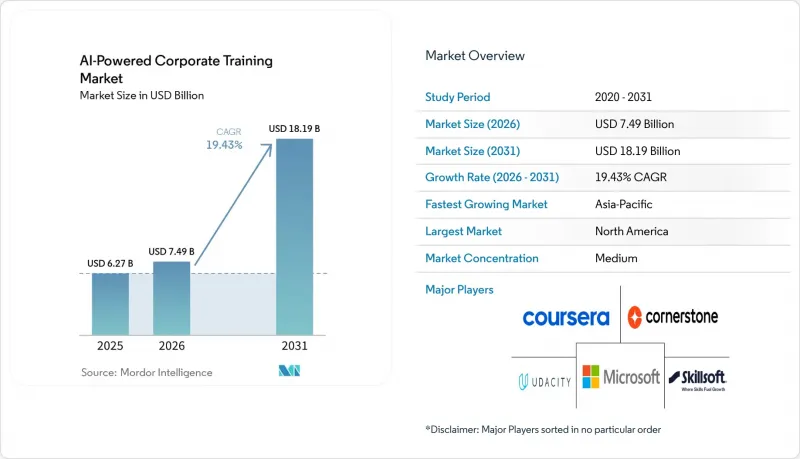

根據 Mordor Intelligence 預測,人工智慧驅動的企業培訓市場規模預計將從 2025 年的 62.7 億美元成長到 2026 年的 74.9 億美元,並將從 2026 年到 2031 年以 19.43% 的複合年成長率成長,到 20319 億美元。

本報告按組件(解決方案、服務)、部署方式(雲端、本地部署、混合部署)、組織規模(大型企業、中小企業)、最終用戶行業(銀行、金融服務和保險等)、學習模式(自主學習、講師主導等)、技術(機器學習等)和地區進行細分。市場預測以美元計價。

全球人工智慧驅動型企業培訓市場趨勢與分析

技能減半週期的快速縮短正在重新定義訓練採購週期。

技術技能生命週期的縮短,尤其是在數位化和資料密集領域,正在重塑人工智慧驅動的企業培訓市場。世界經濟論壇的報告指出,2030年,現有員工技能的39%預計將會改變或過時,63%的雇主認為技能缺口是企業轉型面臨的最大障礙。這降低了年度技能更新培訓的有效性,因為如今職位要求的變化不僅發生在週期之間,而是在業務週期內。因此,人工智慧驅動的企業培訓市場正從靜態目錄形式轉向持續更新的內容、自適應學習路徑以及對工作績效的頻繁檢驗。 2026年發表在《人工智慧前沿》(Frontiers in Artificial Intelligence)上的一項研究指出,技能再培訓疲勞會造成巨大的認知和動力負擔,這意味著平台設計以及內容廣度對於持續推廣至關重要。隨著持續技能再培訓成為一項常規營運支出,能夠逐步更新培訓內容並將其與實際工作場景相結合的供應商將更有利於與企業保持合作關係。

遠距辦公和混合辦公的普及正在推動基礎設施投資。

隨著遠距辦公和混合辦公模式的持續發展,人工智慧驅動的企業培訓市場持續受益。如今,培訓系統需要服務不同地點、時區和使用不同設備的員工。預計到2025年,雲端採用率將佔市場佔有率的78.44%,反映出分散式組織對彈性運算、集中式內容管理和即時數據連接的需求。混合辦公模式帶來的一個不太明顯的影響是,非同步學習使得雇主更難比較不同團隊的實際技能水平。這推動了對更嚴格的基準測試和檢驗的需求。根據Skillsoft的數據顯示,從2024年12月到2025年12月,Percipio平台上與人工智慧相關的「技能基準測試」完成率年增了994%,其中人工智慧內容完成率增加了261%,人工智慧成就徽章獲取率增加了241%。這些趨勢表明,買家不再僅僅滿足於完成率,而是尋求培訓能夠提升實際應對力的證據。人工智慧驅動的企業培訓市場正受益於此轉變。這是因為,將員工績效指標的分發、評估和追蹤結合的平台正變得比獨立的資料庫更重要。

初始整合和內容轉換的高成本延緩了產品的普及。

人工智慧驅動的企業培訓市場仍然面臨著巨大的普及障礙,尤其是在轉換傳統內容和將新系統連接到現有企業軟體所需的成本和精力方面。許多現有課程是為傳統學習模式設計的,通常需要徹底重新設計,而不是進行小幅修改,以實現自適應交付、基於人工智慧的回饋和對話式練習。這種負擔在中小企業 (SME) 領域尤為突出,預計到 2031 年,中小企業將成長 21.93%,因為初始轉換和整合成本可能與軟體本身的價格不相上下。與 Workday、SAP SuccessFactors、Oracle HCM 和身分識別管理工具的整合進一步增加了實施的複雜性,涉及權限、API、管治規則和資料映射等面向。 SAP 的 Learning Compliance Agent 和 Docebo 基於 MCP 的架構表明,供應商正努力透過預先建置連接器和內建自動化功能來緩解這些障礙。然而,在人工智慧驅動的企業培訓市場中,能夠承擔實施過程中所投入精力的買家仍然具有優勢,因此,實施情況的差異比整體需求所顯示的要大。

細分市場分析

到2025年,解決方案將佔據人工智慧驅動的企業培訓市場64.52%的佔有率,證實了平台層仍是企業買家的核心收入來源。該領域涵蓋人工智慧驅動的學習平台、自適應個人化引擎、技能智慧工具、內容生成應用、評估系統、對話助理和身臨其境型培訓環境。買家之所以繼續在解決方案上投入最多,是因為他們尋求的是一個能夠管理整個學習週期中發現、個人化、交付、檢驗和分析的單一營運層。正是由於這一層的深度,即使企業期望越來越注重結果,解決方案仍然能夠維持較大的市場佔有率。在人工智慧驅動的企業培訓市場,解決方案堆疊不再只是數位課程目錄,而是一個追蹤員工學習訊號的「記錄系統」。

平台整合正在進一步加速這一趨勢,各大廠商都在努力將分散的學習功能整合到更廣泛的產品架構中。 2026年4月,Docebo發布了AgentHub,它將技能智慧、企業知識和基於代理的人工智慧整合到一個封閉回路型環境中。 Docebo也推出了MCP Server,讓Docebo能夠作為原生知識庫在Microsoft Copilot等大規模語言模型(LLM)中運作。同時,根據SAP的數據,在2026年4月接受調查的高階主管中,有62%的人對人才數據與績效的關聯方式感到不滿,這推動了對能夠將培訓與業務成果連結起來的分析工具的需求。儘管服務業目前所佔佔有率仍然較小,但預計到2031年,其年均成長率將達到20.27%,因為企業需要內容轉換、模型調優、實施、分析和績效相關的諮詢服務方面的支持。因此,人工智慧驅動的企業培訓市場中服務的重要性日益增加,並非因為軟體的重要性下降,而是因為如果沒有供應商的持續參與,就很難實現大規模部署。

到2025年,雲端將佔據人工智慧驅動的企業培訓市場78.44%的佔有率,這反映了自適應學習、學習生命週期管理(LLM)推理、技能映射和持續資料同步等技術需求。預計到2031年,該細分市場也將以21.42%的年均成長率成長,顯示在這一大規模市場中的領先地位並未放緩其成長動能。隨著企業尋求更快的更新速度、集中管理以及與協作工具和人力資源平台輕鬆整合,雲端仍然是首選方案。雲端還支援個人化學習流程和可衡量的員工準備度所需的即時回饋循環。在人工智慧驅動的企業培訓市場,對於那些優先考慮速度、規模和廣泛員工存取權限的買家而言,雲端現在已成為預設架構。

近期發布的產品證明了這種主導地位得以延續的原因。微軟宣布其學習代理商(Learning Agent)將技能差距分析和個人化學習計畫與 Microsoft 365 Copilot 和 Teams 整合。此模式依賴微軟的雲端環境和內建的生產力套件。同時,在國防、核能和敏感政府機構中,本地部署仍然至關重要,因為資料主權和安全法規可能使雲端 SaaS 方案難以實施。此外,銀行、金融服務、保險和醫療保健產業對混合解決方案的需求也很強勁。這些用戶通常希望利用基於雲端的 AI 功能,同時對高度敏感的記錄進行更嚴格的內部控制。印度、德國和中國等市場對資料居住要求的預期維持了這種平衡,即使雲端的主導地位持續增強,AI 驅動的企業培訓市場也不太可能完全轉向雲端。

區域分析

2025年,北美在人工智慧驅動的企業培訓市場佔據38.74%的佔有率,並持續保持其最大區域收入來源的地位。其中,美國佔據了大部分佔有率,這主要得益於其高密度的科技就業、成熟的企業軟體採購體係以及高度集中的平台供應商和企業買家。儘管加拿大和墨西哥憑藉其不斷發展的技術生態系統以及近岸外包帶來的技能發展需求而獲得成長,但美國仍然是該地區的重心。另一個優勢是學習系統與更廣泛的企業平台深度整合,這使得利用已存儲在HCM和ERP環境中的員工資料輕鬆實現培訓個人化。此外,許多全球供應商在將新的人工智慧學習功能推廣到其他地區之前,都會先在北美地區進行開發和測試,這也促進了北美人工智慧驅動的企業培訓市場的發展。

預計到2031年,亞太地區將以20.58%的年均成長率成長,成為人工智慧企業培訓市場成長最快的區域市場。這一成長主要得益於企業對人工智慧的廣泛應用、大規模的勞動力基礎,以及彌合中國、印度、日本、韓國和整個東協市場技術技能差距的日益成長的壓力。尤其值得一提的是,印度正在推廣一種將人工智慧與人力結合的模式,並將人工智慧能力建構視為一項策略需求,而非一項可以延緩實施的計畫。歐洲是一個關鍵市場,德國、英國和法國是其主要驅動力。在這些國家,合規要求以及直接投資報酬率(ROI)的考量正在塑造對培訓的需求。歐盟的人工智慧法規定,自2025年2月起,人工智慧素養成為一項正式要求,並自2026年8月起擴大了執法範圍。這將導致企業對有據可查的人工智慧培訓的需求更加系統化。根據 Coursera 引用的研究,德國每年因職缺造成的損失估計為 3,390 億歐元(3,830 億美元),凸顯了技能發展投資不足所帶來的宏觀經濟成本。

儘管南美洲仍然是一個相對較小的區域市場,但巴西和阿根廷正崛起為成長迅猛的中心,這得益於其科技業的擴張和跨國公司的湧入,這些都推動了正規人工智慧培訓的普及。在該地區,雲端原生和多語言部署至關重要,因為企業需要盡可能減少實施阻力,為地理位置分散且語言不同的員工提供服務。中東和非洲的情況則更為複雜。波灣合作理事會(GCC)成員國,例如沙烏地阿拉伯和阿拉伯聯合大公國(阿拉伯聯合大公國),正在投資人工智慧人才能力建設,將其作為國家數位化戰略的一部分。在非洲大陸,南非仍是企業培訓最發達的市場,但撒哈拉以南非洲全部區域的普及仍處於起步階段。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 技術職業技能的半衰期很短

- 遠距辦公和混合辦公人員的數量正在迅速增加。

- 企業在個人化學習路徑的支出增加

- 利用LLM整合教練機器人和ERP-HCM數據

- 與內部人才市場關聯的自動化微證書

- 考慮到環境、社會和治理因素,關於持續技能再學習的資訊揭露義務

- 市場限制因素

- 初始整合和內容轉換成本高昂

- 資料隱私和智慧財產權問題

- 使用未經授權的生成式人工智慧工具進行「影子學習」的風險

- 演算法偏見導致的審計正在減慢採購週期。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章:預測市場規模與成長率

- 按組件

- 解決方案

- 人工智慧驅動的學習平台

- 自適應學習與個人化引擎

- 人工智慧技能智慧平台

- AI內容生成工具

- 人工智慧驅動的評估和學習分析

- 互動式人工智慧學習助手

- 身臨其境型人工智慧訓練平台

- 服務

- 解決方案

- 透過部署方法

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- IT/通訊

- 銀行、金融服務和保險業 (BFSI)

- 製造業

- 醫學與生命科學

- 零售與電子商務

- 其他終端用戶產業

- 透過學習模型

- 自學型

- 講師主導

- 混合型

- 透過技術

- 機器學習

- 自然語言處理

- 語音辨識

- 電腦視覺

- 其他新興人工智慧技術

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Coursera, Inc.

- Skillsoft Corporation

- Cornerstone OnDemand, Inc.

- Udacity, Inc.

- SAP SE(Litmos)

- IBM Corporation(SkillsBuild)

- Google LLC(Cloud Learning Services)

- Oracle Corporation

- Pluralsight LLC

- Degreed, Inc.

- Docebo SpA

- OpenSesame Inc.

- EdCast Inc.(upGrad)

- Fuse Universal Ltd.

- 360Learning SA

- Workday, Inc.

- NovoEd, Inc.

- Valamis Group Oy

- CYPHER Learning

- Absorb Software Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the aI-powered corporate training market size is expected to grow from USD 6.27 billion in 2025 to USD 7.49 billion in 2026 and is forecast to reach USD 18.19 billion by 2031 at 19.43% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, and More), Learning Model (Self-Paced, Instructor-Led, and More), Technology (Machine Learning, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Powered Corporate Training Market Trends and Insights

Rapid Skills Half-Life Is Redefining The Training Procurement Cycle

The AI-powered corporate training market is being shaped by the shrinking usable life of technical skills, especially in digital and data-heavy roles. The World Economic Forum reported that 39% of existing workforce skill sets will transform or become outdated by 2030, and 63% of employers identified skill gaps as the biggest barrier to business transformation. This makes annual training refreshes less effective because role requirements are now shifting inside active business cycles rather than between them. The AI-powered corporate training market is therefore moving toward always-on content updates, adaptive pathways, and frequent validation of role readiness instead of static catalogs. A 2026 study in Frontiers in Artificial Intelligence described reskilling fatigue as a real cognitive and motivational burden, which means platform design now matters as much as content breadth for sustained adoption. Vendors that can refresh learning in smaller steps and tie it to real work context are better placed to hold enterprise contracts as continuous reskilling becomes a normal operating expense.

Remote and Hybrid Workforce Proliferation Drives Infrastructure Investment

The AI-powered corporate training market continues to benefit from the lasting shift to remote and hybrid work because training systems now need to serve employees across locations, time zones, and devices. Cloud deployment led with 78.44% share in 2025, which reflects the need for elastic compute, centralized content management, and live data connections across distributed organizations. A less visible effect of hybrid work is that asynchronous learning makes it harder for employers to compare actual skill levels across teams, which raises demand for stronger benchmarking and verifiable credentials. Skillsoft said AI-related Skill Benchmark completions on Percipio rose 994% year over year from December 2024 to December 2025, while AI content completions increased 261% and AI achievement badges rose 241%. Those usage patterns show that buyers are no longer satisfied with completion rates alone and are instead asking for evidence that training improves job readiness. The AI-powered corporate training market is gaining from this shift because platforms that combine delivery, assessment, and workforce signal tracking are becoming more relevant than standalone content libraries.

High Up-Front Integration and Content-Conversion Costs Slow Adoption

The AI-powered corporate training market still faces a meaningful adoption barrier in the cost and effort needed to convert legacy content and connect new systems to existing enterprise software. Much of the installed course base was designed for older learning formats, so adaptive delivery, AI-based feedback, and conversational practice often require full redesign rather than light editing. That burden is especially visible among SMEs, even though the segment is projected to grow at 21.93% through 2031, because upfront conversion and integration work can approach the cost of the software itself. Integration with Workday, SAP SuccessFactors, Oracle HCM, and identity tools adds another layer of implementation complexity around permissions, APIs, governance rules, and data mapping. SAP's Learning Compliance Agent and Docebo's MCP-based architecture both show that vendors are trying to reduce this friction with prebuilt connectors and embedded automation. Even so, the AI-powered corporate training market still favors buyers that can absorb implementation effort, which keeps adoption more uneven than top-line demand might suggest.

Other drivers and restraints analyzed in the detailed report include:

- Rising Enterprise Spend on Personalized Learning Pathways

- LLM-Powered Coaching Bots Integrating With ERP-HCM Data Pipelines

- Data-Privacy and Intellectual-Property Concerns Dampen Platform Confidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 64.52% of the AI-powered corporate training market share in 2025, which confirms that the platform layer remains the core revenue engine for enterprise buyers. This segment covers AI-powered learning platforms, adaptive personalization engines, skills intelligence tools, content generation applications, assessment systems, conversational assistants, and immersive training environments. Buyers continue to spend most heavily on solutions because they want a single operating layer that can manage discovery, personalization, delivery, verification, and analytics across the learning cycle. The depth of this layer also explains why solutions continue to command a larger share, even as enterprise expectations become more outcome-focused. In the AI-powered corporate training market, the solution stack has become the system of record for workforce learning signals rather than a simple catalog of digital courses.

Platform consolidation is reinforcing that position, as leading vendors are trying to unify fragmented learning functions within broader product architectures. Docebo launched AgentHub in April 2026 to connect skills intelligence, enterprise knowledge, and agentic AI within a single closed-loop environment, and it also introduced an MCP Server so Docebo could serve as a native knowledge source within LLMs such as Microsoft Copilot. At the same time, SAP said 62% of C-suite executives surveyed in April 2026 were dissatisfied with the way people data connected to business performance, which strengthens demand for analytics that link training to operating outcomes. Services remain smaller in share, but they are projected to grow at 20.27% through 2031, as enterprises need support with content conversion, model tuning, implementation, analytics, and performance-linked advisory services. The AI-powered corporate training market is therefore seeing services gain importance not because software is losing relevance, but because large deployments are harder to operationalize without ongoing vendor involvement.

Cloud accounted for 78.44% of AI-powered corporate training market size in 2025, which reflects the technical needs of adaptive learning, LLM inference, skills mapping, and continuous data synchronization. The segment is also projected to expand at 21.42% through 2031, which shows that market leadership at scale has not reduced its growth momentum. Cloud remains the preferred route because enterprises want faster updates, centralized administration, and easier integration with collaboration tools and HR platforms. It also supports the real-time feedback loops required for personalized learning journeys and measurable workforce readiness. In the AI-powered corporate training market, cloud is now the default architecture for buyers that prioritize speed, scale, and broad employee access.

Recent product launches show why that advantage persists. Microsoft said its Learning Agent would integrate skill gap analysis and personalized learning plans into Microsoft 365 Copilot and Teams, a model that depends on the company's cloud environment and embedded productivity stack. On-premise deployments still matter in defense, nuclear, and classified government settings because data sovereignty and security rules can make cloud SaaS impractical. Hybrid demand is also holding up in banking, financial services, insurance, and healthcare because these users often want cloud-side AI functionality while keeping sensitive records under tighter internal control. National data residency expectations in markets such as India, Germany, and China are sustaining that balance, which means the AI-powered corporate training market is unlikely to become fully cloud-only even as cloud keeps widening its lead.

Geography Analysis

North America held 38.74% of the AI-powered corporate training market share in 2025, which kept it as the largest regional revenue base. The United States accounted for the bulk of that position because it combines dense technology employment, mature enterprise software procurement, and a strong concentration of platform vendors and enterprise buyers. Canada and Mexico added momentum through growing technology ecosystems and nearshoring-linked upskilling needs, but the regional center of gravity remained in the United States. Another advantage is the depth of integration between learning systems and broader enterprise platforms, which makes it easier to personalize training using workforce data already housed in HCM and ERP environments. The AI-powered corporate training market in North America also benefits from the fact that many global vendors build and test new AI learning features in this region before scaling them elsewhere.

Asia-Pacific is projected to grow at 20.58% through 2031, making it the fastest-growing regional segment in the AI-powered corporate training market size. Growth is being supported by broad enterprise AI adoption, large workforce bases, and increasing pressure to close technical skill gaps across China, India, Japan, South Korea, and ASEAN markets. India stands out because enterprises are moving ahead with AI-human workforce models and treating AI capability building as a strategic requirement rather than a delayed program. Europe remains a significant market led by Germany, the United Kingdom, and France, where compliance requirements are shaping training demand as much as direct return-on-investment logic. The EU AI Act made AI literacy a formal requirement from February 2025 and expanded enforcement obligations from August 2026, which has created a more structured procurement case for documented corporate AI training. Germany's estimated annual cost of unfilled vacancies reached EUR 339 billion (USD 383 billion), in findings cited by Coursera, which underlines the macroeconomic cost of underinvestment in skills development.

South America is still a smaller regional base, but Brazil and Argentina are emerging as practical growth pockets because technology-sector expansion and multinational presence are pushing formal AI training adoption. Cloud-native and multilingual deployments are most relevant there because enterprises often need to serve geographically spread and language-diverse workforces with limited implementation friction. The Middle East and Africa is more uneven, with Gulf Cooperation Council countries such as Saudi Arabia and the United Arab Emirates investing in AI workforce capability as part of national digitalization agendas. South Africa remains the most developed corporate training market on the African continent, while broader sub-Saharan adoption is still at an earlier stage.

- Microsoft Corporation

- Coursera, Inc.

- Skillsoft Corporation

- Cornerstone OnDemand, Inc.

- Udacity, Inc.

- SAP SE (Litmos)

- IBM Corporation (SkillsBuild)

- Google LLC (Cloud Learning Services)

- Oracle Corporation

- Pluralsight LLC

- Degreed, Inc.

- Docebo S.p.A.

- OpenSesame Inc.

- EdCast Inc. (upGrad)

- Fuse Universal Ltd.

- 360Learning SA

- Workday, Inc.

- NovoEd, Inc.

- Valamis Group Oy

- CYPHER Learning

- Absorb Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Skills-half-life in Tech Roles

- 4.2.2 Explosion of Remote Hybrid Workforces

- 4.2.3 Rising Enterprise Spend on Personalized Learning Pathways

- 4.2.4 Integration of LLM-powered Coaching Bots With ERP-HCM Data

- 4.2.5 Auto-generated Micro-credentials Linked to Internal Talent Marketplaces

- 4.2.6 ESG-driven Mandates for Continuous Reskilling Disclosures

- 4.3 Market Restraints

- 4.3.1 High Up-front Integration Content-conversion Costs

- 4.3.2 Data-Privacy Intellectual-Property Concerns

- 4.3.3 'Shadow-learning' Risk From Unsanctioned Gen-AI Tools

- 4.3.4 Algorithmic Bias Audits Delaying Procurement Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 AI-powered Learning Platforms

- 5.1.1.2 Adaptive Learning and Personalization Engines

- 5.1.1.3 AI Skills Intelligence Platforms

- 5.1.1.4 AI Content Generation Tools

- 5.1.1.5 AI Assessment and Learning Analytics

- 5.1.1.6 Conversational AI Learning Assistants

- 5.1.1.7 Immersive AI Training Platforms

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 IT Telecom

- 5.4.2 BFSI

- 5.4.3 Manufacturing

- 5.4.4 Healthcare Life Sciences

- 5.4.5 Retail eCommerce

- 5.4.6 Other End-User Industries

- 5.5 By Learning Model

- 5.5.1 Self-Paced

- 5.5.2 Instructor-Led

- 5.5.3 Blended

- 5.6 By Technology

- 5.6.1 Machine Learning

- 5.6.2 Natural Language Processing

- 5.6.3 Speech an Voice Recognition

- 5.6.4 Computer Vision

- 5.6.5 Other Emerging AI Technology

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 ASEAN

- 5.7.4.6 Australia New Zealand

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of the Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Coursera, Inc.

- 6.4.3 Skillsoft Corporation

- 6.4.4 Cornerstone OnDemand, Inc.

- 6.4.5 Udacity, Inc.

- 6.4.6 SAP SE (Litmos)

- 6.4.7 IBM Corporation (SkillsBuild)

- 6.4.8 Google LLC (Cloud Learning Services)

- 6.4.9 Oracle Corporation

- 6.4.10 Pluralsight LLC

- 6.4.11 Degreed, Inc.

- 6.4.12 Docebo S.p.A.

- 6.4.13 OpenSesame Inc.

- 6.4.14 EdCast Inc. (upGrad)

- 6.4.15 Fuse Universal Ltd.

- 6.4.16 360Learning SA

- 6.4.17 Workday, Inc.

- 6.4.18 NovoEd, Inc.

- 6.4.19 Valamis Group Oy

- 6.4.20 CYPHER Learning

- 6.4.21 Absorb Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球企業培訓市場:機會與策略展望(至2035年)

全球企業培訓市場:機會與策略展望(至2035年) 2034年循環經營模式教育培訓市場預測:按培訓類型、交付方式、經營模式、最終用戶和地區分類的全球分析混合式學習市場預測至2034年-按組成部分、交付方式、部署方式、學習模型、應用、最終用戶和地區分類的全球分析

2034年循環經營模式教育培訓市場預測:按培訓類型、交付方式、經營模式、最終用戶和地區分類的全球分析混合式學習市場預測至2034年-按組成部分、交付方式、部署方式、學習模型、應用、最終用戶和地區分類的全球分析 企業培訓市場規模、佔有率和趨勢分析報告:按組成部分、培訓類型、最終用途、地區和細分市場預測(2026-2033 年)2026年全球跨學科學習市場報告實地考察培訓市場預測至2034年:按服務、學習形式、技能類型、最終用戶和地區分類的全球分析混合式學習解決方案市場預測至2034年-按組件、學習模型、技術、應用、最終用戶和地區分類的全球分析

企業培訓市場規模、佔有率和趨勢分析報告:按組成部分、培訓類型、最終用途、地區和細分市場預測(2026-2033 年)2026年全球跨學科學習市場報告實地考察培訓市場預測至2034年:按服務、學習形式、技能類型、最終用戶和地區分類的全球分析混合式學習解決方案市場預測至2034年-按組件、學習模型、技術、應用、最終用戶和地區分類的全球分析 工業培訓市場:依培訓類型、交付方式、最終用戶產業和地區分類。

工業培訓市場:依培訓類型、交付方式、最終用戶產業和地區分類。 2026-2030年全球企業培訓市場企業內部培訓服務市場:依交付方式及地區分類

2026-2030年全球企業培訓市場企業內部培訓服務市場:依交付方式及地區分類